• The company was founded to transport kerosene from eastern refineries to Utah by railroad tank and sell it

in bulk, making it affordable for the pioneers.

• Today, the Conoco brand is owned by ConocoPhillips and Conoco Quality PROclean Gasolines are sold at

more than 3,100 retail fuel sites in the United States.

• The company has 32,500 employees and assets of $173 billion.

• Top competitors are BP, Exxon, Mobil, and Royal Dutch/Shell.

• This system is usually appropriate in situations in which there are continuous operations on standard types

of products.

1. Products are not made in batches or special orders.

3. Beginning work in process inventory and costs added during the current period.

4. Multiply units in ending work in process inventory by stage of completion for each cost element to

6. Yes. All cost data is posted to the departmental Work in Process accounts.

8. If products are not the same, the average cost calculation will be meaningless.

10. Each element of cost in beginning inventory is added to amount of that element incurred during month.

11. Number of units of product transferred out of department is multiplied by 100 percent to determine number

Note to the instructor : These questions are designed to check students’ understanding of new terms, concepts, and

procedures presented in the chapter.

Discussion Questions

CHAPTER 28

PROCESS COST ACCOUNTING

Chapter Opener: Thinking Critically

Students’ responses will vary. As ConocoPhillips products move through different refineries, production costs are

most likely classified and tracked within each refining facility. For example, labor, materials, and overhead costs

for gallons of oil in production process for the Louisiana facility might be recorded separately from accounting

entries recorded for Venezuela operations.

Fast Facts

Managerial Implications: Thinking Critically

EXERCISE 28.1

Equivalent units of production for prior department costs

EXERCISE 28.2

Equivalent units of production for materials:

EXERCISE 28.3

Equivalent units of production for labor and overhead

EXERCISE 28.4

1. Cost per equivalent unit for materials:

Transferred out to next department (6,000 × 100%) = 6,000

3. Cost of material in ending work in process = 2,000 × $3 = $6,000

EXERCISE 28.5

1. Equivalent units for materials

Materials

2. Cost per unit for material

Material costs ÷ Materials equivalent units = ($6,000 + $25,900) ÷ 3,000

=

$10.63

EXERCISE 28.6

1. Equivalent units for overhead

2. Cost per unit for overhead

Overhead costs equivalent units = ($3,000 + $15,000) ÷ 2,900 = $6.21

EXERCISE 28.7

PAGE

POST.

REF.

