Chapter 1

Introducing Accounting in Business

QUESTIONS

1. The purpose of accounting is to provide decision makers with relevant and reliable

2. Technology reduces the time, effort, and cost of recordkeeping. There is still a

demand for people who can design accounting systems, supervise their operation,

3. External users and their uses of accounting information include: (a) lenders, to

measure the risk and return of loans; (b) shareholders, to assess whether to buy,

4. Business owners and managers use accounting information to help answer

5. Service businesses include: Standard and Poor’s, Dun & Bradstreet, Merrill Lynch,

6. The internal role of accounting is to serve the organization’s internal operating

7. Accounting professionals offer many services including auditing, management

8. Marketing managers are likely interested in information such as sales volume,

Financial & Managerial Accounting, 5th Edition

2

9. Accounting is described as a service activity because it serves decision makers by

10. Some accounting-related professions include consultant, financial analyst,

11. Ethics rules require that auditors avoid auditing clients in which they have a direct

12. In addition to preparing tax returns, tax accountants help companies and individuals

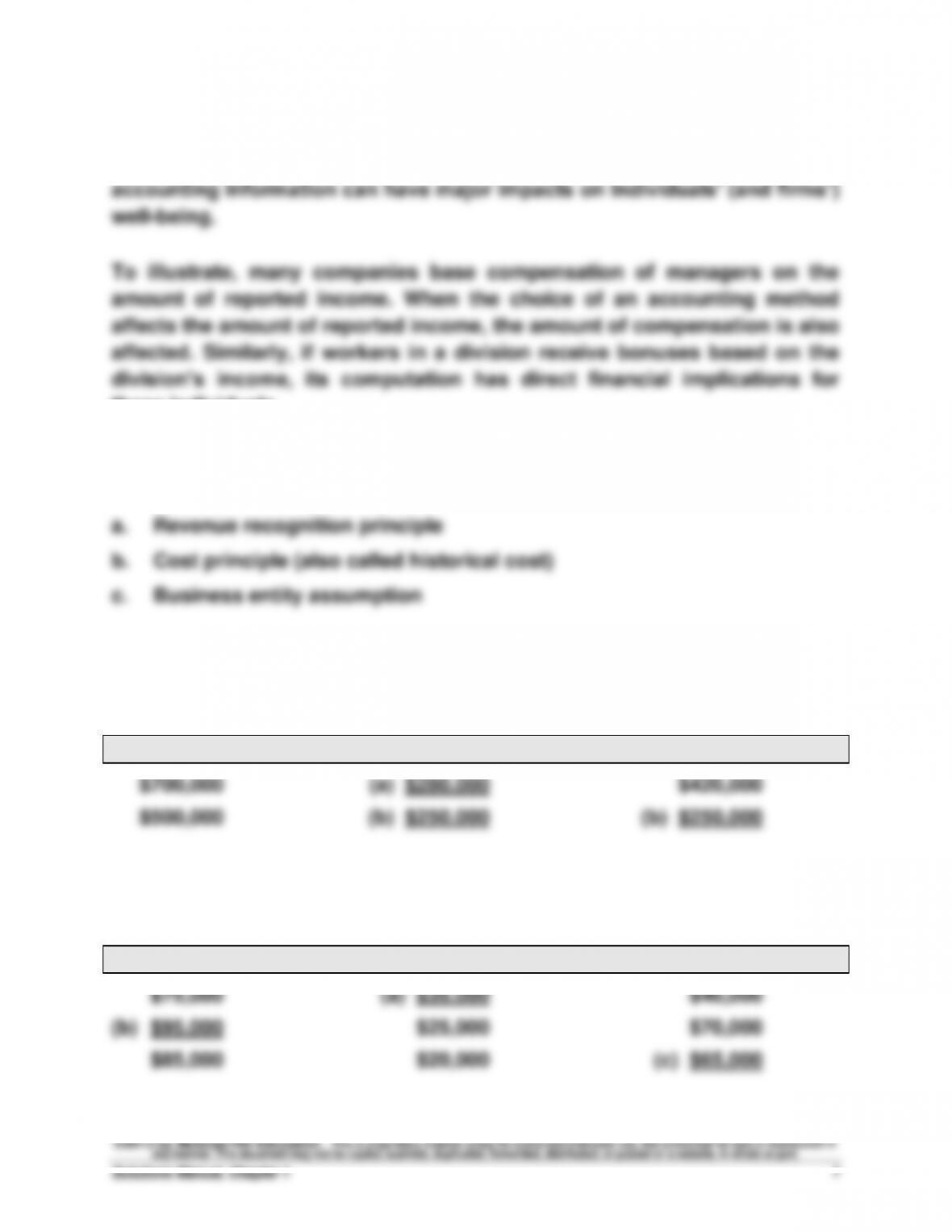

13. The objectivity concept means that financial statement information is supported by

14. This treatment is justified by both the cost principle and the going–concern

15. The revenue recognition principle provides guidance for managers and auditors so

they know when to recognize revenue. If revenue is recognized too early, the

16. Business organizations can be organized in one of three basic forms: sole

proprietorship, partnership, or corporation. These forms have implications for legal

