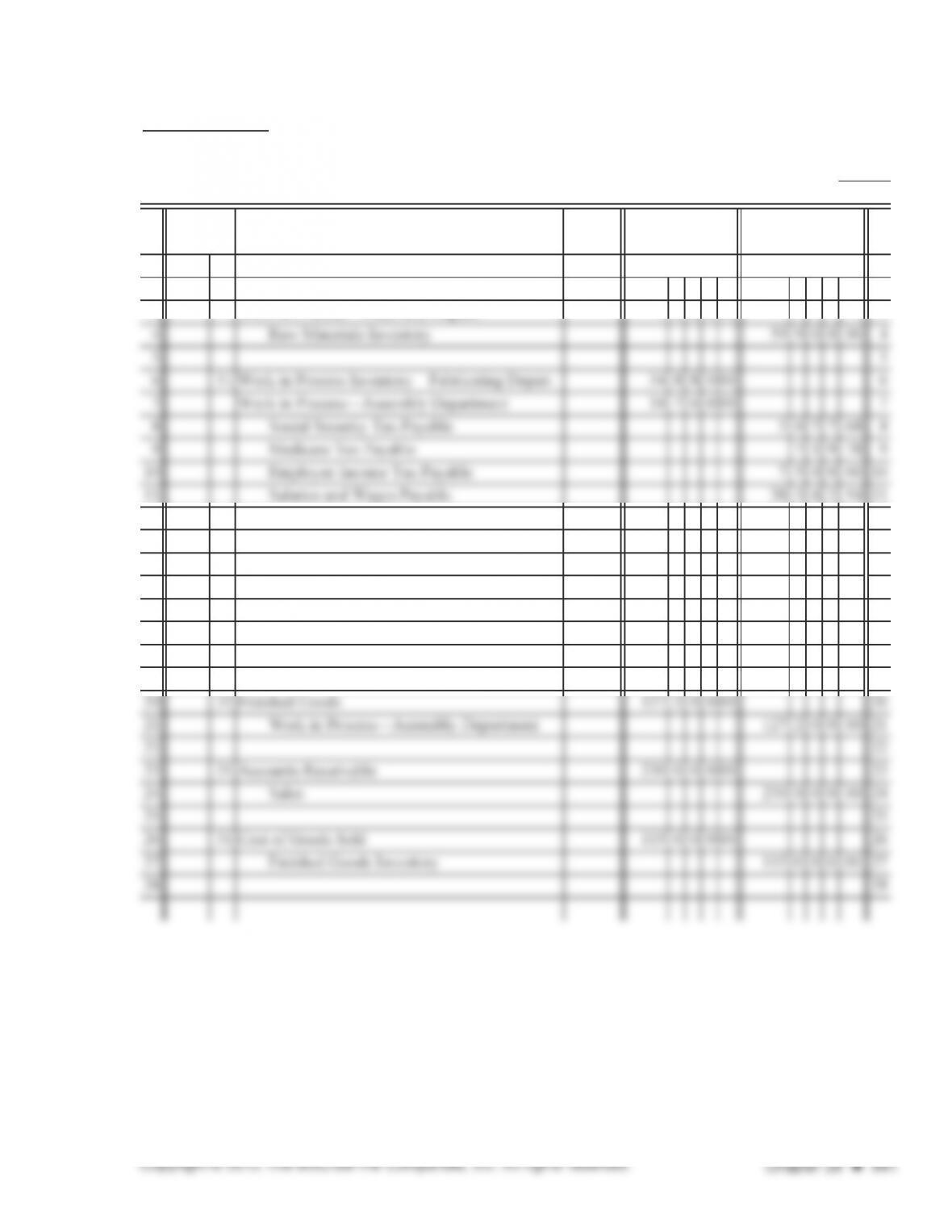

PROBLEM 28.2B

PAGE

POST.

REF.

