• Revenue for Harley-Davidson was $4.2 billion in 2009.

• In 2009, the Company shipped 223,023 Harley-Davidson motorcycles worldwide, compared to 303,479 in

2008.

• Harley-Davidson consistently makes Fortune magazine’s annual “100 Best Companies to Work For” list.

• Every year, about one-half of all new Harley-Davidson® motorcycles are sold to existing Harley® owners.

• One of the company’s strongest assets is H.O.G.®, the Harley Owners Group®, which has over one million

members around the globe.

• Harley-Davidson offers more than 5,500 different Genuine Motor Accessories

• These questions are designed to check students’ understanding of new terms, concepts, and procedures

presented in the chapter.

2. They do not change on a per unit basis as the level of activity changes.

4. Method that determines the fixed and variable components of a semivariable cost.

6. Financial plan based on levels of activity.

8. Shows budgeted costs for several levels of activity, dividing costs between fixed and variable portions.

10. Anticipated costs of making a product under efficient but obtainable work conditions.

12. Human resources.

14. Whether company paid more or less than expected for materials.

16. Production manager.

Note to instructor : These questions are designed to check students’ understanding of new terms, concepts, and

procedures presented in the chapter.

Discussion Questions

CHAPTER 29

CONTROLLING MANUFACTURING COSTS: STANDARD COSTS

Chapter Opener: Thinking Critically

Manufacturing firms like Harley-Davidson often create flexible budgets, accounting for variable levels of

production activity and the associated fixed and variable costs.

Fast Facts

Managerial Implications: Thinking Critically

17. The possible causes of materials variances are: prices of materials rise higher than budgeted; more materials

18. The possible causes of labor variances are: actual hours worked were more or less than hours budgeted;

19. The possible causes of overhead variances are: fixed overhead costs such as wages, insurance, or taxes are

EXERCISE 29.1

Quarter Direct Labor Hours Utilities Cost

3rd–highest quarter 15,000 $3,500

EXERCISE 29.2

95% 100% 105%

Total Budgeted Direct Labor Hours 14,250 15,000 15,750

EXERCISE 29.3

Standard cost per unit of product:

Materials (2 × $10) $20

Percent of Budgeted Hours

EXERCISE 29.4

Standard Cost Actual Cost

Materials:

Standard: 20,000 gallons @ $1.00 $20,000

Actual: 20,200 gallons @ $1.05 $21,210

Labor:

EXERCISE 29.5

Standard cost of materials

Actual cost of materials $20,000

EXERCISE 29.6

Quantity variance for materials:

EXERCISE 29.7

Price variance for materials:

(Standard price í Actual price) × actual useage

Cost Element

EXERCISE 29.8

Standard cost for labor (2,500 hrs × $16.00) $40,000

EXERCISE 29.9

Quantity variance for labor:

(Standard hours í Actual hours) × Standard rate

EXERCISE 29.10

Rate variance for labor:

