Problem 1-8A (Concluded)

Part 3—continued

Ander Electric

Statement of Cash Flows

For Month Ended December 31

Cash flows from operating activities

Cash received from customers1 …………………………...

$ 6,200

Cash paid for rent ………………………………………………..

(1,000)

Cash paid for supplies …………………………………………

(800)

Cash paid for utilities …………………………………………..

(540)

Cash paid to employees ……………………………………….

(1,400)

Net cash provided by operating activities ……………..

$ 2,460

Cash flows from investing activities

Purchase of office equipment ……………………………….

(2,530)

Purchase of electrical equipment ………………………….

(4,800)

Net cash used by investing activities ……………………

(7,330)

Cash flows from financing activities

Investments by stockholder …………………………………

65,000

Dividends to stockholder ……………………………………..

(950)

Net cash provided by financing activities ……………..

64,050

Net increase in cash …………………………………………….

$59,180

Cash balance, Dec. 1 ……………………………………………

0

Cash balance, Dec. 31 ………………………………………….

$59,180

1$1,200 + $5,000 = $6,200

Part 4

If the December 1 investment had been $49,000 cash instead of $65,000 and

the $16,000 difference was borrowed by the company from a bank, then:

Problem 1-9A (60 minutes) Parts 1 and 2

Assets

=

Liabilities

+

Equity

Cash

+

Accounts

Receivable

+

Office

Supplies

+

Office

Equipment

+

Building

=

Accounts

Payable

+

Notes

Payable

+

Common

Stock

–

Dividends

+

Reve-

nues

–

Expen-

ses

a.

+$70,000

+

$10,000

+

$80,000

b.

– 20,000

+

$150,000

+

$130,000

Bal.

50,000

+

10,000

+

150,000

=

+

130,000

+

80,000

c.

– 15,000

+

15,000

Bal.

35,000

+

25,000

+

150,000

=

+

130,000

+

80,000

d.

+

$1,200

+

1,700

+ $2,900

Bal.

35,000

+

1,200

+

26,700

+

150,000

=

2,900

+

130,000

+

80,000

e.

– 500

–

$ 500

Bal.

34,500

+

1,200

+

26,700

+

150,000

=

2,900

+

130,000

+

80,000

–

500

f.

+

$2,800

+

$2,800

Bal.

34,500

+

2,800

+

1,200

+

26,700

+

150,000

=

2,900

+

130,000

+

80,000

+

2,800

–

500

g.

+ 4,000

+

4,000

Bal.

38,500

+

2,800

+

1,200

+

26,700

+

150,000

=

2,900

+

130,000

+

80,000

+

6,800

–

500

h.

– 3,275

–

$3,275

Bal.

35,225

+

2,800

+

1,200

+

26,700

+

150,000

=

2,900

+

130,000

+

80,000

–

3,275

+

6,800

–

500

i.

+ 1,800

–

1,800

Bal.

37,025

+

1,000

+

1,200

+

26,700

+

150,000

=

2,900

+

130,000

+

80,000

–

3,275

+

6,800

–

500

j.

– 700

– 700

Bal.

36,325

+

1,000

+

1,200

+

26,700

+

150,000

=

2,200

+

130,000

+

80,000

–

3,275

+

6,800

–

500

k.

– 1,800

–

1,800

Bal.

$34,525

+

$1,000

+

$1,200

+

$26,700

+

$150,000

=

$2,200

+

$130,000

+

$80,000

–

$3,275

+

$6,800

–

$2,300

Problem 1-9A (Concluded)

Part 3

Problem 1-10A (20 minutes)

1. Return on assets equals net income divided by average total assets.

2. Strictly on the amount of sales to consumers, Coca–Cola’s sales of

3. Success in returning net income from the average amount invested is

4. Current performance figures suggest that Coca-Cola yields a marginally

higher return on assets than PepsiCo. Based on this information alone,

we would be better advised to invest in Coca-Cola than PepsiCo.

Financial & Managerial Accounting, 5th Edition

34

Problem 1-11A (15 minutes)

1. Return on assets is net income divided by the average total assets.

2. Return on assets seems satisfactory for the risk involved in the

3. We know that revenues less expenses equal net income. Taking the

revenues and net income numbers for Kyzera we obtain:

4. We know from the accounting equation that total financing (liabilities

Problem 1-12AA (20 minutes)

Case 1 Return: 5% interest or $100/year.

