• William Boeing founded Pacific Aero Products Company in 1916; the name was changed to Boeing

in 1917.

• In 1917, the company employed 28 people. In 2007, Boeing employed more than 150,000 people in

48 U.S. states and 70 foreign countries.

• Boeing is the largest contractor working for NASA.

• Along with the ISS, the Boeing Company manufactures and services commercial airplanes, military

aircraft, helicopters, a variety of electronic defense systems, and advanced communication systems.

• Boeing’s 2006 sales were $61.5 billion from customers in 145 countries. International sales accounted

for nearly 30 percent of total sales.

Assets are depreciated because they have a limited life and will be used up over time. Depreciation is

the allocation of the cost of the asset over its useful life.

1. Debit Depreciation Expense—Machine, $250; Credit Accum. Depr. – Machine, $250.

3. Expense items that are acquired and paid for in advance of their use.

Supplies, prepaid rent, prepaid insurance, and advertising.

5. b, d, f, g, and i are depreciated. Only long-term tangible assets are subject to depreciation.

7. a. decrease b. none c. none d. decrease

9. Asset cost, accumulated depreciation, book value.

11. Cost of asset less accumulated depreciation.

13.

ADJUSTMENTS AND THE WORKSHEET

CHAPTER 5

Students should suggest that accountants estimate the amount of wear and tear on the equipment. This

expense should be charged against the income earned during that same period. The concept of adjustments

and depreciation can be introduced at this time.

Fast Facts

Charges off an equal amount of cost of asset during each accounting period in asset’s useful life.

Discussion Questions

Chapter Opener: Thinking Critically

Managerial Implications: Thinking Critically

Note to instructor : These questions are designed to check students’ understanding of new terms, concepts,

and procedures presented in the chapter.

