Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Financial & Managerial Accounting, 5th Edition

1406

Exercise C-14 (15 minutes)

2013 return on total assets 2014 return on total assets

in anticipation of increased production and sales in 2015. Or, its

competitors’ returns may have fallen even more than that of Regae’s

returns.

Exercise C-15A (25 minutes)

2013

Dec. 16

Accounts Receivable⎯Bronson Ltd. ..........................

24,791

Sales ................................................................

24,791

Record credit sales (17,000 x $1.4583).

Dec. 31

Foreign Exchange Loss* ................................

342

Accounts Receivable⎯Bronson Ltd .....................

342

Record year-end adjustment.

*Original measure = (17,000 x $1.4583) = $24,791

Year-end measure = (17,000 x $1.4382) = 24,449

Loss for the period = $ 342

2014

Jan. 15

Cash (17,000 x $1.4482) ................................

24,619

Accounts Receivable⎯Bronson Ltd. ....................

24,449

Foreign Exchange Gain* ................................

170

Record cash receipt on account.

*Year-end measure = (17,000 x $1.4382) = $24,449

Final measure = (17,000 x $1.4482) = 24,619

Gain for the period = $ 170

Exercise C-16A (25 minutes)

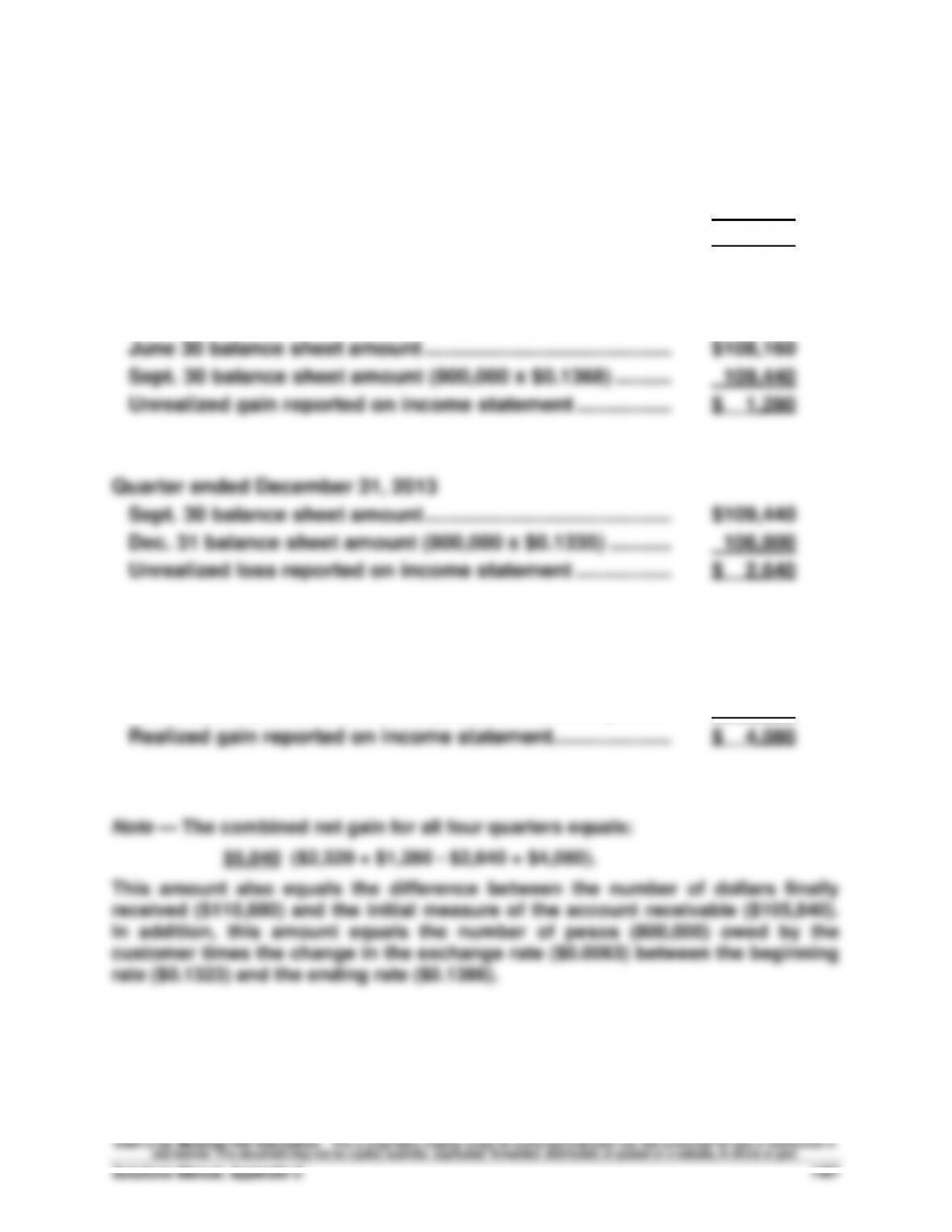

Quarter ended June 30, 2013

May 8 recorded amount (800,000 x $0.1323) ......................

$105,840

June 30 balance sheet amount (800,000 x $0.1352) ...........

108,160

Unrealized gain reported on income statement ................

$ 2,320

Quarter ended September 30, 2013

June 30 balance sheet amount ............................................

$108,160

Sept. 30 balance sheet amount (800,000 x $0.1368) ..........

109,440

Unrealized gain reported on income statement .................

$ 1,280

Quarter ended December 31, 2013

Sept. 30 balance sheet amount ............................................

$109,440

Dec. 31 balance sheet amount (800,000 x $0.1335) ...........

106,800

Unrealized loss reported on income statement .................

$ 2,640

Quarter ended March 31, 2014

Dec. 31 balance sheet amount ............................................

$106,800

Feb. 10, 2014, amount received (800,000 x $0.1386) .........

110,880

Realized gain reported on income statement .....................

$ 4,080

Financial & Managerial Accounting, 5th Edition

1408

Exercise C-17 (15 minutes)

1. Accounting for available-for-sale securities (and as explained in

2. The entirety of the € 18 million net unrealized losses on available-for-