1 2013 1

2 May 31 Work in Process Inventory—Fabricating Depart. 51 9 2 0 00 2

3 Work in Process—Assembly Depart. 798000 3

12 12

13 31 Work in Process Inventory—Fabricating Depart. 17 2 2 2 00 13

14 Work in Process—Assembly Department 10 4 5 5 00 14

15 Manufacturing Overhead 27 6 7 7 00 15

16 16

17 31 Work in Process—Assembly Department 99 7 5 0 00 17

18 Work in Process—Fabricating Department 99 7 5 0 00 18

19 19

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

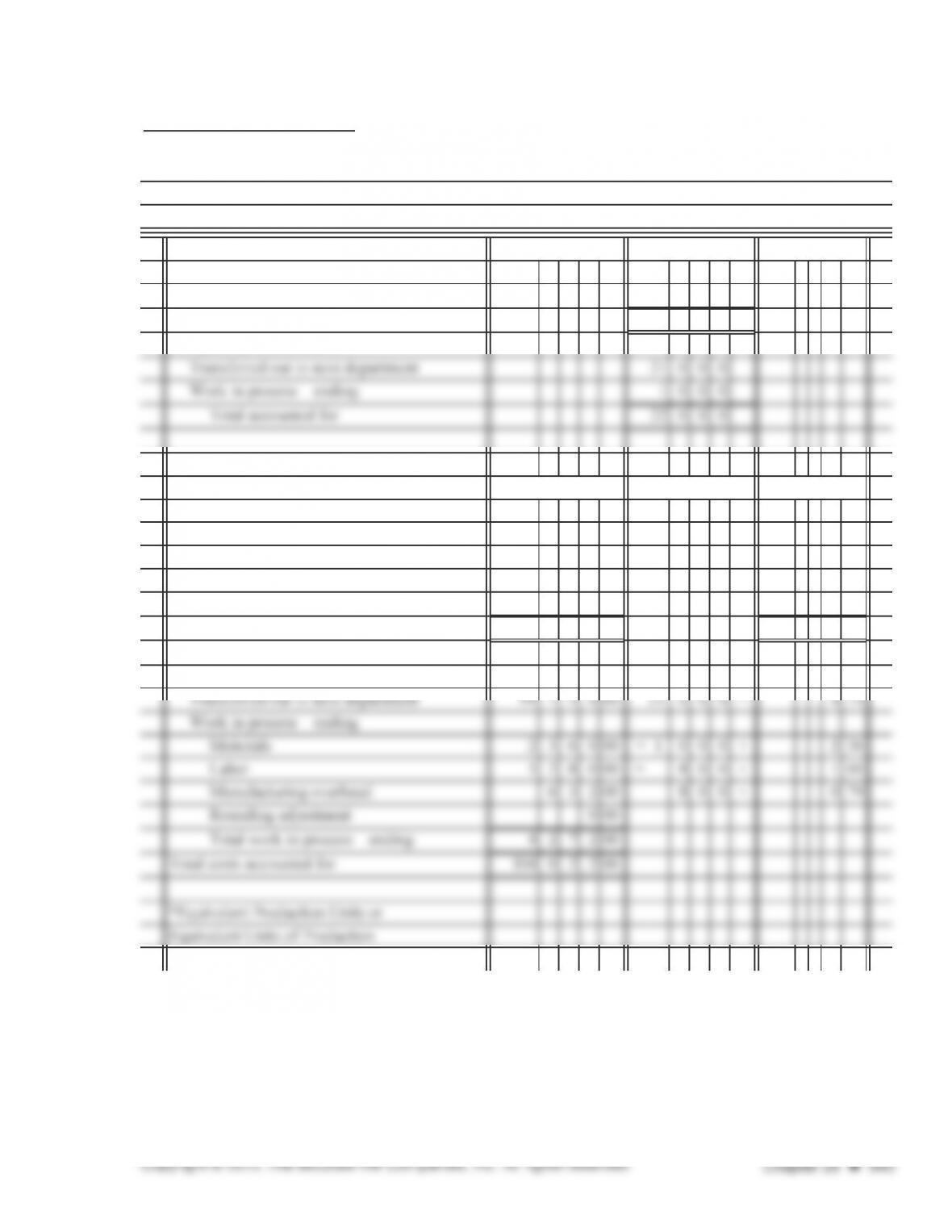

PROBLEM 28.2B (continued)

Fabricating Department

Materials: Units transferred out to next department: 100% × 21,000 units 21 0 0 0

Work in process: 100% × 1,000 units 1 0 0 0

Equivalent units of production for materials 22 0 0 0

Labor and manufacturing overhead

Labor and manufacturing overhead

Units transferred out to finished goods: 100% × 20,000 units 20 0 0 0

Work in process: 50% × 1,000 units 5 0 0

Equivalent units of production for labor and overhead 20 5 0 0

Box Makers, Inc.