(Standard rate í Actual rate) × Actual hours

EXERCISE 29.11

Total overhead variance

Standard overhead (50% of direct labor) $20,000

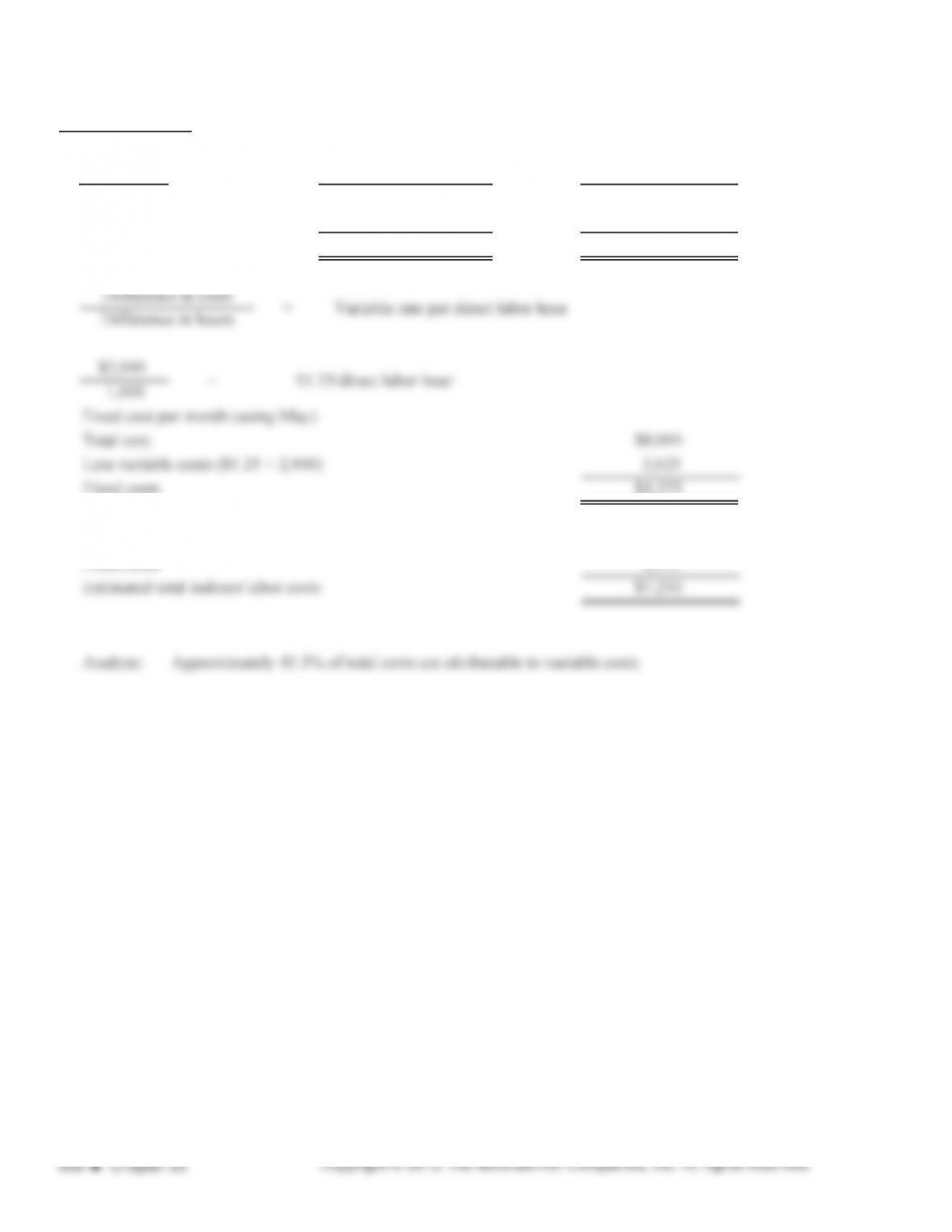

PROBLEM 29.1A

1. Month Direct Labor Hours Indirect Labor Costs

May (high) 2,900 $8,000

February (low) 1,300 $6,000

Differences 1,600 $2,000

Fixed costs $4,375

2. Variable costs ($1.25 × 2,300 hours) = $2,875

Fixed costs 4,375

Difference in costs = Variable rate per direct labor hour

Difference in hours