PROBLEM SET A

Problem C-1A (60 minutes)

Part 1

2013

Jan. 20

Short-Term Investments—Trading (Ford) ................

20,925

Cash ................................................................

20,925

Purchased Ford Motor Co.

shares [(800 x $26.00) + $125].

Feb. 9

Short-Term Investments—Trading (Lucent) ......

97,928

Cash ................................................................

97,928

Purchased Lucent shares

[(2,200 x $44.25) + $578].

Oct. 12

Short-Term Investments—Trading (Z-Seven) .....

5,825

Cash ................................................................

5,825

Purchased Z-Seven shares

[(750 x $7.50) + $200].

2014

Apr. 15

Cash ......................................................................

22,915

Gain on Sale of Short-Term Investments ....

1,990

Short-Term Investments—Trading (Ford) .....

20,925

Sold Ford Motor shares

[(800 x $29.00) - $285].

July 5

Cash ......................................................................

7,585

Gain on Sale of Short-Term Investments ....

1,760

Short-Term Investments—Trading (Z-Seven) ...

5,825

Sold Z-Seven shares

[(750 x $10.25) - $102.50].

22

Short-Term Investments—Trading (Hunt) ...........

48,444

Cash ................................................................

48,444

Purchased Hunt shares

[(1,600 x $30.00) + $444].

Aug. 19

Short-Term Investments—Trading (D.Karan)......

33,140

Cash ................................................................

33,140

Purchased Donna Karan shares

[(1,800 x $18.25) + $290].

Problem C-1A (Concluded)

2015

Feb. 27

Short-Term Investments—Trading (HCA) ................

116,020

Cash ................................................................

116,020

Purchased HCA shares

[(3,400 x $34.00) + $420].

Mar. 3

Cash ......................................................................

39,750

Loss on Sale of Short-Term Investments ................

8,694

Short-Term Investments—Trading (Hunt) .....

48,444

Sold Hunt shares [(1,600 x $25.00) - $250].

June 21

Cash ......................................................................

91,980

Loss on Sale of Short-Term Investments .........

5,948

Short-Term Investments—Trading (Lucent) ....

97,928

Sold Lucent shares [(2,200 x $42.00) - $420].

30

Short-Term Investments—Trading (B&D) ...........

57,595

Cash ................................................................

57,595

Purchased Black & Decker shares

[(1,200 x $47.50) + $595].

