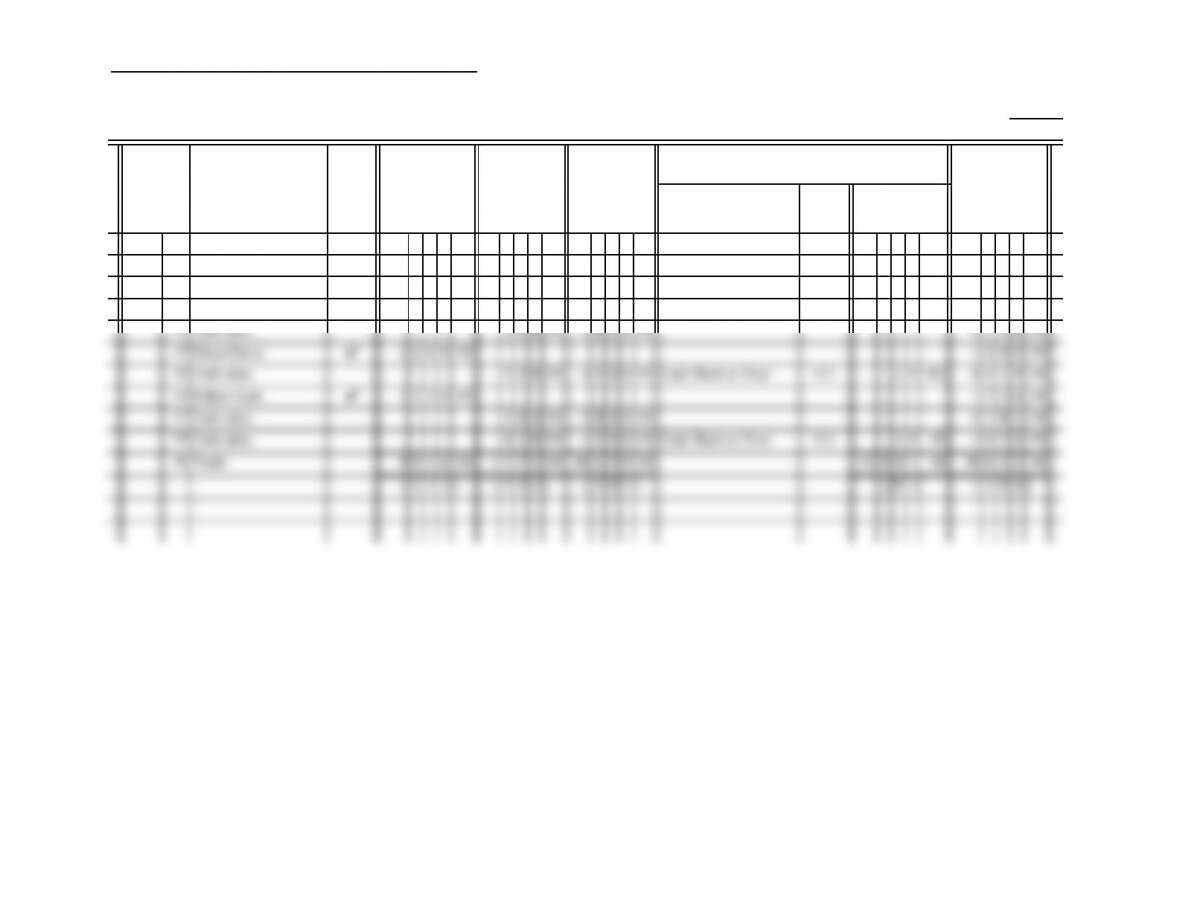

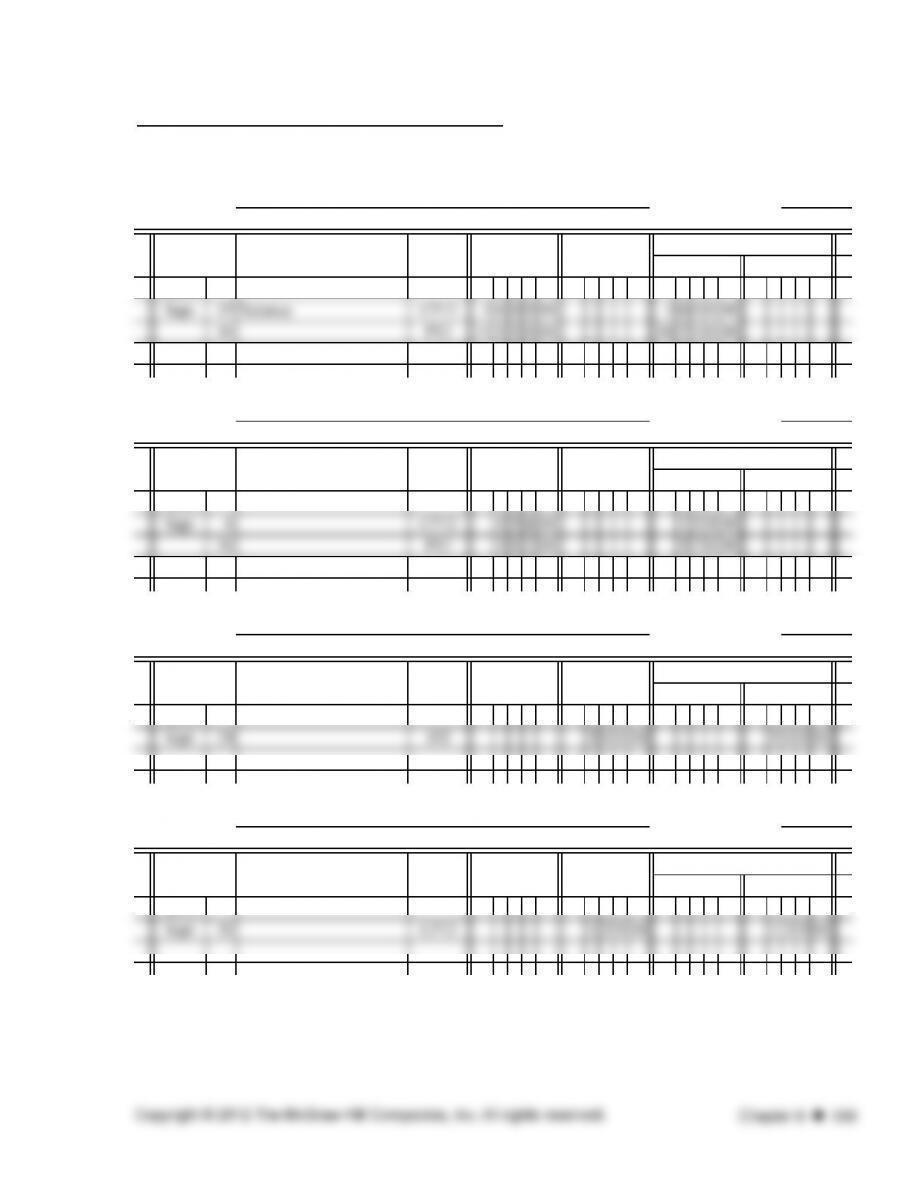

CRITICAL THINKING PROBLEM 9.1 (continued)

PAGE

PURCHASED

FROM

INVOICE

NUMBER

INVOICE

DATE TERMS

POST.

REF.

