•

•

•

•

•

•

•

•

2.

4.

6.

8.

10.

Answers will vary but may include the following.

Groups of accounts.

Notations of the page number of the journal from which a figure comes; number of account to which

the figure was posted; to provide cross-references.

Before entry posted: cross out incorrect item, write correct data above it. After posted: journalize and

post a correcting entry.

To record business transactions in chronological order.

Helps establish audit trail.

Exposing the assets of the business to fraud and theft.

Increasing the risk of producing inaccurate financial statements.

Difficulty in auditing transactions.

Research customer billing. (Customer says no invoice was received.)

Note to instructor: These questions are designed to check students’ understanding of new terms, concepts,

and procedures presented in the chapter.

Discussion Questions

Managerial Implications: Thinking Critically

Willamette Valley Vineyards produces some 100,000 cases of wine annually that is distributed

throughout the United States, Canada, and the Pacific Rim.

CHAPTER 4

THE GENERAL JOURNAL AND THE GENERAL LEDGER

Willamette Valley Vineyards is set to become the first winery in the world to use cork stoppers

harvested from responsibly managed forestlands certified by the Rainforest Alliance to Forest

Stewardship Council (FSC) standards.

The vineyard uses biofuel in company tractors and delivery vehicles and has a biofuel policy which

offers up to 50 gallons of biofuel a month, at no cost, to each employee.

Willamette Valley (NASDAQ: WVVI) produced revenues of $16,563,712 in 2009 versus

$16,048,238 in the prior year, an increase of 3.2%.

Fast Facts

The resolution of the dispute with regards to the taxes paid by the vineyard depended upon the vineyard’s

recordkeeping and accounting practices. The Alcohol and Tobacco Tax Trade Board uncovered some

reporting errors which resulted in the vineyard having to revise statements and pay fines.

