AppD – Accounting for Partnerships

Appendix D

Accounting for Partnerships

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Identify characteristics of

partnerships and similar

organizations.

1, 2, 3, 4, 5,

7, 8, 9

D-1

D-1, D-2

RIA, CA,

CIP, GD, ED

Analytical objectives:

Al. Compute partner return on

equity and use it to evaluate

partnership performance.

D-8

D-12

Procedural objectives:

P1. Prepare entries for partnership

formation.

D-4

TTN

P2. Allocate and record income and

loss among partners.

6, 7, 9

D-2, D-3

D-3, D-4,

D-5, D-6

D-1, D-2,

D-3

EC, TTN,

TIA

P3. Account for the admission and

withdrawal of partners.

12

D-5, D-6

D-7, D-8,

D-9

D-4

P4. Prepare entries for partnership

liquidation.

10, 11

D-7

D-10, D-11

D-5

*See additional information on next page that pertains to these quick studies, exercises and

problems.

AppD – Accounting for Partnerships

*Assignment materials that can be completed by students using:

Sage 50 and QuickBooks Pro 2013 templates – Problems D-1A and D-4A, and D-5A

Excel templates – Problems D-2A and D-3A.

** The Serial Problem for Success Systems, which covers numerous learning objectives, can be

most of the chapters. Even if previous segments were not assigned, students can begin the segment

of the serial problem that is included in this chapter. It is most readily solved if students use the

Working Papers that accompany the book.).

Synopsis of Chapter Revision

• New examples of LLPs and their prevalence among professional services

• New discussion of the potential for multiple drawing accounts in practice

• Revised and streamlined three-step process to liquidate a partnership

PowerPoint® Show Slides

Chapter Learning Objective

PowerPoint® Slides

C1

6-8

P1

9-10

P2

11-19

P3

20-32

P4

33-36

A1

37

AppD – Accounting for Partnerships

Appendix Outline

Notes

I. Partnership Form of Organization—An unincorporated association

of two or more people to pursue a business for profit as co-owners.

A. Characteristics of Partnerships

1. Voluntary Association between partners.

2. Partnership Agreement—partnership contract normally

includes details of partners’ (1) names and contributions, (2)

right and duties, (3) sharing of income and losses, (4)

withdrawal arrangement, (5) dispute procedures, (6) admission

and withdrawal of partners, and (7) rights and duties in the

event a partner dies. This agreement should be in writing but is

binding even if only expressed orally.

3. Limited Life—death, bankruptcy, or expiration of the contract

period automatically ends a partnership.

4. Taxation—partnerships are not subject to tax on income—

partners report their share of income on their personal income

tax return.

5. Mutual agency—each partner is an agent of the partnership

and can enter into and bind the partnership to any contract

within the normal scope of its business.

6. Unlimited liability—each general partner is responsible for

payment of all the debts of the partnership if the other partners

are unable to pay their share.

7. Co-Ownership of Property—assets are owned jointly by all

partners but claims on partnership assets are based on their

capital account and the partnership contract.

B. Organizations with Partnership Characteristics

1. Limited Partnership (L.P. or Ltd.) has two classes of partners,

general and limited. General partners assume unlimited

liability for the debts of the partnership. The limited partners

assume no personal liability beyond their invested amounts and

cannot take an active role in managing the company.

2. Limited liability partnership (L.L.P.) is designed to protect

innocent partners from malpractice or negligence claims

resulting from the acts of another partner. Generally, all

partners are personally liable for other partnership debts.

for as a “C” corporation.

4. Limited Liability Company (L.L.C. or L.C) owners are called

role. L.L.C.’s have a limited life and are typically classified as

AppD – Accounting for Partnerships

Appendix Outline

Notes

C. Choosing a Business Form

Factors to be considered include: taxes, liability risk, tax and fiscal

year-end, ownership structure, estate planning, business risks, and

earnings and property distributions.

II. Basic Partnership Accounting—same as accounting for a

proprietorship except for transactions directly affecting partners’

equity. Use separate capital and withdrawal accounts for each partner.

A. Organizing a Partnership

Each partner’s investment is recorded at an agreed upon value,

normally the fair market value of the assets and liabilities at their

date of contribution.

B. Dividing Income or Loss

1. Any agreed upon method of dividing income or loss is

allowed. If there is no agreement, the net income or loss is

divided equally.