Equivalent Units Production Computations

Month Ended May 31, 2013

PROBLEM 28.2B (continued)

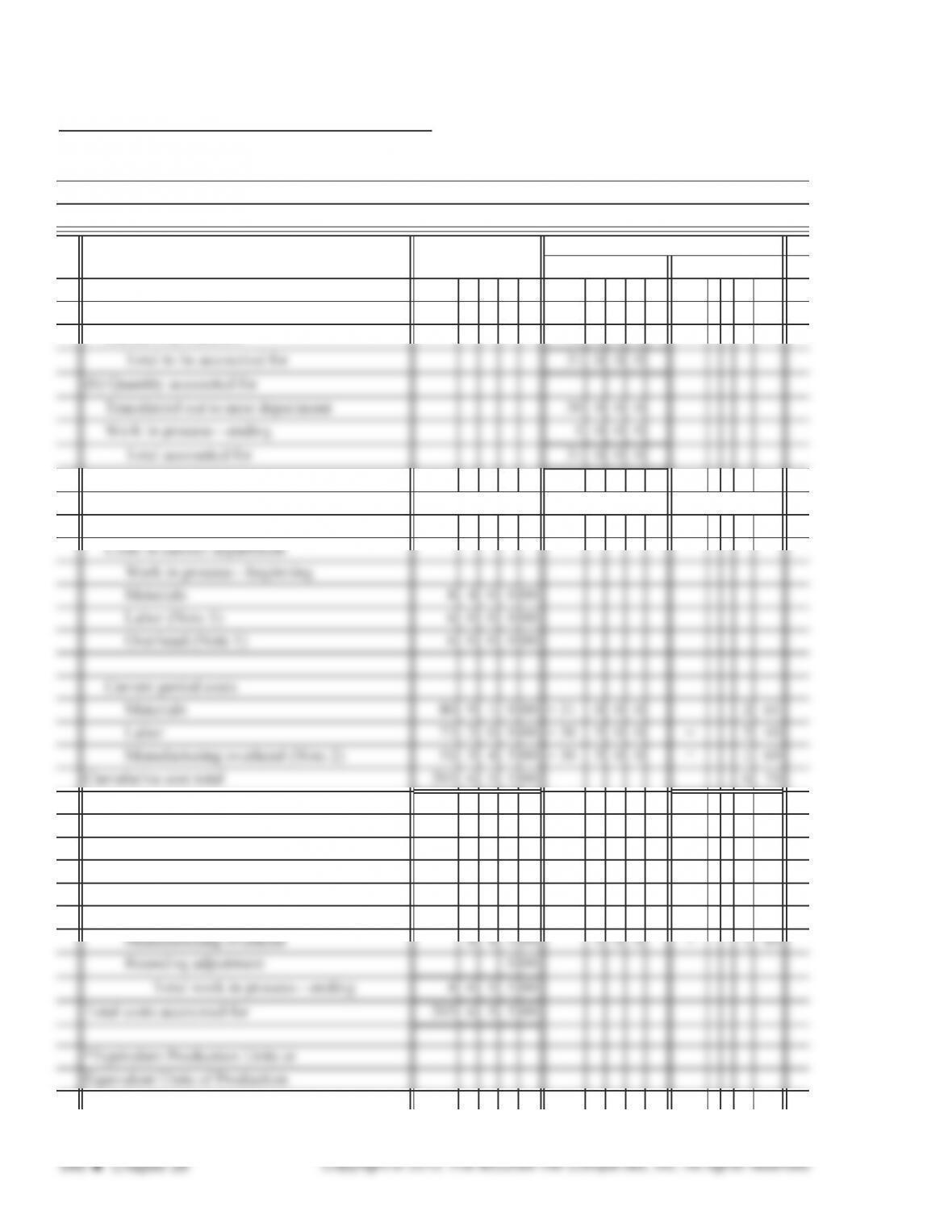

QUANTITY SCHEDULE

(a) Quantity to be accounted for

Started in production 22000

Total to be accounted for 22000

(b) Quantity accounted for

COST SCHEDULE

(c) Costs to be accounted for

Costs in current department