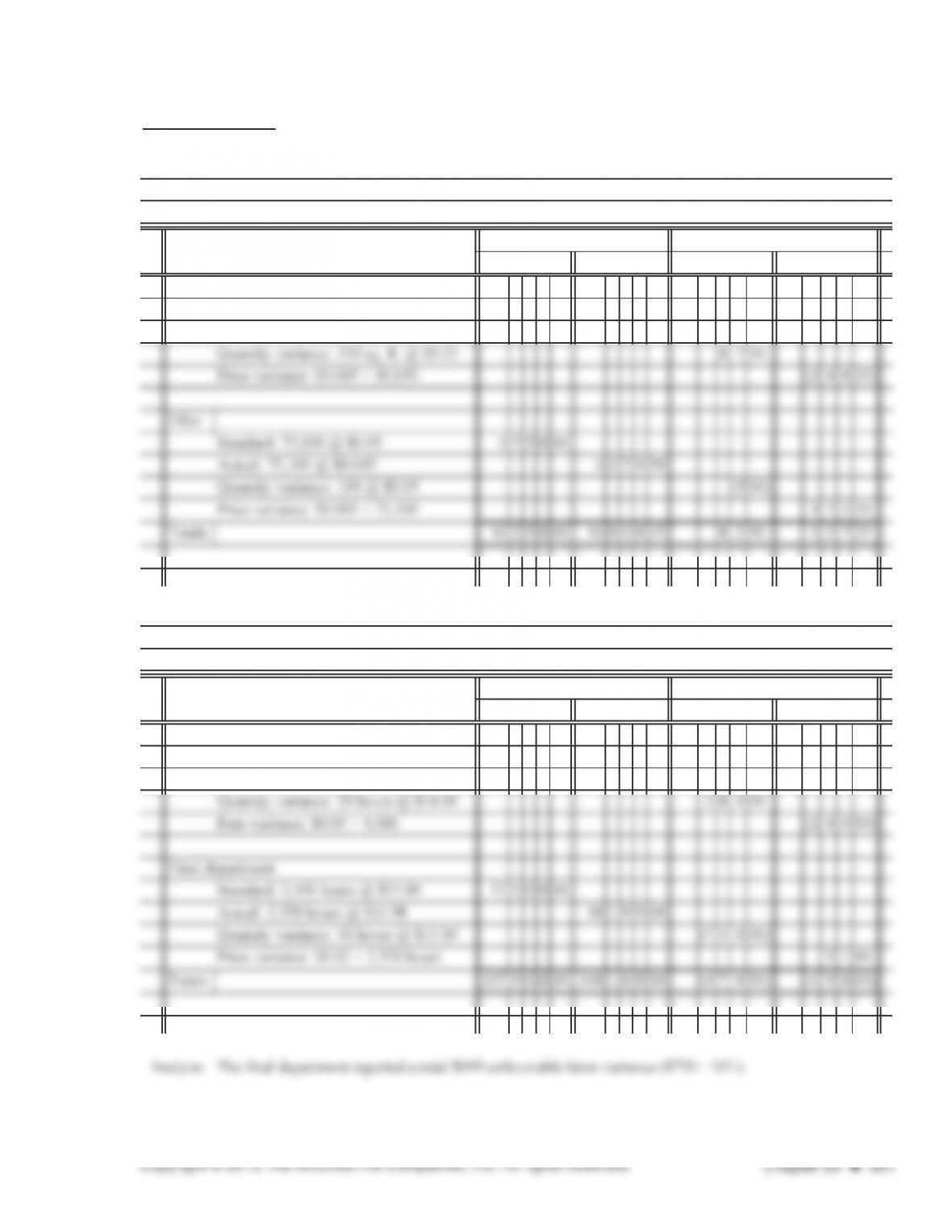

PROBLEM 29.2A

1.

Number of direct hours 2250hrs 2500hrs 2750hrs

Percent of expected capacity 9 0 % 1 0 0 % 1 1 0 %

Variable costs

Indirect labor ($1.00/hour) 225000 250000 275000

Total manufacturing costs 871250 922500 973750

2.

Indirect labor [$1,800 + ($1.00 × 1,900)] 3 7 0 0 00 3 6 5 0 00 5 0 00

Payroll taxes [$100 + ($0.25 × 1,900)] 5 7 5 00 3 7 5 00 2 0 0 00

Flexible Budget for Manufacturing Overhead

Month of May 2013

Bibee Products, Inc.

Bibee Products, Inc.

