Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

AppC - Investments and International Operations

Appendix C

Investments and International Operations

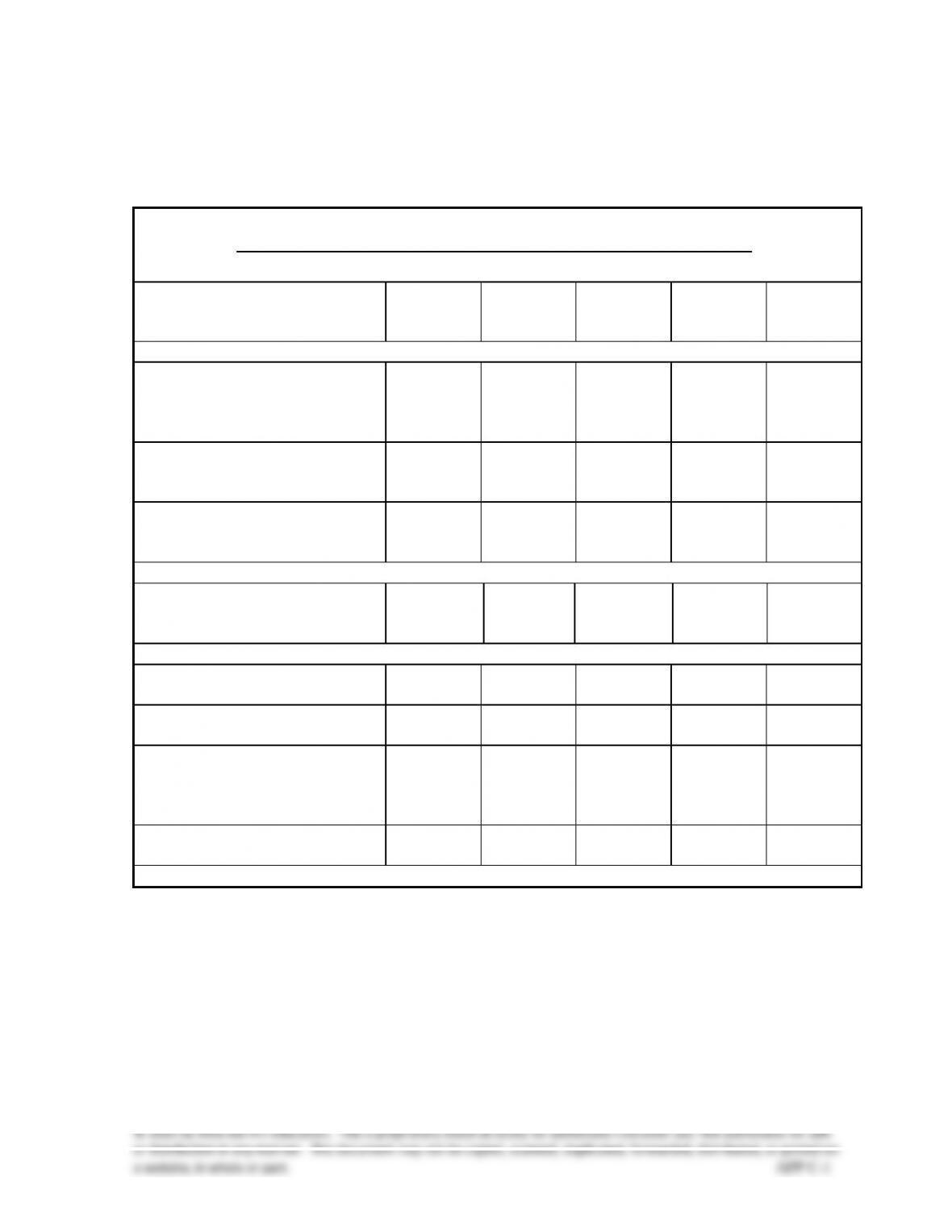

Student Learning Objectives and Related Assignment Materials*

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems

(A &B set)**

Beyond the

Numbers

Conceptual objectives:

C1. Distinguish between debt and

equity securities and between

short-term and long-term

investments.