Risk: Very low; it is the risk of the financial institution not

paying interest and principal.

Case 2 Return: Expected winnings from your bet.

Problem 1-13AB (15 minutes)

1.

F

5.

I

2.

I

6.

O

3.

I

7.

O

4.

F

8.

O

Problem 1-14AB (15 minutes)

An organization pursues three major business activities: financing,

investing, and operating.

If financial statements are to be informative about an organization’s

activities, then they will need to report on these three major activities. Also

note that planning is the glue that links and coordinates these three major

activities—it includes the ideas, goals, and strategies of an organization.

Financial & Managerial Accounting, 5th Edition

36

PROBLEM SET B

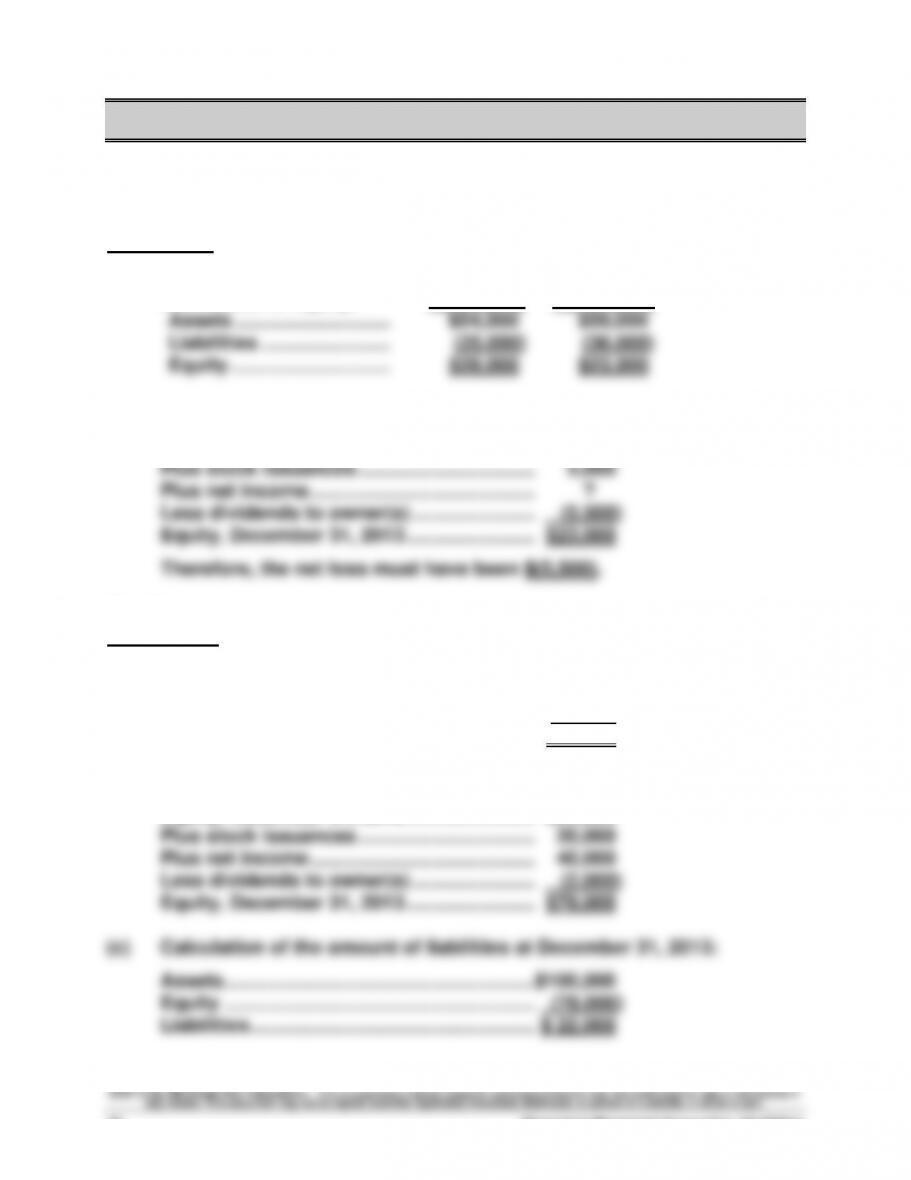

Problem 1-1B (40 minutes)

Part 1

Company V

(a) and (b)

Calculation of equity: 12/31/2012 12/31/2013

Assets ………………………..

