• Avon Representatives collectively earn an estimated $6 billion each year

• Avon’s brand has 90% awareness across the globe and the company sells four lipsticks every second of the

day.

• The Avon Foundation for Women is the world’s largest corporate philanthropy for women, and has raised

and awarded $725 million.

• Answers will vary. Costs, contribution margin, and the effect on net profit may be cited. Nonfinancial

matters may also be considered, including quality of, and demand for, the product.

2. Accounting procedure whereby all manufacturing costs, including fixed costs, are charged to cost of goods

manufactured.

4. In most cases, direct costing; offers computation of the contribution margin.

6. Net sales minus variable cost of goods sold and variable operating expenses.

8. Future earnings or potential benefits that are given up because of action taken.

10. Effect on employee morale, pace of technology improvements, availability of cash for purchase.

12. Cash from sale should offset the cost of new equipment.

14. New equipment may entail training or layoffs.

These questions are designed to check students’ understanding of new terms, concepts, and procedures presented

in the chapter.

Discussion Questions

CHAPTER 30

COST-REVENUE ANALYSIS FOR DECISION MAKING

Chapter Opener: Thinking Critically

For Avon, the decision to cease operations at the site aligned with the company’s restructuring efforts aimed at

enhancing the company’s efficiency, effectiveness, and profitability. Other companies may have different reasons

for closing plants.

Fast Facts

Managerial Implications: Thinking Critically

EXERCISE 30.1

1. Variable manufacturing costs ($65 x 10,000 units) $650,000

2. Total cost of goods manufactured $750,000

3. Cost of goods manufactured $750,000

4. Sales ($175 x 9,000 units) $1,575,000

Cost of Goods Sold 675,000

EXERCISE 30.2

1. Units in Ending Inventory 1,000

2. Sales ($175 x 9,000 units) $1,575,000

Cost of Goods Sold:

3. Manufacturing Margin $990,000

Variable selling and administrative ($25 x 9,000) 225,000

EXERCISE 30.3

EXERCISE 30.6

Decrease in direct labor (12,000 units x $1.00) $12,000

Decrease in variable overhead (12,000 units x $1.00) 12,000

EXERCISE 30.7

The firm would save $2.00 per part if purchased.

Cost to purchase the part:

Purchase price $42.00

Cost to manufacture the part:

EXERCISE 30.8

The most Bay should pay would be the cost it would incur to manufacture it. There are other factors t

consider besides just the direct saving from purchasing the product–idle time, customer concerns, etc

Chapter 30 973

Copyright © 2012 The McGraw-Hill Companies, Inc. All rights reserved.