2013

Sept. 6

Reed Millings

Company 827 9/3 2/10, n/30 ✔445000 445000

PURCHASES JOURNAL 12

DATE

ACCOUNTS

PAYABLE

PURCHASES

DEBIT

FREIGHT-IN

DEBIT

352 Chapter 9 Copyright © 2012 The McGraw-Hill Companies, Inc. All rights reserved.

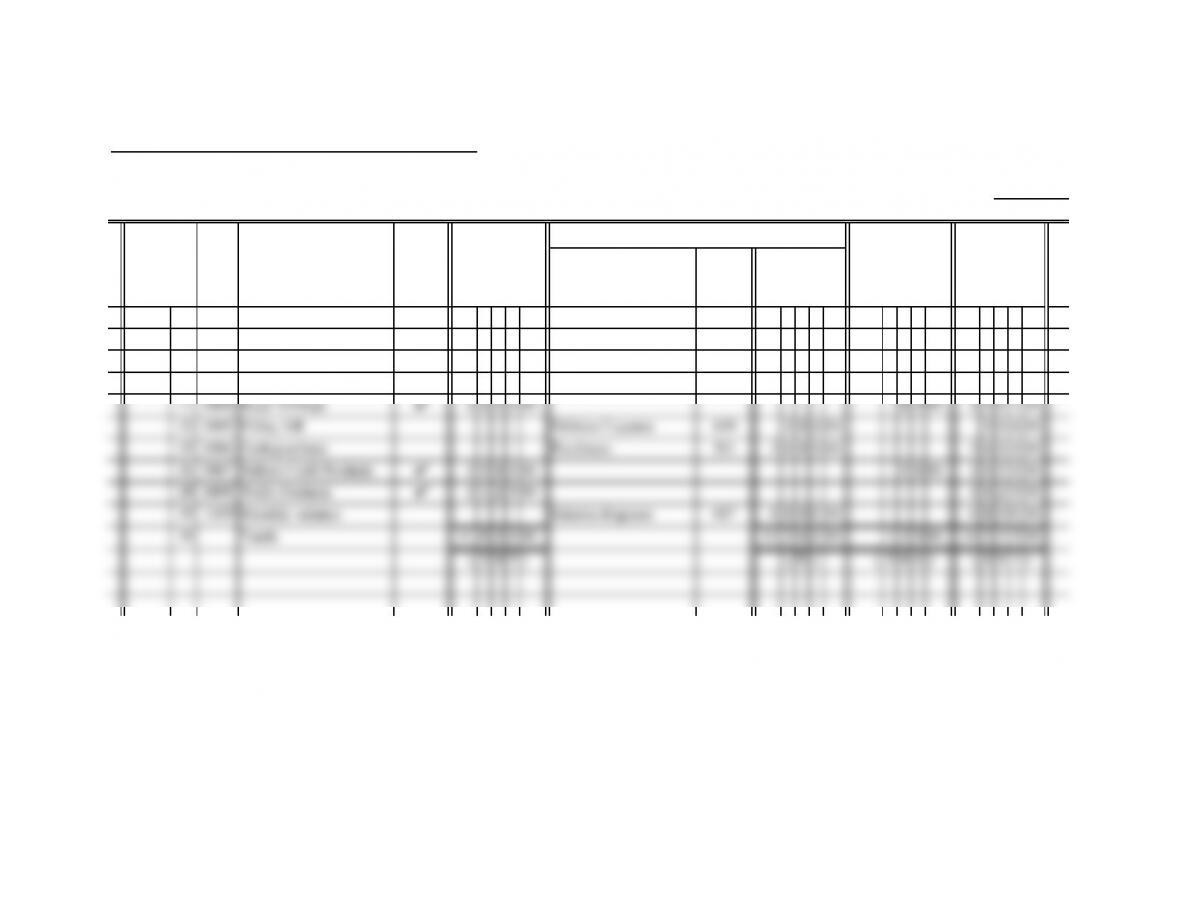

CRITICAL THINKING PROBLEM 9.1 (continued)

PAGE

POST.

REF.