$54,000

$59,000

Liabilities ……………………

(25,000)

(36,000)

Equity …………………………

$29,000

$23,000

(c) Calculation of net income for 2013:

Equity, December 31, 2012 …………………… $29,000

Part 2

Company W

(a) Calculation of equity at December 31, 2012:

Assets …………………………………………………. $80,000

Liabilities …………………………………………….. (60,000)

Equity …………………………………………………. $20,000

(b) Calculation of equity at December 31, 2013:

Equity, December 31, 2012 …………………… $20,000

Problem 1-1B (Continued)

Part 3

Company X

First, calculate the beginning and ending equity balances:

12/31/2012 12/31/2013

Assets ………………………..

$141,500

$186,500

Liabilities ……………………

(68,500)

(65,800)

Equity …………………………

$ 73,000

$120,700

Then, find the amount of stock issuances during 2013 as follows:

Equity, December 31, 2012 …………………………. $ 73,000

Plus stock issuances …………………………………. ?

Plus net income …………………………………………. 18,500

Less dividends to owner(s) ………………………… 0

Equity, December 31, 2013 …………………………. $120,700

Thus, the stock issuances must have been … $ 29,200

Part 4

Company Y

First, calculate the beginning balance of equity:

Dec. 31, 2012

Assets …………………………………………………. $92,500

Liabilities …………………………………………….. 51,500

Equity …………………………………………………. $41,000

Next, find the ending balance of equity as follows:

Equity, December 31, 2012 …………………… $41,000

Finally, find the ending amount of assets by adding the ending balance of

equity to the ending balance of liabilities:

Dec. 31, 2013

Financial & Managerial Accounting, 5th Edition

38

Problem 1-1B (Concluded)

Part 5

Company Z

First, calculate the balance of equity as of December 31, 2013:

Next, find the beginning balance of equity as follows:

Thus, the beginning balance of equity is $44,000.

Finally, find the beginning amount of liabilities by subtracting the

beginning balance of equity from the beginning balance of assets:

