Chapter 01 – Introducing Accounting in Business

Chapter 01

Introducing Accounting in Business

Student Learning Objectives and Related Assignment Materials*

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems**

(A & B set)

Beyond the

Numbers

Conceptual objectives:

C1. Explain the purpose and

importance of accounting.

1, 2, 6, 9

1-1, 1-3

1-2, 1-6

TIA

C2. Identify users and uses of, and

opportunities in accounting.

3, 4, 5, 7, 8,

10, 12, 35

1-2, 1-4

1-1, 1-3, 1-6

CIP, HTR

C3. Explain why ethics are crucial

to accounting.

11

1-5

1-4, 1-6

EC

C4. Explain generally accepted

accounting principles, and

define and apply several

accounting principles.

13, 14, 15,

19

1-6, 1-13

1-5, 1-7

1-7, 1-8, 1-9

EC

C5. Identify and describe the three

major activities of

organizations. (Appendix 1B)

16, 30, 31

1-20

1-13, 1-14

Analytical objectives:

A1. Define and interpret the

accounting equation and each of

its components.

17, 18, 20,

21

1-7, 1-8

1-8, 1-9

1-1, 1-2, 1-9,

1-11

RIA, CA,

CIP, ED, GD

A2. Compute and interpret return

on assets.

1-12

1-18

1-10, 1-11

RIA, CA,

TTN, GD

A3. Explain the relation between

return and risk. (Appendix 1A)

28, 29

1-12

RIA, CA,

GD

Procedural objectives:

P1. Analyze business transactions

using the accounting equation.

1-9, 1-10

1-8, 1-10,

1-11, 1-12,

1-13

1-1, 1-2, 1-7,

1-8, 1-9

ED

P2. Identify and prepare basic

financial statements and explain

how they interrelate.

22, 23, 24,

25, 26, 27,

32, 33, 34

1-11

1-14, 1-15,

1-16, 1-17,

1-19, 1-21

1-3, 1-4, 1-5,

1-6, 1-7, 1-8,

1-9

Notes appear on next page.

Chapter 01 – Introducing Accounting in Business

a website, in whole or part. 1-2

* Assignment materials that can be completed by students using:

Sage50 and QuickBooks Pro 2013 templates – None.

Excel templates – Problems 1-7A, 1-8A.

McGraw-Hill’s Connect – All of the Quick Studies, all of the Exercises, and Problems in set A.

** The Serial Problem for Success Systems, which covers numerous learning objectives, can be

most of the chapters. Even if previous segments are not assigned, students can begin the problem

in any chapter. It is most readily solved if students use the Working Papers that accompany the

book.).

Synopsis of Chapter Revisions

• Twitter: NEW opener with new entrepreneurial assignment

• Streamlined and reorganized discussion of the users of accounting information

• Updated salary information and added more margin notes on the value of education

• New presentation on the ‘fraud triangle’ and its relevance to accounting and internal

control

• New discussion on the joint role of the FASB and IASB in standard setting

• Revised layout for accounting principles and assumptions

• New information on the Dodd-Frank act and its relevance to accounting and users

• New survey data from executives on the impact of fraud in our economic downturn

• New world map on the adoption of IFRS or some variant of IFRS across countries

• New company (Dell) for the return on assets section of Decision Analysis

PowerPoint® Slides

Chapter Learning Objective

PowerPoint® Slides

C1

6-7

C2

8-11

C3

12-13

C4

14-18

A1

19-23

P1

24-34

P2

35-39

A2

40

Chapter 01 – Introducing Accounting in Business

Chapter Outline

Notes

I. Importance of Accounting

Accounting is an information and measurement system that identifies,

records and communicates relevant, reliable, and comparable

information about an organization’s business activities.

Recordkeeping, or bookkeeping, which includes just one function of

accounting, is the recording of transactions and events, either

manually or electronically. Technology is a key part of modern

business and has changed the way we store, process, and summarize

large masses of data. Technology has allowed accounting to expand

to include consulting, planning and other financial services.

A. Users of Accounting Information

Accounting is the language of business because all organizations

set up an accounting information system to communicate data to

help people make better decisions.