EXERCISE 5.1

1. Rent Expense, $900 Dr.

2. Supplies Expense, $4,400 Dr.

3. Depreciation Expense—Equipment, $500 Dr.

EXERCISE 5.2

1. Insurance Expense, $250 Dr.

2. Advertising Expense, $1,250 Dr.

EXERCISE 5.3

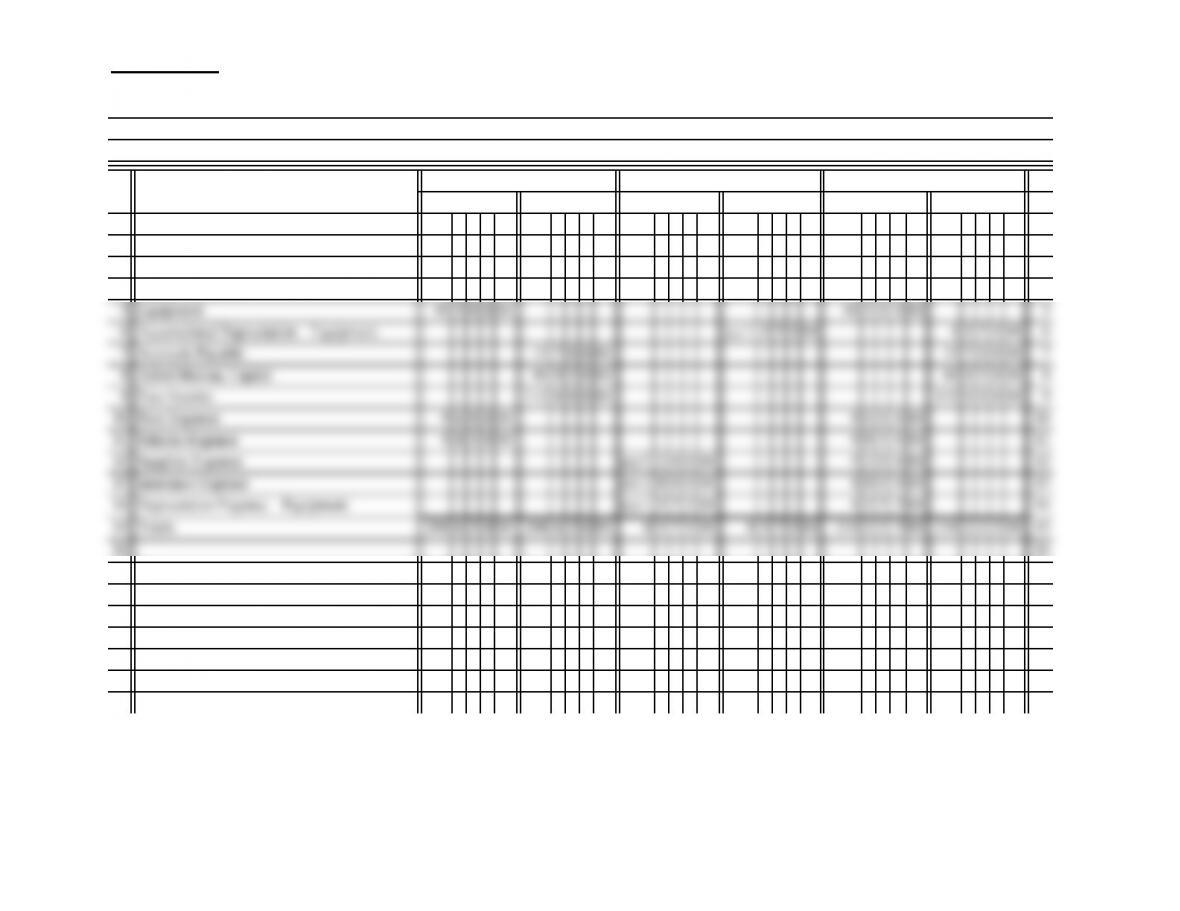

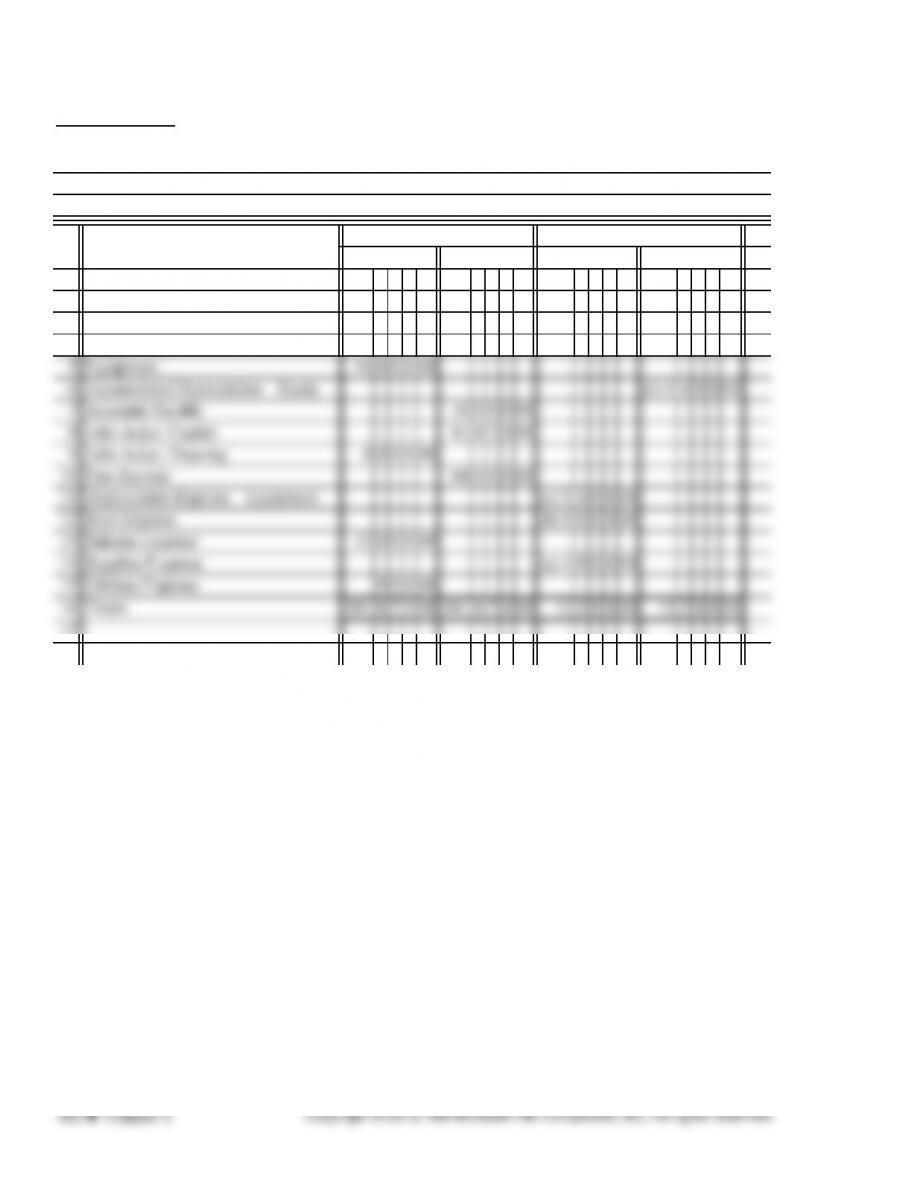

1 Cash 62 0 0 0 00 62 0 0 0 00 1

2 Accounts Receivable 21 5 0 0 00 21 5 0 0 00 2

3 Supplies 800000 (a) 5 2 0 0 00 2 8 0 0 00 3

4 Prepaid Insurance 720000 (b) 1 8 0 0 00 5 4 0 0 00 4

17 17

18 18

19 19

20 20

21 21

22 22

Herron Company

Worksheet (Partial)

Month Ended January 31, 2013

ACCOUNT NAME TRIAL BALANCE

DEBIT CREDIT

ADJUSTMENTS

DEBIT CREDIT

ADJUSTED TRIAL BALANCE

DEBIT CREDIT

EXERCISE 5.4

Net Income Before Adjustments $80,000

Less Adjustments:

EXERCISE 5.5

PAGE

POST.

REF.

1 1

2 2013 2

3 Dec. 31 Supplies Expense 523 1000000 3