1 2013 1

2 Sept. 30 Work in Process Inventory—Fab Dept. 4100000 2

3 Work in Process Inventory—Finishing Dept. 600000 3

4 Raw Materials Inventory 4700000 4

5 5

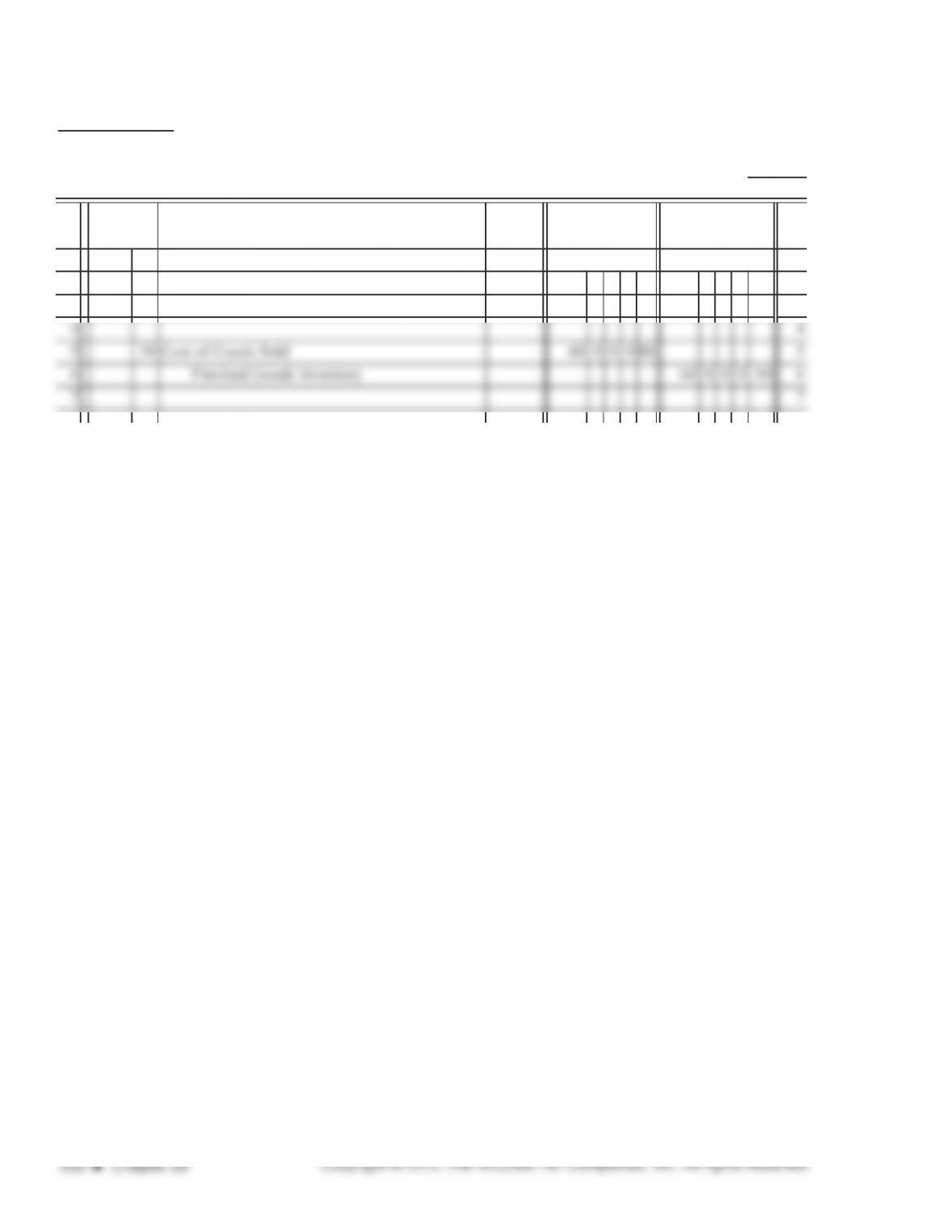

EXERCISE 28.8

PAGE

POST.

REF.

1 2013 1

2 Sept. 30 Work in Process—Finishing Department 5900000 2

3 Work in Process Inventory—Fab Dept. 5900000 3

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

EXERCISE 28.9

PAGE

POST.

REF.