liability, taxation, continuity, number of owners, and legal status as follows:

Proprietorship Partnership Corporation

Business entity yes yes yes

*Proprietorships and partnerships that are set up as LLCs provide limited liability.

17. (a) Assets are resources owned or controlled by a company that are expected to

18. Equity is increased by investments from the stockholder(s) and by net income

19. Accounting principles consist of (a) general and (b) specific principles. General

principles are the basic assumptions, concepts, and guidelines for preparing

20. Revenue (or sales) is the amount received from selling products and services.

21. Net income (also called income, profit or earnings) equals revenues minus expenses

22. The four basic financial statements are: income statement, statement of retained

23. An income statement reports a company’s revenues and expenses along with the

24. Rent expense, utilities expense, administrative expenses, advertising and promotion

25. The statement of retained earnings explains the changes in retained earnings from

26. The balance sheet describes a company’s financial position (types and amounts of

27. The statement of cash flows reports on the cash inflows and outflows from a

28. Return on assets, also called return on investment, is a profitability measure that is

29A. Return refers to income, and risk is the uncertainty about the return we expect to

30B. Organizations carry out three major activities: financing, investing, and operating.

Financing provides the means used to pay for resources. Investing refers to the

Financial & Managerial Accounting, 5th Edition

4

31B. An organization’s financing activities (liabilities and equity) pay for investing

activities (assets). An organization cannot have more or less assets than its

32. The dollar amounts in Polaris’s financial statements are rounded to the nearest

33. At March 31, 2011, Arctic Cat had ($ in thousands) assets of $272,906, liabilities of

34. Confirmation of KTM’s accounting equation follows (numbers in EUR thousands):

Assets

=

Liabilities

+

Equity

485,775

=

266,000

+

219,775

35. The independent auditor for Polaris, is Ernst & Young, LLP. The auditor expressly

QUICK STUDIES

Quick Study 1-1

(a) and (b)

GAAP: Generally Accepted Accounting Principles

SEC delegates part of this responsibility to the FASB.

FASB: Financial Accounting Standards Board

Importance: FASB is an independent group of full-time members who are

responsible for setting accounting rules.

IASB: International Accounting Standards Board.

Importance: A global set of accounting standards issued by the IASB.

Many countries require or permit companies to comply with

IFRS in preparing their financial statements. The FASB is

undergoing a process with the IASB to converge GAAP and

IFRS and to create a single set of accounting standards for

global use.

Quick Study 1-2

a.

E

g.

E

b.

E

h.

E

c.

E

i.

I

d.

E

j.

E

e.

I

k.

E

f.

E

l.

I

Financial & Managerial Accounting, 5th Edition

6

Quick Study 1-3

Internal controls serve several purposes:

• They involve monitoring an organization’s activities to promote

cameras, security guards, and many others.

Quick Study 1-4

Accounting professionals practice in at least four main areas. These four

areas, along with a listing of some work opportunities in each, are:

1. Financial accounting

• Preparation

2. Managerial accounting

• Cost accounting

3. Tax accounting

• Preparation

4. Accounting-related

• Lending

Quick Study 1-5

The choice of an accounting method when more than one alternative

method is acceptable often has ethical implications. This is because

these individuals.

Quick Study 1-6

Quick Study 1-7

Assets = Liabilities + Equity

Quick Study 1-8

Assets = Liabilities + Equity

Financial & Managerial Accounting, 5th Edition

8

Quick Study 1-9

(a) Examples of business transactions that are measurable include:

• Selling products and services.

(b) Examples of business events that are measurable include:

• Decreases in the value of securities (assets).