Adjusting Entries

3

DATE DESCRIPTION DEBIT CREDIT

GENERAL JOURNAL

EXERCISE 5.5 (continued)

ACCOUNT Supplies ACCOUNT NO.

ACCOUNT Prepaid Insurance ACCOUNT NO.

2013

ACCOUNT Accumulated Depreciation—Equipment ACCOUNT NO.

ACCOUNT Depreciation Expense—Equipment ACCOUNT NO.

2013

CREDIT

DESCRIPTION

POST.

REF. DEBIT

BALANCE

131

GENERAL LEDGER

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT

121

DATE DESCRIPTION

POST.

REF. DEBIT

DATE DESCRIPTION

POST.

REF. DEBIT

DATE

142

517

CREDIT

BALANCE

DEBIT CREDIT

BALANCE

DEBIT CREDIT

CREDIT

CREDIT

CREDIT DEBIT

EXERCISE 5.5 (continued)

ACCOUNT Insurance Expense ACCOUNT NO.

2013

ACCOUNT Supplies Expense ACCOUNT NO.

2013

DESCRIPTION

DEBIT

GENERAL LEDGER

CREDITDATE

BALANCE

DEBIT

DATE DESCRIPTION CREDIT CREDIT

521

523

POST.

REF. CREDIT

BALANCE

DEBIT

POST.