ACTUAL

BUDGET

FOR

1,900

HOURS OVER UNDER

Manufacturing Overhead Budget Performance Report

Month of May 2013

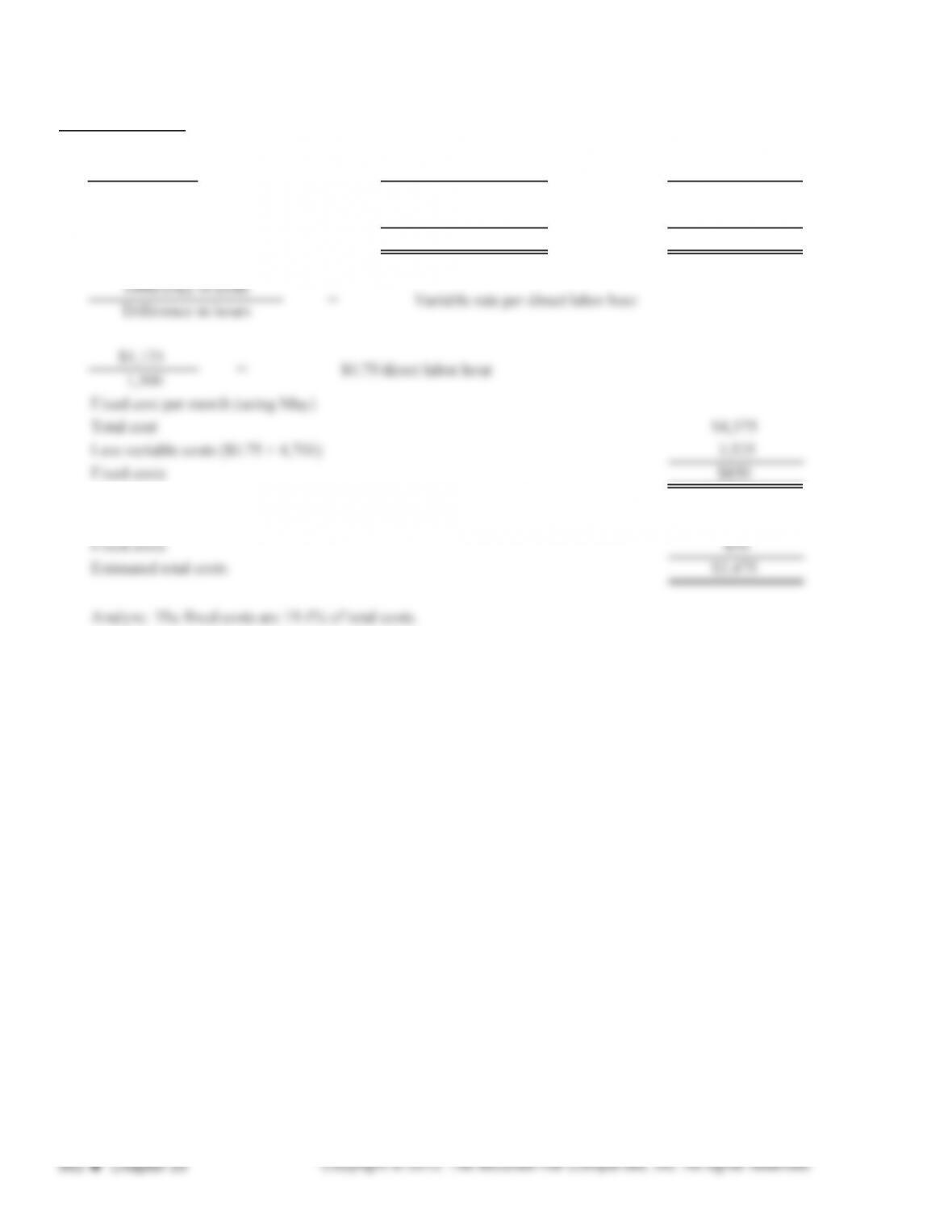

PROBLEM 29.3A

1

.