Chapter Opener: Thinking Critically

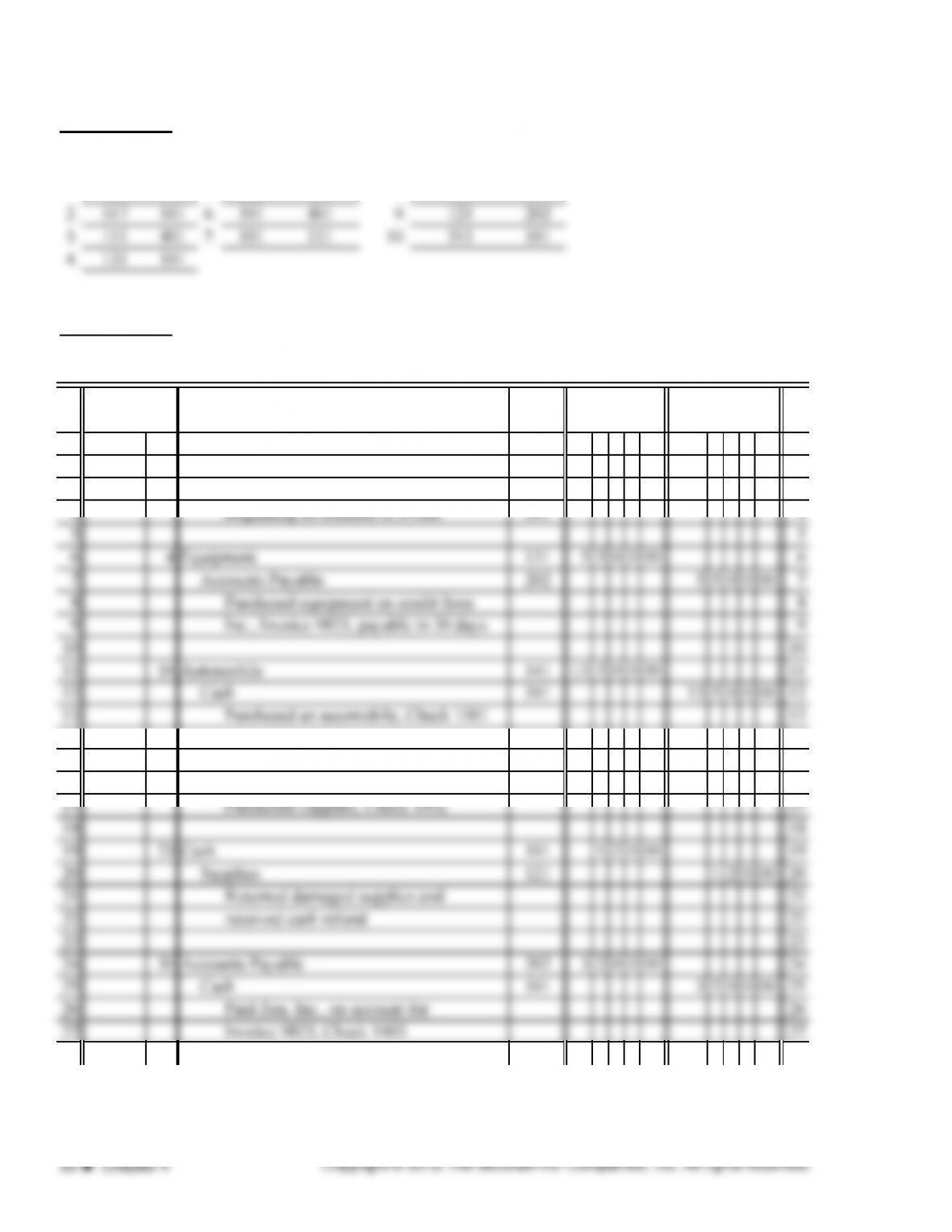

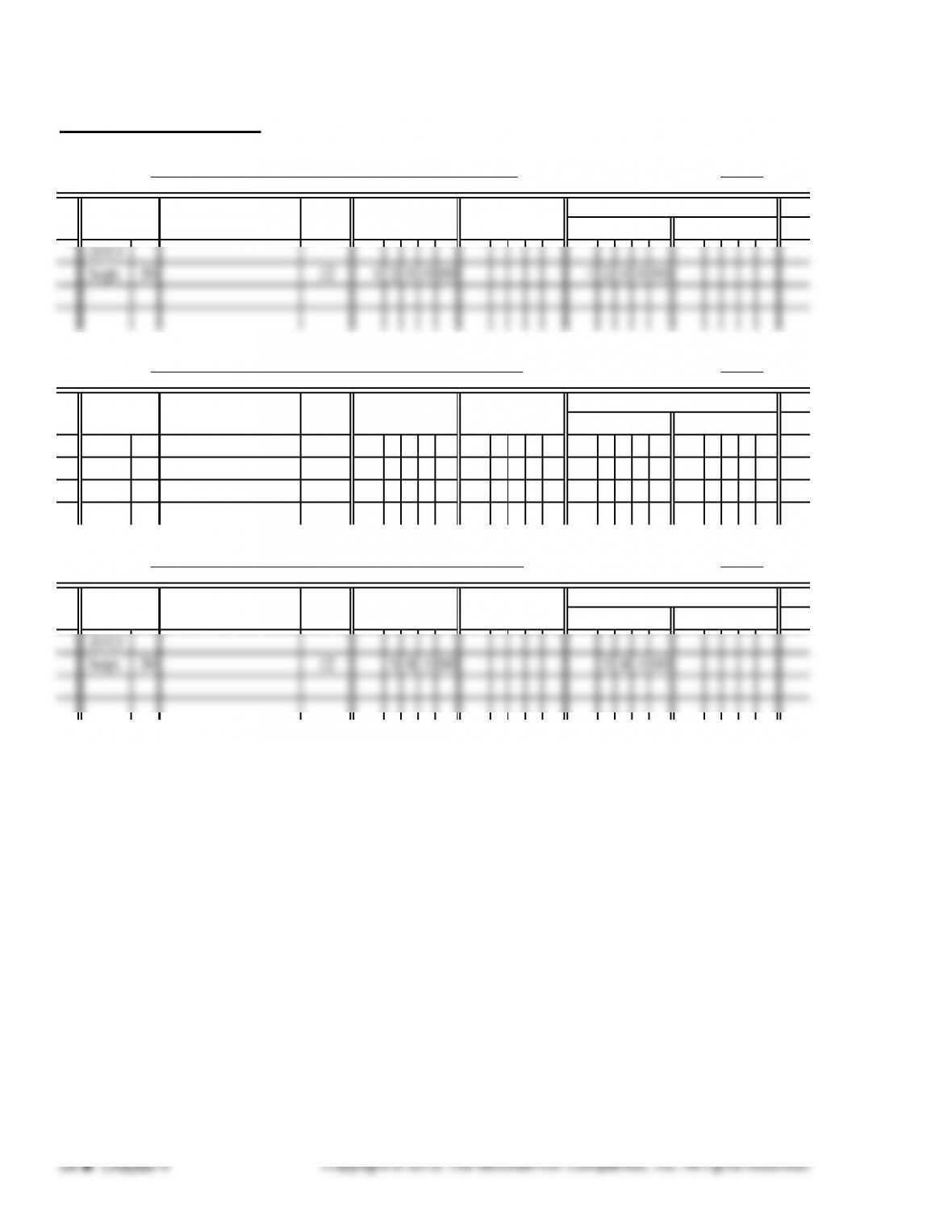

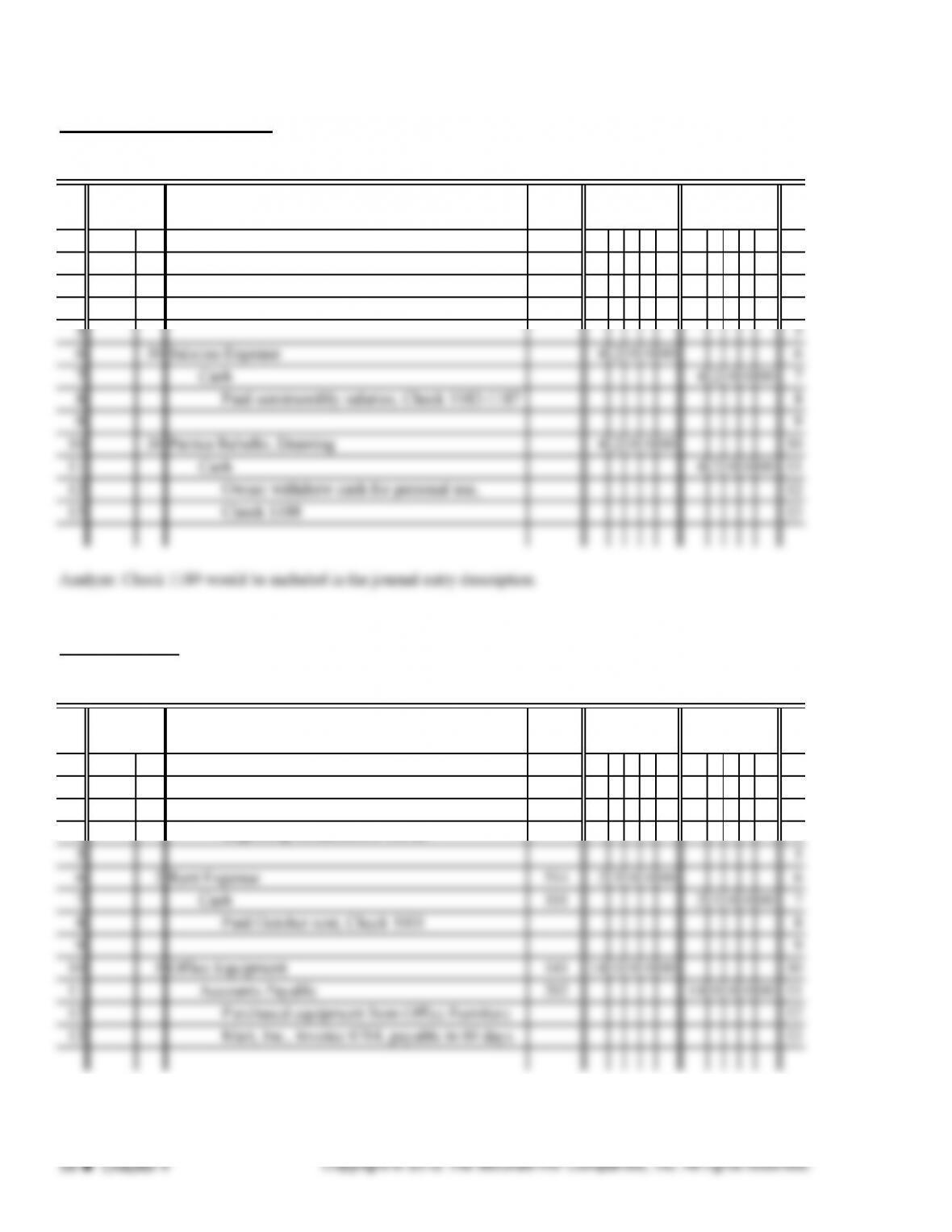

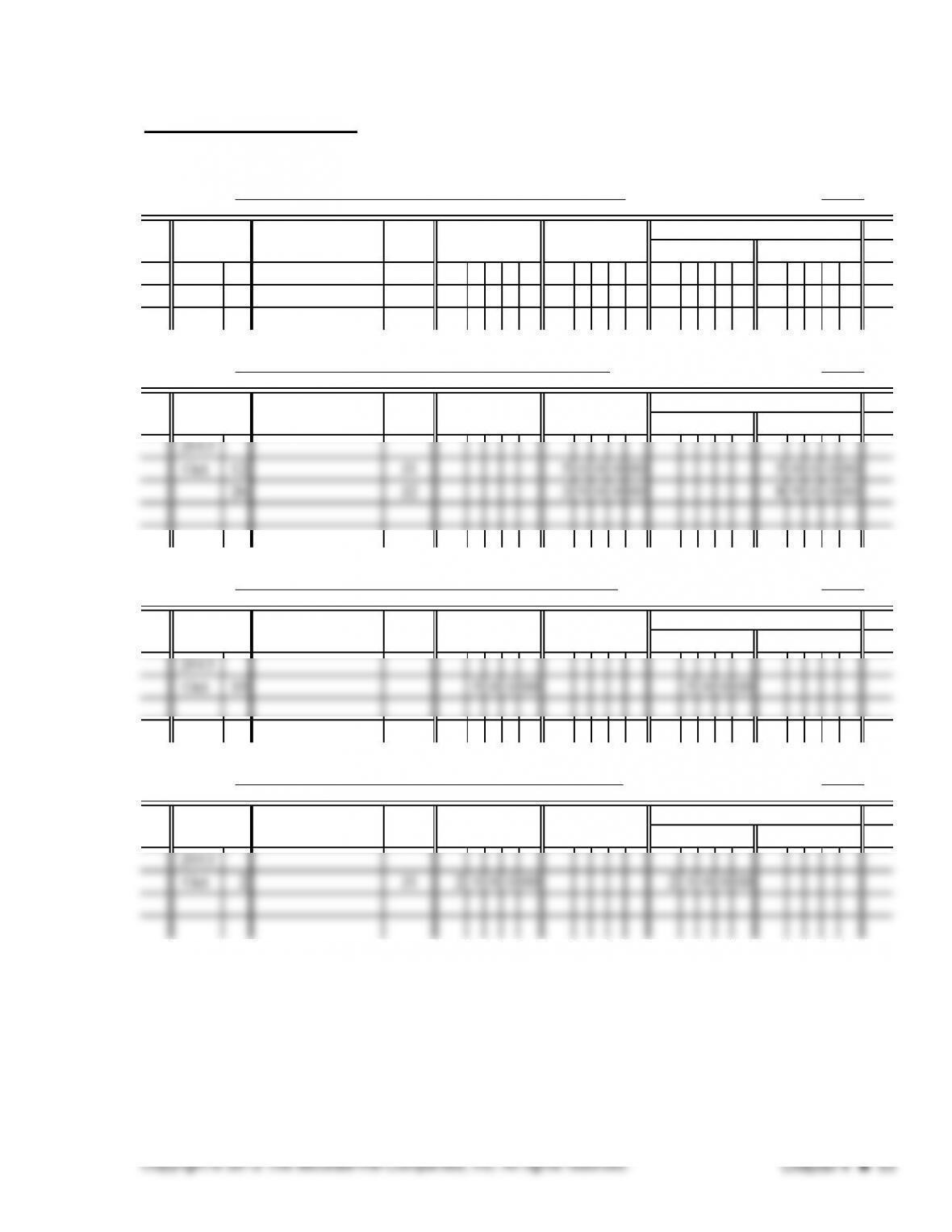

EXERCISE 4.1

Debit Debit Credit Debit Credit

1. 401 5. 202 101 8. 101 301

14 14

15 20 Supplies 121 4 2 0 00 15

16 Cash 101 4 2 0 00 16

17 Purchased supplies, Check 1002 17

18 18

19 23 Cash 101 1 2 0 00 19

20 Supplies 121 1 2 0 00 20

21 Returned damaged supplies and 21

22 received cash refund 22

23 23

24 30 Accounts Payable 202 320000 24

25 Cash 101 320000 25

26 Paid Zen, Inc., on account for 26