REF. DEBIT

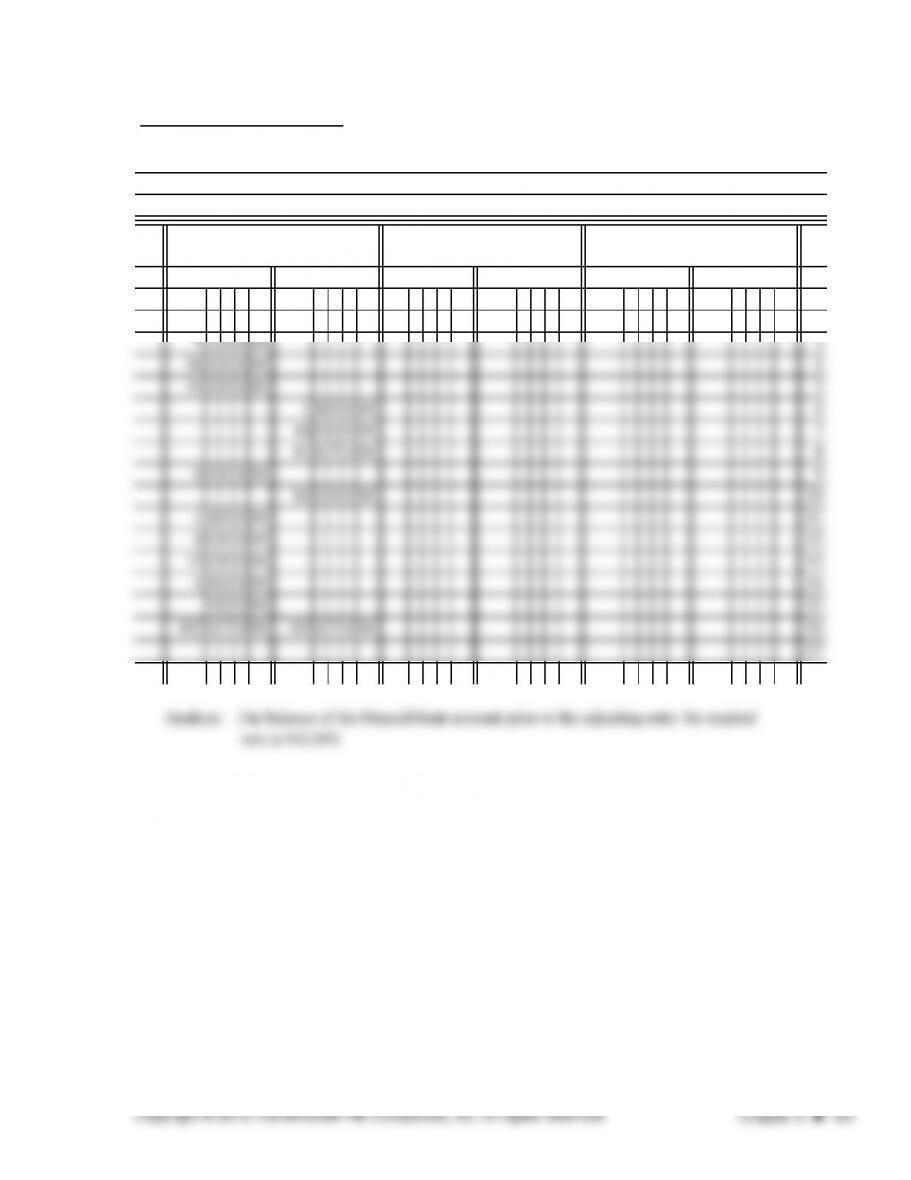

PROBLEM 5.1A

Dumas Company

Worksheet (Partial)

Month Ended January 31, 2013

1 Cash 10400000

2 Accounts Receivable 2080000

3 Supplies 3840000 (a) 32 0 0 0 00

4 Prepaid Insurance 6000000 (b) 10 0 0 0 00

18

19

ACCOUNT NAME

ADJUSTMENTS

DEBIT CREDIT

TRIAL BALANCE

CREDITDEBIT

PROBLEM 5.1A (continued)

10400000 10400000 1

2080000 2080000 2

640000 640000 3

3200000 3200000 11

1000000 1000000 12

3120000 3120000 13

220000 220000 14

ADJUSTED TRIAL BALANCE INCOME STATEMENT BALANCE SHEET

DEBIT CREDIT DEBIT CREDIT DEBIT CREDIT

PROBLEM 5.2A

The University Bookstore

Worksheet (Partial)