Dec. 31, 2012

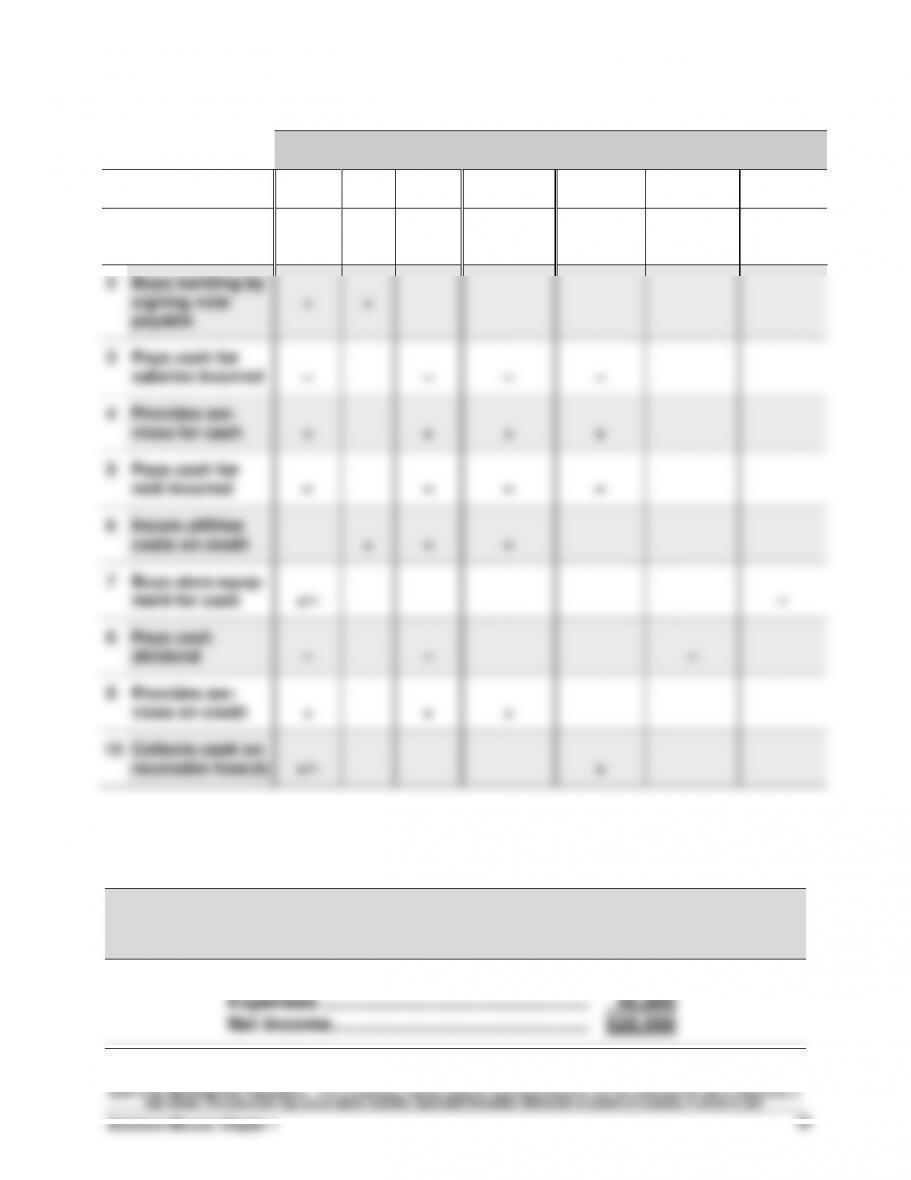

Problem 1-2B (25 minutes)

Balance Sheet

Income

Statement

Statement of

Cash Flows

Transaction

Total

Assets

Total

Liab.

Total

Equity

Net

Income

Operating

Activities

Financing

Activities

Investing

Activities

1

Owner invests

cash for its stock

+

+

+

2

Buys building by

signing note

payable

+

+

3

Pays cash for

salaries incurred

–

–

–

–

4

Provides ser-

vices for cash

+

+

+

+

5

Pays cash for

rent incurred

–

–

–

–

6

Incurs utilities

costs on credit

+

–

–

7

Buys store equip–

ment for cash

+/–

–

8

Pays cash

dividend

–

–

–

9

Provides ser-

vices on credit

+

+

+

10

Collects cash on

receivable from (9)

+/–

+

Problem 1-3B (15 minutes)

Offshore Co.