Materials 5192000÷ 22 000= 236

Labor 3488000÷ 21 800= 160

Manufacturing overhead 1722200÷ 21 800= 079

Cumulative cost total 104 0 2 2 00 4 75

(d) Costs accounted for

Box Makers, Inc.

TOTAL COST E.P. UNITS* UNIT COST

Cost of Production Report-Fabricating Department

Month Ended May 31, 2013

UNITS

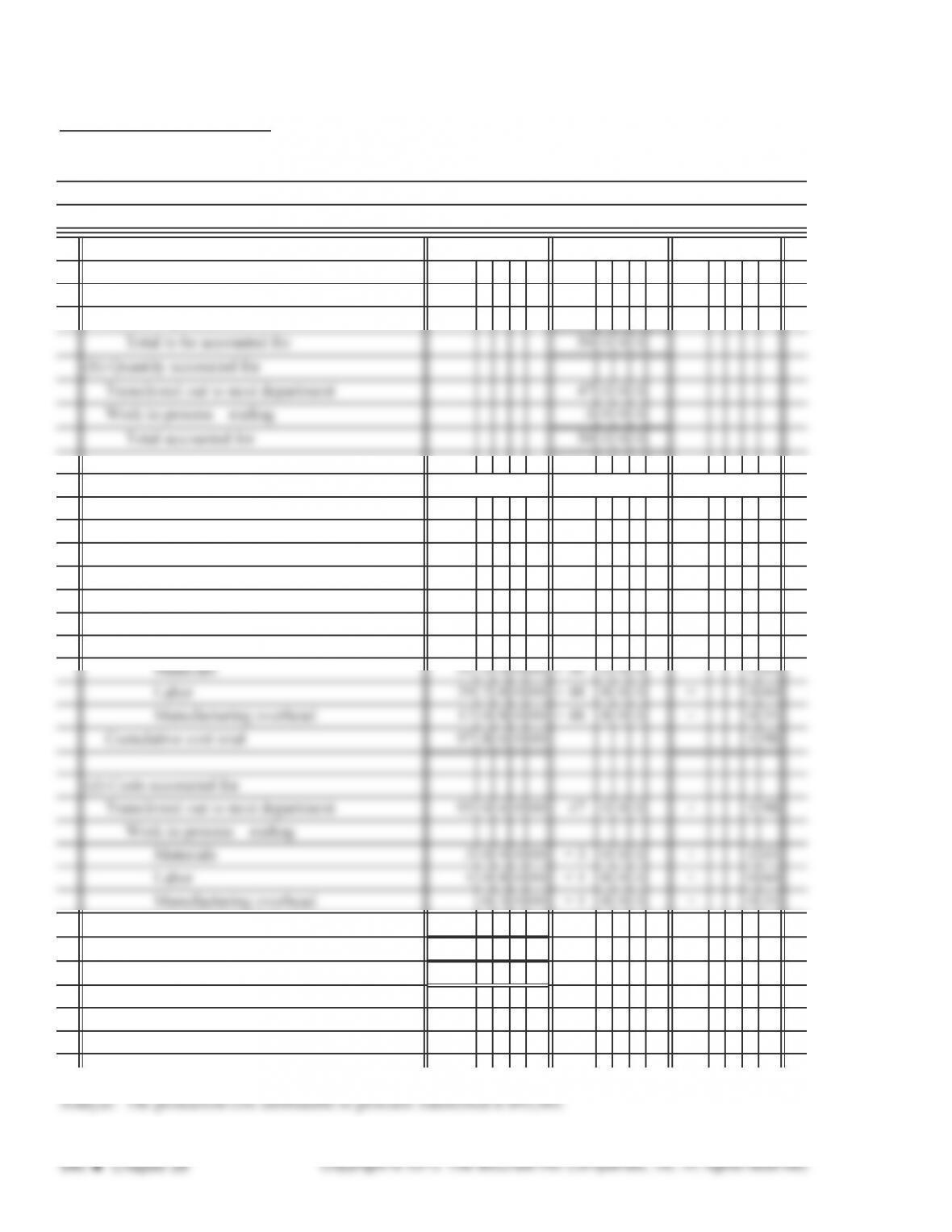

PROBLEM 28.2B (continued)