1. External information users are not directly involved in

running the organization; they include shareholders, lenders,

directors, customers, suppliers, regulators, lawyers, brokers,

and the press. External users have limited access to an

organization’s information but they must receive information

that is relevant, reliable and comparable. Financial

accounting is the area of accounting aimed at serving external

users by providing them with general-purpose financial

statements.

2. Internal information users are those directly involved in

managing and operating an organization. They use the

information to help improve the efficiency and effectiveness

of an organization. Managerial accounting is the area of

accounting that serves the decision-making needs of internal

users. Internal users and the information they require include:

a. Research and development managers need data on current

and projected costs and revenues to decide whether to

pursue or continue research and development projects.

b. Purchasing managers need data on quality and quantity of

merchandise and materials purchases.

c. Human resource managers need data on current payroll

costs, employee benefits, performance and compensation.

d. Production managers need data on costs and quality of

production processes.

e. Distribution managers need data on quantity and delivery

schedules.

f. Marketing managers need data on sales and costs to

effectively target consumers and set prices.

Chapter 01 – Introducing Accounting in Business

Chapter Outline

Notes

g. Service managers need data on warranties and

maintenance information to provide a valuable product to

its customers.

B. Opportunities in Accounting

1. The four broad areas of opportunities in accounting include

financial accounting, managerial accounting, taxation, and

accounting-related careers.

2. The majority of opportunities are in private accounting as

employees working for businesses. Public accounting

providing services such as auditing and tax advice to

businesses, offers the next largest number of opportunities

while still other opportunities exist in government and not-for-

profit agencies, including business regulation and

investigation of law violations.

3. The professional standing of accounting specialists are

denoted by a certificate such as certified public accountant

(CPA), certified management accountant (CMA), certified

internal auditor (CIA), certified bookkeeper (CB), certified

payroll professional (CPP), personal financial specialist (PFS),

certified fraud examiner (CFE) and certified forensic

accountant (CrFA).

II. Fundamentals of Accounting

A. Ethics – A Key Concept

Ethics are beliefs that distinguish right from wrong; they are

accepted standards of good and bad behavior.

1. Ethical behavior is important in all successful organizations.

Users must be able to trust accounting information. Good

ethics are good business.

2. The AICPA and IMA have set up ethical codes of conduct.

B. Fraud Triangle

1. The fraud triangle asserts that three factors must exist for a

person to commit fraud: opportunity, pressure, and

rationalization.

2. Both internal and external users rely on internal controls to

reduce the likelihood of fraud. Internal controls are

procedures designed to protect company property, ensure

reliable reports, promote efficiency, and encourage adherence

to company policies.

C. Generally Accepted Accounting Principles

Financial accounting is governed by rules known as generally

accepted accounting principles, GAAP. GAAP aims to make

accounting information relevant, reliable and comparable. The

Securities and Exchange Commission (SEC) has legal authority to

set GAAP.

Chapter 01 – Introducing Accounting in Business

Chapter Outline

Notes

1. Setting Accounting Principles

a. The SEC has delegated the task of setting GAAP to the

Financial Accounting Standards Board (FASB), a private

group that sets both broad and specific principles.

D. International Standards. The International Accounting

Standards Board (IASB) issues International Financial Reporting

Standards (IFRS) that identify preferred accounting practices. The

FASB and IASB are pursuing a convergence process aimed to

achieve a single-set of accounting standards for global use.

Currently, there are two sets of accepted accounting principles in the

U.S.: U.S. GAAP for U.S. SEC registrants and IFRS for non-U.S.

SEC registrants. FASB will begin to incorporate IFRS standards into

U.S. GAAP over a period of 5 years or so.

E. Conceptual Framework and Convergence. The FASB and IASB

are attempting to converge the conceptual framework. The

framework consists of:

Objectives – providing useful information to investors,

creditors, and others.

Qualitative Characteristics – requires that information be

relevant, reliable, and comparable.

Elements – defines items that financial statements can

contain.

Recognition and Measurement – sets criteria that an item

must meet for it to be recognized as an element, and how to

measure that element.