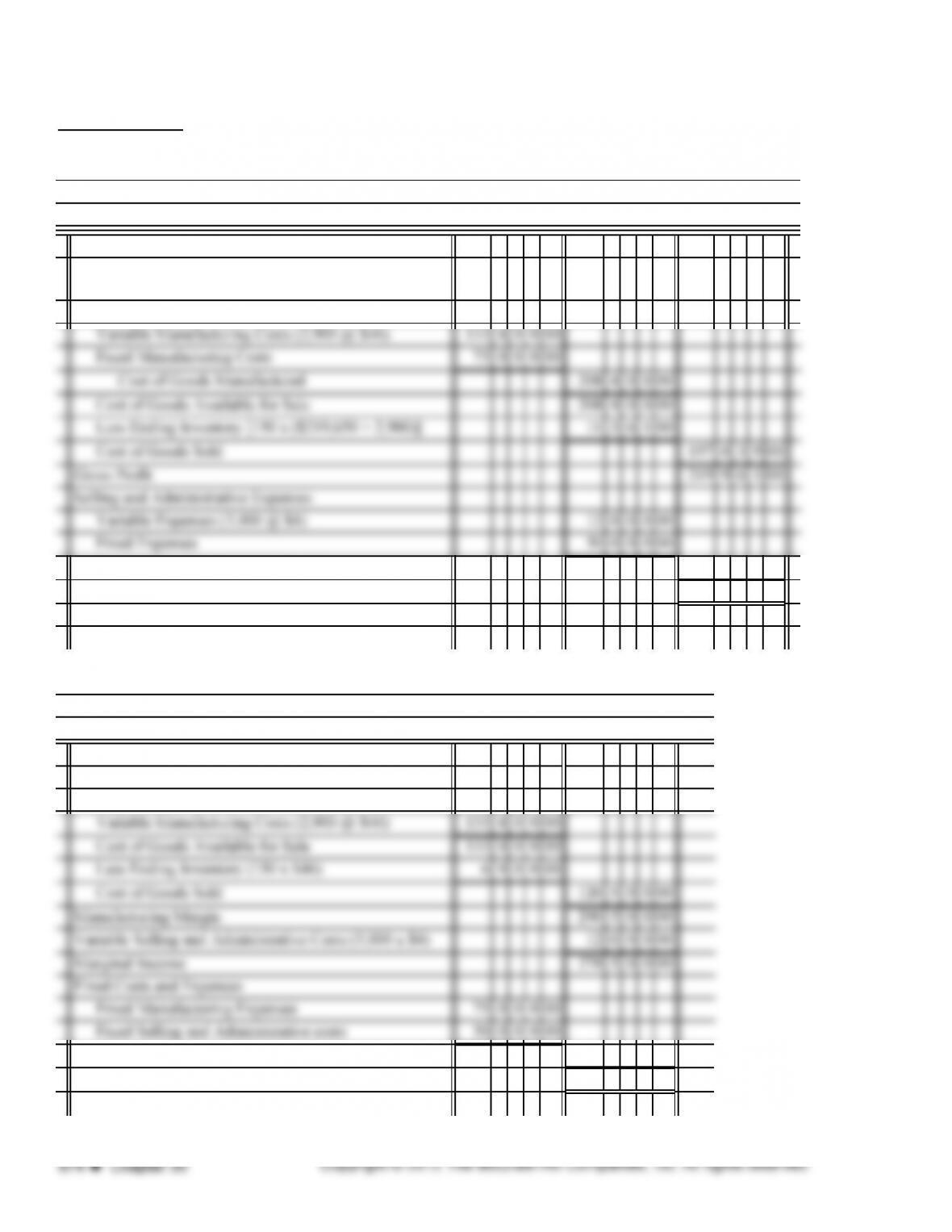

PROBLEM 30.1A

1.

Sales (3,000 units @ $139) 41700000

Cost of Goods Sold

Beginning Inventory

Total Selling and Administrative Expenses 6200000

Net Income 15796100

2.

Sales (3,000 units @ $139) 41700000

Cost of Goods Sold

Beginning Inventory

Total Fixed Costs and Expenses 12500000

Net Income 15350000

For Year Ended December 31, 2013

For Year Ended December 31, 2013

Income Statement (Absorption Costing)

Income Statement (Direct Costing)

Omega Corporation

Omega Corporation

PROBLEM 30.1A (continued)

Computations:

Difference in ending inventory

PROBLEM 30.2A

1.

Sales (5,000 units @ $105) 52500000

Cost of Goods Sold

Cost of Goods Manufactured

Direct Materials ($24 x 5,400) 12960000

The primary difference in net income arises from the difference in the treatment of fixed costs. In the direct

costing method, all of the fixed manufacturing costs are currently expensed. Under absorption costing, a portion

of the fixed manufacturing costs are included in the value of the ending inventory and therefore not totally

expensed.

Tech Inc.

Income Statement (Direct Costing)

Year Ended December 31, 2013

PROBLEM 30.2A (continued)

2.