1

2013

1

GENERAL JOURNAL 32

DATE DESCRIPTION DEBIT CREDIT

1 2013 1

2 Sept. 8 121 3 7 0 00 2

205

✔37000

4 Bought store supplies, Invoice 4204 dated 4

5 September 6, net amount due in 30 days 5

6 6

Supplies

3Accounts Payable/Rocker Company3

6

6

205

5

5

0

0

00

12

Accounts

12

17

23

23

28

on

28

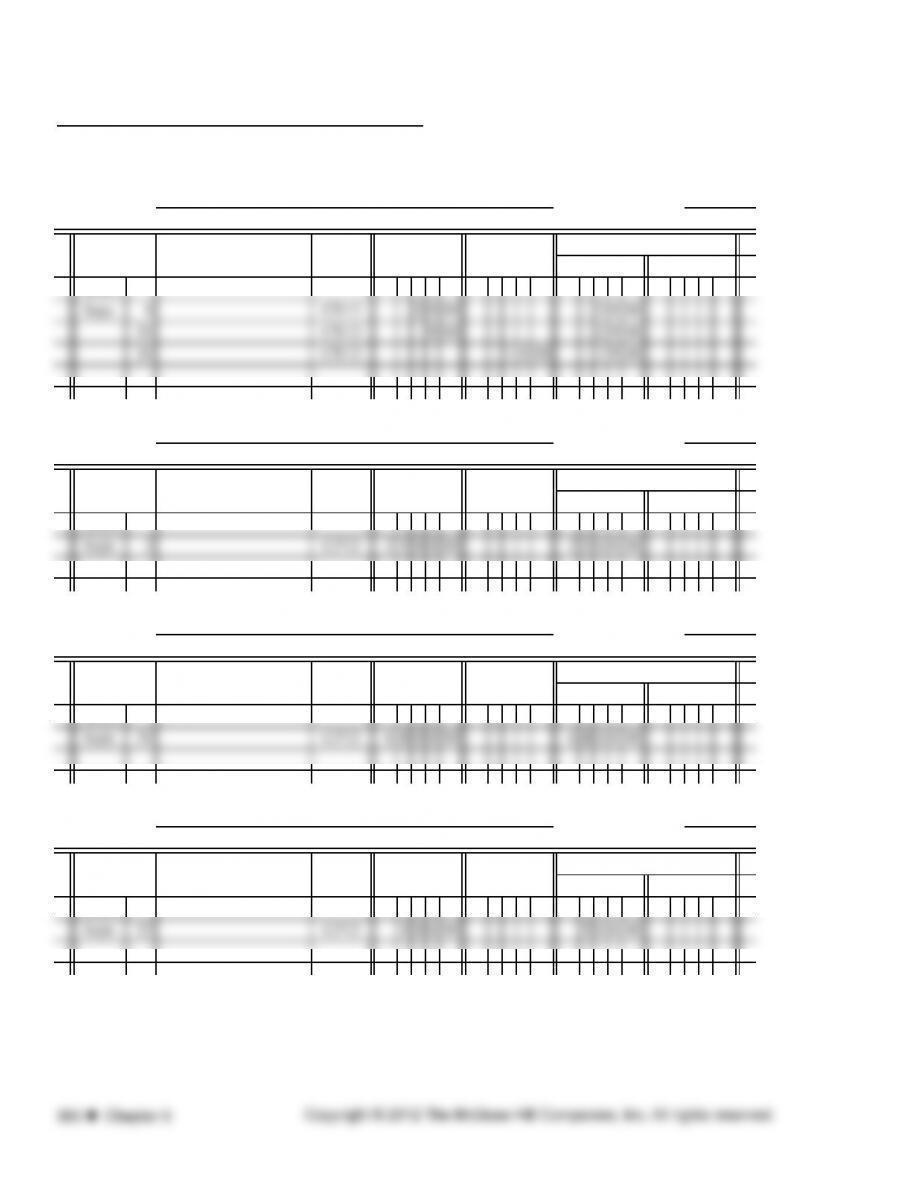

CRITICAL THINKING PROBLEM 9.1 (continued)

PAGE

ACCOUNT NAME

POST.

REF.

2013

Sept. 1 David Prater ✔1050 00 1050 00

5 Additional investment Sergio Cortez, Capital 301 15000 00 15000 00

6 Cash sales 3 1 2 00 390000Cash Short or Over 611 ( 2 0 00) 4192 00

12

CASH DEBITAMOUNTDATE DESCRIPTION

POST.