QUANTITY SCHEDULE

(a) Quantity to be accounted for

Total accounted for 21000

COST SCHEDULE

(c) Costs to be accounted for

Costs in prior department 9975000÷ 21 000= 475

Costs in current department

Materials 798000÷ 21 000= 038

Labor 1476000÷ 20 500= 072

Manufacturing overhead 1045500÷ 20 500= 051

Total current department costs 3319500 161

TOTAL COST E.P. UNITS* UNIT COST

Box Makers, Inc.

Cost of Production Report-Assembly Department

Month Ended May 31, 2013

UNITS

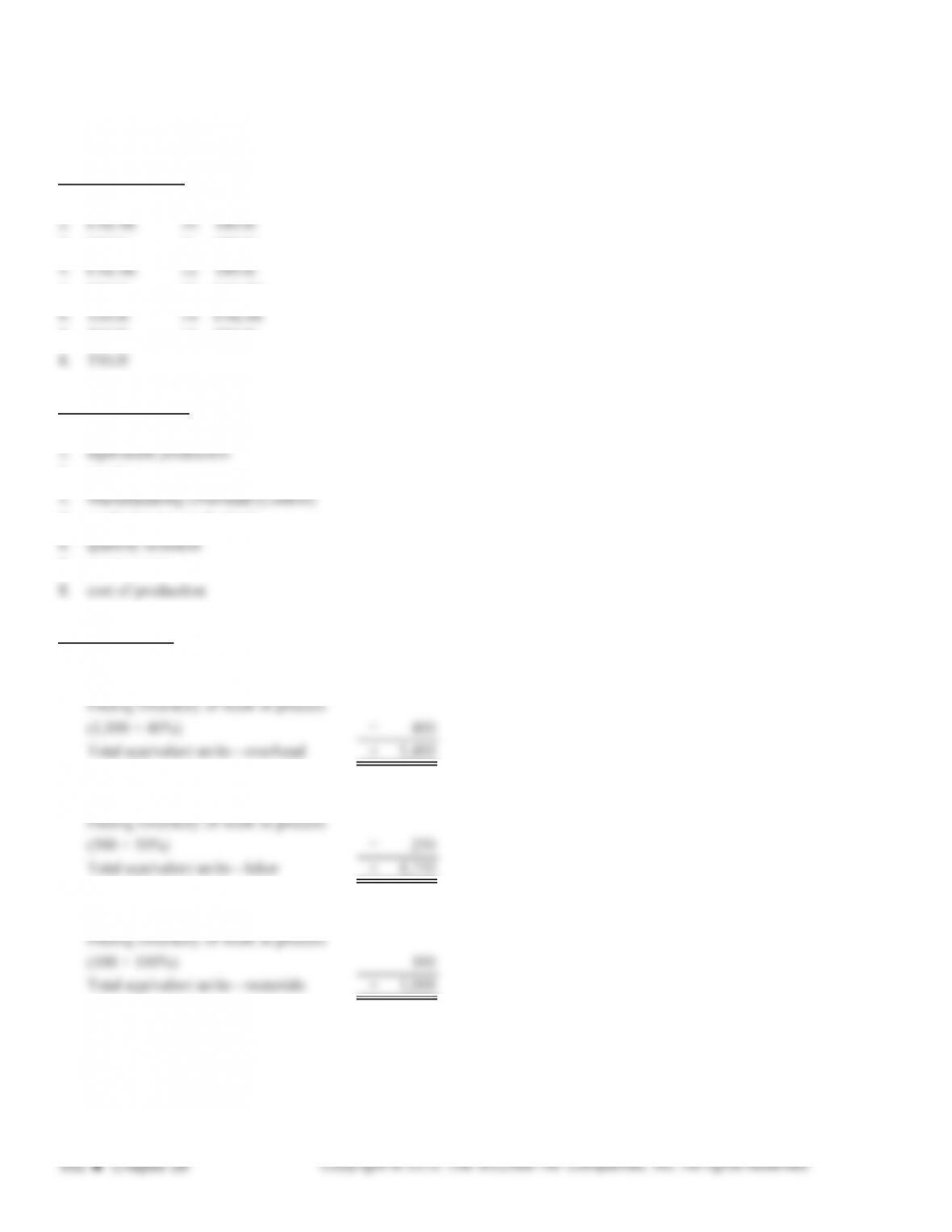

PROBLEM 28.3B

First Department

Materials: Units transferred out to next department: 100% × 47,000 units 47 0 0 0

Work in process: 100% × 3,000 units 3 0 0 0

Equivalent Unit Production Computations

Month Ended April 30, 2013

NC Chemical Company

PROBLEM 28.3B (continued)

