Problem E-6BA (Continued)

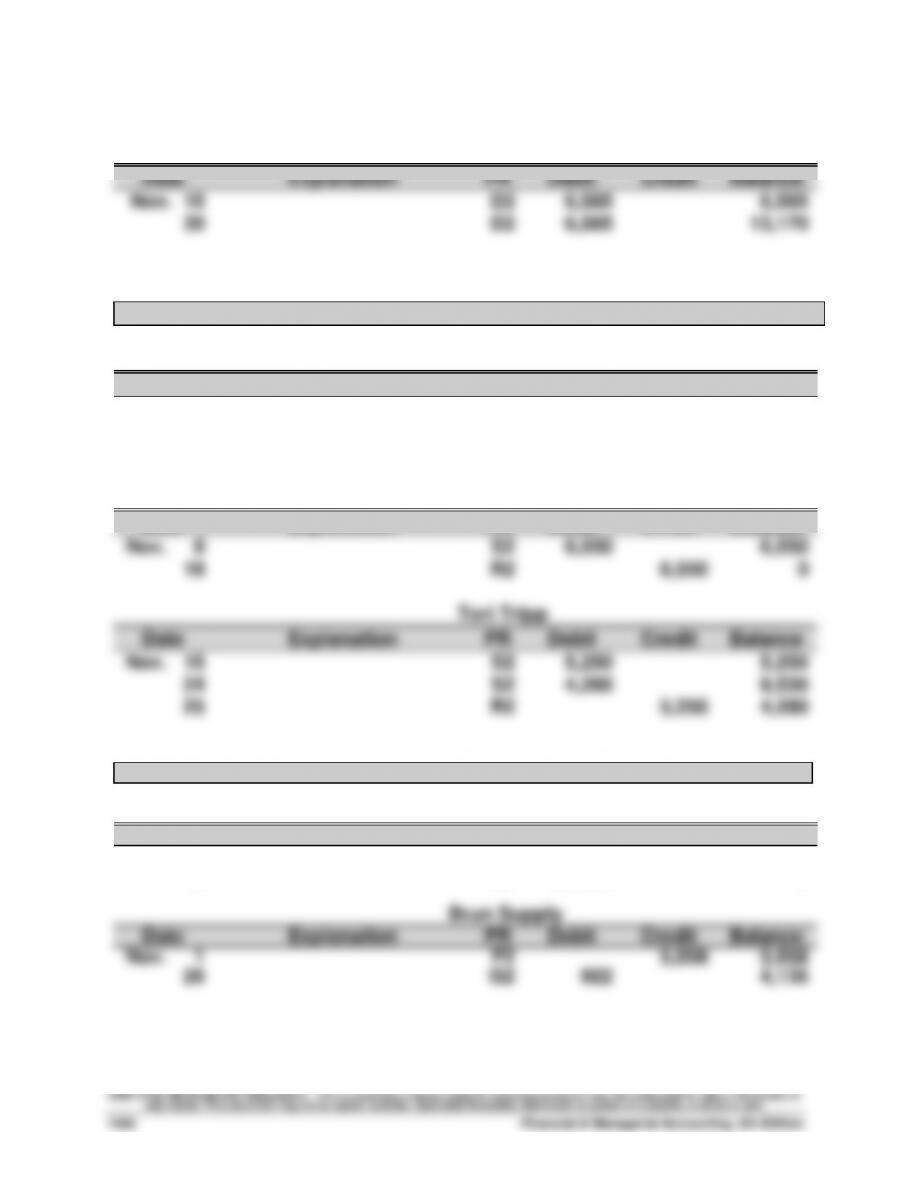

Sales Salaries Expense

Acct. No. 621

Date

Explanation

PR

Debit

Credit

Balance

Nov. 15

D2

6,585

6,585

30

D2

6,585

13,170

ACCOUNTS RECEIVABLE LEDGER

Carlos Mantel

Date

Explanation

PR

Debit

Credit

Balance

Nov. 10

S2

13,500

13,500

19

R2

13,500

0

22

S2

3,695

3,695

Cyd Rounder

Date

Explanation

PR

Debit

Credit

Balance

Nov. 8

S2

6,550

6,550

18

R2

6,550

0

Date

Explanation

PR

Debit

Credit