1, 5, 8, 9, 10

C-5, C-6

C-4, C-12

TTN, TIA

C2. Describe how to report equity

securities with controlling

influence.

4, 17

C-6, C-11

C-5

C-4

TIA

C3. Explain foreign exchange rates

between currencies.

(Appendix C-A)

12, 13, 14

C-15, C-14

C-15, C-16

C-6

RIA, HTR,

ED

Analytical objectives:

Al. Compute and analyze the

components of return on total

assets.

18

C-12, C-13

C-14

RIA, CA,

GD

Procedural objectives:

P1. Account for trading securities.

2, 16

C-1, C-16

C-1, C-6,

C-8

C-1

TIA

P2. Account for held-to-maturity

securities.

C-7, C-9

C-2, C-8,

C-12

EC, TIA

P3. Account for available-for-sale

securities.

3, 6, 7, 15

C-2, C-3,

C-4, C-8,

C-10

C-3, C-7,

C-8, C-9,

C-10, C-11,

C-12, C-17

C-2, C-3,

C-4, C-5

EC, TIA

P4. Account for equity securities

with significant influence.

4, 11

C-9

C-12, C-13

C-4, C-5

CIP, TIA

Notes appear on next page.

AppC - Investments and International Operations

*Assignment materials that can be completed by students using:

Sage 50 and QuickBooks Pro 2013 templates – Problems C-1A and C-3A.

Excel template – None.

** The Serial Problem for Success Systems, which covers numerous learning objectives, can be

most of the chapters. Even if previous segments were not assigned, students can begin the segment

of the serial problem that is included in this chapter. It is most readily solved if students use the

Working Papers that accompany the book.)