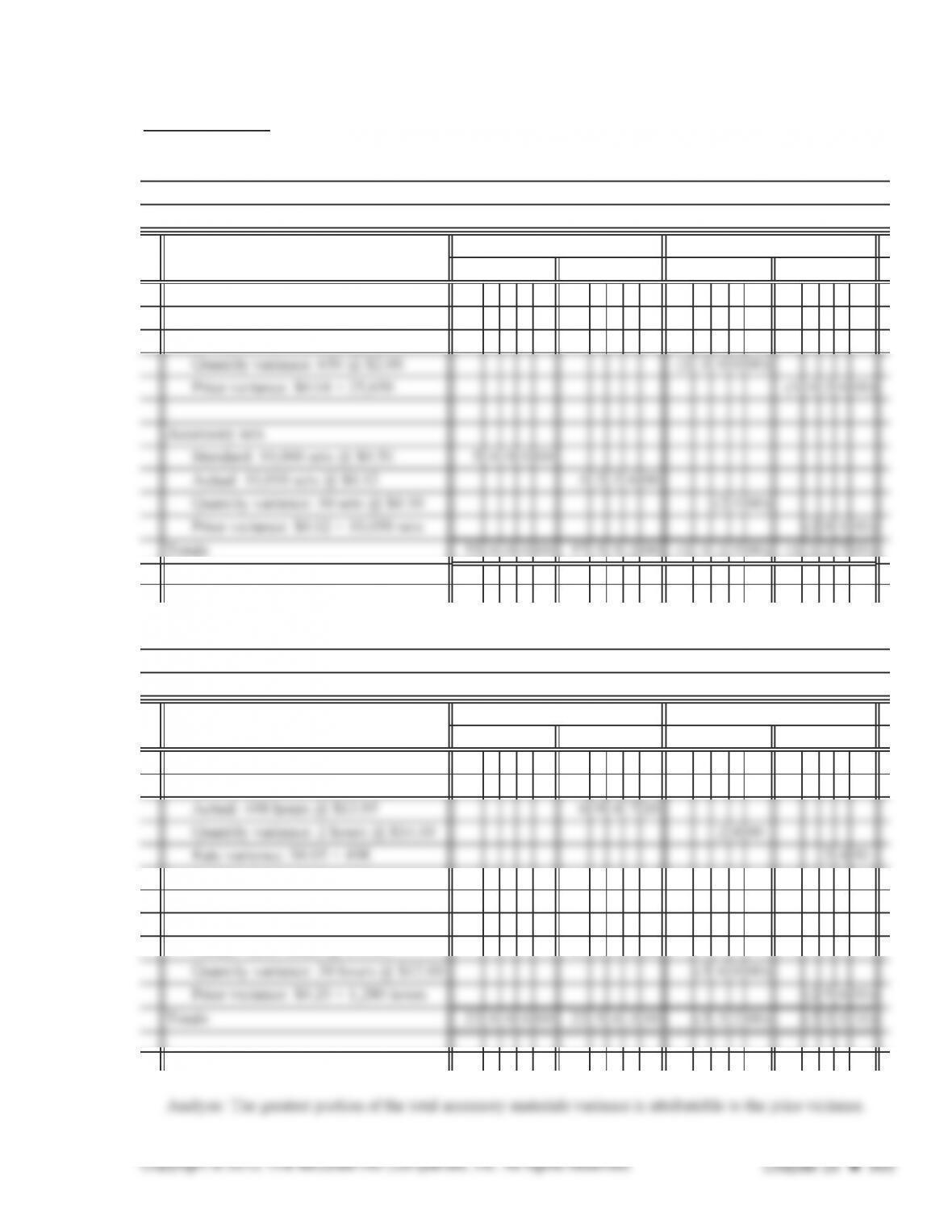

Starter

Standard: 7,000 gal @ $0.40 (Note 1) 280000

Actual: 7,050 gal @ $0.38 267900

Quantity variance: 50 gal @ $0.40 (2 0 00)

Activator

Standard: 500 gal @ $12.00 600000

Actual: 490 gal @ $12.20 597800

2

.

Starter

Analyze: Only the starter liquid was purchased at less than the standard price.