QUANTITY SCHEDULE

(a) Quantity to be accounted for

Work in process—beginning 2000

Started in production 48 0 0 0

COST SCHEDULE

(c) Costs to be accounted for

Costs in current department

Work in process—beginning

Materials 650000

Labor 530000

Overhead 258000

Rounding adjustment 0 00

Total work in process—ending 480000

Total costs accounted for 97 8 6 0 00

*Equivalent Production Units or

Equivalent Units of Production

NC Chemical Company

TOTAL COST E.P. UNITS* UNIT COST

Equivalent Unit Production Computations

Month Ended April 30, 2013

UNITS

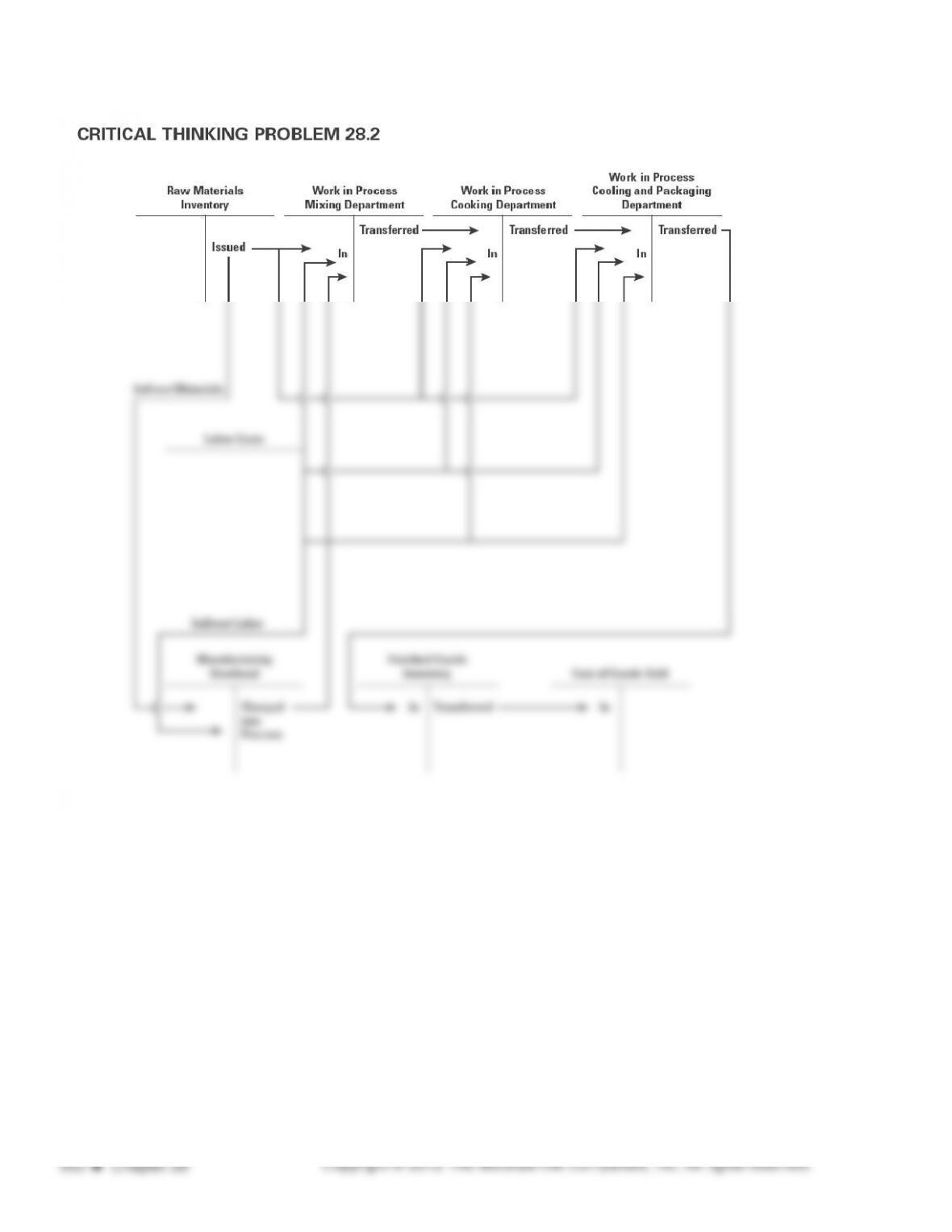

CRITICAL THINKING PROBLEM 28.1

Mixing Department

Materials: Units transferred out to next department: 100% × 30,000 units 30 0 0 0

Work in process: 100% × 1,000 units 1 0 0 0

Month Ended May 31, 2013

Texas Manufacturing, Inc.

Equivalent Unit Production Computations

CRITICAL THINKING PROBLEM 28.1 (continued)

(a) Quantity to be accounted for

Work in process—beginning 1000

Started in production 30 0 0 0

COST SCHEDULE

(c) Costs to be accounted for

(d) Costs accounted for

Transferred out to next department 201 0 0 0 00 = 30 0 0 0 × 6 70

Work in process—ending

Materials 261000 = 1 000 × 261

Labor 120000 500 × 240

Texas Manufacturing, Inc.

TOTAL COST E.P. UNITS* UNIT COST

Cost of Production Report

Month Ended May 31, 2013

QUANTITY SCHEDULE

Mixing Department

UNITS

CRITICAL THINKING PROBLEM 28.1 (continued)

Texas Manufacturing, Inc.

Equivalent Unit Production Computations

Month Ended May 31, 2013

Work in Process

,

Jul

y

1

Work

in

Process

,

July

1

$2 150 $500 $300 $2 950