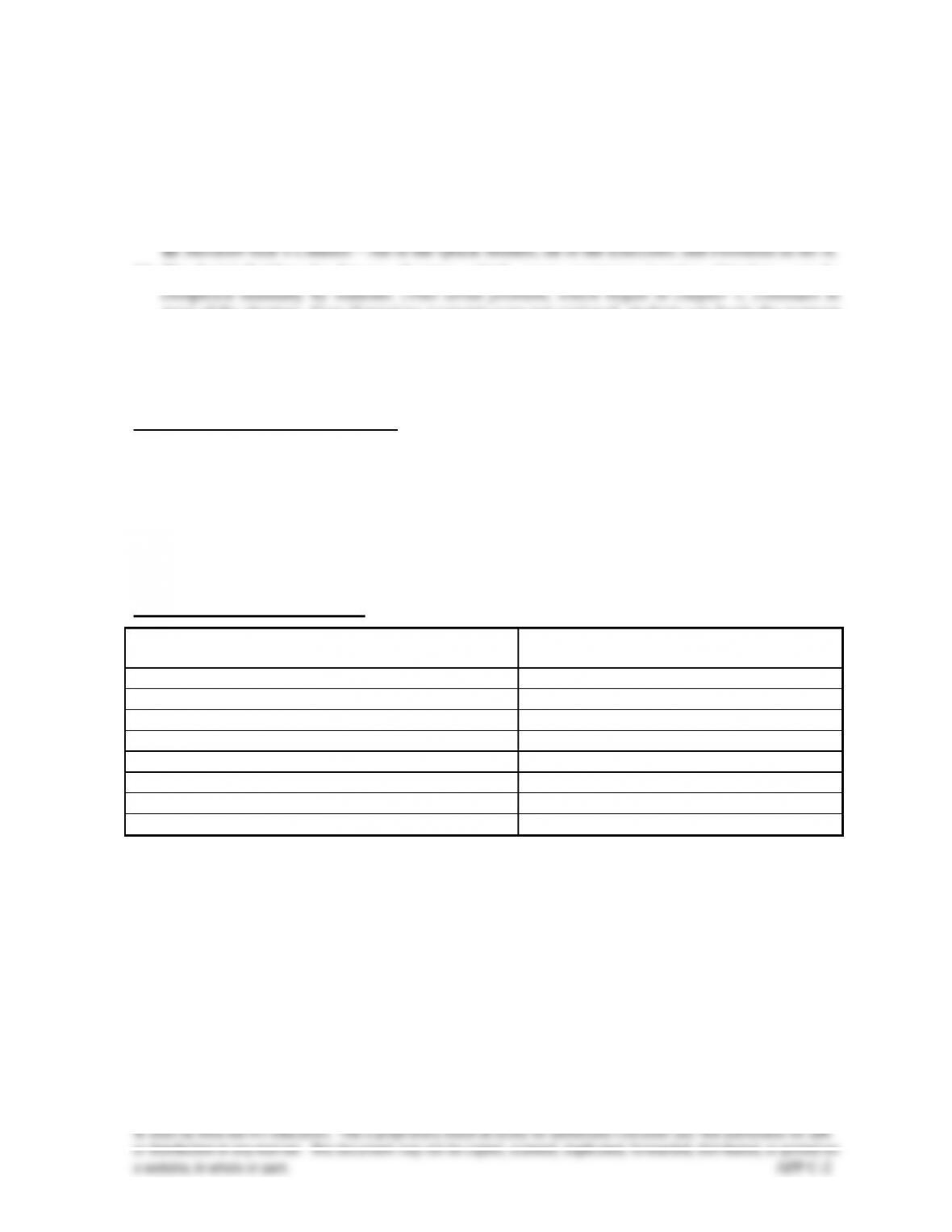

Synopsis of Chapter Revision

• myYearbook (MeetMe Inc.): NEW opener with new entrepreneurial assignment

• New discussion of the two optional presentations for comprehensive income per FASB

guidance in 2012

• Revised discussion of accounting for securities

• New reference to Greek debt in the context of international operations

PowerPoint® Show Slides

Chapter Learning Objective

PowerPoint® Slides

C1

6-8, 10-16

C2

9, 28-30

P1

17-18

P2

19-24

P3

20-21

P4

22-27

A1

31

C3

32-34

AppC - Investments and International Operations

Appendix Outline

Notes

I. Basics of Investments

A. Motivation for Investments

1. Companies transfer excess cash into investments to produce

higher income.

2. Some entities, such as mutual funds and pension funds, are set

up to produce income from investments.

3. Companies make investments for strategic reasons. Examples:

investments in competitors, suppliers, and even customers.

B. Short-Term versus Long-Term Investments

1. Short-term investments—current assets that must meet these

two requirements:

a. Expected to be converted into cash within one year or the

current operating cycle of the business, whichever is

longer.

b. Readily convertible to cash.

2. Long-term investments—investments not meeting the two

requirements for short-term investments.

3. Debt Securities versus Equity Securities debt securities

reflect a creditor relationship such as investments in notes,

bonds, and certificates of deposit. Equity securities reflect an

owner relationship such as shares of stock issued by

companies.

C. Classification and Reporting

1. Accounting for investments depends on three factors:

a. Security type, either debt or equity.

b. The company’s intent to hold the security either short-

term or long-term, and

c. The company’s (investor’s) percent ownership in the other

company’s (investee’s) equity securities.

d. Exhibit C.2 identifies five classes of securities using these

three factors.

D. Debt Securities: Accounting Basics

1. Acquisition: debt securities are recorded at cost when

purchased. They are classified as held-to-maturity (HTM)

securities. If they are short-term, they are classified as Short-

Term Investments (HTM).

2. Interest earned: interest revenue for investments in debt

securities is recorded when earned.

3. Disposition: when the bonds mature, the proceeds are recorded

as a debit to cash and a credit to Long-Term Investments

(HTM).

AppC - Investments and International Operations

Appendix Outline

Notes

E. Equity Securities: Accounting Basics

1. Acquisition: equity securities that are available-for-sale are

recorded at cost when acquired, including commissions or

brokerage fees paid.

2. Dividends earned: any cash dividends received are credited to

Dividend Revenue and reported in the income statement.