Balance

Nov. 15

S2

5,250

5,250

24

S2

4,280

9,530

25

R2

5,250

4,280

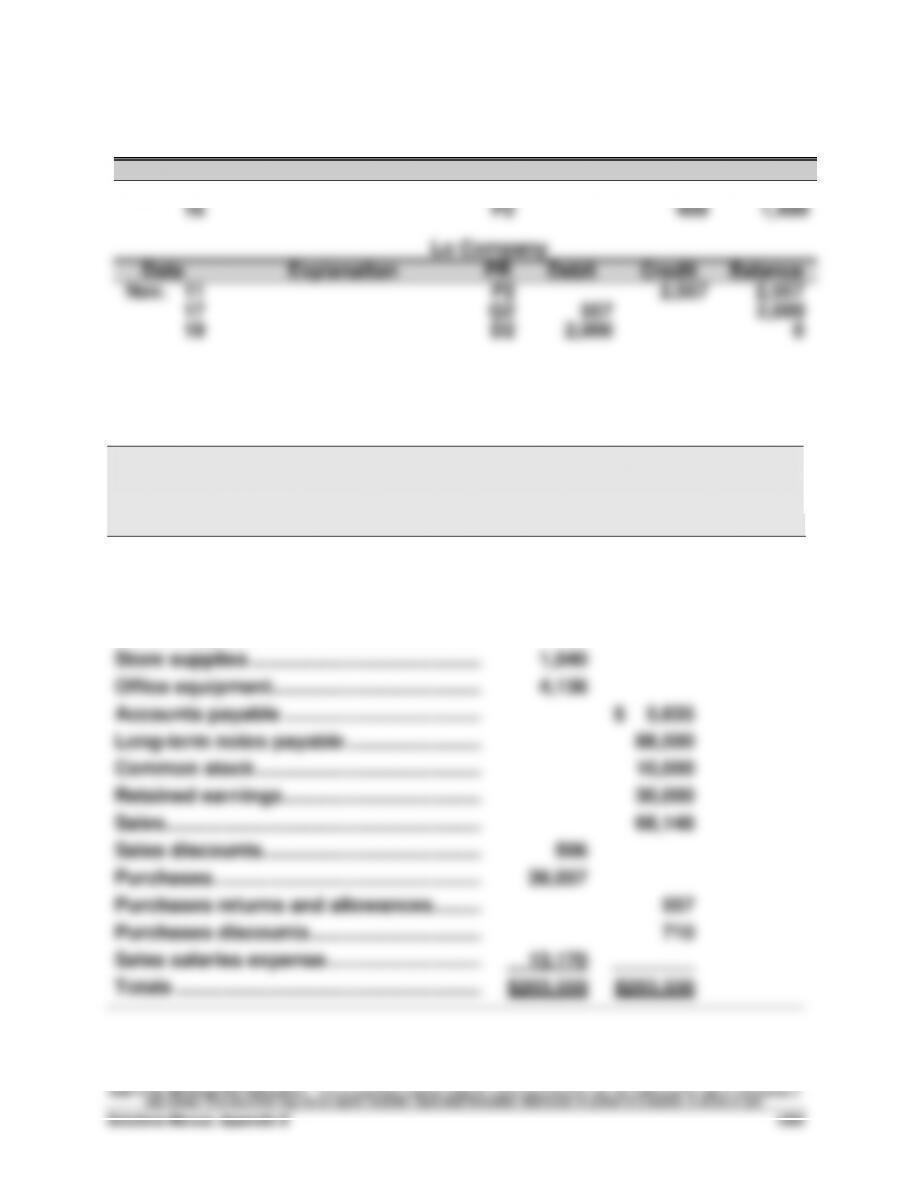

Problem E-6BA (Continued)

Grebe Company

Date

Explanation

PR

Debit

Credit

Balance

Nov. 5

P2

1,040

1,040

16

P2

459

1,499

Date

Explanation

PR

Credit

Balance

17

19

Financial & Managerial Accounting, 5th Edition

1564

Problem E-6BA (Concluded)

Part 3—continued

GRASSLEY COMPANY

Schedule of Accounts Receivable

November 30

Carlos Mantel. ……………………………………..……….