$2

,

150 + $500 + $300 = $2

,

950

$2,150

$500

$300

$2,950

Finished Goods Inventory July 1

Fi

n

i

s

h

e

d

G

oo

d

s

I

nventory,

J

u

l

y

1

y, y

$10 000 + $4 500 = $14 500

$10

,

000

+

$4

,

500

=

$14

,

500

Cost

for

$10

000

+

$4

000

$4

Work

in

Process

Inventory,

$6

$1

Fi

i

h

d

G

d

I

J

l

31

$4

$6

$10,000

+

$4,000

$3,500

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

1. The choice of system depends on types of products manufactured and how orders are filled (special or

2. Quantity can be easily determined by review of account balance. This facilitates the prompt and efficient

ordering of raw materials to maintain a proper level of finished goods.

Ethical Dilemma:

Financial Statement Analysis:

Teamwork:

Internet Connection:

Virginia overstating the ending inventory has violated business ethics by not recording correct information.

The three processes to create cement lends it to process costing. Each activity is dependent on the previous

activity before it can start its assigned task. Job costing could be used if the process started with a customer order

and only the amount ordered by the customer was produced in a batch.

Part A True-False

1. FALSE 9. TRUE

3. TRUE 11. TRUE

5. TRUE 13. FALSE

7. TRUE 15. TRUE

Part B Completion

1. job order cost

3. service

5. producing (or production)

7. process cost

Part C Exercises

1. Transferred to next department

(5,000 × 100%) = 5,000

2. Transferred to next department

(4,500 × 100%) = 4,500

3. Transferred to next department

(900 × 100%) = 900

SOLUTIONS TO PRACTICE TEST