1 2013 1

2 Sept. 30 Accounts Receivable 100 0 0 0 00 2

3 Sales 100 0 0 0 00 3

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 28.1A

Molding Department

Materials: Units transferred to assembly department 2 9 0 0

Work in process (100 units × 100%) 1 0 0

Assembly Department

Materials: Units transferred to completion department 2600

Work in process (300 units × 80%) 2 4 0

Equivalent production for materials in assembly department 2840

Labor and Overhead: Units transferred to completion department 2600

Work in process (300 units × 80%) 2 4 0

Equivalent production for labor and overhead in assembly department 2840

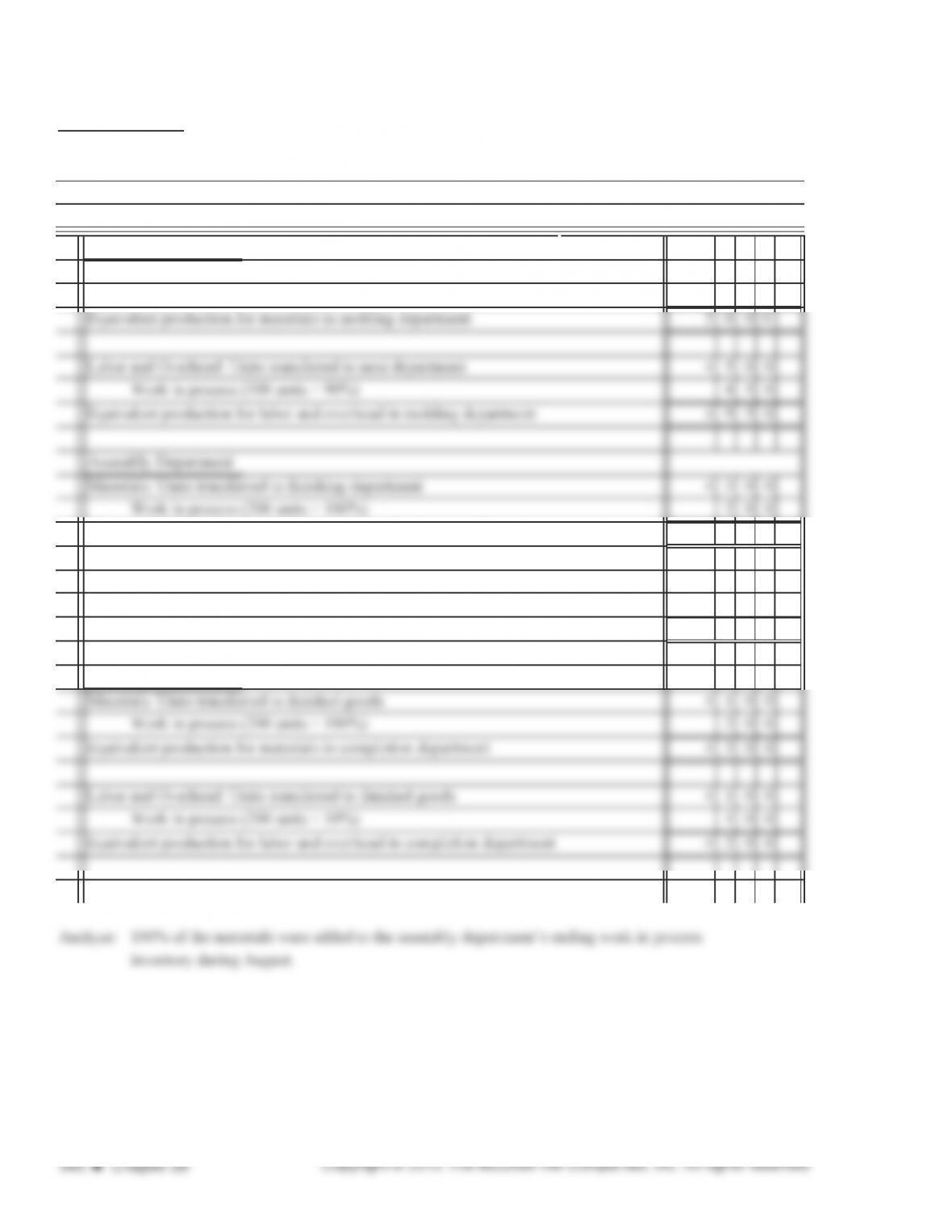

Completion Department

GoingGreen, Inc.