Income Statement

For Year Ended December 31, 2013

Revenues …………………………………………. $68,000

Financial & Managerial Accounting, 5th Edition

40

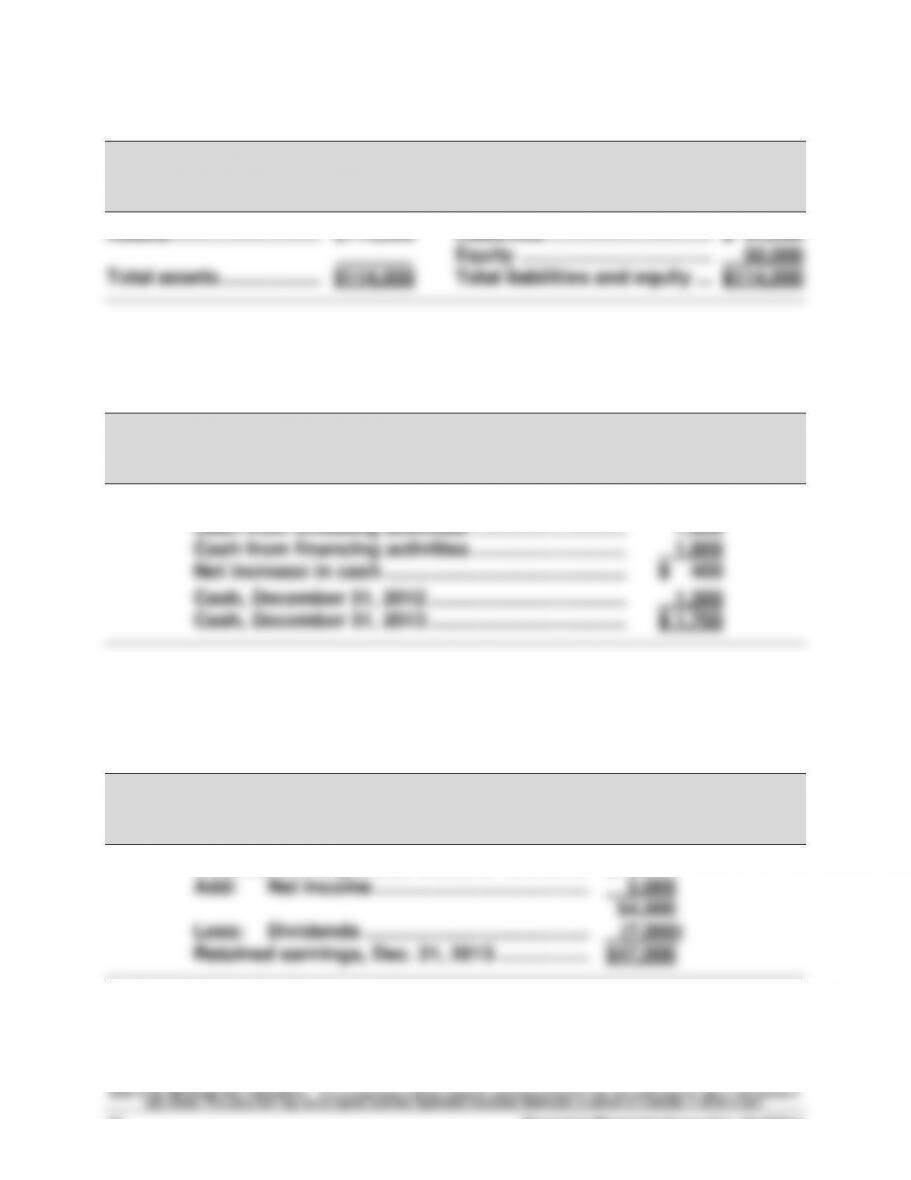

Problem 1-4B (15 minutes)

TLC Company

Balance Sheet

December 31, 2013

Problem 1-5B (15 minutes)

HalfLife Co.

Statement of Cash Flows

For Year Ended December 31, 2013

Cash used by operating activities …………………. $(3,000)

Problem 1-6B (15 minutes)