Sales (400 x $75) 3000000

Variable Manufacturing Costs

Materials (400 x $24) 960000

Marginal Income on Order 360000

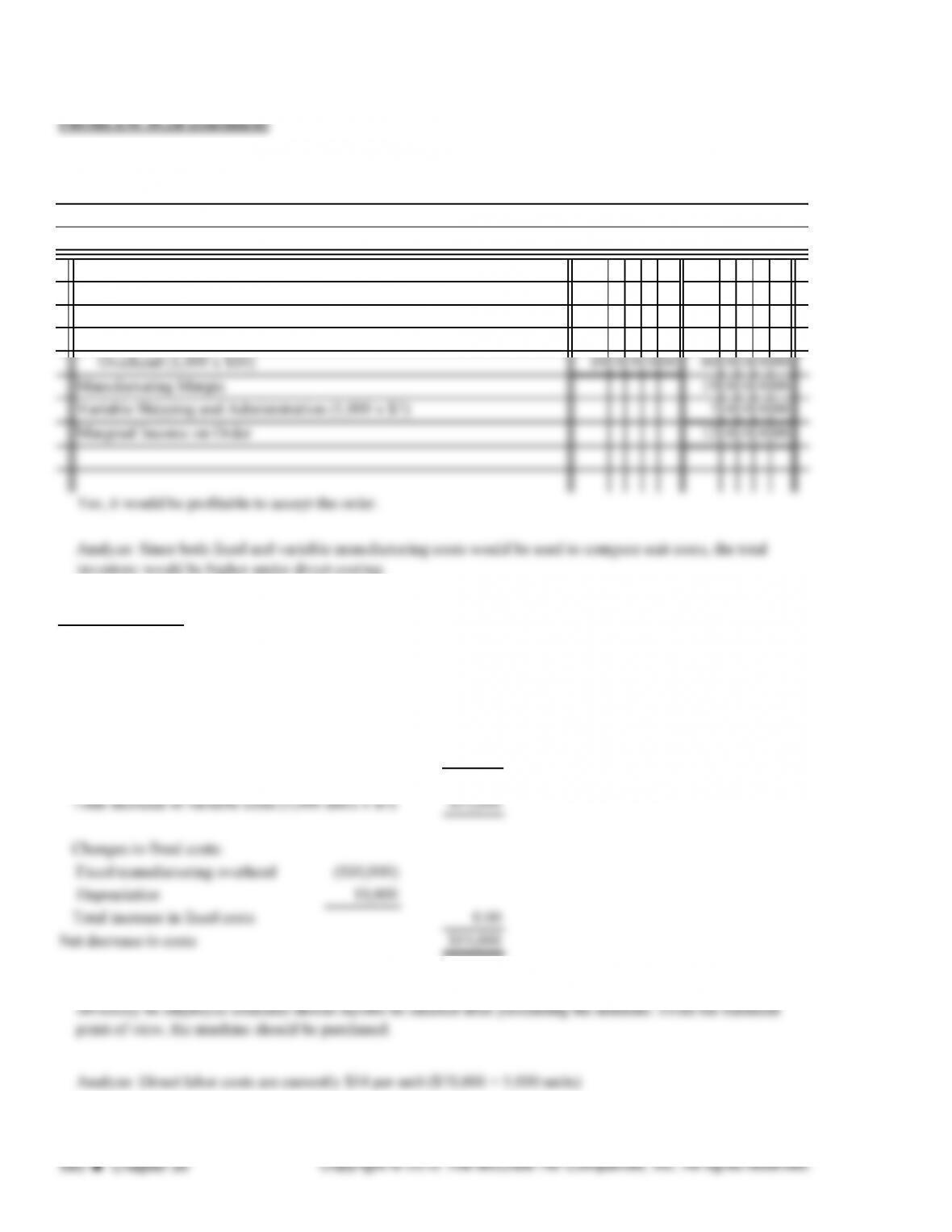

Accept the order.

PROBLEM 30.3A

1.

Decreases in variable costs:

Direct labor $8.00

Variable manufacturing overhead 1.25

Increases in fixed costs:

Fixed manufacturing overhead $40,000

2.

Computations

Foreign Sales Order

Tech Inc.

The machine will pay for itself in 4.2 years. Management should probably buy the machine. There will

ANALYSIS OF EFFECTS OF PURCHASING MACHINE

PROBLEM 30.4A

1.