27 Invoice 9823, Check 1003 27

Credit

101

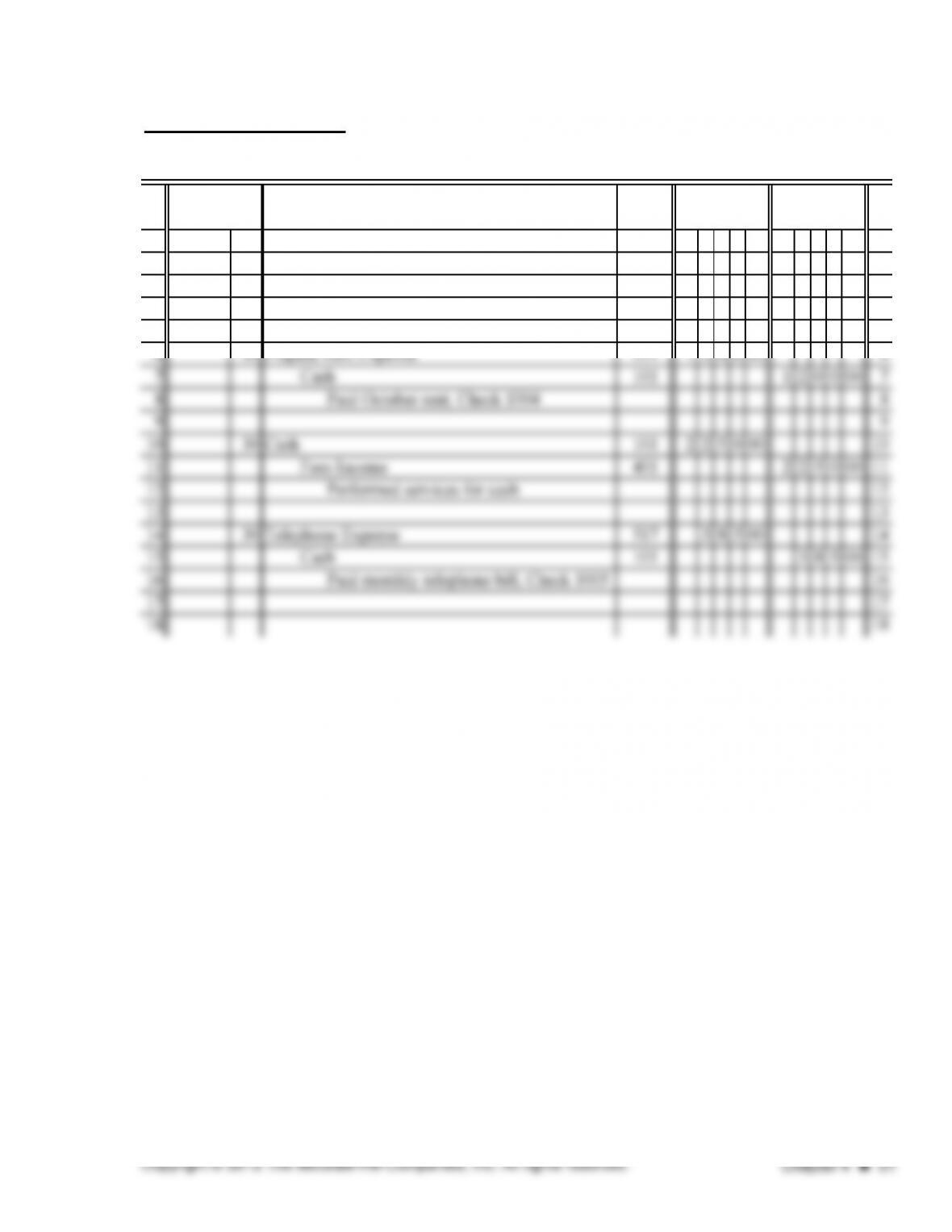

EXERCISE 4.2 (continued)

PAGE 2

POST.

REF.

1 2013 1

2 Sept. 30 Mary Vinzant, Drawing 302 200000 2

3 Cash 101 200000 3

4 Owner withdrew cash for personal use 4

5 5

CREDIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT

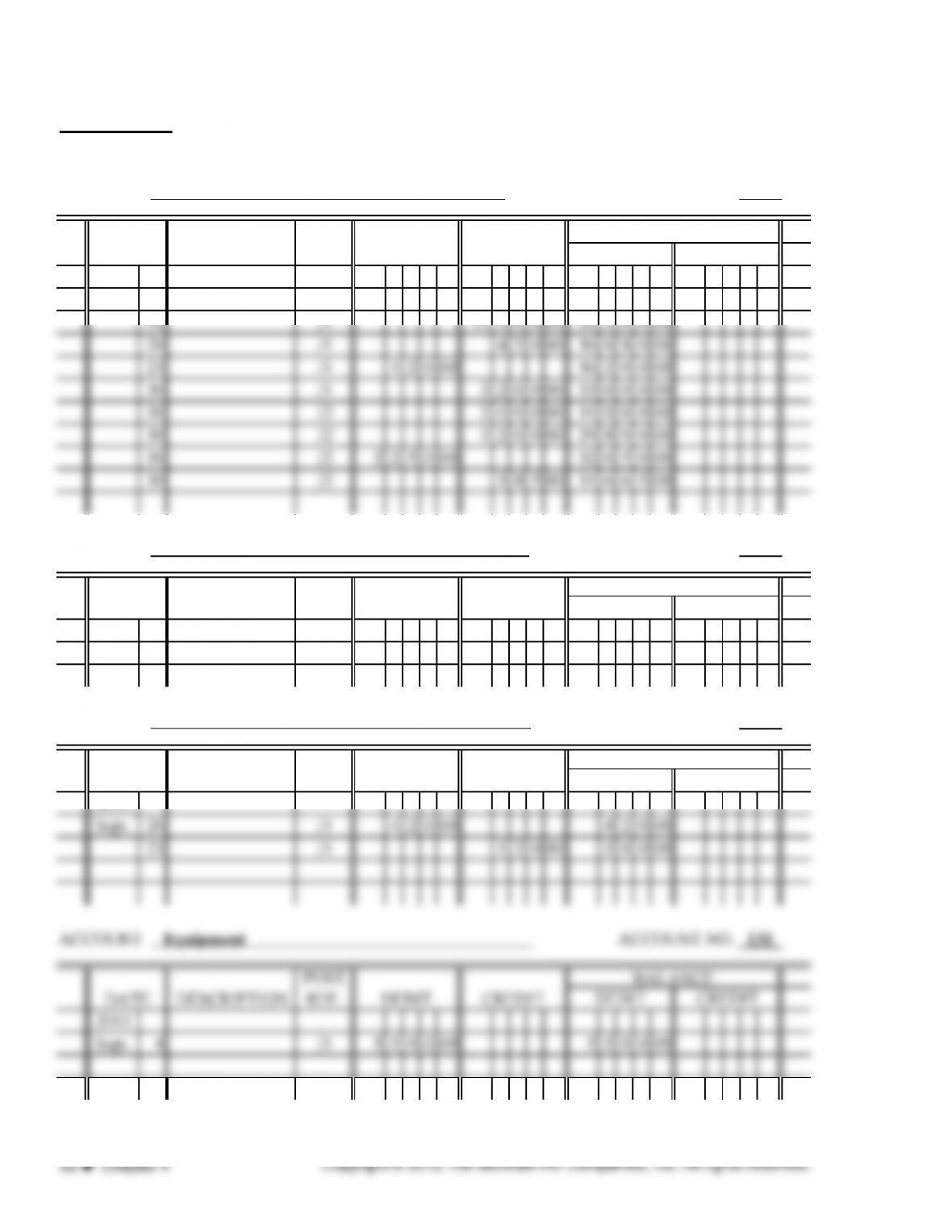

EXERCISE 4.3

ACCOUNT Cash ACCOUNT NO. 101

2013

Sept. 1 J1 5000000 5000000

ACCOUNT Accounts Receivable ACCOUNT NO. 111

ACCOUNT Supplies ACCOUNT NO. 121

2013

E

2013

Sept. 4 J1 550000 550000

DATE

BALANC

E

DEBIT CREDIT

DEBIT CREDITDESCRIPTION

POST

REF. DEBIT

POST

REF.