$2,800.00 $2,679.00 $121.00

Standard Actual Variance

Analysis of Materials Variance

For Month of June 2013

Cal Chemical Company

COST ELEMENTS

COSTS VARIANCES

STANDARD ACTUAL QUANTITY PRICE

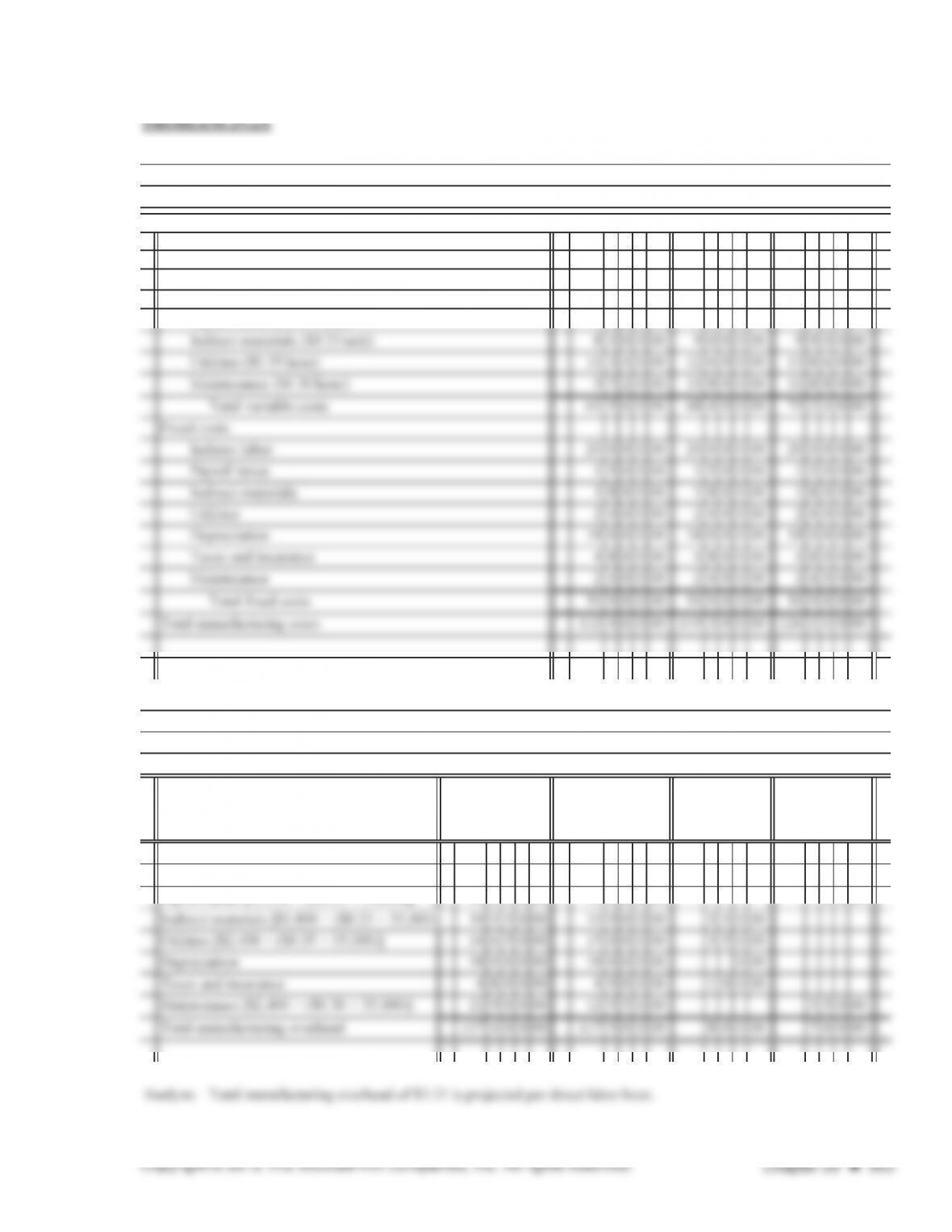

PROBLEM 29.4A

1.

Framing

Standard: 50,000 sq. ft. @ $0.25 1250000

Actual: 49,650 sq. ft. @ $0.255 1266075

2.

Cutting department

Standard: 5,000 hours @ $14.00 7000000

Actual: 4,980 hours @ $14.05 6996900

Evad Manufacturing Company

Analysis of Labor Variances

For Month of March 2013

COST ELEMENTS

COSTS

Evad Manufacturing Company

Analysis of Materials Variances

For Month of March 2013

COST ELEMENTS

COSTS VARIANCES

VARIANCES

QUANTITY

QUANTITY

STANDARD PRICE

PRICE

ACTUAL

ACTUALSTANDARD

PROBLEM 29.1B

1. Month Direct Labor Hours Utility Costs

May (high) 4,700 $4,375

January (low) 3,200 3,250

Differences 1,500 $1,125

2. Variable cost ($0.75 × $3,500) = $2,625

Difference in costs = Variable rate per direct labor hour

Difference in hours

1.