Quick Study 1-10

a. For December 31, 2011, the account and its dollar amount (in

thousands) for Polaris are:

(1)

Assets

=

$1,228,024

(2)

Liabilities

=

$ 727,968

(3)

Equity

=

$ 500,056

b. Using Polaris’s amounts from (a) we verify that (in millions):

Assets

=

Liabilities

+

Equity

$1,228,024

=

$ 727,968

+

$ 500,056

Quick Study 1-11

[Code: Income statement (I), Balance sheet (B), Statement of retained earnings (E), or

Statement of cash flows (CF).]

*The more advanced student might know that this item would also appear on the CF, which is an acceptable

answer.

Quick Study 1-12

Quick Study 1-13 (10 minutes)

a. International Financial Reporting Standards (IFRS)

Financial & Managerial Accounting, 5th Edition

10

EXERCISES

Exercise 1-1 (10 minutes)

1.

A

5.

C

2.

B

6.

C

3.

A

7.

B

4.

A

8.

B

Exercise 1-2 (10 minutes)

Exercise 1-3 (20 minutes)

Part A.

1.

I

5.

I

2.

I

6.

E

3.

E

7.

I

4.

E

8.

I

Part B.

1.

I

5.

I

2.

E

6.

E

3.

I

7.

I

4.

E

Exercise 1-4 (20 minutes)

a. Situations involving ethical decision making in coursework include

performing independent work on examinations and individually

b. Managers face several situations demanding ethical decision making

c. Accounting professionals who prepare tax returns can face situations

d. Auditing professionals with competing audit clients are likely to learn

Financial & Managerial Accounting, 5th Edition

12

Exercise 1-5 (10 minutes)

Code

Description

Principle/Assumption

E

1.

Usually created by a pronouncement from an

authoritative body.

Specific accounting

principle

G

2.

Financial statements reflect the assumption that

the business continues operating.

Going-concern

assumption

A

3.

Derived from long-used and generally accepted

accounting practices.

General accounting

principle

C

4.

Every business is accounted for separately from

its owner or owners.

Business entity

assumption

D

5.

Revenue is recorded only when the earnings

process is complete.

Revenue recognition

principle

B

6.

Information is based on actual costs incurred in

transactions.

Cost principle

F

7.

A company records the expenses incurred to

generate the revenues reported.

Matching (expense

recognition) principle

H.

8.

A company reports details behind financial

statements that would impact users’ decisions.

Full disclosure

principle

Exercise 1-6 (10 minutes)

1.

4.

2.

5.

D

Exercise 1-7 (10 minutes)

a.

Corporation

e.

Sole proprietorship

b.

Sole proprietorship

f.

Sole proprietorship

c.

Corporation

g.

Corporation

d.

Partnership

Exercise 1-8 (20 minutes)