2. Common methods of dividing partnership earnings use:

a. Allocation on stated ratios—partners must agree on the

fractional share each receives.

b. Allocation on capital balances—based on the ratio of each

partner’s relative capital balance.

c. Allocation on service, capital, and stated ratios—salary

and interest allowances, and a fixed ratio are specified.

i. When income exceeds allowances, the remainder is

allocated to individual partners using a fixed ratio and

added to their individual planned allowance.

ii. When allowances exceed the income, the negative

amount or shortage is allocated using the ratio and

applied against each partner’s total allowance.

3. Salaries to partners and interest on partners’ investments are

not partnership expenses; they are allocations of net income.

4. Partners may agree to salary and interest allowances to reward

unequal contributions of services or capital.

C. Partnership Financial Statements

Similar to those of other organizations except:

1. The statement of partners’ equity shows changes for each

partner’s capital account, including the allocation of income.

2. The equity section of the balance sheet generally lists a

separate capital account for each partner.

AppD – Accounting for Partnerships

Appendix Outline

Notes

III. Admission and Withdrawal of Partners

A. Admission of a Partner

1. Purchase of Partnership Interest

a. The purchase is a personal transaction between one or

more current partners and the new partner.

b. Purchaser does not become a partner until accepted by the

current partners.

c. Involves a reallocation of current partners’ capital to

reflect the transaction.

2. Investing Assets in a Partnership

a. The transaction is between the new partner and the

partnership. Invested assets become partnership property.

b. New partner’s equity recorded for assets invested may be

equal to, less than, or greater than the investment.

c. Bonuses to old partners are allocated based on their

income and loss sharing agreement. Occurs when current

value of partnership is greater than the recorded amounts

of equity so partners will require new partner to pay a

bonus for the privilege of joining.

d. Bonus to new partner when the new partner’s equity

differs from the investment. Occurs when new partner

needs additional cash or has exceptional talents.

B. Withdrawal of a Partner—two ways:

1. Withdrawing partner sells his or her interest to another person

who pays cash or other assets to the withdrawing partner.

2. Cash or other assets of the partnership can be distributed to the

withdrawing partner in settlement of his or her interest.

3. No Bonus if withdrawing partner takes cash or assets equal to

his/her equity balance.

4. Bonus to Remaining Partners when withdrawing partner is

willing to take less than the recorded value of his or her

equity, there is a bonus to remaining partner’s equity.

5. Bonus to Withdrawing Partner which means that the remaining

partners reduce their equity by the amount of the bonus given

to the withdrawing partner.

C. Death of a Partner

1. Dissolves a partnership.

2. Deceased partner’s estate is entitled to receive his or her

equity. Contract usually calls for closing of the books and

determining current value of assets and liabilities to update

equity.

the equity to remaining partners or to an outsider, or it can

involve withdrawing assets.

AppD – Accounting for Partnerships

Appendix Outline

Notes

IV. Liquidation of a Partnership

A. Involves four steps:

1. Noncash assets are sold for cash and a gain or loss on

liquidation is recorded.

2. Allocate gain or loss from liquidation of the assets to partners

using their income-and-loss ratio.

3. Pay or settle all partner liabilities.

4. Distribute any remaining cash to partners based on their

capital account balances.

B. Allocating gains or losses on liquidation may result in:

1. No Capital Deficiency—all partners’ have a zero or credit

balance in their capital accounts equivalent to final

distribution of cash.

2. Capital deficiency—when at least one partner has a debit

balance in his/her capital account.

a. Partners Pays Deficiency: partners with a capital

deficiency, must, if possible, cover the deficit by paying

cash into the partnership.

b. Partner Cannot Pay Deficiency: when a partner is unable

to pay the deficiency, the remaining partners with credit

balances absorb the unpaid deficit according to their

income-and-loss ratio. Inability to cover deficiency does

not relieve partner of liability.

V. Global View – Partnership accounting according to U.S. GAAP is

similar, but not identical, to that under IFRS.

A. Both U.S. GAAP and IFRS include broad and similar guidance for

partnership accounting.

B. Different legal systems dictate different implications and

D. Different legal systems impact those agreements and their

implications to the parties.

VI. Decision Analysis—Partnership Return on Equity

A. The partnership return on equity ratio evaluates partnership

success compared with other opportunities.

B. It is calculated by dividing a partner’s share of net income by that

partner’s average partner equity.

a website, in whole or part APP D-7

AppD – Accounting for Partnerships

a website, in whole or part APP D-8

SOLUTION: Appendix D Alternative Demonstration Problem #1

1.