Cost to purchase:

Purchase price 4 8 00

Shipping costs 5 00 5 3 00

2. There are no specific answers to the question. Areas of concern could include labor relations, effect on

Chicago Equipment Corporation

Analysis of Effects of Making or Buying a Part

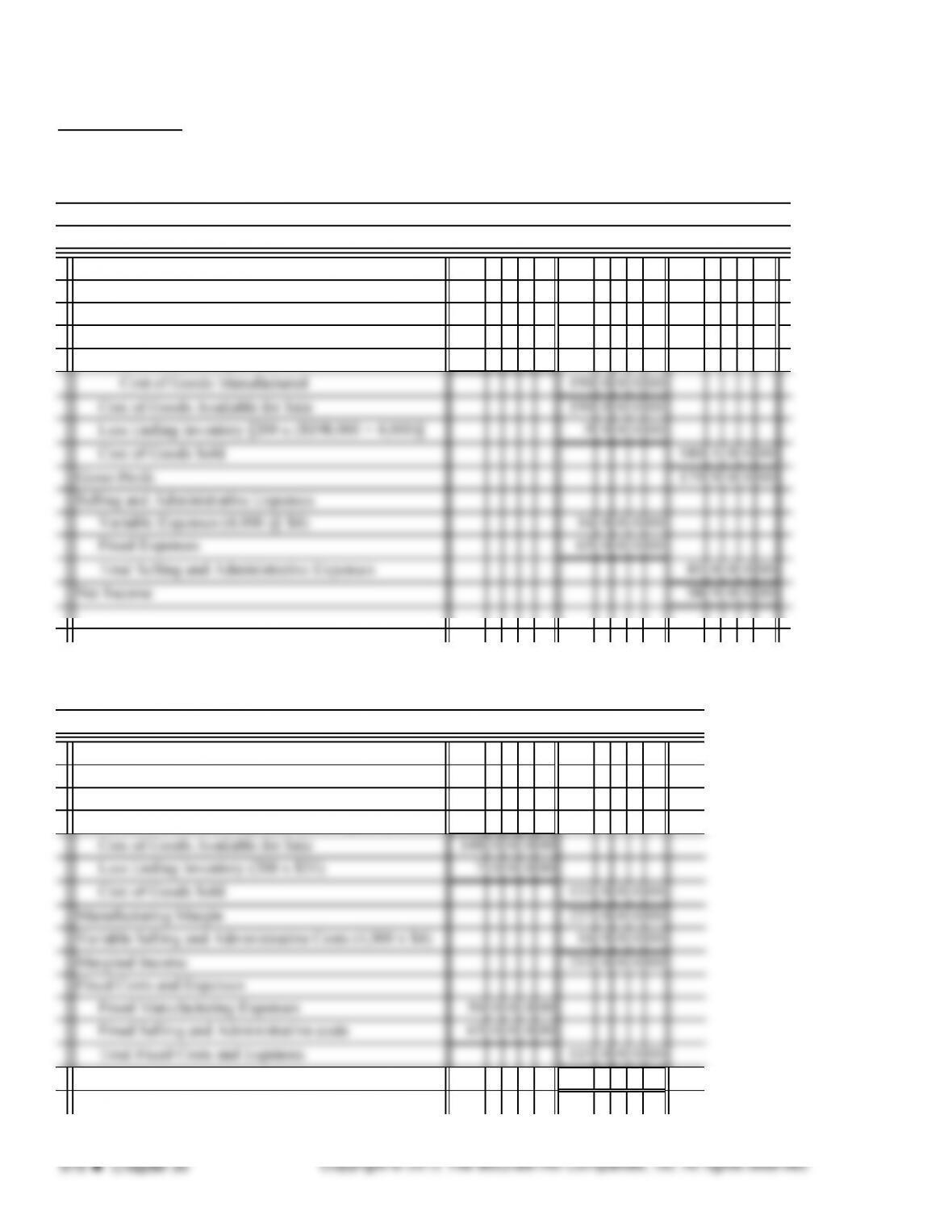

PROBLEM 30.1B

1.