Nov. 1

Cash ......................................................................

32,541

Loss on Sale of Short-Term Investments .........

599

Short-Term Investments—Trading (D.Karan) ....

33,140

Sold Donna Karan shares

[(1,800 x $18.25) - $309].

Problem C-2A (40 minutes)

Part 1

2013

Apr. 16

Short-Term Investments—AFS (Gem) .........................

97,180

Cash ...............................................................................

97,180

Purchased 4,000 shares of Gem

[(4,000 x $24.25) + $180].

May. 1

Short-Term Investments—AFS (T-bills) .......................

100,000

Cash ................................................................

100,000

Purchased U.S. Treasury bills.

July 7

Short-Term Investments—AFS (Pepsi) ........................

98,675

Cash ................................................................

98,675

Purchased 2,000 shares of PepsiCo

[(2,000 x $49.25) + $175].

20

Short-Term Investments—AFS (Xerox) ........................

16,955

Cash ................................................................

16,955

Purchased 1,000 shares of Xerox

[(1,000 x $16.75) + $205].

Aug. 3

Cash ...............................................................................

101,500

Short-Term Investments—AFS (T-bills) .................

100,000

Interest Revenue ..........................................................

1,500

Proceeds of U.S. Treasury bills

($100,000 x .06 x 3/12).

15

Cash .....................................................................................

3,400

Dividend Revenue ..................................................

3,400

Received dividends on Gem (4,000 x $0.85).

28

Cash* ....................................................................................

59,775

Short-Term Investments—AFS (Gem)** .................

48,590

Gain on Sale of Short-Term Investments .............

11,185

Sold 2,000 shares of Gem.

*(2,000 x $30) - $225 **($97,180 x 2,000/4,000)

Oct. 1

Cash ..............................................................................

3,800

Dividend Revenue ............................................

3,800

Received dividends on PepsiCo (2,000 x $1.90).

Dec. 15

Cash .........................................................................

2,100

Dividend Revenue ............................................

2,100

Received dividends on Gem (2,000 x $1.05).

31

Cash .........................................................................

2,600

Dividend Revenue ............................................

2,600

Received dividends on PepsiCo (2,000 x $1.30).

Financial & Managerial Accounting, 5th Edition

1412

Problem C-2A (Continued)

