Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

• Once an order is generated, indi creates a customized garment and ships it to the customer for free

within 4 weeks.

• All orders come with a Perfect Fit Promise and Worry-Free Shopping Guarantee, which promises fit

adjustments until 100% satisfaction or customer’s money back.

• The average price for a pair of indi jeans is $185.

• indiTailored – sister company to indi – offers customers in search of the perfect dress shirt the same

customization, fit and delivery options as indieDenim.

• Customer dissatisfaction: Businesses who extend credit to their customers risk customer

dissatisfaction if accounts are not updated frequently.

• Ineffective collection efforts: Effective accounts receivable collection efforts rely on accurate

account balances.

• Cash flow: Negative cash flow situations may stem from improper maintenance of accounts

receivable or from delayed accounts receivable billings.

1. Retail: sell goods directly to consumers. Wholesale: sell goods to retailers.

3. Subtract balance of Sales Returns and Allowances from balance of Sales.

5. Contra revenue account.

7. Time of sale; Sales Tax Pa

y

able.

9. a. Debit Accounts Receivable, credit Sales, b. Debit Accounts Receivable from Credit Card

Companies, credit Sales.

11. The credit card company.

ACCOUNTING FOR SALES AND ACCOUNTS RECEIVABLE

CHAPTER 7

Students should recognize that technology is an important factor in the success of a merchant like

indieDenim. As a direct merchant, indieDenim customers shop directly with them — from home or office,

by phone, mail, fax or Web. They ship directly to their customers. Their direct merchant method of doing

business makes shopping simpler, faster and more convenient.

Fast Facts

Note to instructor : These questions are designed to check students’ understanding of the new terms,

concepts, and procedures presented in the chapter.

Discussion Questions

Chapter Opener: Thinking Critically

Managerial Implications: Thinking Critically

A company which fails to maintain up-to-date accounts receivable records may face the following:

Discussion Questions (continued)

13.

15.