1. Principles and Assumptions of Accounting

Accounting principles (and assumptions) are both general (basic

assumptions, concepts and guidelines for preparing financial

statements) and specific (detailed rules used in reporting

transactions). The principles, assumptions and constraints

discussed in this chapter are:

a. Measurement principle or Cost principle—accounting

information is based on actual costs incurred in business

Chapter 01 – Introducing Accounting in Business

Chapter Outline

Notes

f. Monetary unit assumption—transactions and events are

expressed in monetary, or money, units (generally the

currency of the country in which the business operates).

g. Time period assumption—presumes that the life of a

company can be divided into time periods and that useful

reports can be prepared for those periods.

h. Business entity assumption—a business is accounted for

separately and distinctly from its owner(s). A business

entity can take one of three legal forms:

i. Sole proprietorship is a business owned by one person

that has unlimited liability. Requires no special legal

requirements. The business is not subject to an income

tax but the owner is responsible for personal income tax

on the net income of the entity.

ii. Partnership is a business owned by two or more people,

called partners, who are subject to unlimited liability. No

special legal requirements must be met. The only

requirement is an oral or written agreement between the

partners which usually outlines how profits and losses

are to be shared. The business is not subject to an

income tax, but the owners are responsible for personal

income tax on their individual share of the net income of

the entity.

iii. Corporation is a business that is a separate legal entity

whose owners are called shareholders or stockholders.

These owners have limited liability because the business

dividends.

i. Accounting Constraints – the two constraints include

Materiality constraint – only information that would

influence the decisions of a reasonable person need be

disclosed and

more transparency, accountability and truthfulness in reporting

transactions. Auditors also must verify the effectiveness of internal

controls.

G. Dodd-Frank – is an act which promotes accountability and

transparency in the financial system, attempts to end the notion of

Chapter 01 – Introducing Accounting in Business

Chapter Outline

Notes

consumers from abusive financial services.