Part 2

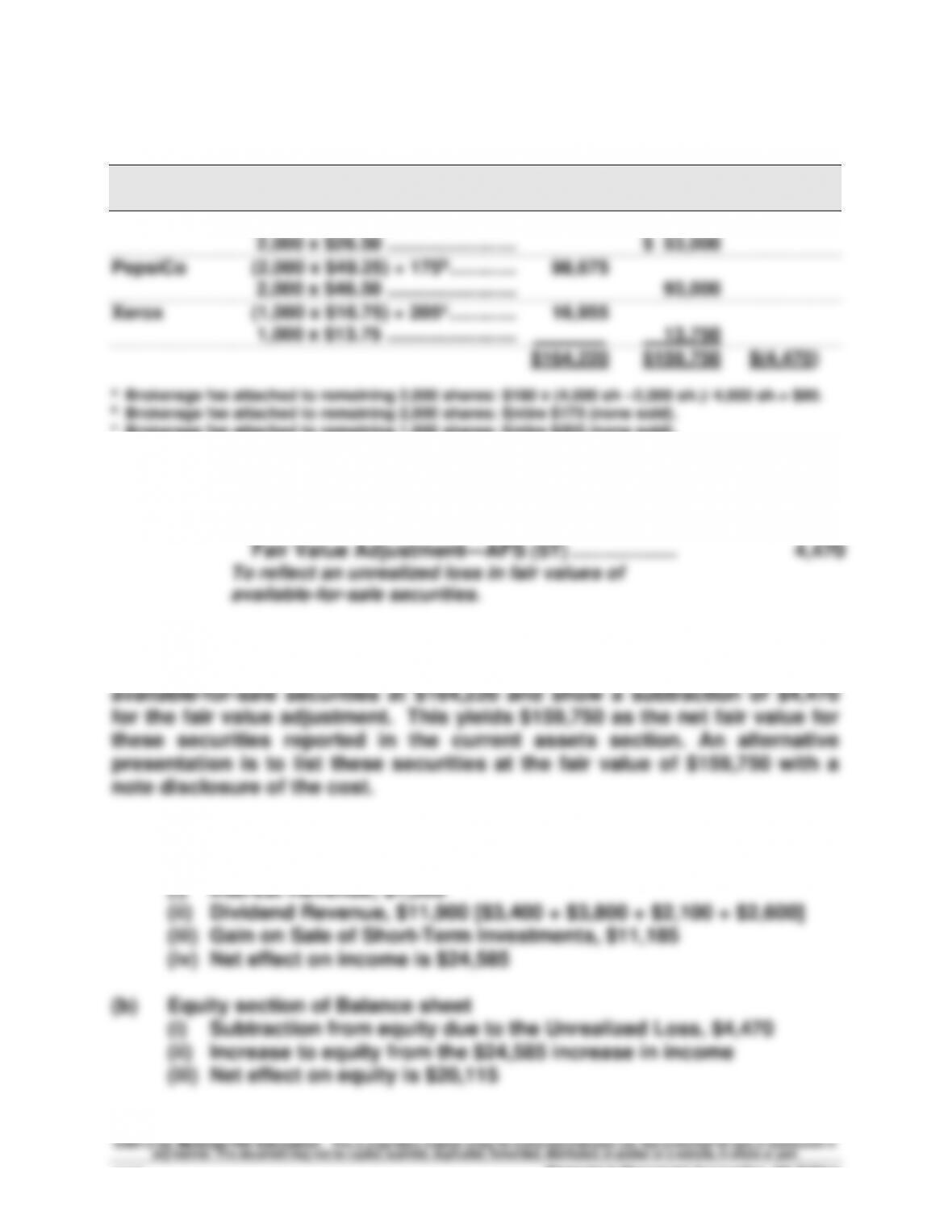

Comparison of Cost and Fair Values for AFS Portfolio

Unrealized

Cost Fair Value Gain (Loss)

Gem Co. (2,000 x $24.25) + 90a ............... $ 48,590

Part 3

Dec. 31

Unrealized Loss⎯Equity ................................................

4,470

Fair Value Adjustment—AFS (ST) .....................

4,470

To reflect an unrealized loss in fair values of

available-for-sale securities.

Part 4

The balance sheet would report the cost of these short-term investments in

Part 5

(a) Income statement

Problem C-3A (60 minutes)

Part 1

2013

Jan. 20

Long-Term Investments—AFS (J&J) .............................

20,740

Cash ..........................................................................

20,740

Purchased Johnson & Johnson

shares [(1,000 x $20.50) + $240].

Feb. 9

Long-Term Investments—AFS (Sony) ............................

55,665

Cash ..........................................................................

55,665

Purchased Sony shares

[(1,200 x $46.20) + $225].

June 12

Long-Term Investments—AFS (Mattel) ................................

40,695

Cash ....................................................................................

40,695

Purchased Mattel shares

[(1,500 x $27.00) + $195].

Dec. 31

Unrealized Loss⎯Equity ..............................................

3,650

Fair Value Adjustment—AFS (LT)* ..........................

3,650

Annual adjustment to fair values.

*

Cost

Fair Value

J & J ..................

$ 20,740

$ 21,500

Sony ..................

55,665

45,600

Mattel ................

40,695

46,350

Total ..................

$117,100

$113,450

J & J: 1,000 x $21.50 = $21,500

Sony: 1,200 x $38.00 = $45,600

Mattel: 1,500 x $30.90 = $46,350

Fair Adj.: $117,100 - $113,450 = $3,650

Financial & Managerial Accounting, 5th Edition

1414

Problem C-3A (Continued)

2014

Apr. 15

Cash ..........................................................................................

22,975

Gain on Sale of Investments ................................

2,235

Long-Term Investments—AFS (J&J) ................................

20,740

Sold Johnson & Johnson shares

[(1,000 x $23.50) - $525].

July 5

Cash ..........................................................................................

35,615

Loss on Sale of Investments ..................................................

5,080

Long-Term Investments—AFS (Mattel) ..............................

40,695

Sold Mattel shares [(1,500 x $23.90) - $235].

July 22

Long-Term Investments—AFS (Sara Lee) ................................

13,980

Cash ....................................................................................

13,980

Purchased Sara Lee shares

[(600 x $22.50) + $480].