1 Cash 45 1 5 0 00

2 Accounts Receivable 662400

3 Supplies 12 0 0 0 00 (a) 4 8 0 0 00

4 Prepaid Rent 42 0 0 0 00 (b) 6 0 0 0 00

Month Ended November 30, 2013

ACCOUNT NAME

TRIAL BALANCE ADJUSTMENTS

DEBIT CREDIT DEBIT CREDIT

PROBLEM 5.2A (continued)

45 1 5 0 00 1

662400 2

ADJUSTED TRIAL

BALANCE INCOME STATEMENT BALANCE SHEET

DEBIT CREDIT DEBIT CREDIT DEBIT CREDIT

PROBLEM 5.3A

7950 000

1680000

10800 000

5130000

Ted Coe, Capital, December 1, 2013

Net income for December

Month Ended December 31, 2013

Orange Corporation

Statement of Owner’s Equity

Expenses

Salaries Expense

Orange Corporation

Income Statement

Month Ended December 31, 2013

Revenue

Fees Income

PROBLEM 5.3A (continued)

Cash 7720000

Accounts Receivable 1200000

Supplies 410000

Prepaid Advertising 1200000

Equipment 6000000

Orange Corporation

Balance Sheet

December 31, 2013

Assets

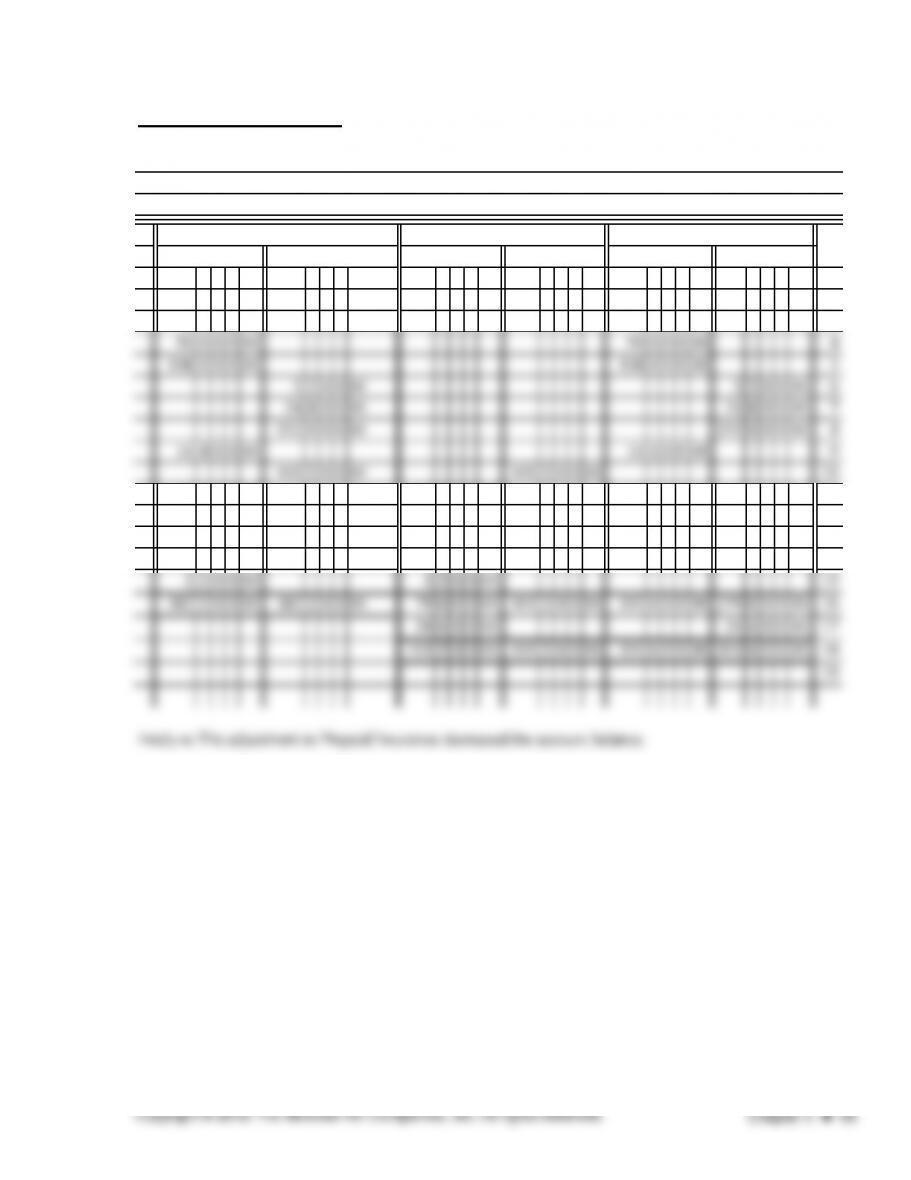

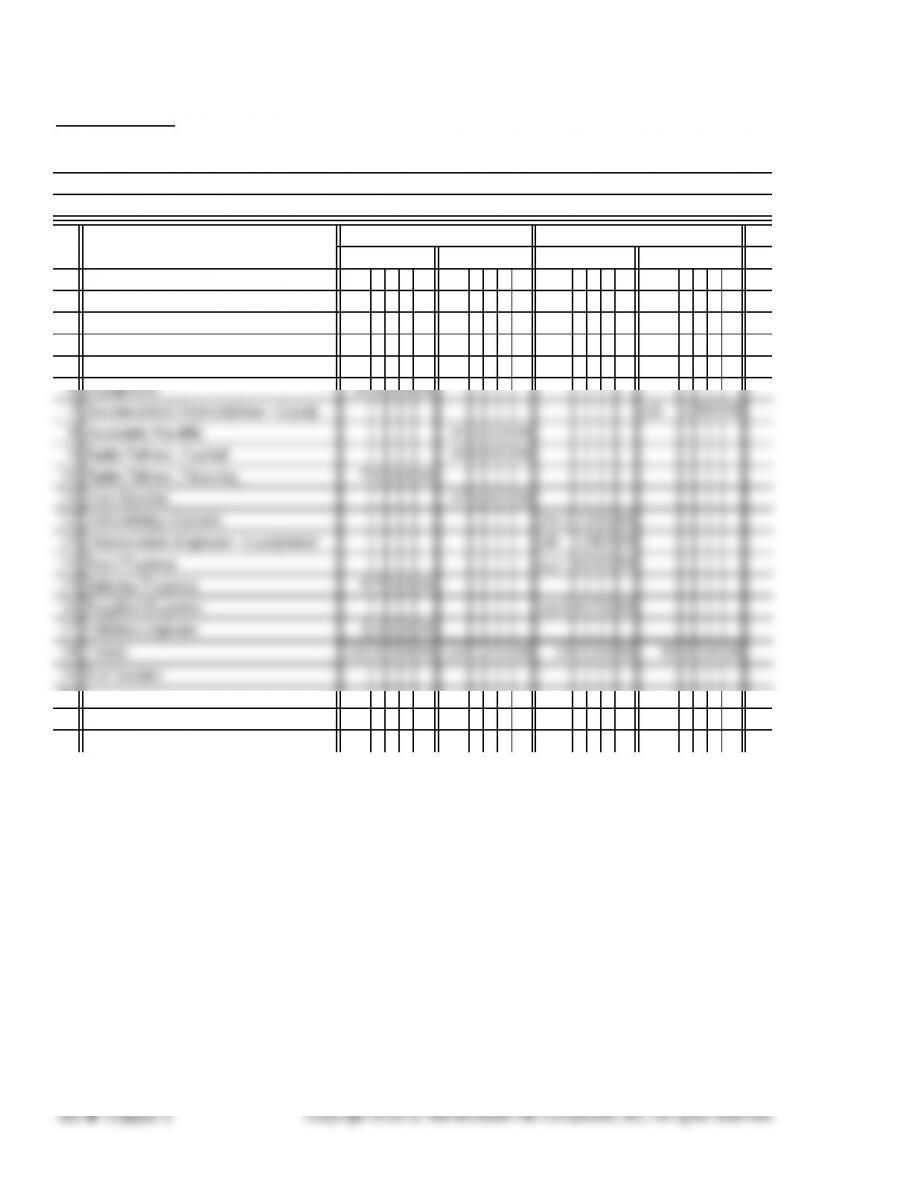

PROBLEM 5.4A

Palmer Creative Designs

Worksheet

1 Cash 35 5 0 0 00

2 Accounts Receivable 12 6 0 0 00