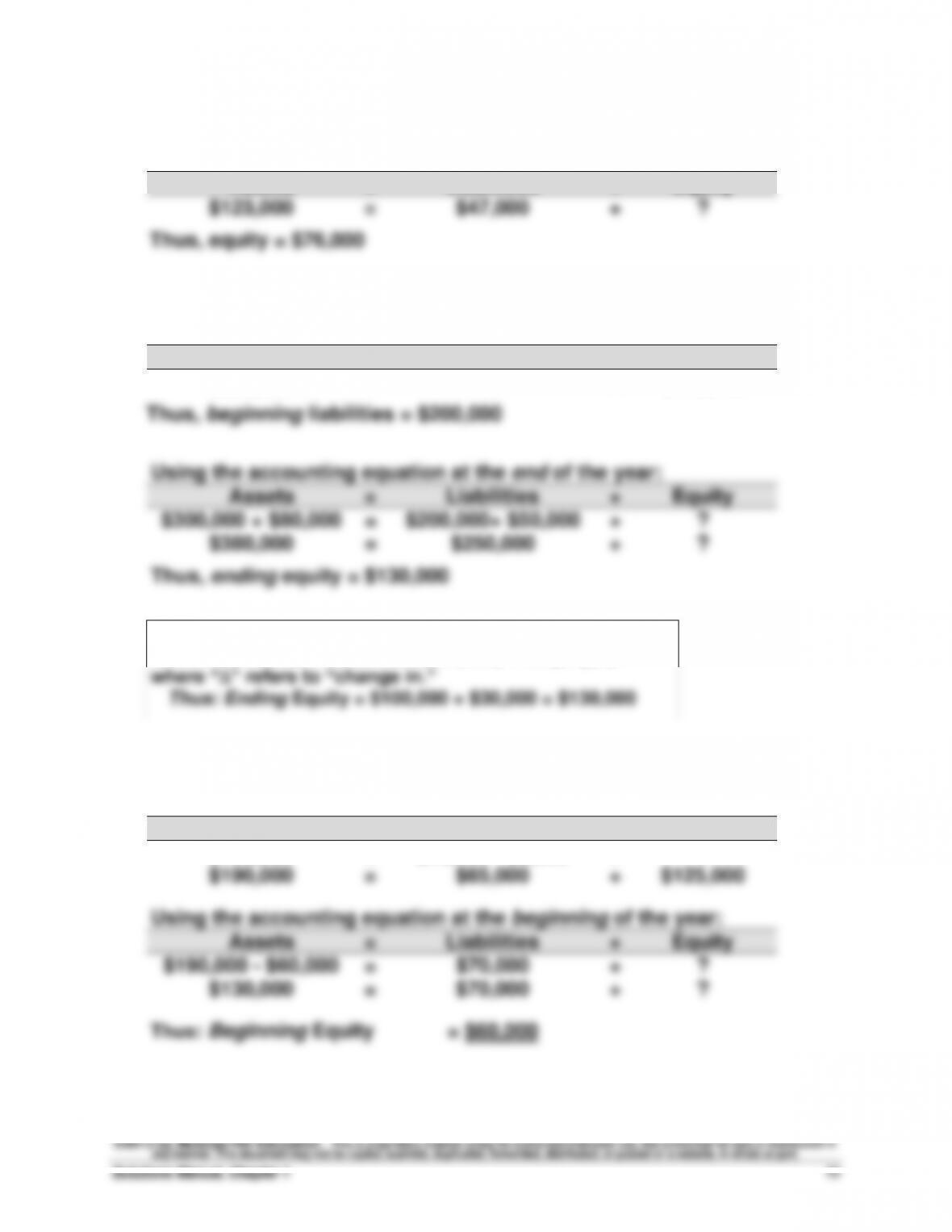

a. Using the accounting equation:

Assets

=

Liabilities

+

Equity

$123,000

=

$47,000

+

?

b. Using the accounting equation at the beginning of the year:

Assets

=

Liabilities

+

Equity

$300,000

=

?

+

$100,000

Assets

=

Liabilities

+

Equity

$300,000 + $80,000

=

$200,000+ $50,000

+

?

$380,000

=

$250,000

+

?

Alternative approach to solving part (b):

Assets($80,000) = Liabilities($50,000) + Equity(?)

c. Using the accounting equation at the end of the year:

Assets

=

Liabilities

+

Equity

$190,000

=

$70,000 – $5,000

+

?

$190,000

=

$65,000

+

$125,000

Assets

=

Liabilities

+

Equity

$190,000 – $60,000

=

$70,000

+

?

$130,000

=

$70,000

+

?

Financial & Managerial Accounting, 5th Edition

14

Exercise 1-9 (10 minutes)

Assets

=

Liabilities

+

Equity

(a) $ 65,000

=

$ 20,000

+

$45,000

$100,000

=

$ 34,000

+

(b) $66,000

$154,000

=

(c) $114,000

+

$40,000

Exercise 1-10 (15 minutes)

Examples of transactions that fit each case include:

a. Cash dividends (or some other asset) paid to the stockholder(s) of the

business; OR, the business incurs an expense paid in cash.

f. Business incurs an expense that is not yet paid (for example, when

employees earn wages that are not yet paid).