CREDIT

BALANC

E

DEBIT CREDIT

DATE DESCRIPTION

GENERAL LEDGER

DATE DESCRIPTION

POST

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

EXERCISE 4.3 (continued)

ACCOUNT Automobile ACCOUNT NO. 141

ACCOUNT Accounts Payable ACCOUNT NO. 202

ACCOUNT Mary Vinzant, Capital ACCOUNT NO. 301

ACCOUNT Mary Vinzant, Drawing ACCOUNT NO. 302

ACCOUNT Fees Income ACCOUNT NO. 401

DEBIT CREDIT

CREDIT

BALANC

E

DEBIT

CREDIT CREDIT

DEBIT

BALANC

E

DEBIT

POST

REF.

DATE DESCRIPTION

POST

REF.

DATE DESCRIPTION

CREDIT

DEBIT CREDIT

BALANC

E

DEBIT

DATE DESCRIPTION

POST

REF.

DATE

DESCRIPTION

DESCRIPTION

DATE

CREDIT

BALANC

E

DEBIT CREDIT

DEBIT

POST

REF.

CREDIT

POST

REF. DEBIT CREDIT

BALANC

E

DEBIT

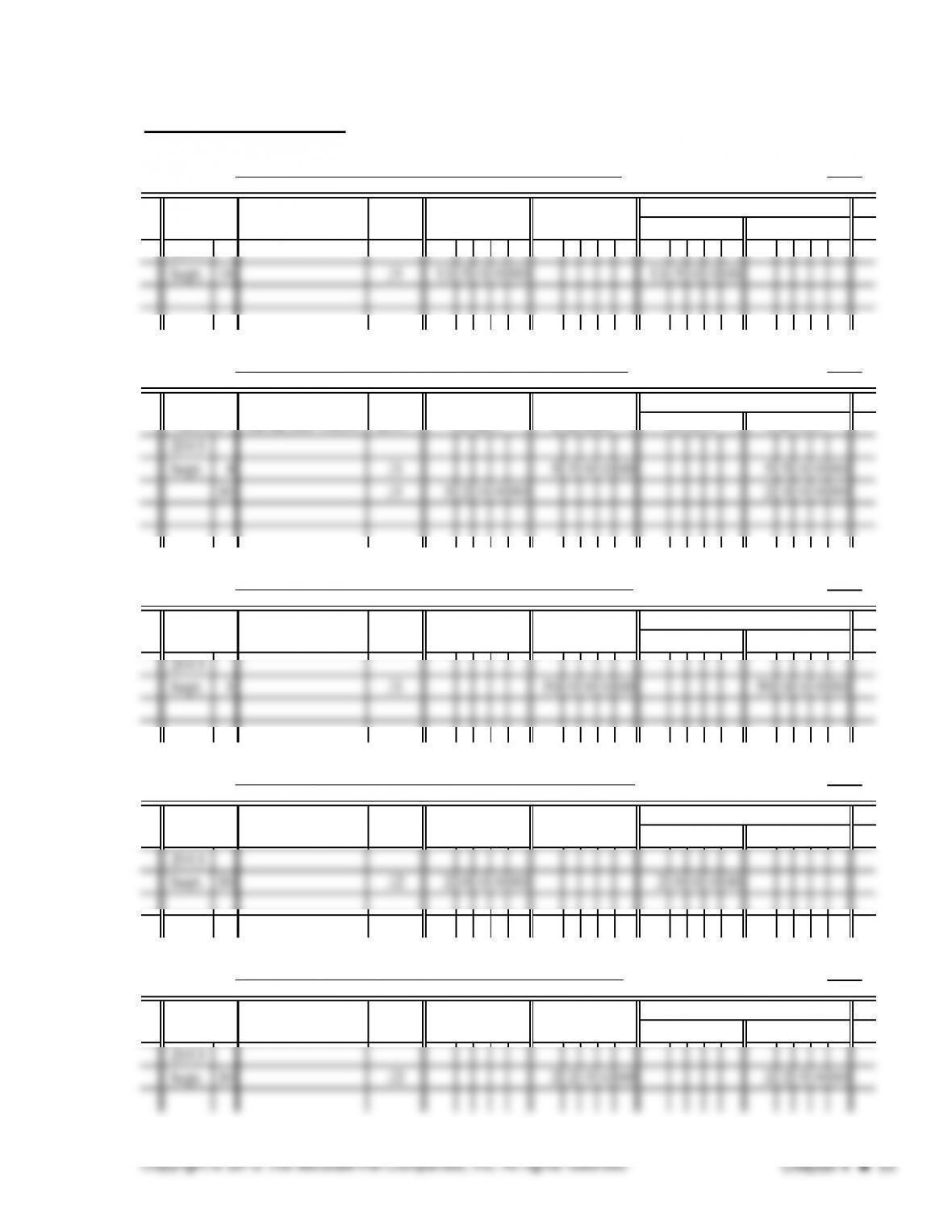

EXERCISE 4.3 (continued)

ACCOUNT Rent Expense ACCOUNT NO. 511

ACCOUNT Salaries Expense ACCOUNT NO. 514

ACCOUNT Telephone Expense ACCOUNT NO. 517

CREDIT

DEBIT

POST

REF.

BALANC

E

DEBIT

DATE

POST

REF.

CREDITDESCRIPTION

BALANC

E

DESCRIPTION DEBIT CREDIT

BALANC

E

DEBIT

POST

REF. DEBIT CREDIT CREDIT

DEBIT CREDIT

DATE

DATE

DESCRIPTION

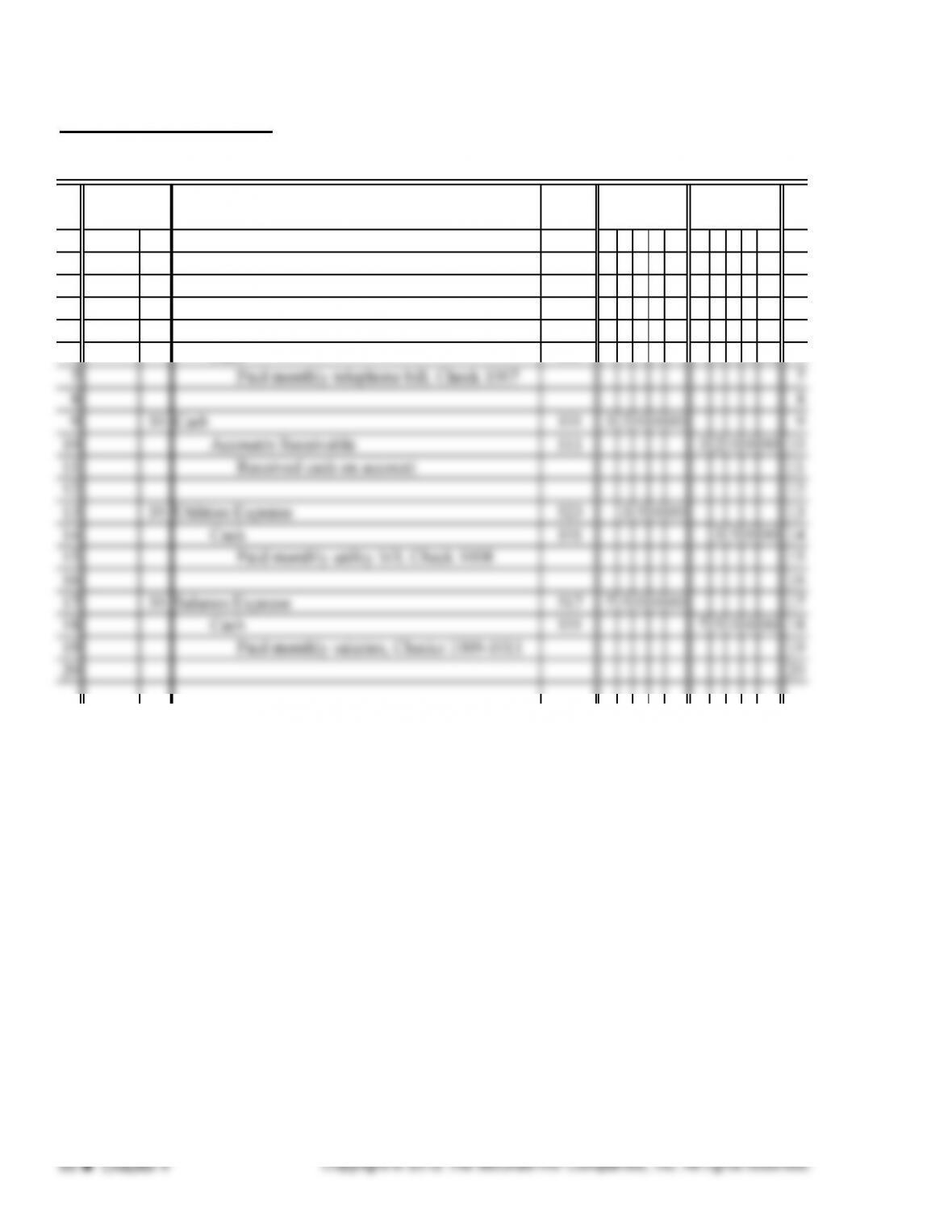

EXERCISE 4.4

PAGE

POST.