3 Supplies 7 7 5 0 00 (a) 6 6 5 0 00

4 Prepaid Advertising 8 4 0 0 00 (b) 2 1 0 0 00

5 Prepaid Rent 19 2 0 0 00 (c) 1 6 0 0 00

20

21

Month Ended January 31, 2013

ACCOUNT NAME

TRIAL BALANCE ADJUSTMENTS

DEBIT CREDIT DEBIT CREDIT

PROBLEM 5.4A (continued)

35 5 0 0 00 35 5 0 0 00 1

12 6 0 0 00 12 6 0 0 00 2

110000 110000 3

630000 630000 4

ADJUSTED TRIAL INCOME STATEMENT BALANCE SHEET

DEBIT CREDIT DEBIT CREDIT DEBIT CREDIT

PROBLEM 5.4A (continued)

4760000

970000

6000000

2597000

700000

1897000

7897000

Revenue

Fees Income

Palmer Creative Designs

Income Statement

Month Ended January 31, 2013

Statement of Owner’s Equity

Month Ended January 31, 2013

Expenses

Salaries Expense

Less Withdrawals for January

Increase in Capital

Sadie Palmer, Capital, January 31, 2010

Palmer Creative Designs

Sadie Palmer, Capital, January 1, 2010

Net income for January

PROBLEM 5.4A (continued)

Cash 3550000

Accounts Receivable 1260000

Supplies 110000

Prepaid Advertising 630000

PAGE

POST.

REF.

P

O

1 1

2 2013 2

3 Jan. 31 Supplies Expense 517 6 6 5 0 00 3

4 Supplies 121 665000 4