3. Disposition: when the securities are sold, the proceeds are

compared with cost, and any gain or loss is recorded.

report most noninfluential investments at fair value. Reporting

requirements depend on whether the investments are classified as trading,

held-to-maturity or available-for-sale.

A. Trading securities are debt and equity securities that the company

intends to actively manage and trade for profit. Frequent purchases and

sales are expected and are made to earn profits on short-term price

the portfolio of trading securities is reported on the income

statement in the Other Revenues and Gains (or Expenses and

B. Held-to-maturity - includes debt securities intended to be held to

maturity. Reported in current assets if their maturity dates are

within one year or operating cycle. Amortized cost method used for

reporting purposes. No fair value adjustment to the portfolio of

HTM securities.

C. Available-for-Sale Securities (AFS)

1. Available-for-sale includes debt and equity securities not

classified as trading or held-to-maturity. AFS securities are

purchased to yield interest, dividends or increases in fair value.

They are not actively managed.

2. Valuing and reporting AFS securities – companies adjust the

cost of the portfolio of AFS securities to reflect changes in fair

value through a fair value adjustment to its total portfolio cost.

AppC - Investments and International Operations

Appendix Outline

3. Selling AFS securities – identical to that described for the sale

of trading securities. The difference between the cost of the

individual securities sold and the net proceeds is recognized as

a gain or loss.

III. Reporting of Influential Investments

A. Investment in Securities with Significant Influence

A long-term investment classified as equity securities with

significant influence implies that the investor can exert significant

influence over the investee.

equity in the undistributed (distributed) earnings of the

investee.

the date of the sale.

B. Investment in Securities with Controlling Influence. A long-term

investment classified as equity securities with controlling

influence implies that the investor can exert a controlling influence

over the investee.

1. An investor who owns more than 50% of a company’s voting

stock has control over the investee. (In some cases, controlling

influence can extend to situations of less than 50%

ownership.)

2. The equity method with consolidation is used to account for

long-term investments in equity securities with controlling

influence.

a. The investor reports consolidated financial statements

when owning such securities. The controlling investor is

Notes

AppC - Investments and International Operations

Appendix Outline

Notes

called the parent and the investee is called the subsidiary.

b. Consolidated financial statements show the financial

position, results of operations, and cash flows of all

entities under the parent’s control, including all

subsidiaries; these statements are prepared as if the

business were organized as one entity.

c. The parent uses the equity method in its accounts, but the

investment account is not reported on the consolidated

financial statements.

C. Accounting Summary for Investments in Securities—See Exhibit

C.8 for a summary of the accounting for investments in securities.

D. Comprehensive Income

1. The term comprehensive income refers to all changes in

equity for a period except those due to investments and

distributions to owners. This means that it includes:

a. The revenues, gains, expenses, and losses reported in net

income, and

b. The gains and losses that bypass net income but affect

equity.

U.S. GAAP and IFRS.

1. Trading securities are accounted for using fair values with

comprehensive income as fair value change.

3. Held-to-maturity securities are accounted for using amortized

4. Both systems review held-to-maturity securities for impairment.

6. Under IFRS available-for-sale securities are referred to as

available-for-sale financial assets.

B. Accounting for Influential Securities – broadly similar across U.S.

GAAP and IFRS.

1. Under the equity method, the share of investee’s net income is

reported in the investor’s income in the same period the investee

earns that income.

AppC - Investments and International Operations

Appendix Outline

Notes

of investee income less the share of investee dividends.

3. Under the consolidation method, investee and investor revenues

and expenses are combined, absent intercompany transactions

and subtracting noncontrolling interests.

4. Nonintercompany assets and liabilities are similarly combined

and noncontrolling interests are subtracted from equity.

5. U.S. GAAP companies refer to earnings from long-term

investments as equity in earnings of affliates whereas IFRS

companies use equity in earnings of associated companies.

6. U.S. GAAP companies refer to noncontrolling interests in

consolidated subsidiaries are minority interess whereas IFRS

companies commonly use noncontrolling interests.