Proceeds from sale

$85,000

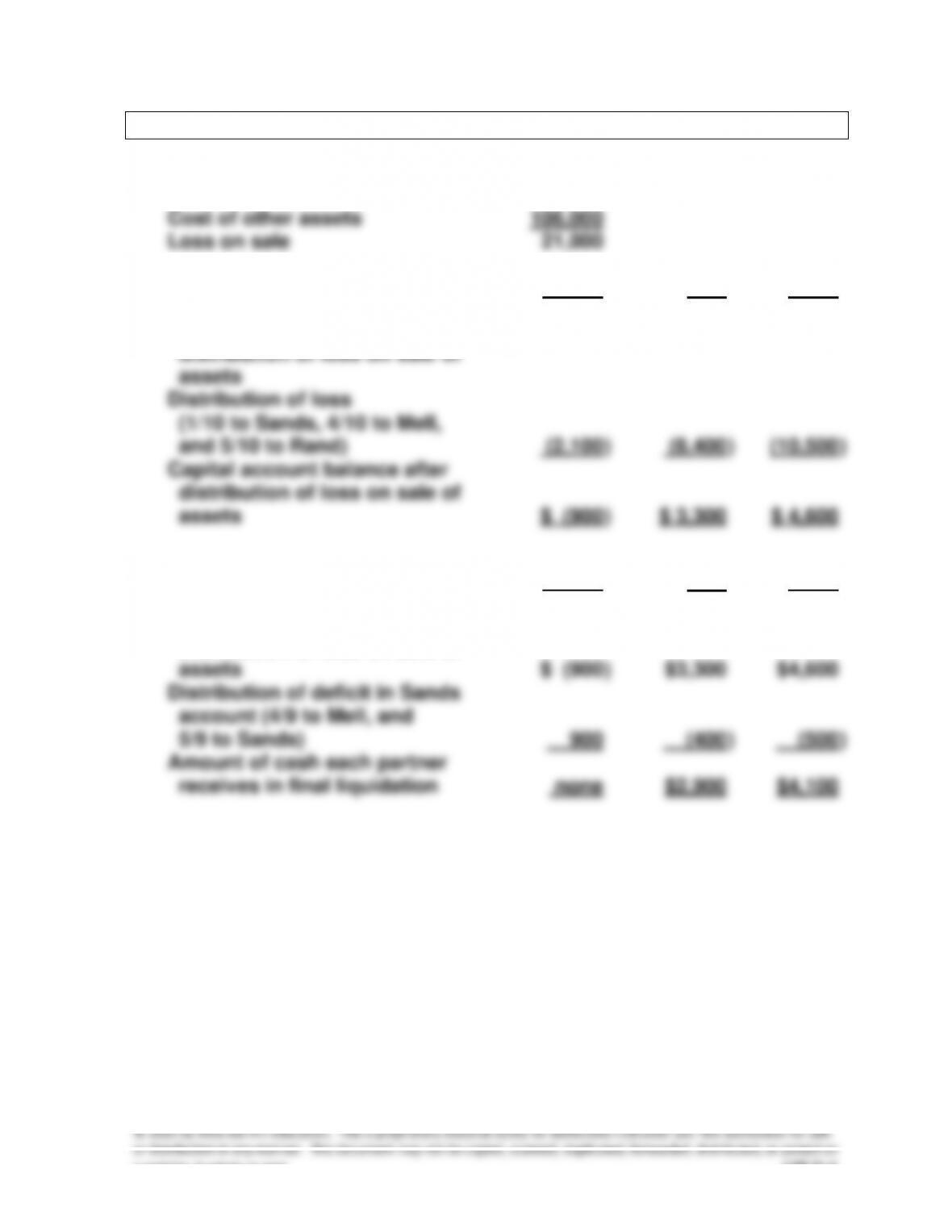

Cost of other assets

106,000

Loss on sale

21,000

2.

Sands

Mell

Rand

Capital account balance prior to

distribution of loss on sale of

assets

$1,200

$11,700

$15,100

Distribution of loss

(1/10 to Sands, 4/10 to Mell,

and 5/10 to Rand)

(2,100

)

(8,400

)

(10,500

)

Capital account balance after

distribution of loss on sale of

assets

$ (900

)

$ 3,300

$ 4,600

3.

Sands

Mell

Rand

Capital account balance after

distribution of loss on sale of

assets

$ (900

)

$3,300

$4,600

Distribution of deficit in Sands

account (4/9 to Mell, and

5/9 to Sands)

900

(400

)

(500

)

Amount of cash each partner

receives in final liquidation

none

$2,900

$4,100