14 14

DESCRIPTION

January 31, 2013

Adjusting Entries

3

Palmer Creative Designs

Balance Sheet

DEBIT CREDIT

Assets

DATE

GENERAL JOURNAL

PROBLEM 5.4A (continued)

ACCOUNT Supplies ACCOUNT NO.

ACCOUNT Prepaid Advertising ACCOUNT NO.

2013

ACCOUNT Prepaid Rent ACCOUNT NO.

ACCOUNT Accumulated Depreciation—Equipment ACCOUNT NO.

CREDIT

DESCRIPTION

POST.

REF. DEBIT

BALANCE

130

GENERAL LEDGER

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT

121

DATE DESCRIPTION

POST.

REF. DEBIT

DATE DESCRIPTION

POST.

REF. DEBIT

DATE

131

142

CREDIT

BALANCE

DEBIT CREDIT

BALANCE

DEBIT CREDIT

CREDIT

CREDIT

CREDIT DEBIT

PROBLEM 5.4A (continued)

ACCOUNT Supplies Expense ACCOUNT NO.

ACCOUNT Advertising Expense ACCOUNT NO.

ACCOUNT Rent Expense ACCOUNT NO.

ACCOUNT Depreciation Expense—Equipment ACCOUNT NO.

2013

517

520

GENERAL LEDGER

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

CREDIT

BALANCE

DEBIT

519

CREDIT

CREDITDATE DESCRIPTION

POST.

REF. DEBIT

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

DATE DESCRIPTION

POST.