Sales (4,000 units @ $90) 36000000

Cost of Goods Sold

Beginning Inventory 0 00

Variable Manufacturing Costs (4,000 @ $35) 14000000

Fixed Manufacturing Costs 5000000

2.

Sales (4,000 units @ $90) 36000000

Cost of Goods Sold

Beginning Inventory 0 00

Variable Manufacturing Costs (4,000 @ $35) 14000000

Net Income 9600000

For Year Ended December 31, 2013

LB Industries

Income Statement (Absorption Costing)

LB Industries

Income Statement (Direct Costing)

PROBLEM 30.1B (continued)

Computations:

Difference in Net Income $2,900

PROBLEM 30.2B

1.

Sales (4,800 units @ $125) 600 0 0 0 00

Cost of Goods Sold

Cost of Goods Manufactured

Direct Materials ($26 x 5,000) 130 0 0 0 00

Direct Labor ($24 x 5,000) 120 0 0 0 00

Variable Factory Overhead ($10 x 5,000) 50 0 0 0 00

Total Fixed Costs and Expenses 200 0 0 0 00

Net Income 78 4 0 0 00

Income Statement (Direct Costing)

Year Ended December 31, 2013

Pitt Corporation

The difference in net income arises from the difference in the treatment of fixed costs. In the direct costing mode,

all of the fixed manufacturing costs are expensed in the current period. Under absorption costing, a portion of the

fixed manufacturing costs are included in the value of the ending inventory and therefore not totally expensed.

2.

Sales (1,000 x $79) 79 0 0 0 00

Variable Manufacturing Costs:

Materials (1,000 x $26) 26 0 0 0 00

Labor (1,000 x $24) 24 0 0 0 00

PROBLEM 30.3B

1.

Decreases in variable costs:

Direct labor $2.00

Variable manufacturing overhead 1.00

Per unit decrease in variable costs $3.00

2.

Foreign Sales Order

Pitt Corporation

Computations

ANALYSIS OF EFFECTS OF PURCHASING MACHINE

The machine will pay for itself in 3.3 years. Management should probably buy the machine. There will

obviously be employee concerns should layoffs be enacted after purchasing the machine. From the financial

point of view, the machine should be purchased.

Analyze: Since both fixed and variable manufacturing costs would be used to compute unit costs, the total

inventory would be higher under direct costing.

PROBLEM 30.4B

1.

Cost to purchase:

Purchase price 8 5 00

Shipping costs 5 00 9 0 00

2. There are no specific answers to the question. Areas of concern could include labor relations,

effect on suppliers, effect on current customers, and the opportunity to take on new production.

Analyze:

The $1 reduction in shipping would still have the cost of purchase at $89, more than the cost to

produce the unit.

Cal Computer Company

Analysis of Effects of Making or Buying a Part

CRITICAL THINKING PROBLEM 30.1

CRITICAL THINKING PROBLEM 30.1

1

I f 4 h Q 2013 i l l d

1.

Income for 4th Quarter 2013 is calculated:

1.

Income for 4th Quarter 2013 is calculated:

Sl

20

0

0

0

00

Sales

20

0

0

0

00

Cost and Expenses

Cost and Expenses

p

Variable Costs

Variable Costs

Product Costs

10

0

0

0

00

Product Costs

10

0

0

0

00

i

Containers

8

0

0

00

Containers

8

0

0

00

F i ht I

4

0

0

00

Freight In

4

0

0

00

g

Delivery

4

0

0

00

Delivery

4

0

0

00

Sales Commission

4

0

0

0

00

Sales Commission

4

0

0

0

00

Advertising

2

0

0

0

00

Advertising

2

0

0

0

00

Wh i

4

0

0

00

Warehousing

4

0

0

00

Warehousing

4

0

0

00

Oth V i bl

6

0

0

00

Other Variable

6

0

0

00

Total Variable Costs

18

6

0

0

00

Total Variable Costs

18

6

0

0

00

Contribution Margin

1

4

0

0

00

Contribution Margin

1

4

0

0

00

Advertising

5

0

0

00

Advertising

5

0

0

00

Warehousing

2

0

0

00

Warehousing

2

0

0

00

O h fi d

3

0

0

00

Other fixed costs

3

0

0

00

Other fixed costs

3

0

0

00

TtlFi dC t

1

0

0

0

00

Total Fixed Costs

1

0

0

0

00

Net Income

4

0

0

00

Net Income

4

0

0

00

2

Bdl h lli h i ldb i i h d b i

2.