V. Decision Analysis—Components of Return on Total Assets

A. A company’s return on total assets is used to assess financial

performance.

B. It can be separated into two components: profit margin and total

asset turnover.

C. Return on total assets is calculated as profit margin x total asset

turnover.

D. Profit margin is calculated as net income divided by net sales. It

reflects the percent of net income in each dollar of net sales.

E. Total asset turnover is calculated as net sales divided by average

total assets. It reflects a company’s ability to produce net sales

from total assets.

F. Generally, if a company is to maintain or improve its return on

total assets, it must meet any decline in either profit margin or

total asset turnover with an increase in the other. If not, return on

assets will decline.

VI. Investments in International Operations (Appendix C-A)

Some entities’ operations occur in so many different countries that the

companies are called multinationals.

A. Exchange Rates between Currencies

The price of one currency stated in terms of another currency is

called a foreign exchange rate.

B. Sales and Purchases Listed in a Foreign Currency

1. When a U.S. company makes a credit sale to an international

customer, accounting for the sale and the accounts receivable

is straightforward if sales terms require the international

the U.S. company must account for the sale and the account

receivable in a different manner.

a. The sales price must be translated from the foreign

AppC - Investments and International Operations

a website, in whole or part. APP C-8

Appendix Outline

Notes

currency to dollars by multiplying the sales price (stated in

the foreign currency) by the exchange rate on the date of

the sale; entry (for U.S. company) for sale of merchandise

on credit: debit Accounts Receivable, credit Sales

b. If the receivable is still outstanding at the end of the end of

the accounting period, the receivable must again be

translated from the foreign currency to dollars by

multiplying the sales price (stated in the foreign currency)

by the exchange rate at the end of the accounting period.

Entry assuming the amount of the receivable (when

translated) is higher: debit Accounts Receivable, credit

Foreign Exchange Gain.

3. When payment is received from the foreign customer, the U.S.

company will immediately exchange the payment into dollars.

Entry assuming the amount of the payment (when translated)

is lower: debit Cash, debit Foreign Exchange Loss, credit

Accounts Receivable.

4. The balance in the Foreign Exchange Gain (or Loss) account

is reported on the income statement and closed to the Income

Summary account at year-end.

C. Consolidated Statements with International Subsidiaries

Before preparing consolidated statements, the parent must

translate financial statements of a foreign subsidiary into U.S.

dollars.

AppC - Investments and International Operations

a website, in whole or part. APP C-9

Appendix C – Alternate Demonstration Problem #1

2013

Jan

1

Purchased 8,000 shares (20%) of Investee Company’s outstanding

stock at a cost of $150,000.

May

31

Investee Company declared and paid a cash dividend of $1.50 per

share.

Dec

31

Investee Company announced that its net income for the year was

$100,000.

2014

Oct

1

Investee Company declared and paid a cash dividend of $1.00 per

share.

Dec

31

Investee Company announced that its net income for the year was

$80,000.

2015

Jan

1

Investor Corporation sold all of its shares of Investee Company

for $178,000 cash.

Required:

Prepare journal entries on Investor Corporation’s books using the equity

method, which assumes that Investor has significant influence over

Investee Company.

AppC - Investments and International Operations

a website, in whole or part. APP C-10

Solution: Appendix C – Alternate Demonstration Problem #1

2013

Jan

1

Long-Term Investment--Investee Stock ..

150,000

Cash ......................................................

150,000

May

31

Cash ............................................................

12,000

Long-Term Investment--Investee Stock

12,000

Dec

31

Long-Term Investment--Investee Stock ..

20,000

Earnings from Long-Term Investment

--Investee Stock ...............................

20,000

2014

Oct

1

Cash ............................................................

8,000

Long-Term Investment--Investee Stock

8,000

Dec

31

Long-Term Investment--Investee Stock ..

16,000

Earnings from Long-Term Investment

--Investee Company ........................

16,000

2015

Jan

1

Cash ............................................................

178,000

Long-Term Investment--Investee Stock

166,000

Gain on Sale of Investments ..............

12,000