REF.

ACCOUNTS

RECEIVABLE

CREDIT

SALES TAX

PAYABLE

CREDIT

CASH RECEIPTS JOURNAL

SALES

CREDIT

OTHER ACCOUNTS CREDIT

CRITICAL THINKING PROBLEM 9.1 (continued)

PAGE

ACCOUNT NAME

POST.

REF.

2013

Sept. 1 1401 Sadler Floor Coverings ✔194000 194000

2 1402 Monthly rent Rent Expense 614 250000 250000

6 1403 Freight charge Freight-In 502 1 5 8 00 1 5 8 00

ACCOUNTS

PAYABLE

DEBIT

OTHER ACCOUNTS DEBIT

PURCHASES

DISCOUNT

CREDIT

12

CASH

CREDITAMOUNTDATE

CK.

NO. DESCRIPTION

POST.

REF.

CASH PAYMENTS JOURNAL

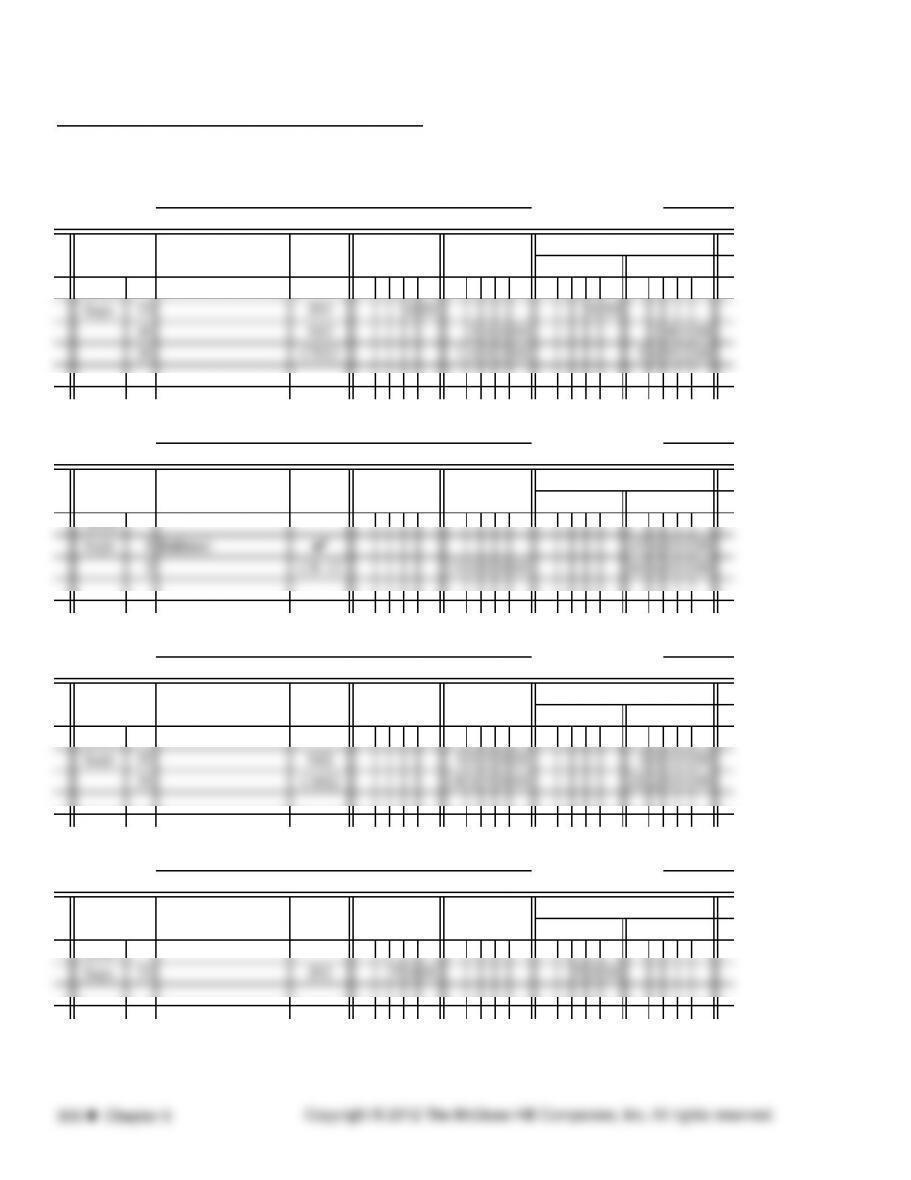

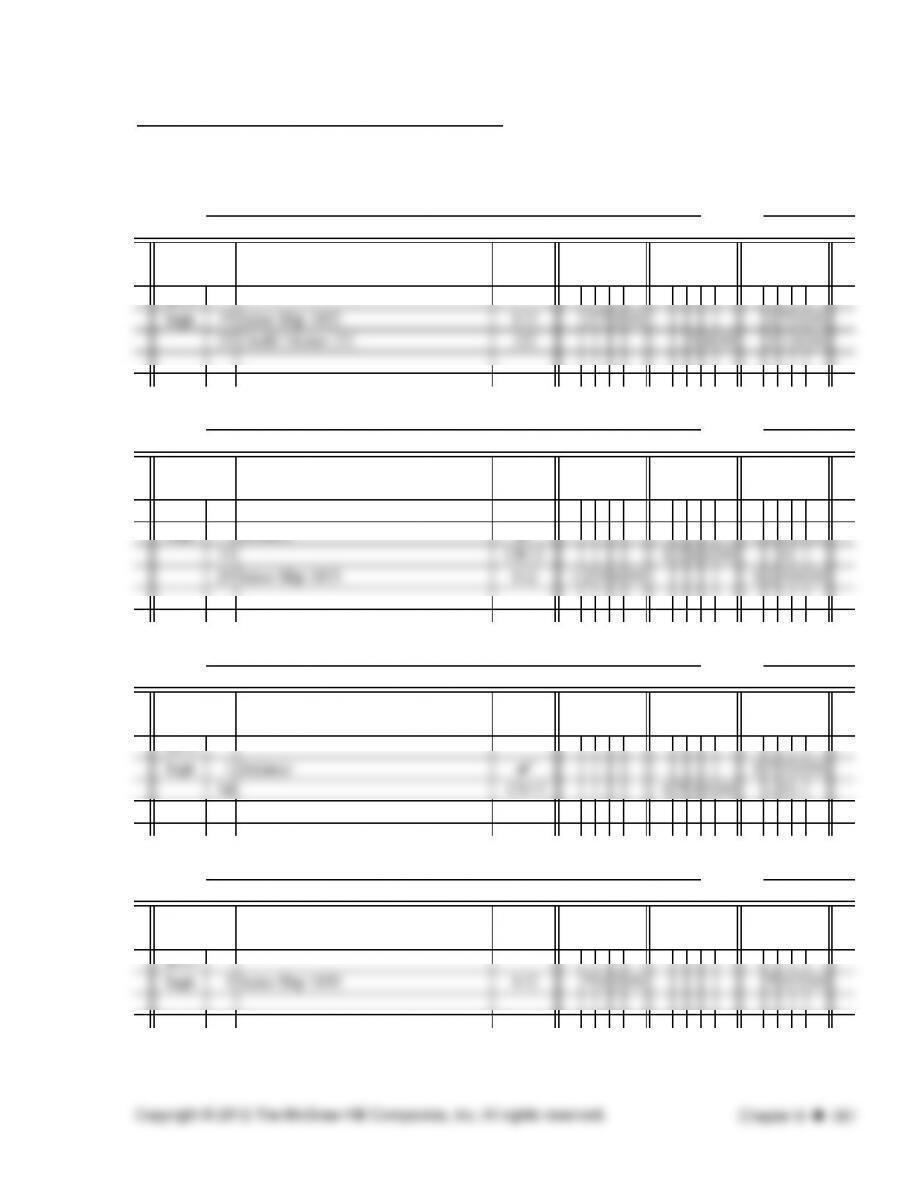

CRITICAL THINKING PROBLEM 9.1 (continued)

ACCOUNT Cash ACCOUNT NO.