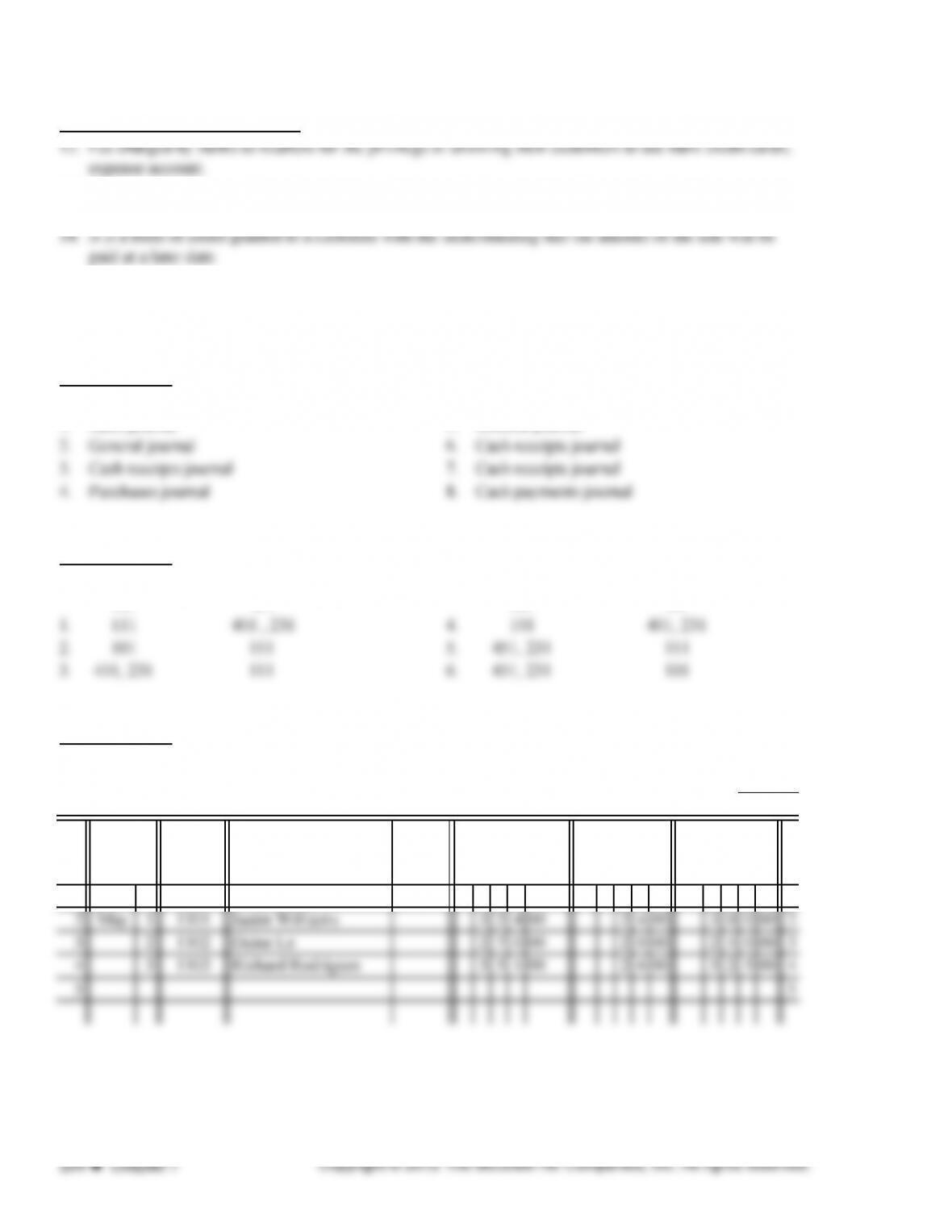

EXERCISE 7.1

1. Sales journal 5. General journal

EXERCISE 7.2

Cr.

EXERCISE 7.3

PAGE

1 2013 1

2 May 1 1101 Justin Williams 3 2 4 00 2 4 00 3 0 0 00 2

3 2 1102 Daine Le 2 7 0 00 2 0 00 2 5 0 00 3

4 3 1103 Richard Rodrigues 3 5 1 00 2 6 00 3 2 5 00 4

5 5

expense account.

The bank deposits cash from the sale to the business checking account the same day the sale is

authorized.