ATV Company

Statement of Retained Earnings

For Year Ended December 31, 2013

Retained earnings, Dec. 31, 2012 ……………. $49,000

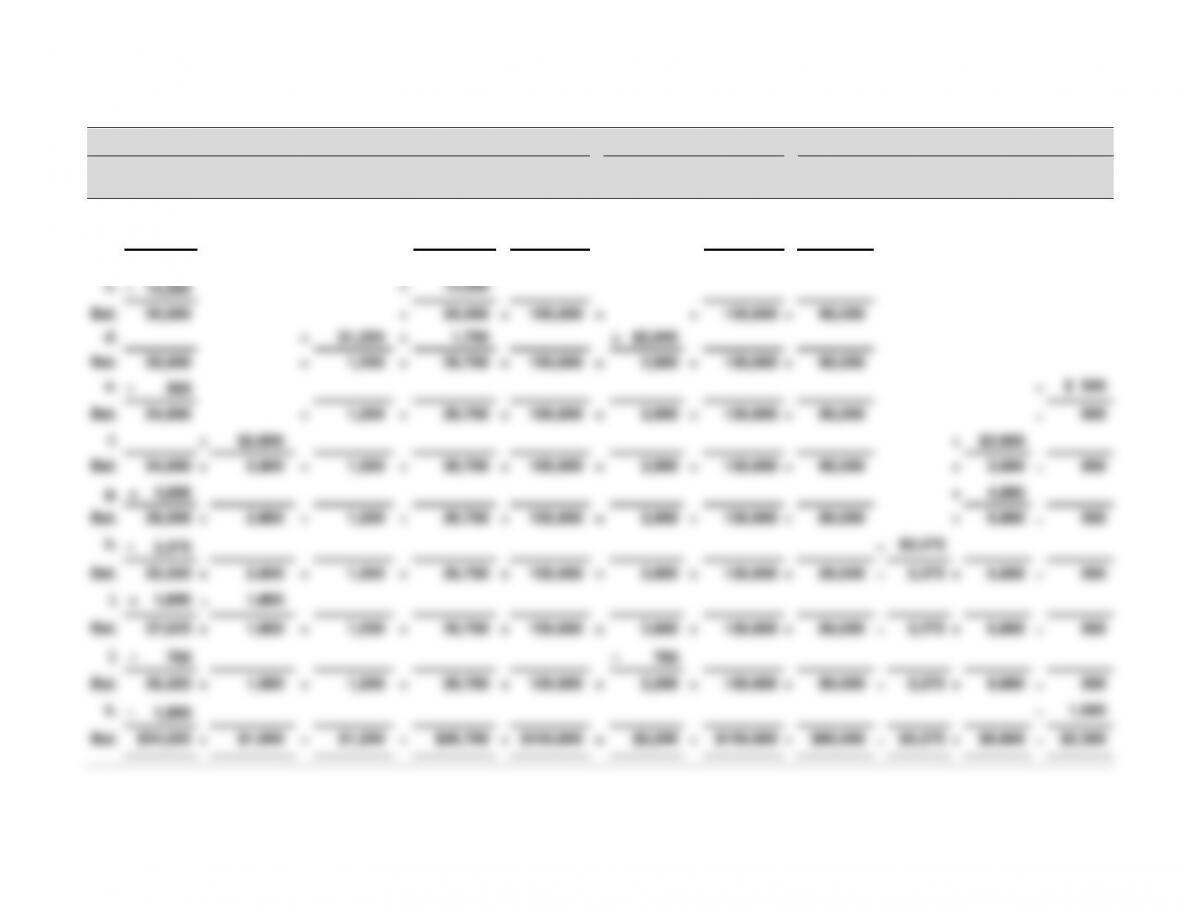

Problem 1-7B (60 minutes) Parts 1 and 2

Assets

=

Liabilities

+

Equity

Date

Cash

+

Accounts

Receivable

+

Equipment

=

Accounts

Payable

+

Common

Stock

–

Dividends

+

Revenues

–

Expenses

June

1

+$130,000

=

+

$130,000

2

– 6,000

=

–

$6,000

4

+

$2,400

=

+ $2,400

6

– 1,150

=

–

1,150

8

+ 850

=

+

$ 850

14

+

$7,500

=

+

7,500

16

– 800

=

–

800

20

+ 7,500

–

7,500

=

21

+

7,900

=

+

7,900

24

+

675

=

+

675

25

+ 7,900

–

7,900

=

26

– 2,400

=

– 2,400

28

– 800

=

–

800

29

– 4,000

=

–

$4,000

30

– 150

=

–

150

30

– 890

=

–

890

$130,060

+

$ 675

+

$2,400

=

$ 0

+

$130,000

–

$4,000

+

$16,925

–

$9,790

Financial & Managerial Accounting, 5th Edition

42

Problem 1-7B (Continued)

Part 3

Holly’s Maintenance Co.