$3,695

Tori Tripp …………………………………………….……….

4,280

Total accounts receivable …………………….…….

$7,975

GRASSLEY COMPANY

Schedule of Accounts Payable

November 30

Brun Supply. ………………………………………..……….

$4,136

Grebe Company …………………………………..……….

1,499

Total accounts payable ………………………..…

$5,635

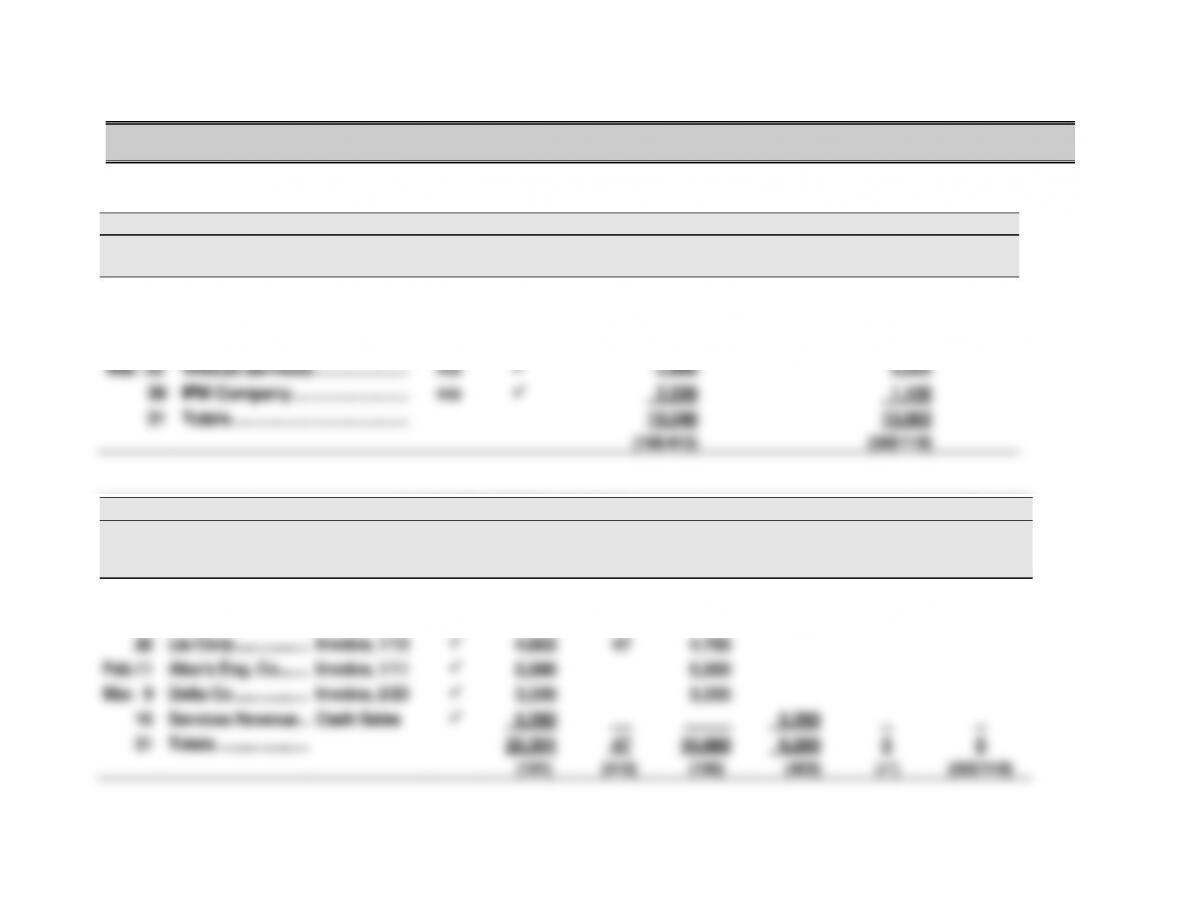

SERIAL PROBLEM – SP E

Serial Problem, Success Systems (100 minutes) Parts 1 and 2

SALES JOURNAL

Page 2

Date

Account Debited

Invoice

Number

PR

Accounts Receivable Dr.