2013

ACCOUNT Notes Receivable ACCOUNT NO.

2013

ACCOUNT Accounts Receivable ACCOUNT NO.

2013

Sept. 1 Balance ✔614000

DATE

BALANCE

CREDITDESCRIPTION DEBIT

CREDIT

DESCRIPTION DEBIT

DESCRIPTION

CREDIT

109

POST.

REF.

BALANCE

BALANCE

POST.

REF.

CREDIT

CREDIT

DEBIT

DEBIT CREDIT

DEBIT

111

POST.

REF.

GENERAL LEDGER

DEBIT

DATE

101

DATE

CRITICAL THINKING PROBLEM 9.1 (continued)

ACCOUNT Supplies ACCOUNT NO.

ACCOUNT Inventory ACCOUNT NO.

ACCOUNT Notes Payable ACCOUNT NO.

2013

ACCOUNT Accounts Payable ACCOUNT NO.

2013

Sept. 1 Balance ✔956000

DESCRIPTION

POST.

REF. CREDIT

CREDIT

GENERAL LEDGER

DESCRIPTION

DEBIT

BALANCE

DEBIT CREDIT

121

DEBIT

BALANCE

DATE

131

DATE

DATE DESCRIPTION

DEBIT

BALANCE

POST.

REF.

CREDIT

DEBIT

DEBIT

CREDIT

BALANCE

CREDIT

CREDIT

201

205

CREDIT

DATE DESCRIPTION

POST.

REF. DEBIT

POST.

REF. DEBIT

CRITICAL THINKING PROBLEM 9.1 (continued)

ACCOUNT Sales Tax Payable ACCOUNT NO.

2013

ACCOUNT Sergio Cortez, Capital ACCOUNT NO.

ACCOUNT Sales ACCOUNT NO.

2013

ACCOUNT Sales Returns and Allowances ACCOUNT NO.

2013

GENERAL LEDGER

CREDIT

451

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

CREDIT

401

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT

CREDIT

301

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT

231

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT

CRITICAL THINKING PROBLEM 9.1 (continued)

ACCOUNT Purchases ACCOUNT NO.

2013

ACCOUNT Freight-In ACCOUNT NO.

2013

ACCOUNT Purchases Returns and Allowances ACCOUNT NO.

2013

ACCOUNT Purchases Discounts ACCOUNT NO.

2013

GENERAL LEDGER

501

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

502

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

503

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

504

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

CRITICAL THINKING PROBLEM 9.1 (continued)

ACCOUNT Cash Short or Over ACCOUNT NO.

2013

ACCOUNT Rent Expense ACCOUNT NO.

2013

ACCOUNT Salaries Expense ACCOUNT NO.

2013

ACCOUNT Utilities Expense ACCOUNT NO.

2013

619

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

CREDIT

617

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

CREDIT

614

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT

GENERAL LEDGER

611

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT

CRITICAL THINKING PROBLEM 9.1 (continued)

NAME Rachel Carter TERMS n/30

DESCRIPTION

POST.

REF.

2013

NAME Mesia Davis TERMS n/30

DESCRIPTION

POST.

REF.

2013

Sept. 1 Balance ✔126000

NAME Robert Kent TERMS n/30

DESCRIPTION

POST.

REF.

NAME Pam Lawrence TERMS n/30

DESCRIPTION

POST.

REF.

CREDIT

DATE DEBIT CREDIT BALANCE

CREDIT

CREDIT

DATE BALANCEDEBIT

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

DATE

DEBITDATE

BALANCEDEBIT

BALANCE

CRITICAL THINKING PROBLEM 9.1 (continued)

NAME David Prater TERMS n/30

DESCRIPTION

POST.

REF.

2013

NAME Henry Tolliver TERMS n/30

DESCRIPTION

POST.