REF.

1 2013 1

2 Nov. 5 Cash 1400000 2

3 Accounts Receivable 1600000 3

4 Fees Income 3000000 4

EXERCISE 4.5

PAGE

POST.

REF.

1 2013 1

2 July 30 Telephone Expense 9 5 0 00 2

CREDIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT

CREDIT

EXERCISE 4.6

PAGE

POST.

REF.

1 2013 1

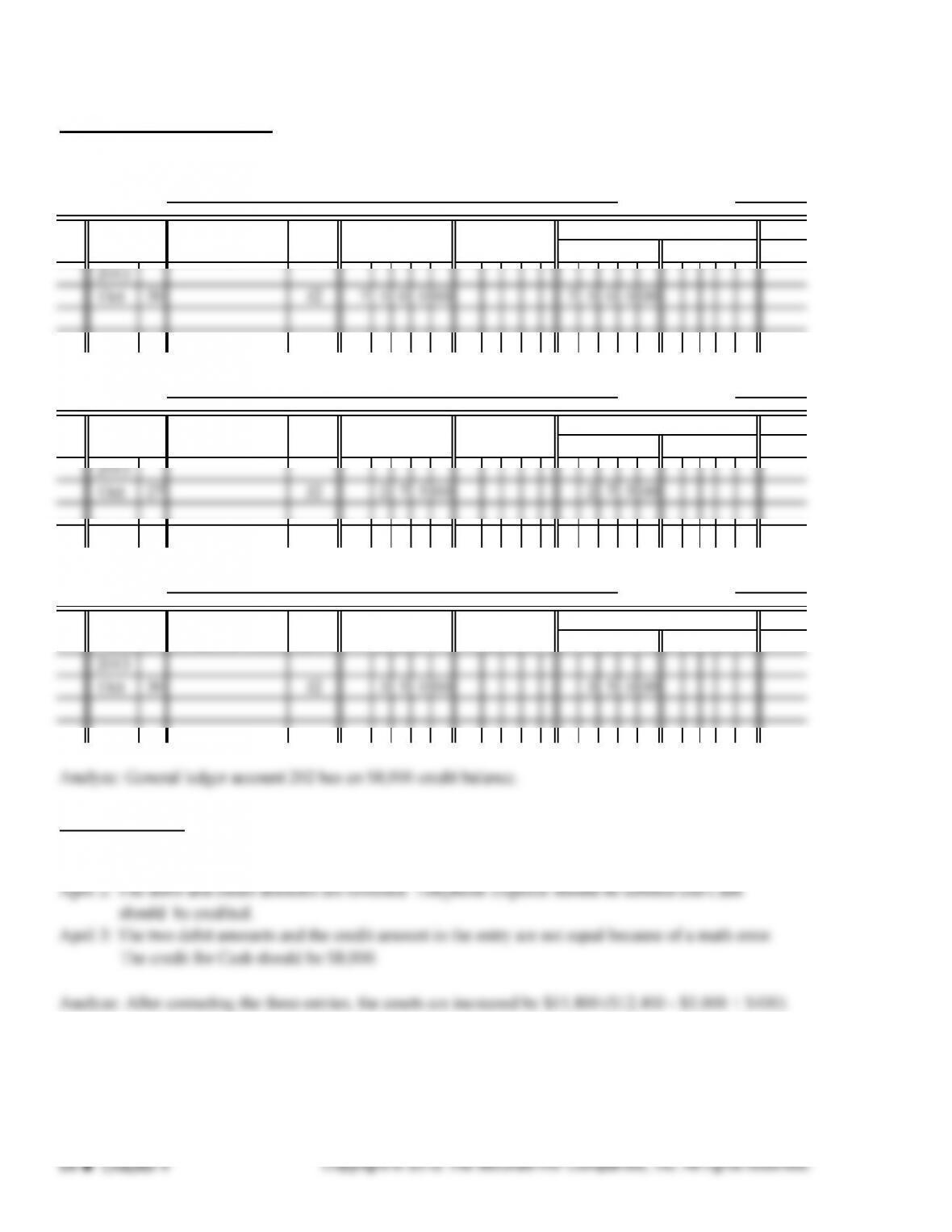

PROBLEM 4.1A

PAGE 1

POST.

REF.

1 2013 1

2 Sept. 1 Rent Expense 140000 2

3 Cash 140000 3

4 Paid September rent, Check 1169 4

5 5

6 5 Cash 250000 6

7 Fees Income 250000 7

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

DATE DESCRIPTION DEBIT

GENERAL JOURNAL

CREDIT

PROBLEM 4.1A (continued)

PAGE 2

POST.

REF.

1 2013 1

2 Sept. 15 Salaries Expense 420000 2

3 Cash 420000 3

4 Paid semimonthly salaries, Checks 1172-1177 4

5 5

14 14

15 20 Equipment 276000 15

16 Cash 276000 16

17 Purchased nets, Check 1179 17

18 18

19 21 Cash 9 5 0 00 19

20 Accounts Receivable 9 5 0 00 20

21 Received cash on account 21

22 22

CREDIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT

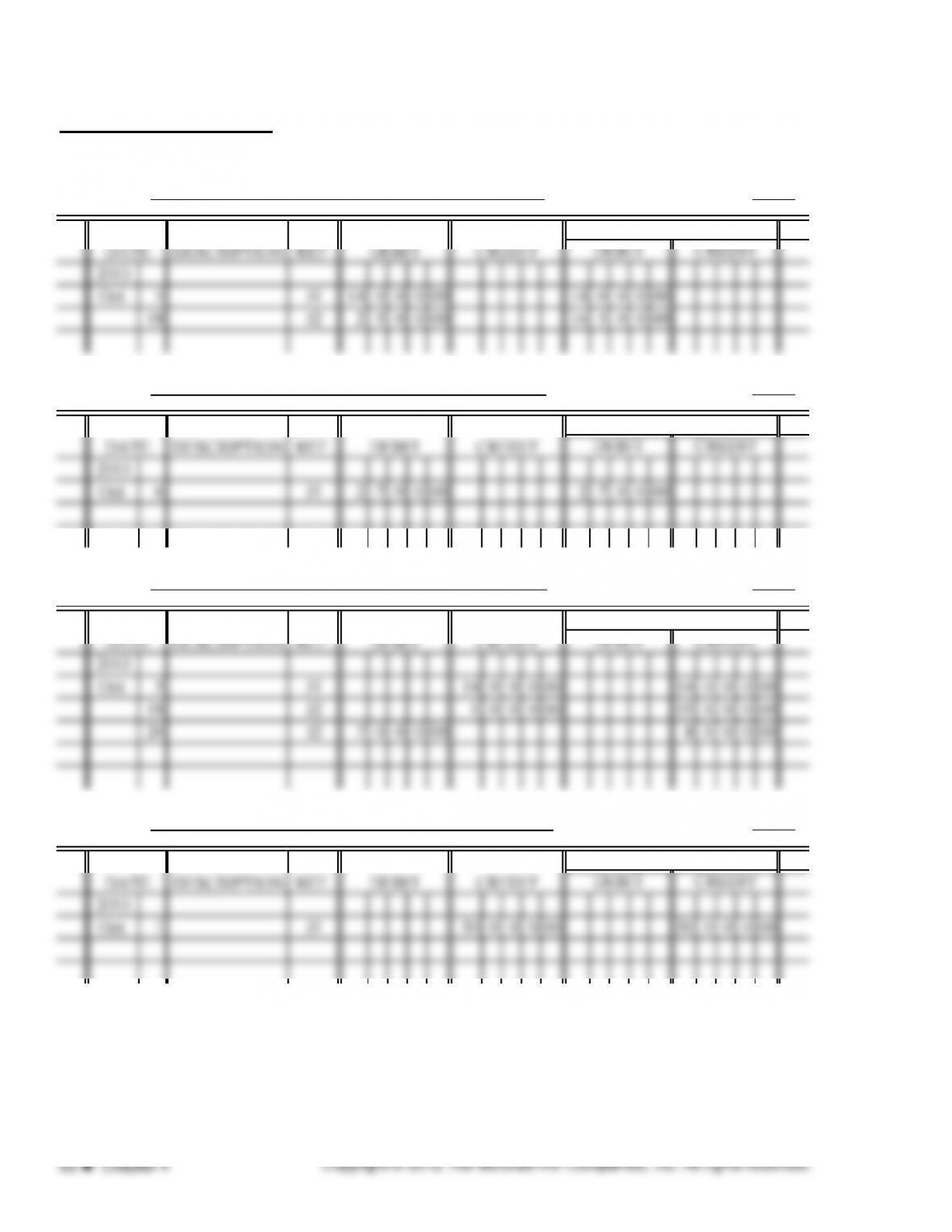

PROBLEM 4.1A (continued)

PAGE 3

POST.