Aug. 19

Long-Term Investments—AFS (Eastman Kodak) .......................

15,498

Cash ....................................................................................

15,498

Purchased Eastman Kodak shares

[(900 x $17.00) + $198].

Dec. 31

Unrealized Loss⎯Equity ........................................................

10,168

Fair Value Adjustment—AFS (LT)* ................................

10,168

Annual adjustment to fair values.

*

Cost

Fair Value

Kodak ...................

$15,498

$17,325

Sara Lee ...............

13,980

12,000

Sony .....................

55,665

42,000

Total .....................

$85,143

$71,325

Kodak: 900 x $19.25 = $17,325

Sara Lee: 600 x $20.00 = $12,000

Sony: 1,200 x $35.00 = $42,000

$85,143 - $71,325 = $13,818

Fair Value Adjustment account:

Required balance ..... $13,818 Cr.

Unadjusted balance.. 3,650 Cr.

Required change...… $10,168 Cr.

Problem C-3A (Continued)

2015

Feb. 27

Long-Term Investments—AFS (Microsoft) ................................

161,325

Cash ...................................................................................

161,325

Purchased Microsoft shares

[(2,400 x $67.00) + $525].

June 21

Cash .........................................................................................

56,720

Gain on Sale of Investments ................................

1,055

Long-Term Investments—AFS (Sony) ...............................

55,665

Sold Sony shares [(1,200 x $48.00) - $880].

June 30

Long-Term Investments—AFS (Black & Decker) ........................

50,835

Cash ...................................................................................

50,835

Purchased Black & Decker shares

[(1,400 x $36.00) + $435].

Aug. 3

Cash .........................................................................................

9,315

Loss on Sale of Investments ................................

4,665

Long-Term Investments—AFS (Sara Lee) ...........................

13,980

Sold Sara Lee shares

[(600 x $16.25) - $435].

Nov. 1

Cash .........................................................................................

19,850

Gain on Sale of Investments ................................

4,352

Long-Term Investments—AFS (E. Kodak) ..........................

15,498

Sold Eastman Kodak shares

[(900 x $22.75) - $625].

Dec. 31

Fair Value Adjustment—AFS (LT)* ................................

21,858

Unrealized Loss—Equity ................................

13,818

Unrealized Gain—Equity ...................................................

8,040

Annual adjustment to fair values.

*

Cost

Fair Value

Black & Decker .................

$ 50,835

$ 54,600

Microsoft ...........................

161,325

165,600

Total...................................

$212,160

$220,200

Black & Decker: 1,400 x $39.00 = $ 54,600

Microsoft: 2,400 x $69.00 = $165,600

$212,160 - $220,200 = $8,040 (fair value exceeds cost)

Fair Value Adjustment account:

Required balance ............ $ 8,040 Dr.

Unadjusted balance......... 13,818 Cr.

Required change ............. $21,858 Dr.

Financial & Managerial Accounting, 5th Edition

1416

Problem C-3A (Concluded)

Part 2

12/31/2013

12/31/2014

12/31/2015

Long-Term AFS Securities (cost)...................

$117,100

$85,143

$212,160

Fair Value Adjustment ...............................

(3,650)

(13,818)

8,040

Long-Term AFS Securities (fair value) ..........

$113,450

$71,325

$220,200

Part 3

2013

2014

2015

Realized gains (losses)

Sale of Johnson & Johnson shares .......

$ 2,235

Sale of Mattel shares ................................

(5,080)

Sale of Sara Lee shares ...........................

$(4,665)

Sale of Sony shares ................................

1,055

Sale of Eastman Kodak shares ...............

______

_______

4,352

Total realized gain (loss) ...........................

$ 0

$ (2,845)

$ 742

Unrealized gains (losses) at year-end*.....

$(3,650)

$(13,818)

$ 8,040

* Equals the balance of the Fair Value Adjustment account.