Sales Cr.

Cost of Goods Sold Dr.

Inventory Cr.

Jan. 13

Liu Corp. …………………………………………….

n/a

✓

5,200

3,560

26

KC, Inc. ……………………………………………….

n/a

✓

5,800

4,640

Feb. 23

Delta Co.……………………………….…………….

n/a

✓

3,220

2,660

Mar. 25

Wildcat Services …………………..………

n/a

✓

2,800

2,002

30

IFM Company ……………………….….

n/a

✓

2,220

1,100

31

Totals ………………………………………………….

19,240

13,962

(106/413)

(502/119)

CASH RECEIPTS JOURNAL

Page 2

Date

Account Credited

Explanation

PR

Cash

Dr.

Sales

Discount

Dr.

Accounts

Receivable

Cr.

Services

Revenue

Cr.

Other

Accts.

Cr.

Cost of Goods

Sold Dr.

Inventory Cr.

Jan. 9

Gomez Co …………..………………

Invoice, n/a

✓

2,668

2,668

16

Services Revenue ..…………………………

Cash Sales

✓

4,000

4,000

22

Liu Corp …………………………..

Invoice, 1/13

✓

4,653

47

4,700

Feb.11

Alex’s Eng. Co …….…………………….

Invoice, 1/11

✓

5,500

5,500

Mar. 9

Delta Co …………………………..

Invoice, 2/23

✓

3,220

3,220

16

Services Revenue ..…………………………

Cash Sales

✓

5,260

__

_____

5,260

_

_

31

Totals ………………….……….

25,301

47

16,088

9,260

0

0

(101)

(415)

(106)

(403)

(✓)

(502/119)