REF.

1 2013 1

2 Sept. 28 Utilities Expense 225000 2

3 Cash 225000 3

4 Paid monthly electric bill, Check 1181 4

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

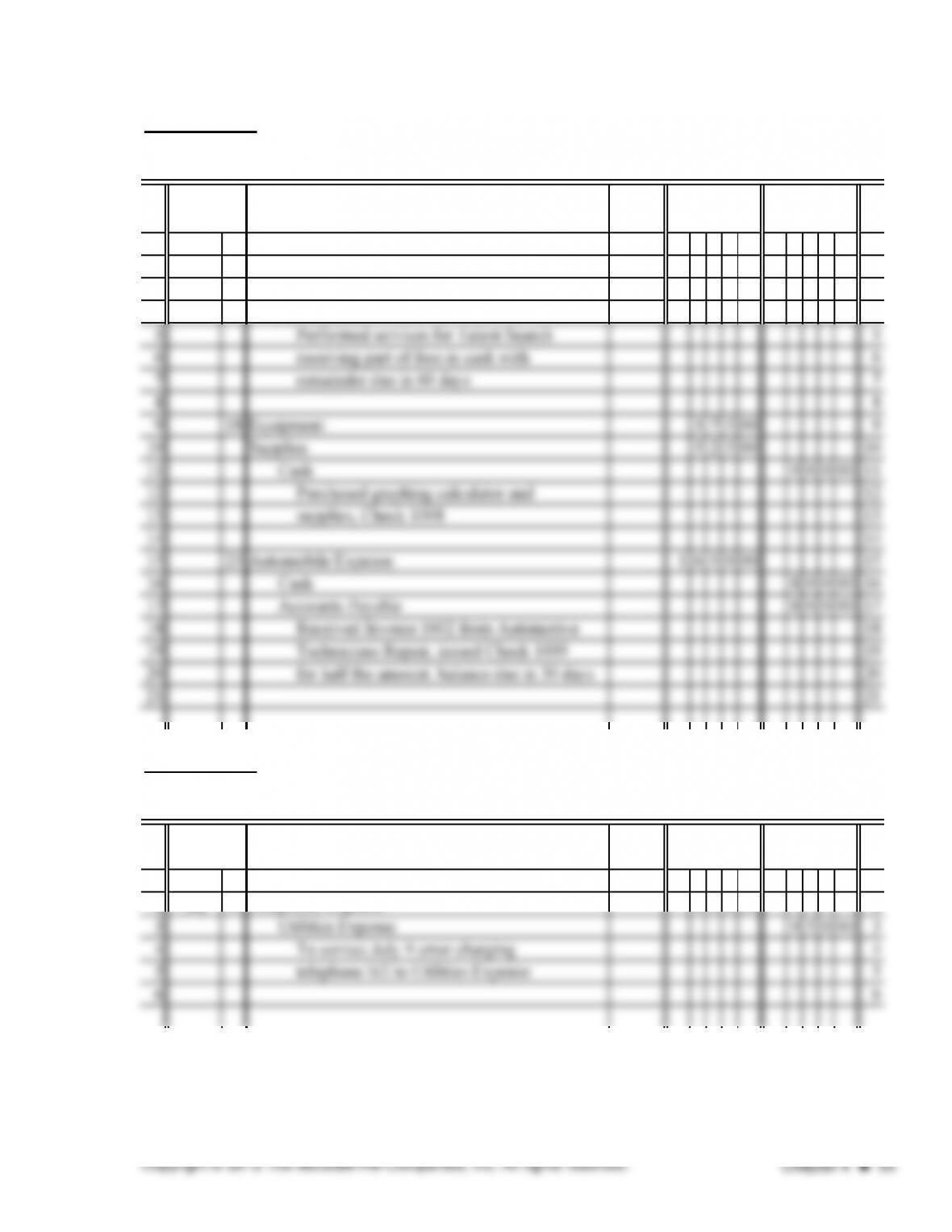

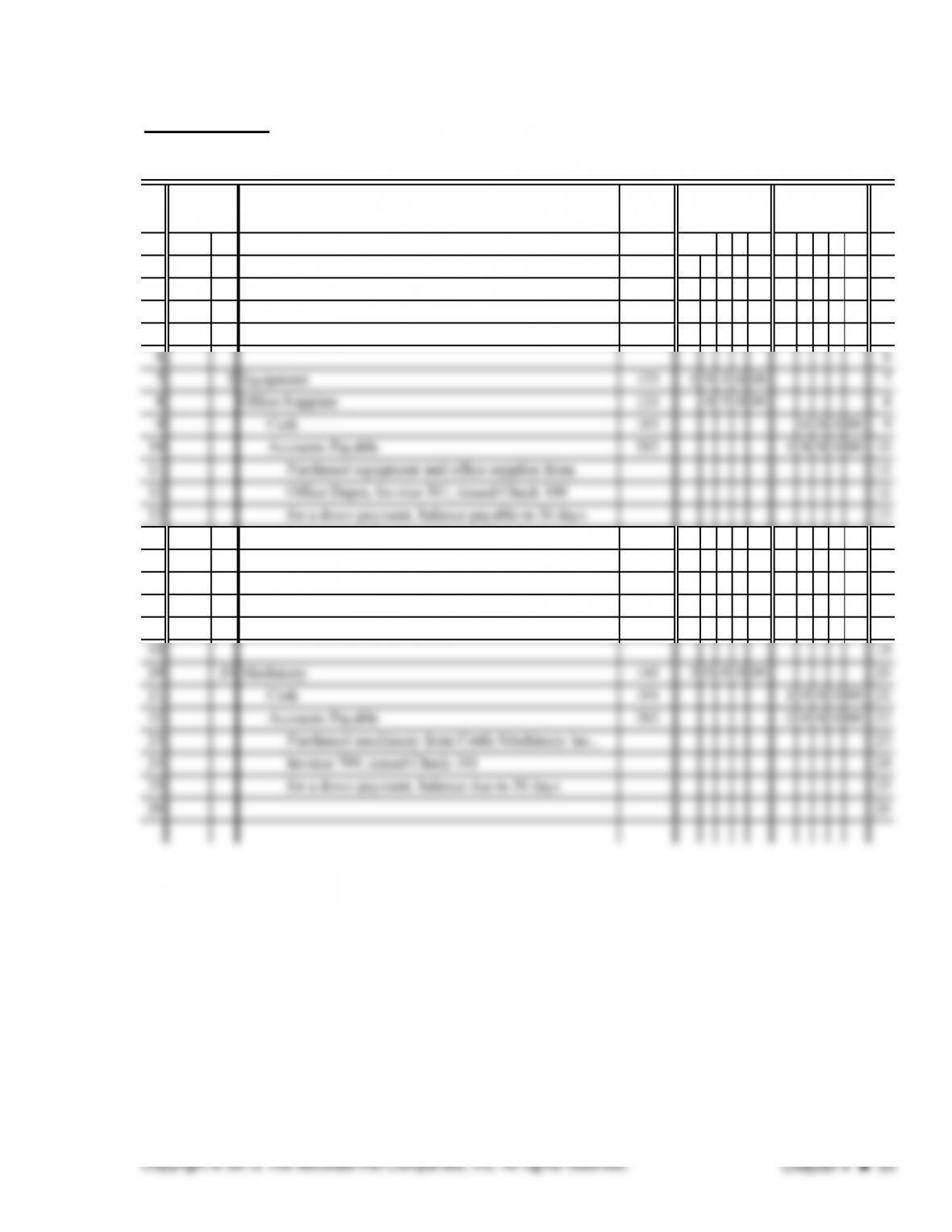

PROBLEM 4.2A (continued)

PAGE 2

POST.