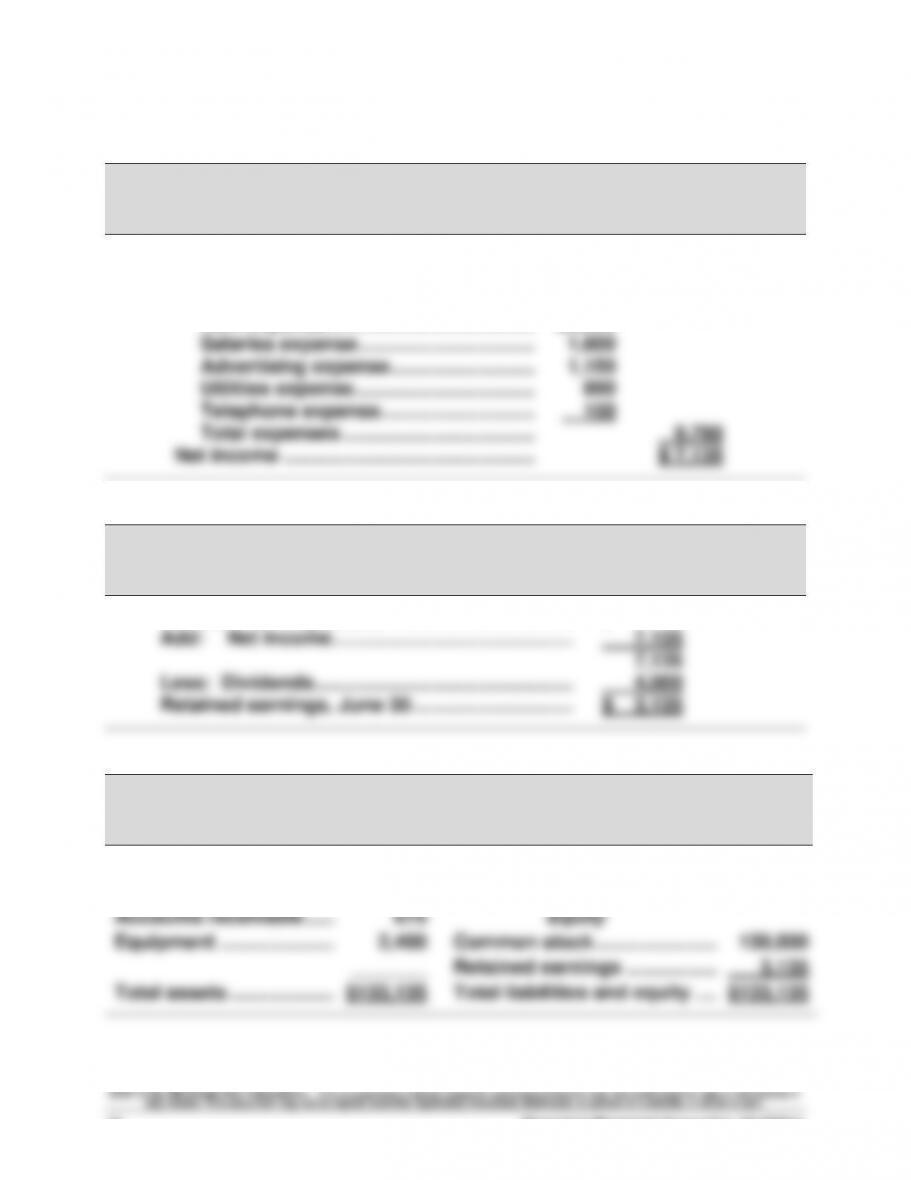

Income Statement

For Month Ended June 30

Revenues

Maintenance services revenue ………. $16,925

Expenses

Rent expense ………………………………… $6,000

Holly’s Maintenance Co.

Statement of Retained Earnings

For Month Ended June 30

Retained earnings, June 1 ………………………….. $ 0

Holly’s Maintenance Co.

Balance Sheet

June 30

Assets

Liabilities

Cash …………………………..

$130,060

Accounts payable ……………………..

$ 0

Accounts receivable ……..

675

Equity

Equipment …………………...

2,400

Common stock …………………..……..

130,000

_______

Retained earnings ……………..……..

3,135

Total assets ………………....

$133,135

Total liabilities and equity …………….

$133,135

Problem 1-7B (Concluded)

Part 3—continued

Holly’s Maintenance Co.

Statement of Cash Flows

For Month Ended June 30

Cash flows from operating activities

Cash received from customers1 …………………………...

$ 16,250

Cash paid for rent ………………………………………………..

(6,000)

Cash paid for advertising …………………………..…………

(1,150)

Cash paid for telephone ……………………………………….

(150)

Cash paid for utilities …………………………………………..

(890)

Cash paid to employees …………………………..…………..

(1,600)

Net cash provided by operating activities ……………..

$ 6,460

Cash flows from investing activities

Purchase of equipment ………………………………………..

(2,400)

Net cash used by investing activities ……………………

(2,400)

Cash flows from financing activities

Investments by stockholder …………………………………

130,000

Dividends to stockholder …………………………..…………

(4,000)

Net cash provided by financing activities ……………..

126,000

Net increase in cash …………………………………………….

$130,060

Cash balance, June 1 …………………………………………..

0

Cash balance, June 30 …………………………………………

$130,060

1$850 + $7,500 + $7,900 = $16,250