Problem C-4A (40 minutes)

Part 1

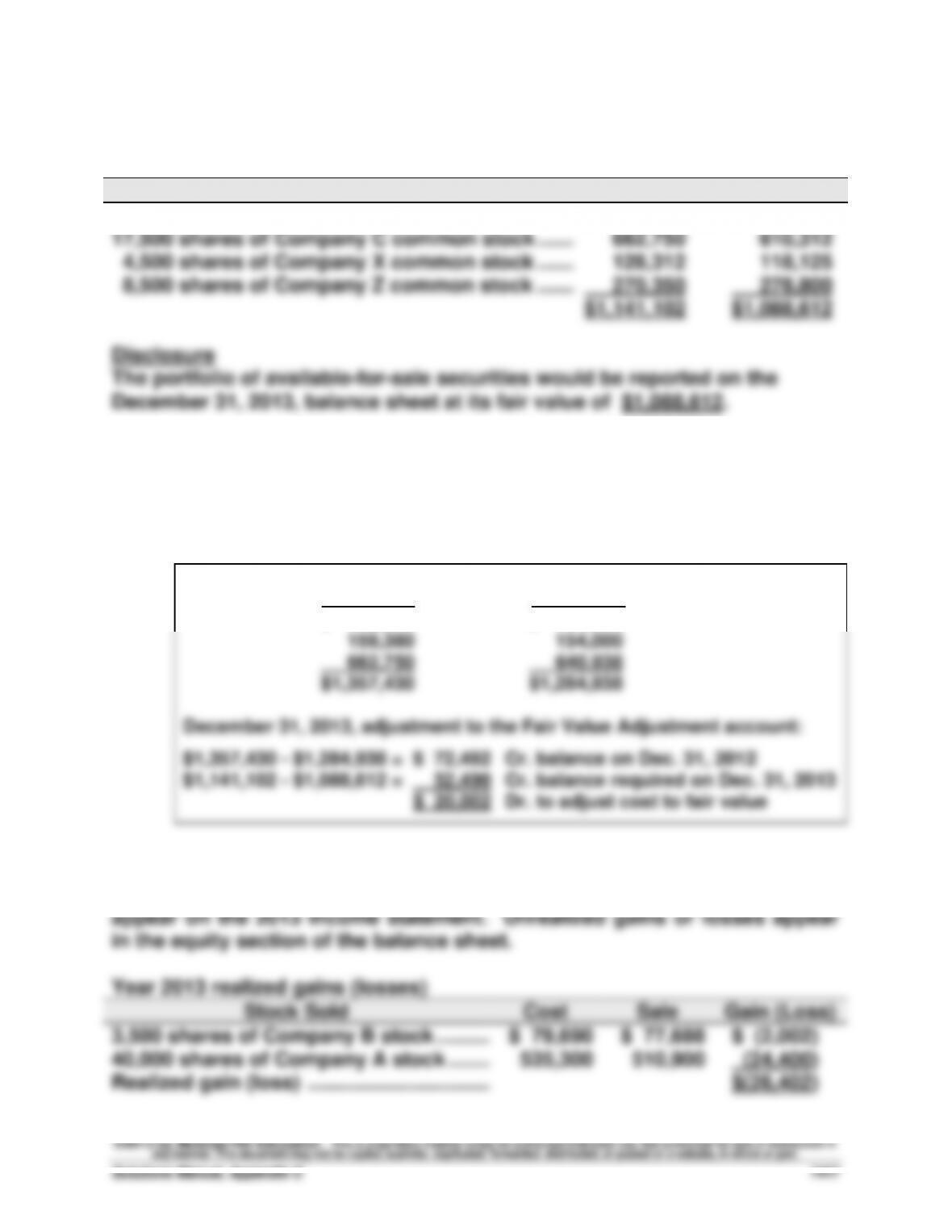

Available-for-sale securities on December 31, 2013

Security

Cost

Fair Value

3,500 shares of Company B common stock ..............

$ 79,690

$ 81,375

17,500 shares of Company C common stock ..............

662,750

610,312

4,500 shares of Company X common stock ..............

128,312

118,125

8,500 shares of Company Z common stock ..............

270,350

278,800

$1,141,102

$1,088,612

Disclosure

The portfolio of available-for-sale securities would be reported on the

December 31, 2013, balance sheet at its fair value of $1,088,612.

Part 2

Dec. 31

Fair Value Adjustment—AFS* ................................

20,002

Unrealized Loss—Equity ................................

20,002

Adjustment to fair value for AFS securities..