REF.

1 2013 6 Art Equipment 151 270000 1

2 Oct. Cash 101 270000 2

3 Purchased art equipment, Check 1002 3

4 4

16 Performed services for cash and on credit 16

17 17

18 15 Cash 101 3 0 0 00 18

19 Supplies 121 3 0 0 00 19

20 20

Returned damaged supplies for cash refund

CREDIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT

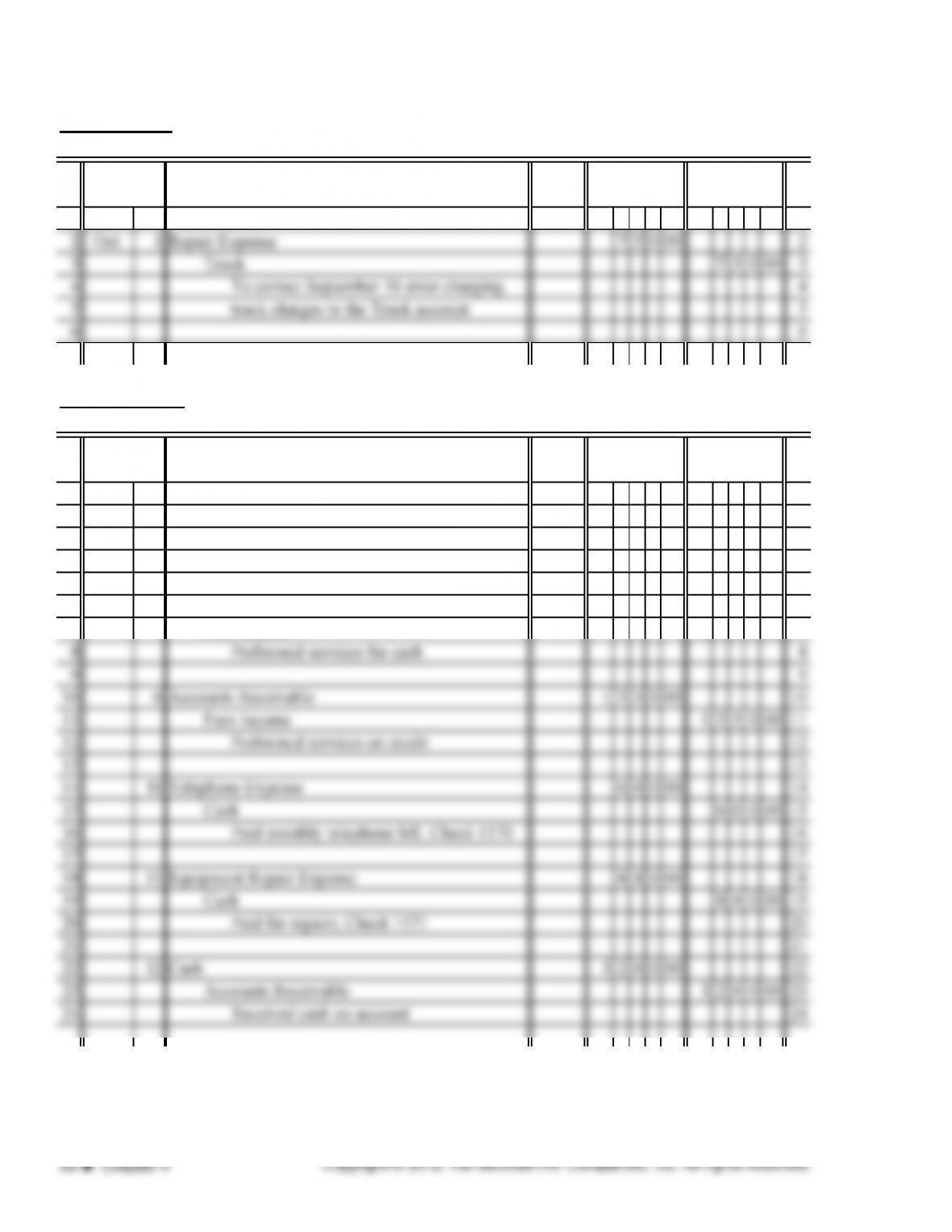

PROBLEM 4.2A (continued)

PAGE 3

POST.

REF.

1 2013 26 Accounts Receivable 111 390000 1

2 Oct. Fees Income 401 390000 2

3 Performed services on credit 3

4 4

5 27 Telephone Expense 520 2 7 5 00 5

6 Cash 101 2 7 5 00 6

CREDIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT

PROBLEM 4.2A (continued)

ACCOUNT Cash ACCOUNT NO. 101

2013

Oct. 1 J1 5000000 5000000

2 J1 250000 4750000

6 J1 270000 4480000

7 J1 105000 4375000

ACCOUNT Accounts Receivable ACCOUNT NO. 111

2013

E

2013

Oct. 7 J1 105000 105000

15 J1 3 0 0 00 7 5 0 00

CREDIT

CREDIT

BALANC

E

POST

REF. DEBIT DEBIT

DATE DESCRIPTION

GENERAL LEDGER

BALANC

E

DEBIT CREDIT

DATE CREDITDEBIT

POST

REF.DESCRIPTION

PROBLEM 4.2A (continued)

ACCOUNT Office Equipment ACCOUNT NO. 141

E

E

ACCOUNT Wilson Adams, Capital ACCOUNT NO. 301

GENERAL LEDGER

BALANC

E

POST

BALANC

E

POST

PROBLEM 4.2A (continued)

ACCOUNT Wilson Adams, Drawing ACCOUNT NO. 302

ACCOUNT Fees Income ACCOUNT NO. 401

ACCOUNT Office Cleaning Expense ACCOUNT NO. 511

ACCOUNT Rent Expense ACCOUNT NO. 514

CREDIT

BALANC

E

DEBIT

CREDITDEBITDATE DESCRIPTION

POST

REF.

POST

REF.DATE

BALANC

E

DEBIT CREDIT

DEBIT CREDITDESCRIPTION

DATE DESCRIPTION

GENERAL LEDGER

DATE DESCRIPTION

POST

REF. DEBIT DEBIT

CREDIT

BALANC

E

CREDIT

CREDIT

POST

REF.

BALANC

E

DEBIT CREDIT

DEBIT

PROBLEM 4.2A (continued)

ACCOUNT Salaries Expense ACCOUNT NO. 517

ACCOUNT Telephone Expense ACCOUNT NO. 520

ACCOUNT Utilities Expense ACCOUNT NO. 523

PROBLEM 4.3A

April 1: The debit should be to Accounts Receivable, not Accounts Payable.

BALANC

E

DEBIT CREDIT

DESCRIPTION

POST

REF. CREDIT

DEBIT CREDIT

GENERAL LEDGER

DATE DESCRIPTION

POST

REF.

DATE DESCRIPTION

DATE

DEBIT CREDIT

BALANC

E

DEBIT

DEBIT CREDIT DEBIT

BALANC

E

CREDIT

POST

REF.