Based only on the calculations shown, it would be appropriate to continue the product because it

2.

Based only on the calculations shown, it would be appropriate to continue the product because it

contributes $1 400 toward paying the fixed costs

contributes $1,400 toward paying the fixed costs.

3

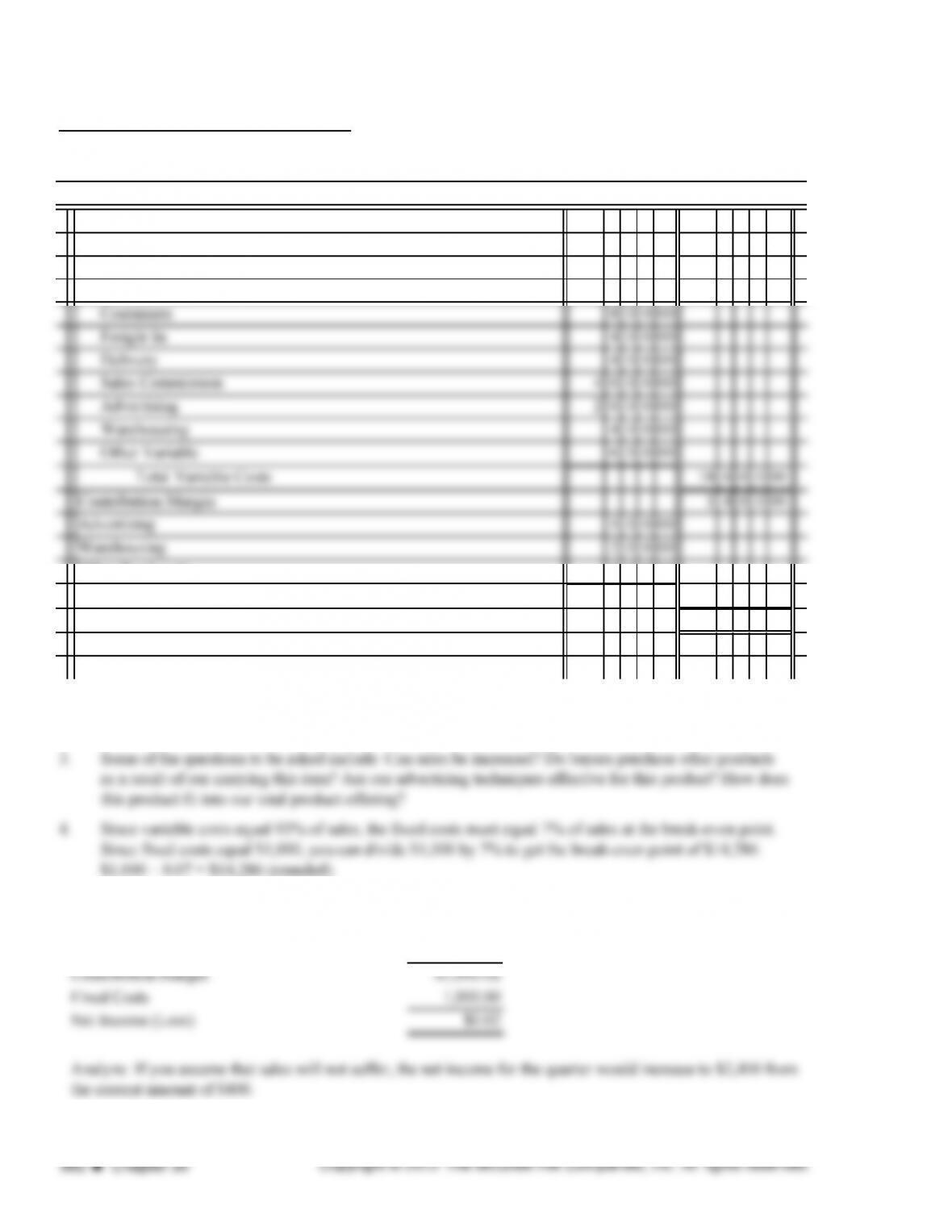

Some of the questions to be asked include: Can sales be increased? Do buyers purchase other products

3.