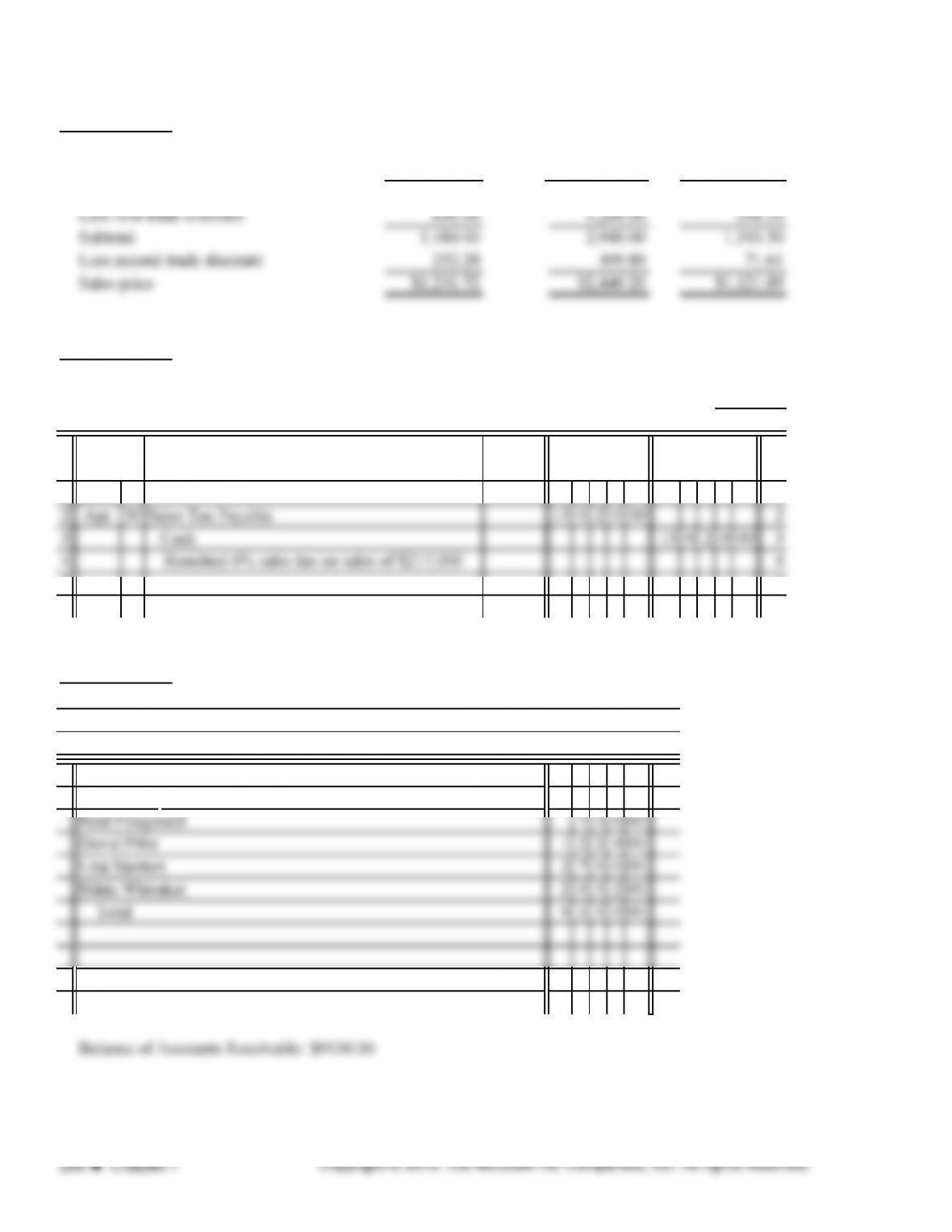

A trade discount is a reduction from the list, or suggested retail, price. Different trade discounts are

offered to different customers, based on the size of the order or other factors.

Dr.

SALES JOURNAL

Dr.

Cr.

SALES

CREDIT

CUSTOMER’S

NAME

POST.

REF.

ACCOUNTS

RECEIVABLE

DEBIT

SALES TAX

PAYABLE

CREDITDATE

SALES

SLIP

NO.

18

EXERCISE 7.4

PAGE

POST.

REF.

15GENERAL JOURNAL

DEBIT CREDITDATE DESCRIPTION

1 2013 1

2 June 5 6 0 0 00 2

3 4 8 00 3

Sales Tax Payable

Sales Returns and Allowances

EXERCISE 7.5

1.

2.

The $6,480 debit is posted to Accounts Receivable (111). July 31 is entered in the date column, S1 in

the Post. Ref. column, and $6,480 in the Debit column. The balance is increased by this amount.

The $480 credit is posted to Sales Tax Payable (231). July 31 is entered in the Date column, S1 in the

EXERCISE 7.7

1

List price $2,120.00

$4,200.00

23

$1,550.00

EXERCISE 7.10

ACCOUNT Accounts Receivable ACCOUNT NO.

BALANCE

111

POST.

GENERAL LEDGER

2013

DEBITCREDIT CREDITDEBITDATE DESCRIPTION

POST.

REF.

ACCOUNT Sales Tax Payable ACCOUNT NO.

2013

231

DEBIT CREDIT

BALANCE

DEBITDATE DESCRIPTION

POST.

REF. CREDIT

2013

Sales Returns and Allowances ACCOUNT NO. 451

ACCOUNT

2013

DEBITDATE

BALANCE

DEBIT CREDITCREDITDESCRIPTION

POST.

REF.

NAME Cara Fountain TERMS

POST

n/30

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

DESCRIPTION

POST

.

REF.

2013

BALANCEDATE DEBIT CREDIT

EXERCISE 7.10 (continued)

NAME Sadie Palmer TERMS

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGE

R

n/30

POST.

REF.