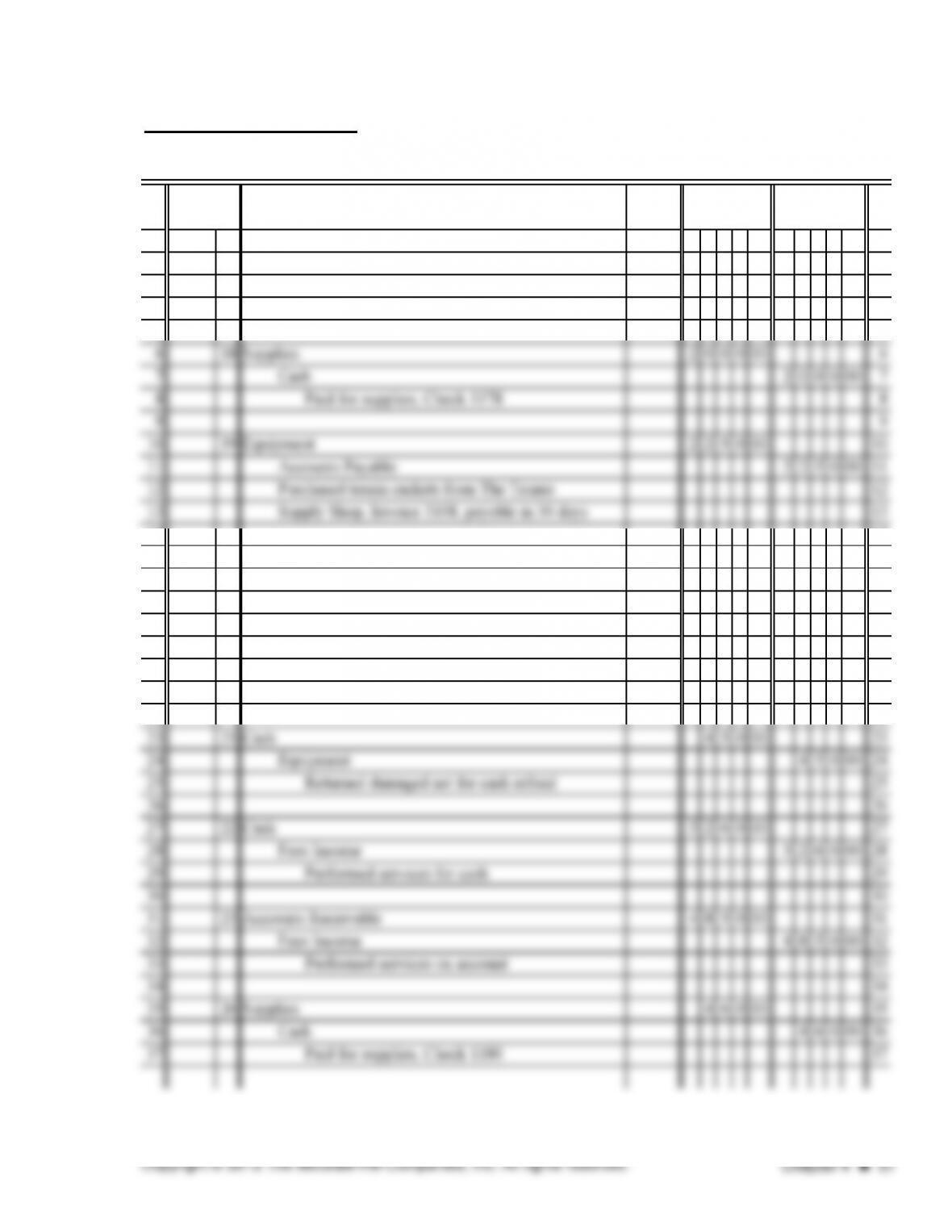

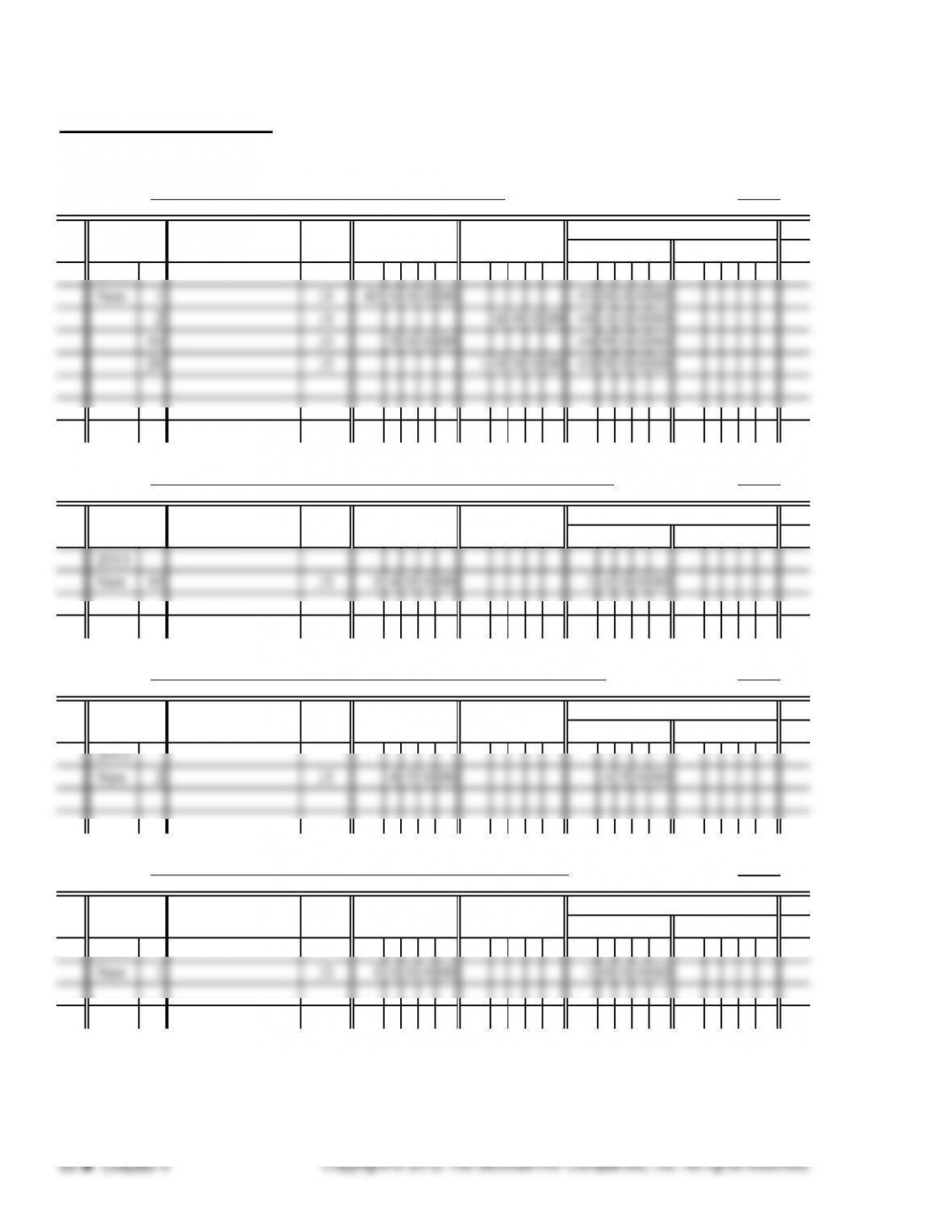

PROBLEM 4.4A

PAGE 1

POST.

REF.

1 2013 1

2 Nov. 1 Cash 101 45 0 0 0 00 2

3 Tools 131 100000 3

4 Erwin Tobias, Capital 301 46 0 0 0 00 4

5 Beginning investment of owner 5

14 14

15 10 Cash 101 5 0 0 00 15

16 Accounts Receivable 111 140000 16

17 Fees Income 401 190000 17

18 Services for cash and credit 18

CREDIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT

PROBLEM 4.4A (continued)

ACCOUNT Cash ACCOUNT NO. 101

2013

ACCOUNT Accounts Receivable ACCOUNT NO. 111

ACCOUNT Office Supplies ACCOUNT NO. 121

ACCOUNT Tools ACCOUNT NO. 131

2013

DATE DESCRIPTION CREDITDEBIT

DATE

BALANC

E

DEBIT CREDIT

POST

REF.

DESCRIPTION

POST

REF.

DESCRIPTION

POST

REF.

CREDIT

CREDIT

GENERAL LEDGER

DATE DESCRIPTION CREDIT

DATE DEBIT

DEBIT

DEBIT

BALANC

E

DEBIT

BALANC

E

POST

REF.

BALANC

E

CREDIT

DEBIT CREDIT

CREDIT DEBIT

PROBLEM 4.4A (continued)

ACCOUNT Machinery ACCOUNT NO. 141

ACCOUNT Equipment ACCOUNT NO. 151

ACCOUNT Accounts Payable ACCOUNT NO. 202

2013

ACCOUNT Erwin Tobias, Capital ACCOUNT NO. 301

2013

DATE DESCRIPTION

BALANC

E

DEBIT CREDIT

DEBIT CREDIT

POST

REF.

CREDIT

CREDIT

DATE DESCRIPTION

POST

REF. DEBIT CREDIT

BALANC

E

DEBIT

POST

REF.

BALANC

E

DEBIT CREDIT

DEBIT

GENERAL LEDGER

CREDIT

POST

REF. DEBIT CREDIT

BALANC

E

DEBIT

DATE DESCRIPTION

DATE DESCRIPTION

PROBLEM 4.4A (continued)

ACCOUNT Fees Income ACCOUNT NO. 401

PROBLEM 4.1B

PAGE 1

1 2013 1

2 Sept. 1 Cash 2500000 2

3 Cathy Cox 2500000 3

4 Beginning investment of owner 4

GENERAL JOURNAL

DESCRIPTIONDATE

POST

REF. DEBIT CREDIT

GENERAL LEDGER

BALANC

E

DEBIT CREDIT

DATE DESCRIPTION

POST

REF. DEBIT CREDIT