Some of the questions to be asked include: Can sales be increased? Do buyers purchase other products

lf i hii d ii hi ff i f hi d d

as a result of our carrying this item? Are our advertising techniques effective for this product? How does

as a result of our carrying this item? Are our advertising techniques effective for this product? How does

this product fit into our total product offering?

this product fit into our total product offering?

4

Si i bl t l 93% f l th fi d t t l 7% f l t th b k i t

4.

Since variable costs equal 93% of sales, the fixed costs must equal 7% of sales at the break-even point.

.

S ce v b e cos s equ 93% o s es, e ed cos s us equ 7% o s es e b e eve po .

Since fixed costs equal $1 000 you can divide $1 000 by 7% to get the break-even point of $14 286:

Since fixed costs equal $1,000, you can divide $1,000 by 7% to get the break-even point of $14,286:

$$

$1,000 ÷ 0.07 = $14,286 (rounded).

$1,000 0.07 $14,286 (rounded).

Sales

$14 286 00

Sales

$14,286.00

Variable costs (93% x 14 286)

13 285 98

Variable costs (93% x 14,286)

13,285.98

Contribution Margin

$1,000.02

Contribution Margin

$1,000.02

Fi d C t

1 000 00

Fixed Costs

1,000.00

,

Net Income (Loss)

$0 02

Net Income (Loss)

$0.02

()

Analyze: If you assume that sales will not suffer the net income for the quarter would increase to $2 400 from

Analyze: If you assume that sales will not suffer, the net income for the quarter would increase to $2,400 from

hf$

the current amount of $400.

the current amount of $400.