Equivalent Production Computations

Month Ended July 31, 2013

PROBLEM 28.2A

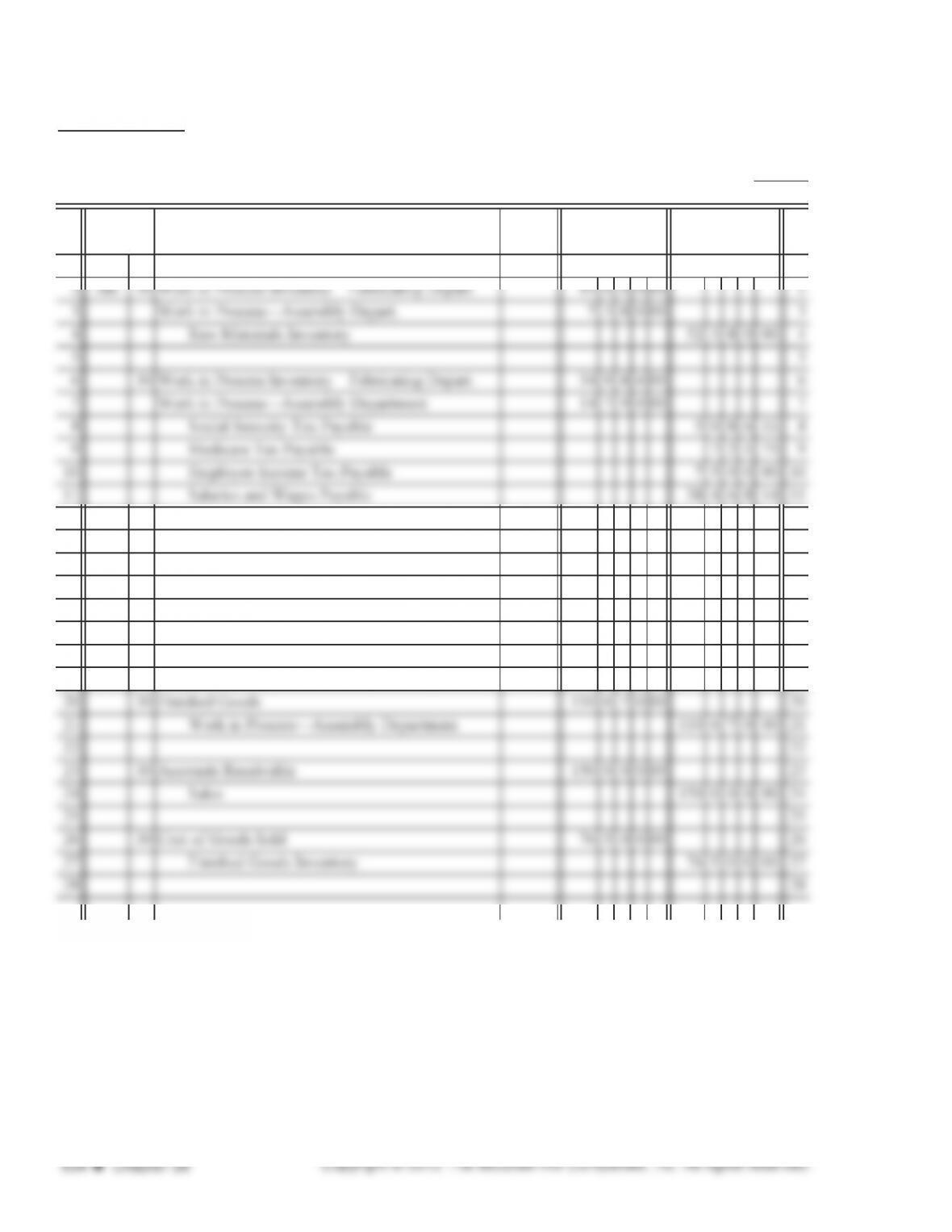

P

AGE

POST.

REF.

1 2013 1

12 12

13 30 Work in Process Inventory—Fabricating Depart. 16 5 1 3 00 13

14 Work in Process—Assembly Department 7 8 3 0 00 14

15 Manufacturing Overhead 24 3 4 3 00 15

16 16

17 30 Work in Process—Assembly Department 87 7 9 5 00 17

18 Work in Process Inventory—Fabricating Dept. 87 7 9 5 00 18

19 19

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 28.2A (continued)