2013

CREDITDATE DESCRIPTION

DEBIT BALANCE

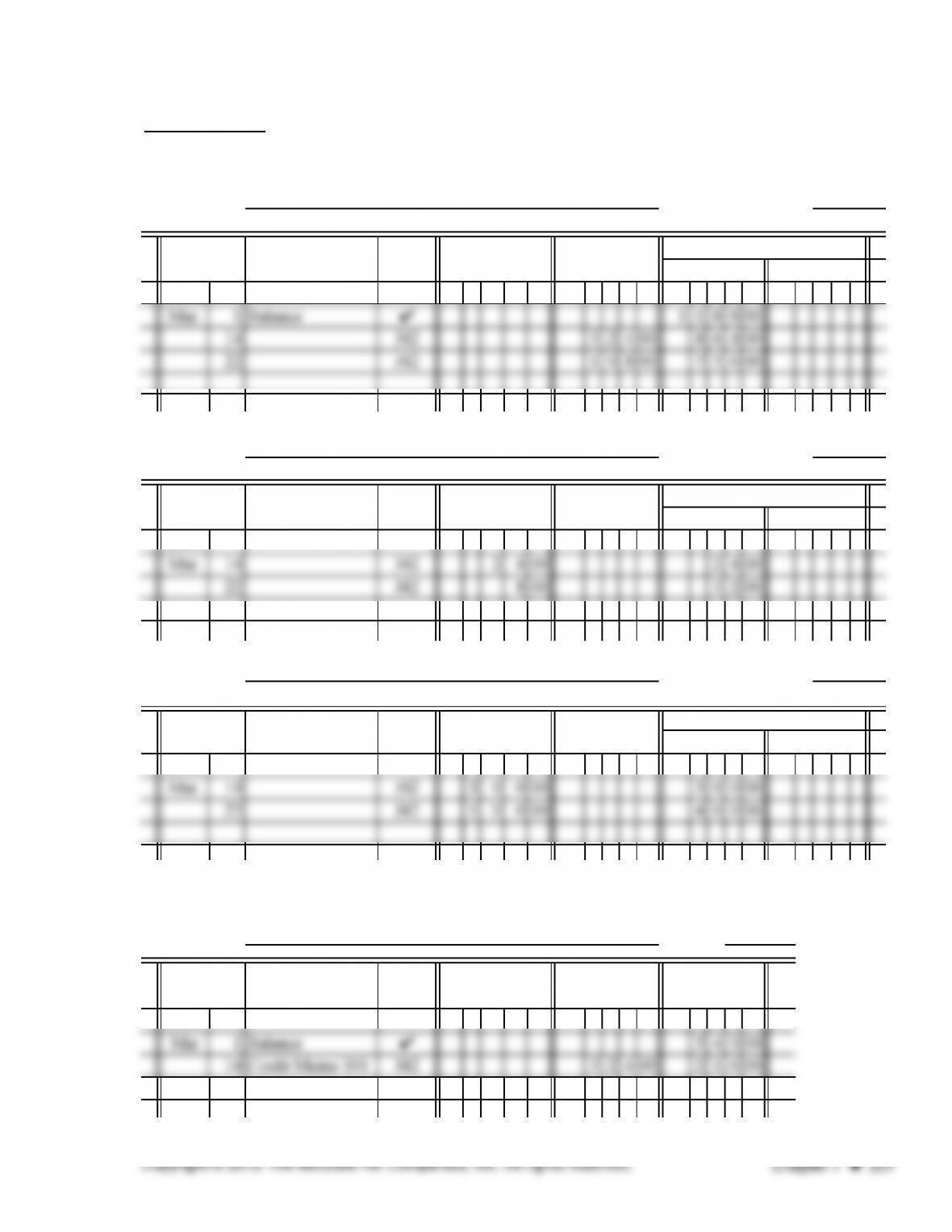

PROBLEM 7.1A

Page

SALES

SLIP

NO

CUSTOMER’S

NAME

POST.

REF

SALES

CREDIT

ACCOUNTS

RECEIVABLE

DEBIT

SALES TAX

PAYABLE

CREDIT

DATE

SALES JOURNAL 8

NO

.

NAME

REF

.