CRITICAL THINKING PROBLEM 30.2

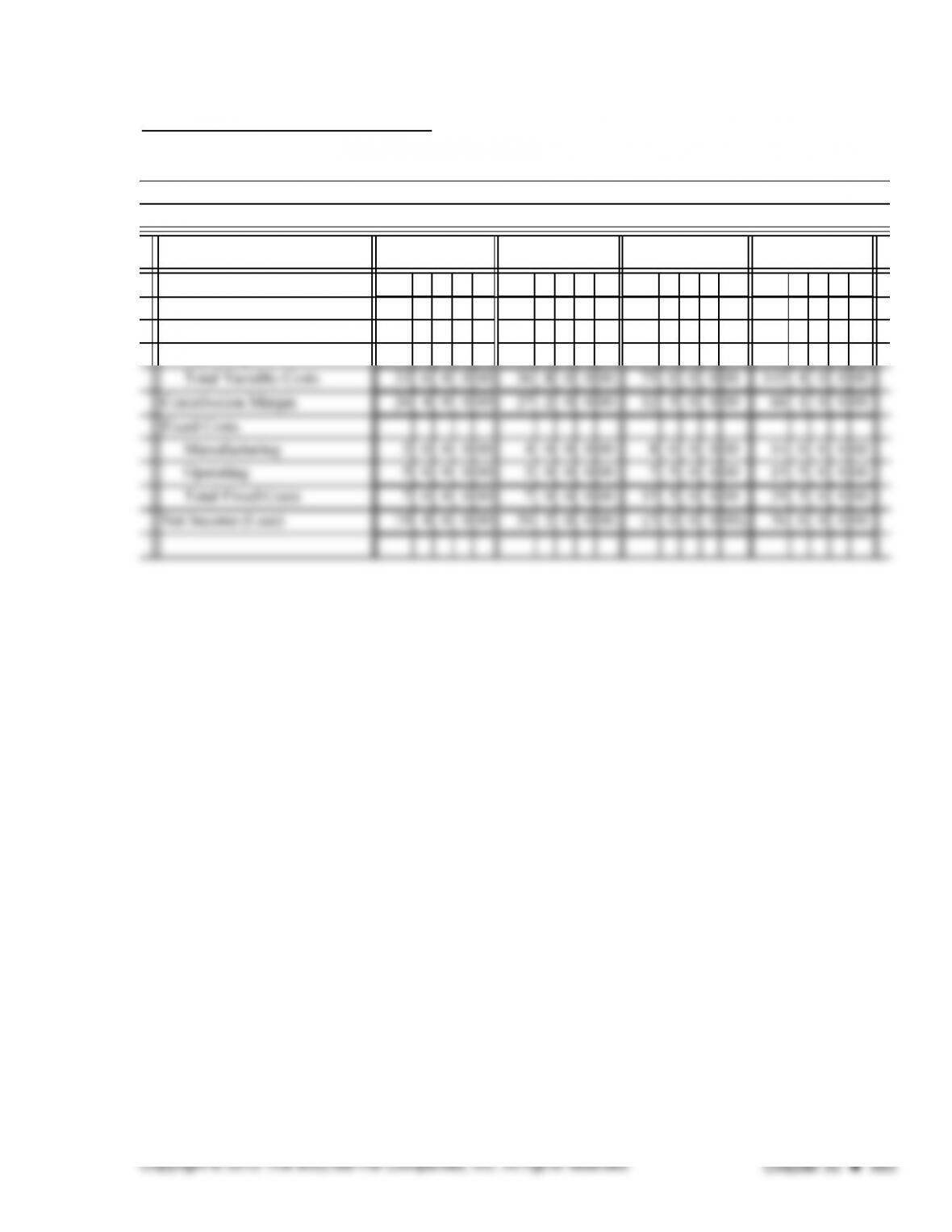

Sales 60 0 0 0 00 64 0 0 0 00 87 5 0 0 00 211 5 0 0 00

Variable Costs

Manufacturing 26 4 0 0 00 28 8 0 0 00 57 5 0 0 00 112 7 0 0 00

Operating 720000 800000 1750000 3270000

Bruin Manufacturing, Inc.

Income Statement (Direct Costing)

ITEM 101 ITEM 102 ITEM 103 TOTAL

CRITICAL THINKING PROBLEM 30.2 (continued)

1.

2. If sales price of Item 103 is increased to $40, resulting in unit sales of 1,000 units:

Sales $40,000.00

Variable Costs:

Manufacturing costs $23,000.00

Operating costs 7,000.00 30,000.00

3.

Sales $52,500.00

Manufacturing costs $16,500.00

Operating costs 12,000.00 28,500.00

Contribution Margin $24,000.00

If Item 103 were discontinued, $12,500.00 that is currently being generated through the contribution

margin to assist with fixed costs would be eliminated.

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

2. Identify variable costs, shipping costs, implications to existing customers.

4. Plant capacity, variable and fixed manufacturing costs, differential cost savings.

Ethical Dilemma:

Financial Statement Analysis:

Making Decisions Using Financial Data

1. Because of the decrease in weekly sales and weighted average sales per square foot, you should probably be

2. The 10-year compounded annual growth was for the average ticket sale is 0.8 percent. The percentage

Teamwork:

Internet Connection:

Upper management should be notified immediately. Brad should complete his analysis and show the corporate

Do you have the factory space? Do you have adequate work force? Is your vendor able to provide additional

material? What are the sunk costs? What are the opportunity costs? Is there a demand for twice the amount of the

product? How long will it take to pay it back?

The IRS website contains a series of business tips and educational features such as how to handle inventory.

Part A True-False

1. TRUE

3. FALSE

5. FALSE

7. TRUE

9. FALSE

11. FALSE

13. TRUE

15. FALSE

17. TRUE

Part B Matching

1. c

3. b

5. f

SOLUTIONS TO PRACTICE TEST