REF. DEBIT

BALANCE

DEBIT

BALANCE

DEBIT

CREDIT

523

CREDIT

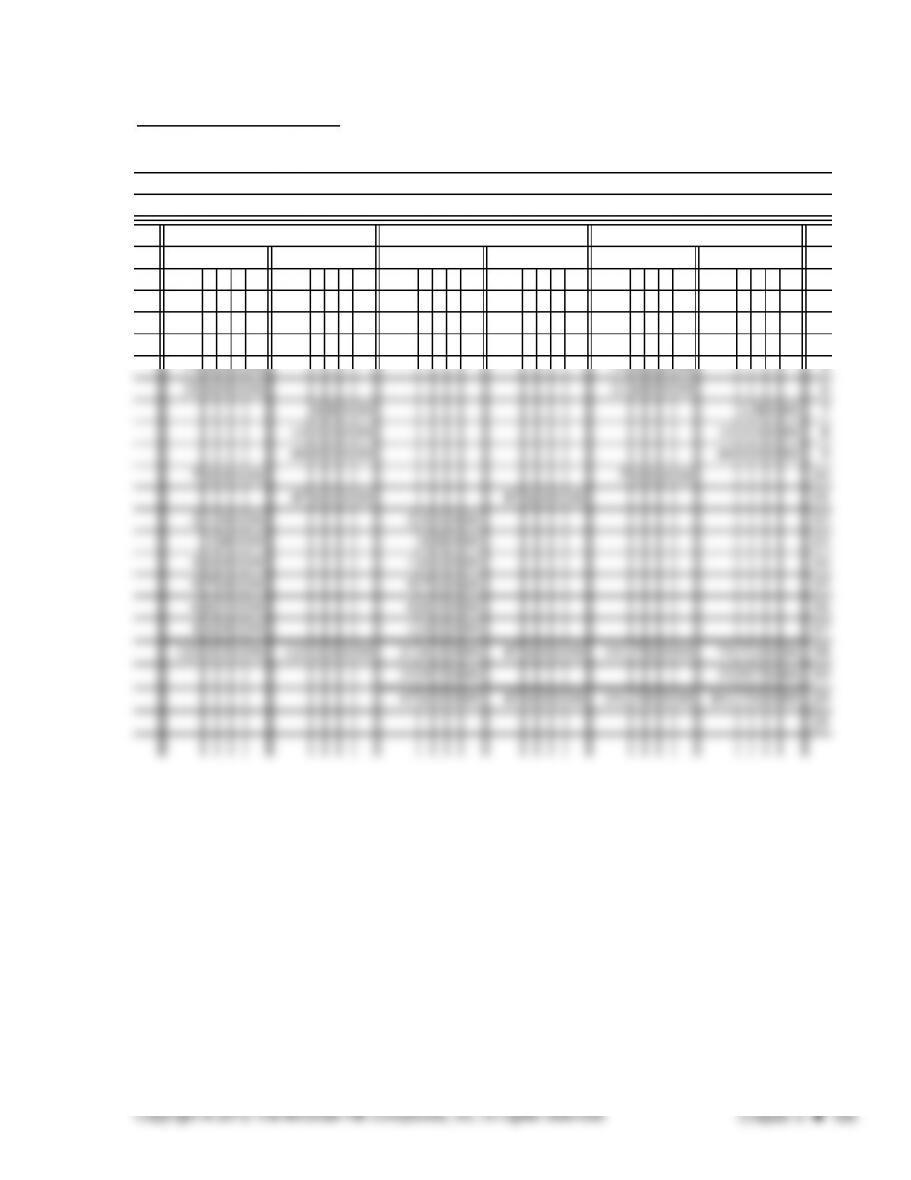

PROBLEM 5.1B

Torres Company

Worksheet

1 Cash 36 5 0 0 00

2 Accounts Receivable 320000

3 Supplies 210000 (a) 1 0 0 0 00

4 Prepaid Rent 12 0 0 0 00 (b) 1 0 0 0 00

5 Equipment 23 0 0 0 00

19

20

21

Month Ended February 28, 2013

CREDITACCOUNT NAME

TRIAL BALANCE ADJUSTMENTS

DEBIT CREDIT DEBIT

36 5 0 0 00 36 5 0 0 00 1

320000 320000 2

110000 110000 3

CREDIT DEBIT CREDIT

PROBLEM 5.1B (continued)

ADJUSTED TRIAL INCOME STATEMENT BALANCE SHEET

DEBIT CREDIT DEBIT