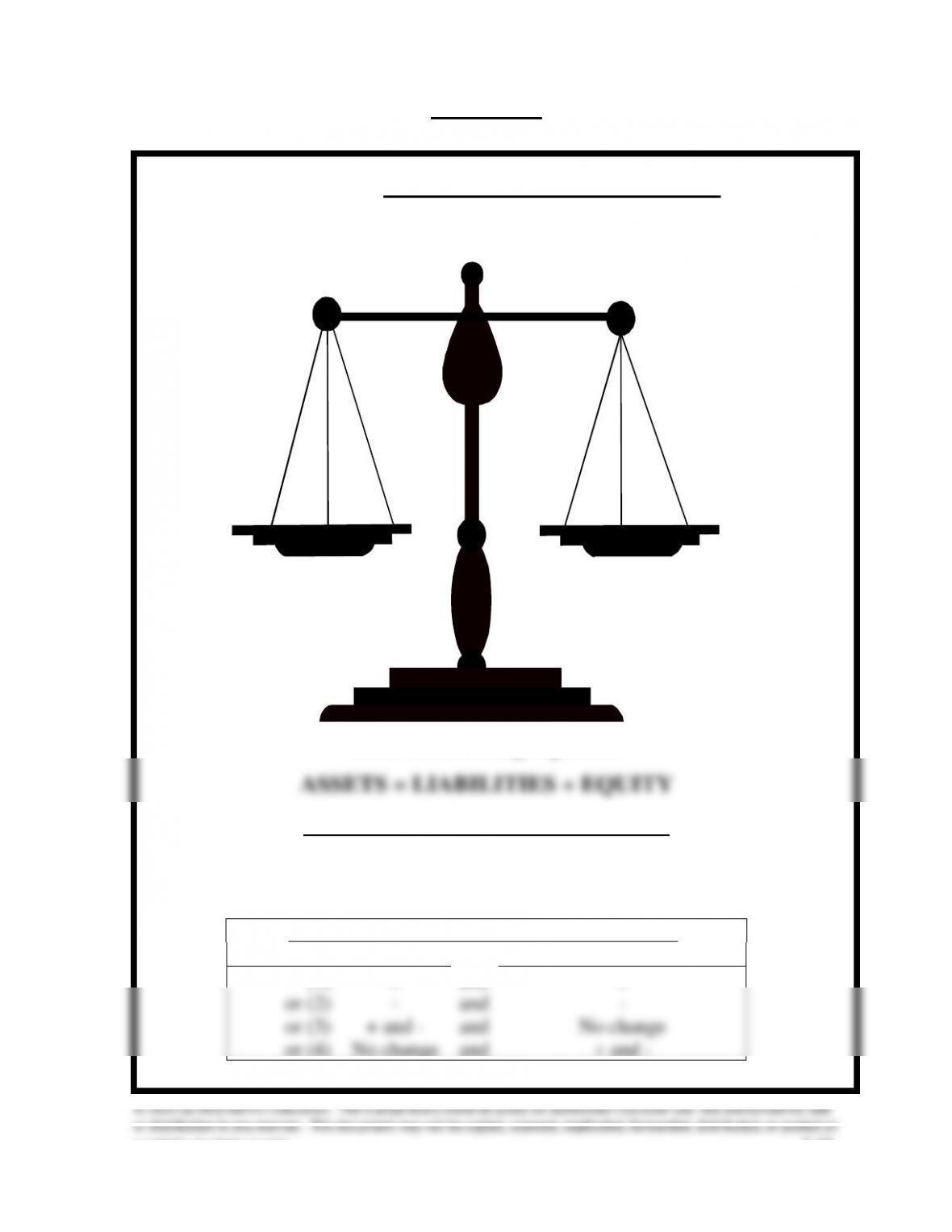

III. Transaction Analysis and the Accounting Equation

A. Accounting Equation – accounting system reflects two basic aspects

of a company: what it owns and what it owes.

1. Assets are resources a company owns or controls.

2. Liabilities are creditors’ claims on assets.

3. Equity is the owner’s claim on assets.

4. The relation of assets, liabilities and equity is reflected in the

accounting equation: Assets = Liabilities + Equity

5. A corporation’s equity—often called stockholders’ or

shareholders’ equity—has two parts: contributed capital and

retained earnings:

a. Contributed capital, refers to the amount that stockholders

invest in the company—included under the title common

stock.

b. Retained earnings refer to income (revenues less expenses)

that is not distributed to stockholders. The distribution of

assets to stockholders is called dividends, which reduce

retained earnings. Revenues increase retained earnings via

net income from a company’s earnings activities. Expenses

decrease retained earnings and are the cost of assets or

services used to earn revenues.

6. The above breakdown of equity yields the expanded accounting

equation: A= L + Contributed Capital + Retained Earnings

A = L + Common Stock – Dividends + Revenues – Expenses

7. Net income occurs when revenues exceed expenses. A net loss

occurs when expenses exceed revenues, which decreases equity.

B. Transaction Analysis

Business activities can be described in terms of transactions and

events. External transactions are exchanges of value between two

entities, which yield changes in the accounting equation. Internal

transactions are exchanges within an entity; they can also affect the

accounting equation. Events refer to those happenings that affect an

entity’s accounting equation and can be reliably measured. The next

section uses the accounting equation to analyze eleven selected

transactions and events. Transactions leave the accounting equation

in balance; assets always equal the sum of liabilities and equity.

Transaction 1: Investment by Owner

+ Assets (Cash) = + Equity (Common Stock)

After this transaction, cash (an asset) and stockholders’ equity equal

Chapter 01 – Introducing Accounting in Business

Chapter Outline

Notes

Transaction 2: Purchase supplies for cash

+Assets (Supplies) = – Assets (Cash)

This transaction changes the form of assets from cash to supplies;

the decrease in cash is exactly equal to the increase in supplies.

Transaction 3: Purchase Equipment for Cash

+ Assets (Equipment) = – Assets (Cash)

Like Transaction 2, this transaction is an exchange of one asset,

cash, for another asset, equipment; the equipment is an asset because

of its expected future benefits.

Transaction 4: Purchase Supplies on Credit

+Assets (Supplies) = + Liability (Account Payable)

The supplies are acquired in exchange for a promise to pay for them

later; the liability created is referred to as accounts payable.

Transaction 5: Provide Services for Cash

+ Assets (Cash) = + Equity (Revenues)

The company earns revenues by providing services to its clients; the

increase in equity is included in revenues because the cash received

from clients is earned by providing services.

Transactions 6 and 7: Payment of Expenses in Cash

– Assets (Cash) = – Equity (Expenses)

These two transactions involve the payment of cash for this month’s

rent and employee salary; the costs of both rent and salary are

expenses, as opposed to assets, because their benefits are used in the

current month (they have no further benefits after the current

month). Both transactions decrease equity which is included in the

column titled Expenses.