1 2013 1

2 July 1 501 Perry Martin 9 7 2 00 7 2 00 9 0 0 00 2

3 6 502 Cindy Han 234900 17400 217500 3

CREDIT

DEBIT

CREDIT

DATE

ACCOUNT Accounts Receivable ACCOUNT NO.

PROBLEM 7.1A (continued)

GENERAL LEDGER

111

BALANCE

2013

POST.

REF.DATE DESCRIPTION CREDITDEBIT CREDIT

BALANCE

DEBIT

ACCOUNT Sales Tax Payable ACCOUNT NO.

DATE DESCRIPTION

POST.

REF.

231

DEBIT CREDIT

BALANCE

DEBIT CREDIT

PROBLEM 7.2A

PAGE

SALES ACCOUNTS

SALES JOURNAL

SALES

TAX

8

1 2013 1

2 Feb. 1 1615 4 9 0 3 20 3 6 3 20 4 5 4 0 00 2

3 5 1616 2 2 6 8 00 1 6 8 00 2 1 0 0 00 3

Sun Yoo

Jacqueline Moore

DATE

SLIP

NO.

POST.

REF.

RECEIVABL

E DEBIT

PAYABLE

CREDITCUSTOMER’S NAME

SALES

CREDIT

PROBLEM 7.2A (continued)

ACCOUNT Accounts Receivable ACCOUNT NO.

2013

Feb. 1 Balance ✔1563600

ACCOUNT Sales Tax Payable ACCOUNT NO.

2013

Feb. 1 Balance ✔7 170 00

ACCOUNT Sales ACCOUNT NO.

2013

ACCOUNT Sales Returns and Allowances ACCOUNT NO.

111

DATE

BALANCE

DEBIT CREDITDESCRIPTION

POST.

REF. DEBIT CREDIT

231

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

401

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

GENERAL LEDGER

451

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

PROBLEM 7.2A (continued)

3506500

PROBLEM 7.3A

PAGE 6

1 2013 1

2 Nov. 1 1001 Pauline Judge ✔1620 00 12000 150000 2

3 5 1002 Janet Hutchinson ✔2268 00 16800 210000 3

12 12

Month Ended February 28, 2013

Revenue

Sales

Armik's Furniture

DATE

SALES

SLIP

NO.

CUSTOMER’S

NAME

POST.

REF.

ACCOUNTS

RECEIVABLE

DEBIT

SALES TAX

PAYABLE

CREDIT

SALES

CREDIT

SALES JOURNAL

Income Statement (Partial)

PROBLEM 7.3A (continued)

PAGE

DATE CREDITDESCRIPTION

16GENERAL JOURNAL

DEBIT

POST.

REF.

1 2013 1

2 Nov. 17 1 5 0 00 2

312003

Accounts Receivable/Lisa Morgan 4

231

111 2

✔

00

451

4 6

Sales Returns and Allowances

Sales Tax Payable

1

PROBLEM 7.3A (continued)

ACCOUNT Sales Tax Payable ACCOUNT NO.

2013

ACCOUNT Sales ACCOUNT NO.

ACCOUNT Sales Returns and Allowances ACCOUNT NO.

2013

NAME Euline Brock TERMS

DESCRIPTION

POST.

REF.

2013

CREDIT

BALANCE

DEBIT

DEBIT

POST.

REF.

CREDIT BALANCE

DATE

CREDIT

DEBIT CREDITDESCRIPTION

DESCRIPTION DEBIT

DATE

GENERAL LEDGER

BALANCE

DEBIT CREDIT

CREDITDESCRIPTION

n/30

BALANCE

DEBIT CREDIT

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

DATE

231

401

451

DATE

POST.

REF. DEBIT

POST.

REF.

PROBLEM 7.3A (continued)

NAME Charles Brown TERMS

DESCRIPTION

POST.

REF.

2013

NAME Janet Hutchinson TERMS

DESCRIPTION

POST.

REF.

2013

NAME Pauline Judge TERMS

DESCRIPTION

POST.

REF.

2013

NAME Lisa Morgan TERMS

DESCRIPTION

POST.