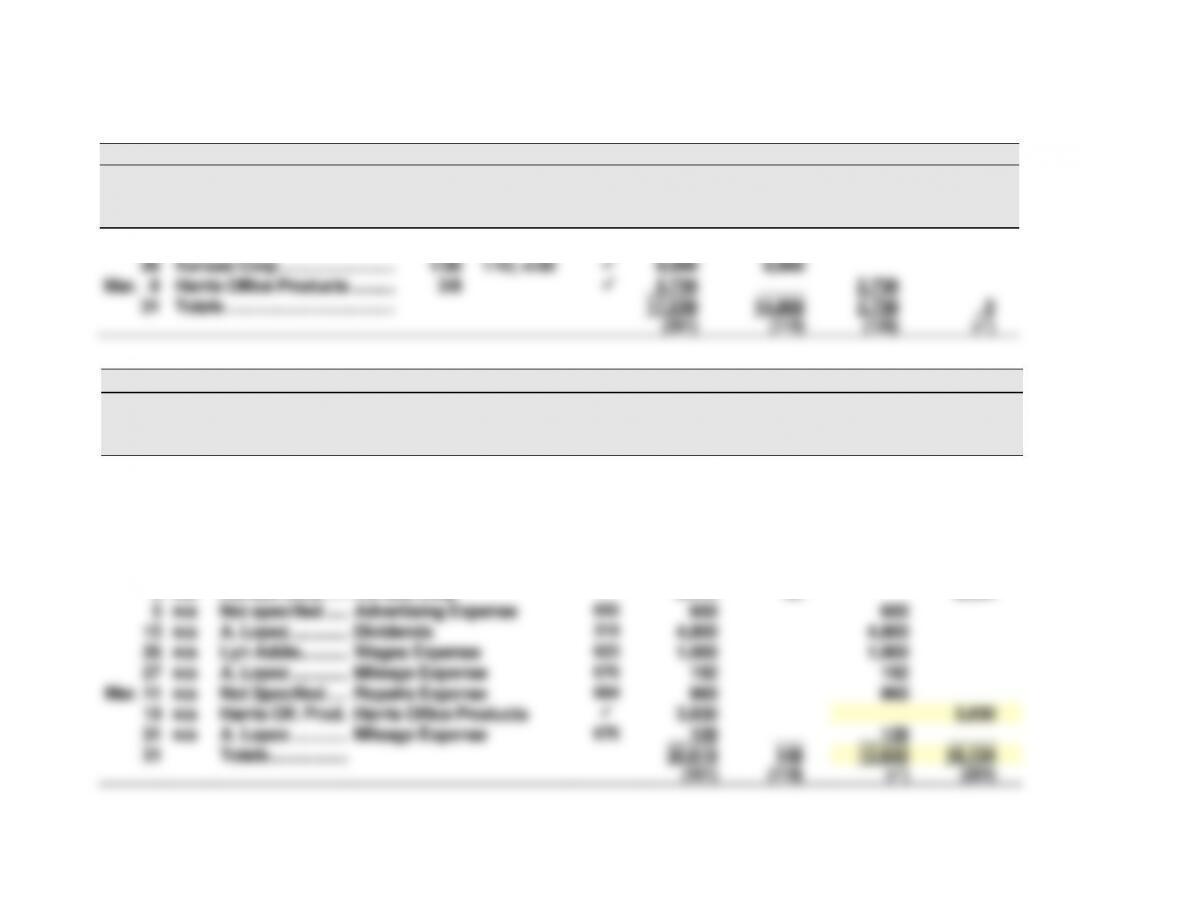

Serial Problem, Success Systems (Continued)

PURCHASES JOURNAL

Page 2

Date

Account

Date of

Invoice

Terms

PR

Accounts

Payable

Cr.

Inventory

Dr.

Computer

Supplies

Dr.

Other

Accounts

Dr.

Jan. 7

Kansas Corp ……………………….….

1/7

1/10, n/30

✓

5,800

5,800

26

Kansas Corp ……………………….….

1/26

1/10, n/30

✓

9,000

9,000

Mar. 8

Harris Office Products ………..……………..

3/8

✓

2,730

_____

2,730

31

Totals ………………………………….……………..

17,530

14,800

2,730

0

(201)

(119)

(126)

(✓)

CASH DISBURSEMENTS JOURNAL

Page 2

Date

Ck.

No.

Payee

Account Debited

PR

Cash

Cr.

Inventory

Cr.

Other

Accounts

Dr.

Accounts

Payable

Dr.

Jan. 4

n/a

Lyn Addie …………………………..

Wages Expense

Wages Payable

623/210

625

125

500

15

n/a

Not specified …………………………..

Merchandise Inventory

119

600

600

17

n/a

Kansas Corp …………………………..

Kansas Corp

✓

5,742

58

5,800

31

n/a

Lyn Addie …………………………..

Wages Expense

623

1,250

1,250

Feb. 1

n/a

Hillside Mall ……..……………………

Prepaid Rent

131

2,475

2,475

3

n/a

Kansas Corp …………………………..

Kansas Corp

✓

8,414

90

8,504

5

n/a

Not specified …………………………..

Advertising Expense

655

600

600

15

n/a

A. Lopez …………..………………

Dividends

319

4,800

4,800

26

n/a

Lyn Addie …………………………..

Wages Expense

623

1,000

1,000

27

n/a

A. Lopez …………..………………

Mileage Expense

676

192

192

Mar. 11

n/a

Not Specified …………………………..

Repairs Expense

684

960

960

19

n/a

Harris Off. Prod ..…………………………

Harris Office Products

✓

3,830

3,830

31

n/a

A. Lopez …………..………………

Mileage Expense

676

128

___

128

_____

31

Totals ……………….………….