Transaction 8: Provide Services and Facilities for Credit

+ Assets (Accts Receivable) = + Equity (Revenues)

The company earns revenues by providing services to its clients; the

clients are billed for the services. This transaction results in an asset,

called accounts receivable, which is the amount owed by this client,

and also yields an increase in equity reflected in the column titled

Revenues.

Transaction 9: Receipt of Cash from Accounts Receivable

+ Assets (Cash) = – Assets (Accounts Receivable)

The client pays the company the amount that it was billed for the

services provided in Transaction 8. This transaction does not change

the total amount of assets and does not affect liabilities or equity; it

converts the receivable (an asset) to cash (an asset). It does not

create new revenue. The revenue was recognized in Transaction 8.

Transaction 10: Payment of accounts payable

– Assets (Cash) = – Liability (Accounts Payable)

The company made a partial payment to the vendor for the supplies

acquired in Transaction 4. This transaction decreases cash and

decreases its liability to the vendor. Equity does not change; this

event does not create an expense. The expense will be recorded in

the future when the company derives the benefits from these supplies

by using them.

Chapter 01 – Introducing Accounting in Business

Chapter Outline

Notes

Transaction 11: Payment of cash dividend

– Assets (Cash) = – Equity (Dividends)

The company declared and paid a dividend to its owner. Dividends

(decreases in equity) are not reported as expenses because they are

not part of the company’s earnings process, and they are not used in

computing net income.

IV. Financial Statements

A Income Statement

Reports on operating revenue and expense activities over a period of

time. Net income (or loss) is computed as sales less all costs and

expenses. Revenues are reported first followed by expenses.

Expenses reflect the costs to generate the revenue reported.

B. Statement of Retained Earnings

Reports changes in retained earnings of the business over a period of

time. Changes result from net income, which increases retained

earnings. A net loss and dividends decrease retained earnings.

Ending retained earnings is reported on the balance sheet.

C. Balance Sheet

Reports a listing of amounts for assets, liabilities, and equity at a

point in time.

D. Statement of Cash Flows

Reports on cash flows for operating, investing, and financing

activities over a period of time.

V. Global View

A. Basic Principles – both U.S. GAAP and IFRS include broad and

similar guidance for financial accounting. However, neither system

specifies particular account names nor the detail required.

B. Transactions Analysis – both U.S. GAAP and IFRS apply transaction

countries.

VI. Decision Analysis—Return on Assets (ROA)

A. Return on assets, also called return on investment (ROI), is a

profitability measure; useful in evaluating management, analyzing

and forecasting profits, and planning activities.

B. Risk is the uncertainty about the return we will earn. All business

investments involve risk, but some involve more risk than others.

C. The lower the risk of an investment, the lower is our expected return.

Chapter 01 – Introducing Accounting in Business

a website, in whole or part. 1-10

Chapter Outline

Higher risk implies higher, but riskier, expected returns.

D. The trade-off between risk and return is a normal part of business.

We use accounting information to assess both return and risk.

Notes

VIII. Business Activities and the Accounting Equation (Appendix 1B)

There are three major types of business activities:

A. Financing Activities—provide the means organizations use to pay

for resources such as land, buildings, and equipment to carry out

plans.

B. Investing Activities—the acquiring and disposing of resources

(assets) that an organization uses to acquire and sell its products or

services.

C. Operating Activities—involve using resources to research, develop,

purchase, produce, distribute, and market products and services.