REF.

2013

CREDIT BALANCE

n/30

n/30

n/30

CREDIT

DEBIT

DATE DEBIT

BALANCEDATE DEBIT

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

CREDIT BALANCE

BALANCEDATE DEBIT CREDIT

n/30

DATE

PROBLEM 7.3A (continued)

NAME Henry Okafor TERMS

DESCRIPTION

POST.

REF.

2013

NAME Dorothy Watts TERMS

DESCRIPTION

POST.

REF.

2013

NAME Winnie Wu TERMS

DESCRIPTION

POST.

REF.

2013

DATE DEBIT CREDIT

DEBIT

CREDITDATE DEBIT

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

CREDIT

BALANCE

n/30

n/30

n/30

BALANCE

BALANCE

DATE

PROBLEM 7.3A (continued)

Euline Brock 410400

Charles Brown 7 5 6 00

Janet Hutchinson 226800

PROBLEM 7.4A

PAGE

INVOICE

NO.

POST.

REF.

1 2013 1

2 Jan. 3 1081 ✔500 00 2

3 8 1082 ✔775 00 3

8 25 1087 ✔427 00 8

9 27 1088 ✔925 00 9

10 31 4779 00 10

11 (1 1 1/ 4 01) 11

12 12

Moore’s Flower Shop

ACCOUNTS

RECEIVABLE

DR./ SALES CR.CUSTOMER’S NAME

7

Carter Garden Supply

Thomas Florist

Total

SALES JOURNAL

The Dining Elegance China Shop

Schedule of Accounts Receivable

November 30, 2013

Thomas Florist

DATE

PROBLEM 7.4A (continued)

PAGE

1 2013 1

DEBIT

POST.

REF.DESCRIPTION

GENERAL JOURNAL 11

CREDITDATE

1

2013

1

2 Jan. 15 5 0 00 2

3

3 00

✔

Sales Returns and Allowances

Accounts Receivable/Thomasville Flower Shop 05

451

111

PROBLEM 7.4A (continued)

ACCOUNT ACCOUNT NO.

GENERAL LEDGER

Sales Returns and Allowances 451

2013

DEBIT DEBIT

BALANCE

CREDITDATE DESCRIPTION

POST.

REF. CREDIT

NAME Applegate Nursery TERMS

POST

n/45

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

DESCRIPTION

POST

.

REF.

2013

CREDITDATE DEBIT BALANCE

Carter Garden Supply TERMS

DESCRIPTION

POST.

REF.

2013

NAME

DATE BALANCECREDITDEBIT

n/45

NAME Cedar Hill Floral Shop TERMS

POST.

REF

n/45

DESCRIPTION REF.

2013

DATE DEBIT CREDIT BALANCE

PROBLEM 7.4A (continued)

NAME Moore’s Flower Shop TERMS n/45

ACCOUNTS RECEIVABLE SUBSIDIARY LEDGER

DESCRIPTION

POST.

REF.

2013

BALANCEDATE DEBIT CREDIT

NAME Thomas Florist TERMS

DESCRIPTION

POST.

REF.

2013

BALANCE

n/45

DATE DEBIT CREDIT

2013

Thomasville Flower Shop TERMS

DESCRIPTION

POST.

REF.

2013

DATE

NAME n/45

BALANCEDEBIT CREDIT

PROBLEM 7.4A (continued)

Applegate Nursery 6 8 0 00

Carter Garden Supply 7 7 5 00

Cedar Hill Floral Shop 4 8 0 00

PROBLEM 7.1B

PAGE

1 2013 1

2 June 1 201 Fatima Fakih 113400 8400 105000 2

3 6 202 Gilbert Gomez 9 9 9 00 7 4 00 9 2 5 00 3

Special Occasions Flower Shop

Schedule of Accounts Receivable

January 31, 2013

DATE

SALES

SLIP

NO.

8

CUSTOMER’S

NAME

POST.

REF.

SALES

CREDIT

SALES TAX

PAYABLE

CREDIT

ACCOUNTS

RECEIVABL

E DEBIT

SALES JOURNAL