30,616

148

12,630

18,134

(101)

(119)

(✓)

(201)

Serial Problem, Success Systems (Concluded)

Part 3

GENERAL JOURNAL

Page 2

2014

Jan. 5 Cash …………………………………………………………. 101 25,000

Common Stock …………………………………. 307 25,000

Additional investment by owner.

11 Accounts Receivable—Alex’s Eng. Co ………. 106.1 5,500

24 Accounts Payable—Kansas Corp………………. 201 496

Merchandise Inventory ……………………… 119 496

Returned merchandise for credit.

Reporting in Action — BTN E-1

1. Polaris’s Note 12 identifies its single reported business segment.

2. Polaris identifies and describes its single reportable segment in its

Note 1 as follows: “its engaged in the design, engineering,

3. Solution depends on the most recent information obtained.

Comparative Analysis — BTN E-2

1. Polaris – Current Year Revenue/Segment Assets

Domestic segment: $1,864,099 / [($957,497 + $873,183)/2] = 203.7%

International segment: $792,850 / [($270,527 + $188,464)/2] = 345.5%

2. Polaris’s domestic revenue as a percent of its domestic assets is

markedly higher than of Arctic Cat’s for both years for the domestic

segment. However, for the international segment, Arctic Cat’s revenue

Ethics Challenge — BTN E-3

1. Independence in fact means that the auditor maintains an objective

point of view of the client. Independence in appearance means that a

2. While auditors are hired by their clients to perform audits, auditors

have a responsibility to the company’s “stakeholders” and the public.

3. Since Erica Gray is a sole practitioner it is questionable whether she

can consult on the client’s accounting system and then remain

objective in subsequent years when she performs the audit of the

company. Large firms often separate consulting and auditing

engagements for the same client by having staff stationed in two

different geographic branches of the firm do the work. Or a large local

firm might be able to perform consulting and auditing for the same

client by assigning different personnel to the two jobs. In this

scenario, Erica Gray would need to do both jobs herself, making it

difficult to maintain independence in fact and appearance.

(Note to instructors: The Sarbanes-Oxley Act specifically prohibits auditors

from providing financial information and system designs for their SEC audit

clients. This was codified by the SEC [Final Ruling 68].)

Communicating in Practice — BTN E-4

The memo should recommend the use of special journals and subsidiary

ledgers. It should explain the time-saving aspect of journalizing in labeled

columns and also the posting of column totals representing the impact of

groups of like transactions. The memo should discuss the timely

information provided by subsidiary ledgers regarding customer and

creditor balances. A discussion of the uses of a schedule for verifying the

accuracy of subsidiary ledgers should also be included.

Taking It to the Net — BTN E-5

(See Dell’s Note 14 – Segment Information)

1. Large Enterprise; Public; Small and Medium Business; and Consumer.

2. The Large Enterprise segment reports $1,854 million of operating income

and the Large Enterprise segment reports $3,108 million of assets.

3. Dell’s Operating Income and Total Assets by Segment

($ millions)

Operating

Income 2012

Total Assets 2012 :

Total Assets 2011

Segment Return

on Assets

Large Enterprise …..……

$ 1,854

$3,108 : $2,934

61.4%

Public ………………….……

$ 1,644

$2,330 : $2,545

67.4%

Small & Medium

Business …………………

$ 1,665

$1,421 : $1,398

118.1%

Consumer …………………

$ 324

$1,503,: $1,458

21.9%

The Small and Medium Business had the highest segment return on

assets for the fiscal year ended 2012 with a 118.1% return. The other

three showed returns on assets ranging from 21% to 67%.

4. The six product groups reported by Dell include: Desktop PCs, Mobility,

$19,104 30.8%

Desktop PCs ……………………………………………….

Software and peripherals ……………………………..

Servers and networking ……………………………….

8,336 13.4

Services ……………………………………………………...

Totals ………………………………………………………….

$62,071 100.0%

Teamwork in Action — BTN E-6

For check figures in the implementation of this activity see the solution

to Problem E-3A or E-3B.

Global Decision — BTN E-7

1. KTM has the following reported segments:

2. KTM discloses dollar amounts for the following line items:

• Profit and Loss Information

i. Net sales