Chapter 01 – Introducing Accounting in Business

a website, in whole or part. 1-11

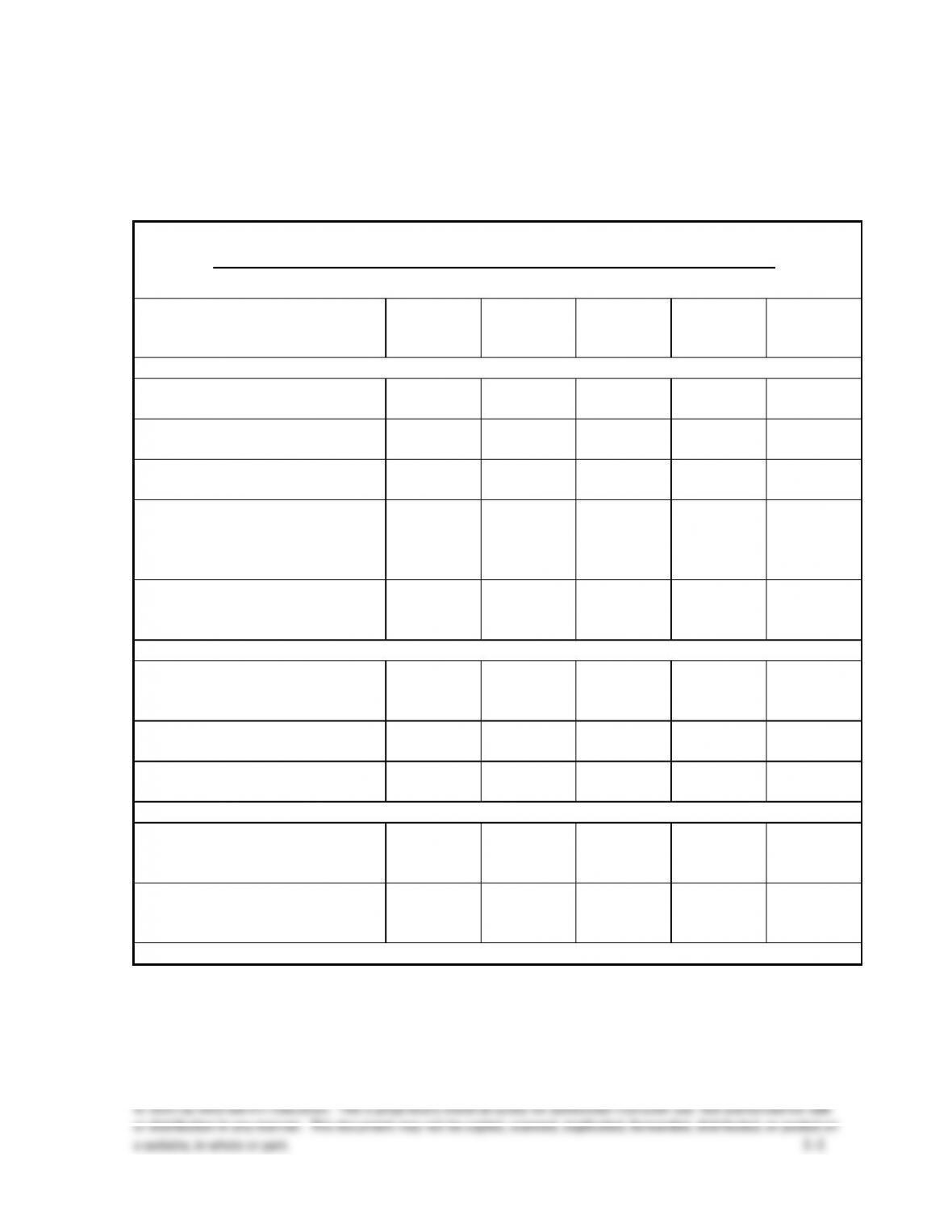

VISUAL #1-1

WARNING: NO MATTER WHAT HAPPENS

ALWAYS KEEP THIS SCALE

IN BALANCE

ASSETS L + E

Basic Accounting Equation

TRANSACTION ANALYSIS RULES

1) Every transaction affects at least two items.

2) Every transaction must result in a balanced equation.

TRANSACTION ANALYSIS POSSIBILITIES:

A

=

L

+

E

(1)

+

and

+

or (2)

–

and

–

or (3)

+ and –

and

No change

or (4)

No change

and

+ and –

Chapter 01 – Introducing Accounting in Business

a website, in whole or part. 1-12

Chapter 1 – Alternate Demonstration Problem #1

One spring, Jane Smith decided to earn money as a lawn service

professional. After discussions with neighbors, she obtained enough

commitments for lawn servicing jobs that she thought she could be

successful at it. On June 1, 2013, on the basis of these commitments,

Jane personally invested $2,000 in the business in exchange for

common stock. She deposited the cash in a business bank account

opened under the name of Ultimate Lawn Care, Inc.