* December 31, 2012, available-for-sale securities

Cost _

Fair Value

$ 535,300

$ 490,000

159,380

154,000

662,750

640,938

$1,357,430

$1,284,938

December 31, 2013, adjustment to the Fair Value Adjustment account:

$1,357,430 - $1,284,938 = $ 72,492 Cr. balance on Dec. 31, 2012

$1,141,102 - $1,088,612 = 52,490 Cr. balance required on Dec. 31, 2013

$ 20,002 Dr. to adjust cost to fair value

Part 3

Only gains or losses realized on the sale of available-for-sale securities

Financial & Managerial Accounting, 5th Edition

1418

Problem C-5A (30 minutes)

Part 1

1. Journal entries (assuming significant influence)

2013

Jan. 5

Long-Term Investments—Kildaire ................................

1,560,000

Cash ................................................................

1,560,000

Purchased Kildaire shares.

Oct. 23

Cash ..........................................................................................

192,000

Long-Term Investments—Kildaire ................................

192,000

Received cash dividend (60,000 x $3.20).

Dec. 31

Long-Term Investments—Kildaire ................................

232,800

Earnings from Long-Term Investment ............................

232,800

Record equity in investee earnings

($1,164,000 x 20%).

2014

Oct. 15

Cash ..........................................................................................

156,000

Long-Term Investments—Kildaire ................................

156,000

Record cash dividend (60,000 x $2.60).

Dec. 31

Long-Term Investments—Kildaire ................................

295,200

Earnings from Long-Term Investment ............................

295,200

Record equity in investee earnings

($1,476,000 x 20%).

2015

Jan. 2

Cash ..........................................................................................

1,894,000

Gain on Sale of Investments ................................

154,000

Long-Term Investments—Kildaire* ................................

1,740,000

Sold Kildaire shares.

* Investment carrying value, January 2, 2015

Original cost ............................................

$1,560,000

Less 2013 dividends ...............................

(192,000)

Plus 2013 earnings ................................

232,800

Less 2014 dividends ...............................

(156,000)

Plus 2014 earnings ................................

295,200

Carrying value at date of sale .................

$1,740,000

Problem C-5A (Continued)

2. Carrying value per share, January 1, 2015 (see computations in part 1)

3. Change in Selk's equity due to stock investment

Earnings from Kildaire (2013) ................................

$232,800

Earnings from Kildaire (2014) ................................

295,200

Gain on sale of investments ................................

154,000

Net increase ................................................................

$682,000

Part 2

1. Journal entries (assuming NO significant influence)

2013

Jan. 5

Long-Term Investments—AFS (Kildaire) ................................

1,560,000

Cash ................................................................

1,560,000

Purchased Kildaire shares.

Oct. 23

Cash ..........................................................................................

192,000

Dividend Revenue .............................................................

192,000

Received cash dividend (60,000 x $3.20).

Dec. 31

Fair Value Adjustment—AFS (LT)* ................................

240,000

Unrealized Gain—Equity ................................

240,000

Record fair value adjustment.

*60,000 x $30.00 = $1,800,000

$1,800,000 - $1,560,000 = $240,000

2014

Oct. 15

Cash ..........................................................................................

156,000

Dividend Revenue .............................................................

156,000

Received cash dividends (60,000 x $2.60).

Dec. 31

Fair Value Adjustment—AFS (LT)* ................................

120,000

Unrealized Gain—Equity ................................

120,000

Record fair value adjustment.

*60,000 x $32.00 = $1,920,000

$1,920,000 - $1,560,000 = $360,000

$360,000 - $240,000 = $120,000

Financial & Managerial Accounting, 5th Edition

1420

Problem C-5A (Concluded)

2015

Jan. 2

Cash ..........................................................................................

1,894,000

Long-Term Investments—AFS (Kildaire) ............................

1,560,000

Gain on Sale of Investments ................................

334,000

Sold Kildaire shares.

Jan. 2

Unrealized Gain—Equity .........................................................

360,000

Fair Value Adjustment—AFS (LT) ................................

360,000

To remove fair value adjustment and related

accounts ($240,000 + $120,000 = $360,000).

2. Investment cost per share, January 1, 2015

3. Change in Selk’s equity due to stock investment

Dividend Revenue (2013) ...............................

$192,000

Dividend Revenue (2014) ...............................

156,000

Gain on sale of investments ..........................

334,000

Net increase ....................................................

$682,000