Number of direct hours 32400hrs 36000hrs 39600hrs

Percent of expected capacity 9 0 % 1 0 0 % 1 1 0 %

Variable costs

Indirect labor ($0.75/hour) 2430000 2700000 2970000

Payroll taxes ($0.25/hour) 810000 900000 990000

2.

Indirect labor [$20,000 + ($0.75 × 35,000)] 4625000 4595000 30000

Payroll taxes [$1,500 + ($0.25 × 35,000)] 1025000 1020000 5000

OVER UNDER

BUDGET FOR

35,000 HOURS

1,900 HOURS ACTUAL

Atlanta Manufacturing Company

Flexible Budget for Manufacturing Overhead

Year Ended December 31, 2013

Atlanta Manufacturing Company

Flexible Budget for Manufacturing Overhead

Year Ended December 31, 2013

PROBLEM 29.3B

1.

Plastic Base

Standard: 22,000 lbs @ $0.65 (Note 1) 1430000

Actual: 22,100 lbs @ $0.64 1414400

Tint

Standard: 1,000 lbs @ $0.22 2 2 0 00

Hardener

Standard: 2,000 lbs @ $0.65 130000

Actual: 2,050 lbs @ $0.66 135300

Note 1: 2,500 pounds are needed for each batch. If 25,000 pounds are to be produced, 10 batches must be

manufactured. Total production cost standards must be prepared for 10 batches.

2.

Plastic Base

Synthetic Manufacturing Co.

Analysis of Materials Variance

For Month of July 2013

COST ELEMENTS

COSTS VARIANCES

ACTUAL PRICESTANDARD QUANTITY

$14,300.00 $14,144.00 $156.00

Standard Actual

Variance

PROBLEM 29.4B

1.

Raw Material

Standard: 25,000 sections @ $2.00 50 0 0 0 00

Actual: 25,650 sections @ $2.04 52 3 2 6 00

2.

Cutting department

Standard: 500 hours @ $14.00 700000

Accessory department

Standard: 1,250 hours @ $12.00 15 0 0 0 00

Actual: 1,280 hours @ $12.20 15 6 1 6 00

Leather Products Company

Analysis of Labor Variances

For Month of January 2013

COST ELEMENTS

COSTS VARIANCES

STANDARD ACTUAL QUANTITY PRICE

Leather Products Company

Analysis of Materials Variance

For Month of January 2013

COST ELEMENTS

COSTS VARIANCES

STANDARD ACTUAL QUANTITY PRICE

CRITICAL THINKING PROBLEM 29.1

1. Standard materials cost ($1.15 × 5,000) $5,750

2. Unfavorable materials quantity variance $115.00

Standard cost per gallon $1.15

3. Total favorable materials variance $38.00

4. Unfavorable labor rate variance $1,050.00

Actual hours worked 1,050

5. Actual labor rate $19.00

6. Actual labor cost $19,950.00

Standard labor cost 18,000.00

CRITICAL THINKING PROBLEM 29.2

Standard labor rate $15.00

The equation that expressed the computation of the total labor variance is

Putting this into an equation gives the following:

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

1. The distinction helps managers identify known cash needs from variable needs.

3. Can result from difference in quality and/or difference in volume purchased.

5. Shared between personnel department and factory line supervisors.

Ethical Dilemma:

Financial Statement Analysis:

Teamwork:

Shelly’s actions are questionable and are very close to unethical. It could be argued that her actions are not

unethical since she received no benefit from the lower labor rate. The only change would be the difference

between the planned and actual net income. Variances are made to indicate possible problems. Shelly’s actions

have flagged the issue she wanted to bring forth to upper management.

The materials should be wax, coloring, labels, and a box. The labor should be a worker that pours the wax and one

Part A True-False

1. FALSE

3. TRUE

5. FALSE

7. FALSE

9. TRUE

11. FALSE

13. FALSE

15. FALSE

17. FALSE

Part B Completion

2. $325,000

4. $240,000

6. $100,000

SOLUTIONS TO PRACTICE TEST