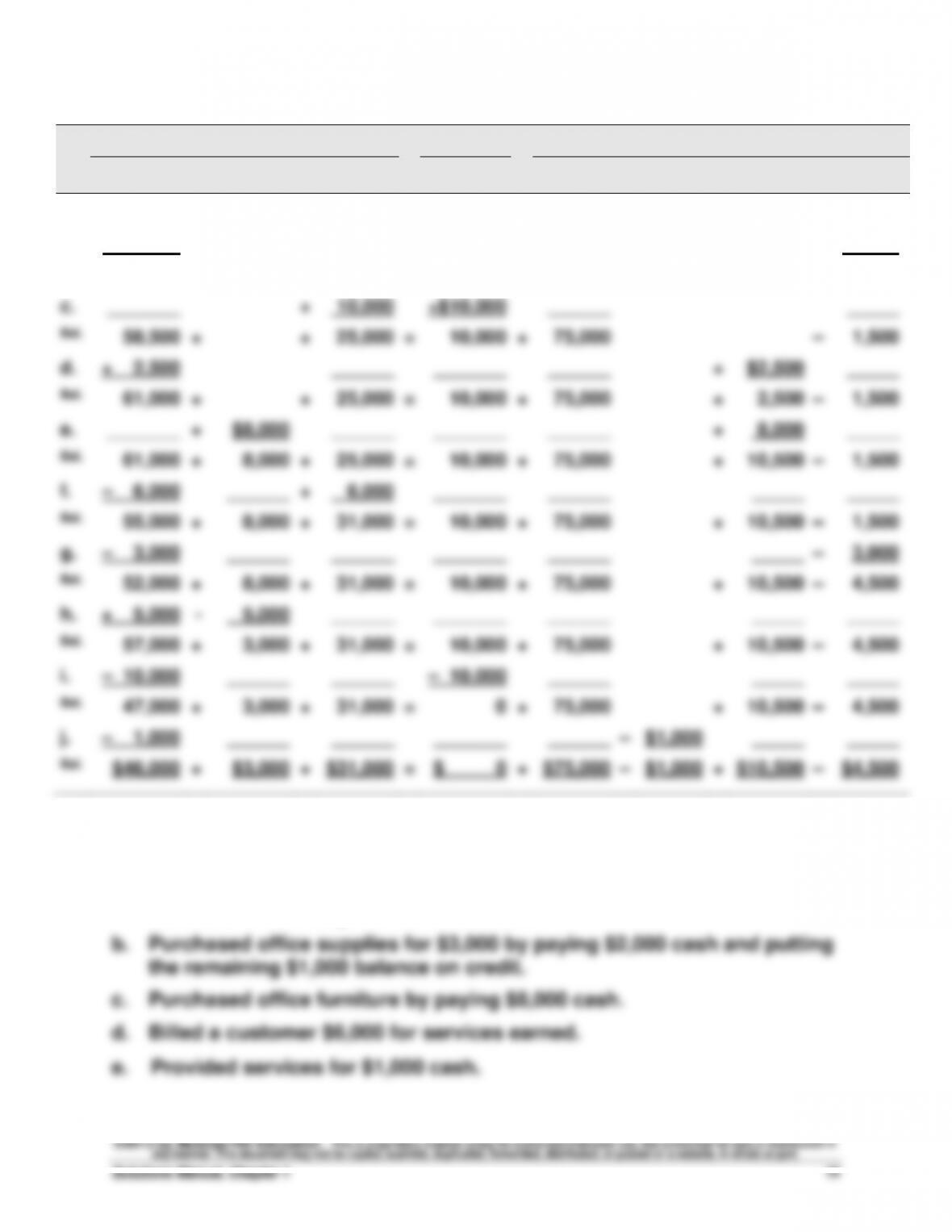

Exercise 1-11 (30 minutes)

Assets

=

Liabilities

+

Equity

Cash

+

Accounts

Receivable

+

Equip-

ment

=

Accounts

Payable

+

Common

Stock

–

Dividends

+

Revenues

–

Expenses

a.

+$60,000

+

$15,000

=

+

$75,000

b.

– 1,500

______

______

–

$1,500

Bal.

58,500

+

+

15,000

=

+

75,000

–

1,500

c.

_______

+

10,000

+$10,000

______

_____

Bal.

58,500

+

+

25,000

=

10,000

+

75,000

–

1,500

d.

+ 2,500

______

_______

______

+

$2,500

_____

Bal.

61,000

+

+

25,000

=

10,000

+

75,000

+

2,500

–

1,500

e.

_______

+

$8,000

______

_______

______

+

8,000

_____

Bal.

61,000

+

8,000

+

25,000

=

10,000

+

75,000

+

10,500

–

1,500

f.

– 6,000

______

+

6,000

_______

______

_____

_____

Bal.

55,000

+

8,000

+

31,000

=

10,000

+

75,000

+

10,500

–

1,500

g.

– 3,000

______

______

_______

______

_____

–

3,000

Bal.

52,000

+

8,000

+

31,000

=

10,000

+

75,000

+

10,500

–

4,500

h.

+ 5,000

–

5,000

______

_______

______

_____

_____

Bal.

57,000

+

3,000

+

31,000

=

10,000

+

75,000

+

10,500

–

4,500

i.

– 10,000

______

______

– 10,000

______

_____

_____

Bal.

47,000

+

3,000

+

31,000

=

0

+

75,000

+

10,500

–

4,500

j.

– 1,000

______

______

_______

______

–

$1,000

_____

_____

Bal.

$46,000

+

$3,000

+

$31,000

=

$ 0

+

$75,000

–

$1,000

+

$10,500

–

$4,500

Exercise 1-12 (20 minutes)

a. Started the business with the owner investing $40,000 cash in the

business in exchange for common stock.