REF.

NAME Jason Williams TERMS n/30

DESCRIPTION

POST.

REF.

2013

21600

DATE DEBIT CREDIT

DATE DEBIT CREDIT

Interior Designs Specialty Shop

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

DATE DEBIT CREDIT BALANCE

BALANCE

BALANCE

Schedule of Accounts Receivable

September 30, 2013

Rachel Carter

CRITICAL THINKING PROBLEM 9.1 (continued)

NAME Booker, Inc. TERMS

DESCRIPTION

POST.

REF.

2013

NAME McKnight Corporation TERMS

DESCRIPTION

POST.

REF.

2013

NAME Nelson Craft Products TERMS

DESCRIPTION

POST.

REF.

2013

NAME Reed Millings Company TERMS

DESCRIPTION

POST.

REF.

2013

DATE DEBIT CREDIT

DEBIT CREDIT BALANCE

DATE DEBIT CREDIT BALANCE

DATE DEBIT CREDIT BALANCE

ACCOUNTS PAYABLE SUBSIDIARY LEDGER

2/10, n/30

2/10, n/30

n/45

1/10, n/30

BALANCE

DATE

CRITICAL THINKING PROBLEM 9.1 (continued)

NAME Rocker Company TERMS

DESCRIPTION

POST.

REF.

2013

NAME Sadler Floor Coverings TERMS

DESCRIPTION

POST.

REF.

2013

NAME Wells Products TERMS

DESCRIPTION

POST.

REF.

2013

n/30

n/30

ACCOUNTS PAYABLE SUBSIDIARY LEDGER

n/30

DATE

CREDIT BALANCE

DEBIT BALANCE

DEBIT CREDIT BALANCE

CREDIT

DATE DEBIT

DATE

CRITICAL THINKING PROBLEM 9.2

1658900

499200

2158100

Scavone Builders

Bank Reconciliation Statement

August 31, 2013

Balance on bank statement

Addition: Deposit in transit, August 28

Deductions for outstanding checks

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

1. a. No assurance money taken actually accounted for.

b. A gap in the control of cash exists, and unauthorized expenditures can be made.

c. Increases the opportunity for theft; no current cash position is known.

d. Increases risk of theft.

e. Weakens internal control over cash receipts.

2. To pay bills in a timely fashion, anticipate fund shortages or overages, and take advantage of

investment opportunities.

3. Errors noted by the bank may not be communicated to management.

4. a. Yes. Blank endorsements are not secure.

b. Yes. Checkbook should be kept in a locked drawer and should be available only to specified

employees.

c. Yes. To deter fraud, different tasks should be assigned to different employees.

d. Yes. Reconciliation should be done soon after receiving bank statement.

e. Yes. Financial records should be maintained for a reasonable number of years in case of a tax audit.

f. No. Most firms write several checks monthly, and the task would be impractical.

5. Essential assets should be safeguarded against loss and theft.

6. Up-to-date cash position; information for day-to-day business decisions.

7. Insures again losses.

8. Control of cash; audit trail.

Ethical Dilemma:

No, this was not an ethical action, as it was not Daniel’s money.

Daniel should admit his theft and make arrangements to repay the amount stolen.

Financial Statement Analysis:

1. 10.20%

2. Increased by $902 million.

3. The balance reported for “Cash and cash equivalents” would be understated by $125,000.

Teamwork:

A Sales Invoice for each job should be given to each customer with a place to incorporate any

additions or subtractions for service. Any changes must be communicated to the home office and an

approval number will be given. The Sales Invoice, as well as each change, should be signed by the

customer. Only cash and money orders should be allowed since the families have just moved and do

not currently have a local bank.

Internet Connection:

Each bank should list the possible interest rates, both variable and fixed. Most banks will be within a

few tenths of points of each other.

366 Chapter 9 Copyright © 2012 The McGraw-Hill Companies, Inc. All rights reserved.

SOLUTIONS TO PRACTICE TEST

Part A True-False

Part B Matching