On August 31, 2013, Jane noted the following events which occurred

during the first three months of business:

▪ On June 1, Jane personally invested $2,000 in the business by

depositing the $2,000 in the business’s bank account.

▪ Deposits during the first three months, all from customer

collections, totaled $11,400.

▪ Checks written during the three month period included the following:

▪ Truck and equipment rental, $1,800

▪ Gas, oil, and lubrication, $880

▪ Miscellaneous supplies used, $90

▪ Helpers, $4,700;

▪ Payroll taxes, $500;

▪ Insurance, $175;

▪ Telephone, $100

▪ Dividend (transferred to personal bank account), $2,000.

Jane also had business records that showed:

▪ Customers still owed $600 for services that were performed.

▪ The business owed another $100 to a vendor for gas and oil.

Chapter 01 – Introducing Accounting in Business

a website, in whole or part. 1-13

Chapter 1 – Alternate Demonstration Problem #1, continued

Required:

1. Show the effect of each transaction on the accounting equation.

2. Prepare an income statement for Ultimate Lawn Care, Inc. for the

three months ended August 31, 2013.

3. Prepare a balance sheet for Ultimate Lawn Care, Inc. at August 31,

2013.

4. Explain why the company’s cash balance at the end of the summer

does not agree with the amount of net income earned during the

summer.

Chapter 01 – Introducing Accounting in Business

a website, in whole or part. 1-14

Solution: Chapter 1 – Alternate Demonstration Problem #1

1.

Item

Assets

=

Liabilities

+

Equity

a.

Issuance of common stock

for cash

+

2,000

+

2,000

b.

Revenue received

+

11,400

+

11,400

c.

Truck and equipment rental

–

1,800

–

1,800

d.

Truck expenses

–

880

–

880

e.

Miscellaneous supplies used

–

90

–

90

f.

Helpers

–

4,700

–

4,700

g.

Payroll taxes

–

500

–

500

h.

Insurance

–

175

–

175

i.

Telephone

–

100

–

100

j.

Dividend

–

2,000

–

2,000

k.

Revenue earned

+

600

+

600

l.

Oil and gas bill not yet paid

+

100

–

100

3,755

100

3,655

2.

ULTIMATE LAWN CARE, INC.

Income Statement

For the three months ended August 31, 2013

Total revenue (11,400 + 600) ………………………………

$12,000

Expenses:

Truck expenses (880 + 100) …………………………..

$ 980

Truck and equipment rental ………………………….

1,800

Supplies ………………………………………………………

90

Helpers ………………………………………………………..

4,700

Payroll taxes ………………………………………………..

500

Insurance …………………………………………………….

175

Telephone ……………………………………………………

100

Total expenses …………………………………………….

8,345

Net income ………………………………………………………..

$ 3,655

Chapter 01 – Introducing Accounting in Business

Solution: Chapter 1 – Alternate Demonstration Problem #1, continued

3.

ULTIMATE LAWN CARE, INC.

Balance Sheet

August 31, 2013

Assets

Liabilities

Cash …………………………….

$3,155

Accounts payable ………..

$ 100

Accounts receivable …….

600

Equity

Common stock …………….

2,000

Retained earnings

(3,655 – 2,000) …………..

1,655

Total assets ………………….

$3,755

Total liabilities and

owner’s equity ………….

$3,755

Cash inflows …………………………………………………..

(a) Issuance of common stock for cash …………

$ 2,000

(b) Fees received ………………………………………….

11,400

Total inflows ……………………………………………

$13,400

Cash outflows …………………………………………………

(c) Truck and equipment rental ……………………..

$ 1,800

(d) Truck expenses ……………………………………….

880

(e) Buy supplies ……………………………………………

90

(f) Pay salaries …………………………………………….

4,700

(g) Pay taxes ………………………………………………..

500

(h) Buy insurance …………………………………………

175

(i) Pay phone bill ………………………………………….

100

(j) Dividend to owner ……………………………………

2,000

Total outflows ………………………………………….

10,245

Ending cash balance ……………………………………….

$ 3,155

4.

First, note that the issuance of common stock for cash (transaction a)

and the cash dividend (transaction j) affect the cash balance, but do not

enter into the determination of net income. In addition, an expense