Fabricating Department

Materials: Units transferred out to next department: 100% × 4,500 units 4 5 0 0

Work in process: 100% × 500 units 5 0 0

Equivalent units of production for materials 5000

Labor and manufacturing overhead

Labor and manufacturing overhead

Units transferred out to finished goods: 100% × 4,200 units 4200

Work in process: 50% × 300 units 1 5 0

Equivalent units of production for labor and overhead 4350

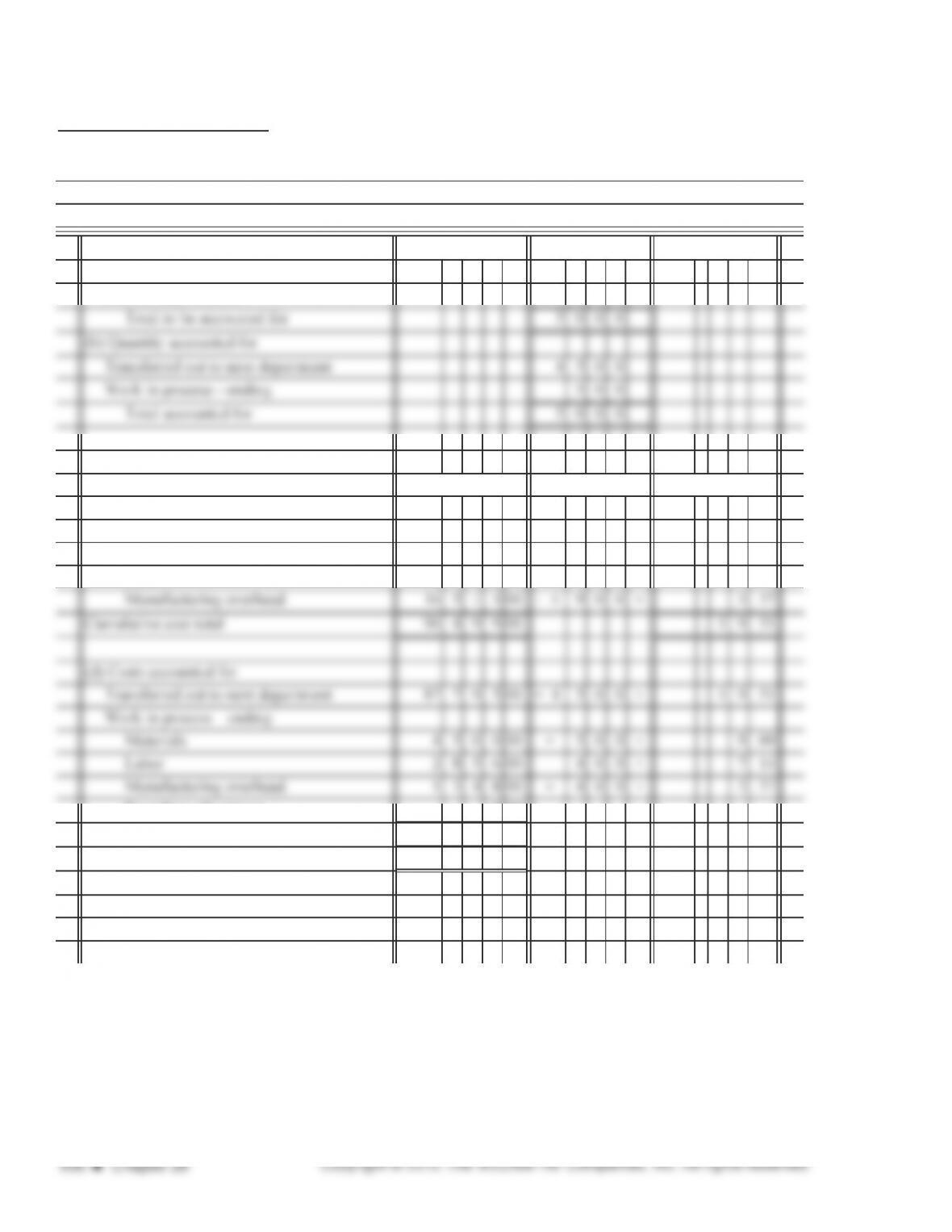

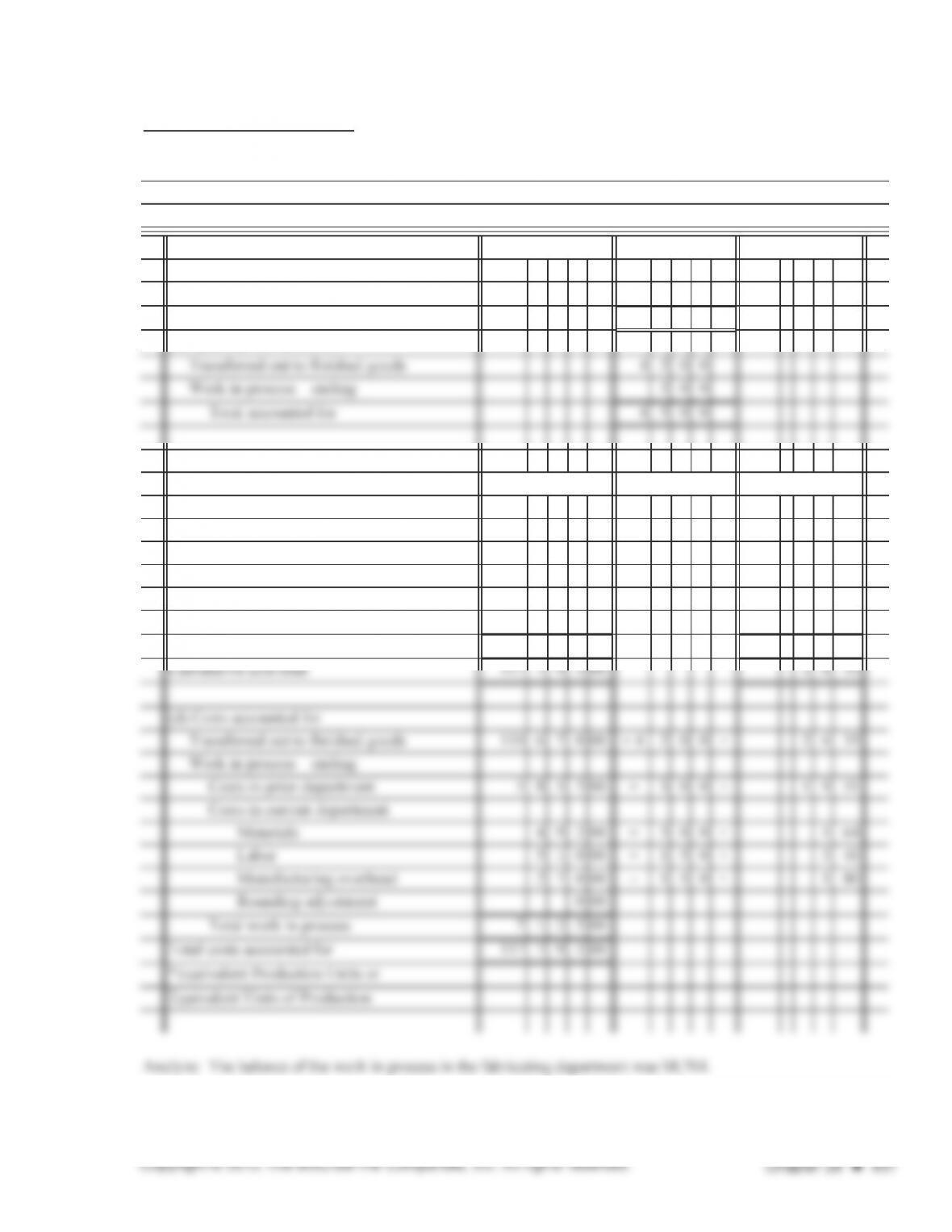

Rahc Games, Inc.

Computation of Equivalent Unit Production

Month Ended June 30, 2013

PROBLEM 28.2A (continued)

QUANTITY SCHEDULE

(a) Quantity to be accounted for

Started in production 5000

COST SCHEDULE

(c) Costs to be accounted for

Costs in current department

Materials 45 0 0 0 00 ÷ 5 0 0 0 = 9 00

Labor 34 9 8 6 00 ÷ 4 9 0 0 = 7 14

Rounding adjustment 0 00

Total work in process—ending 870400

Total costs accounted for 96 4 9 9 00

*Equivalent Production Units or

Equivalent Units of Production

TOTAL COST E.P. UNITS* UNIT COST

Rahc Games, Inc.

Cost of Production Report—Fabricating Department

Month Ended June 30, 2013

UNITS

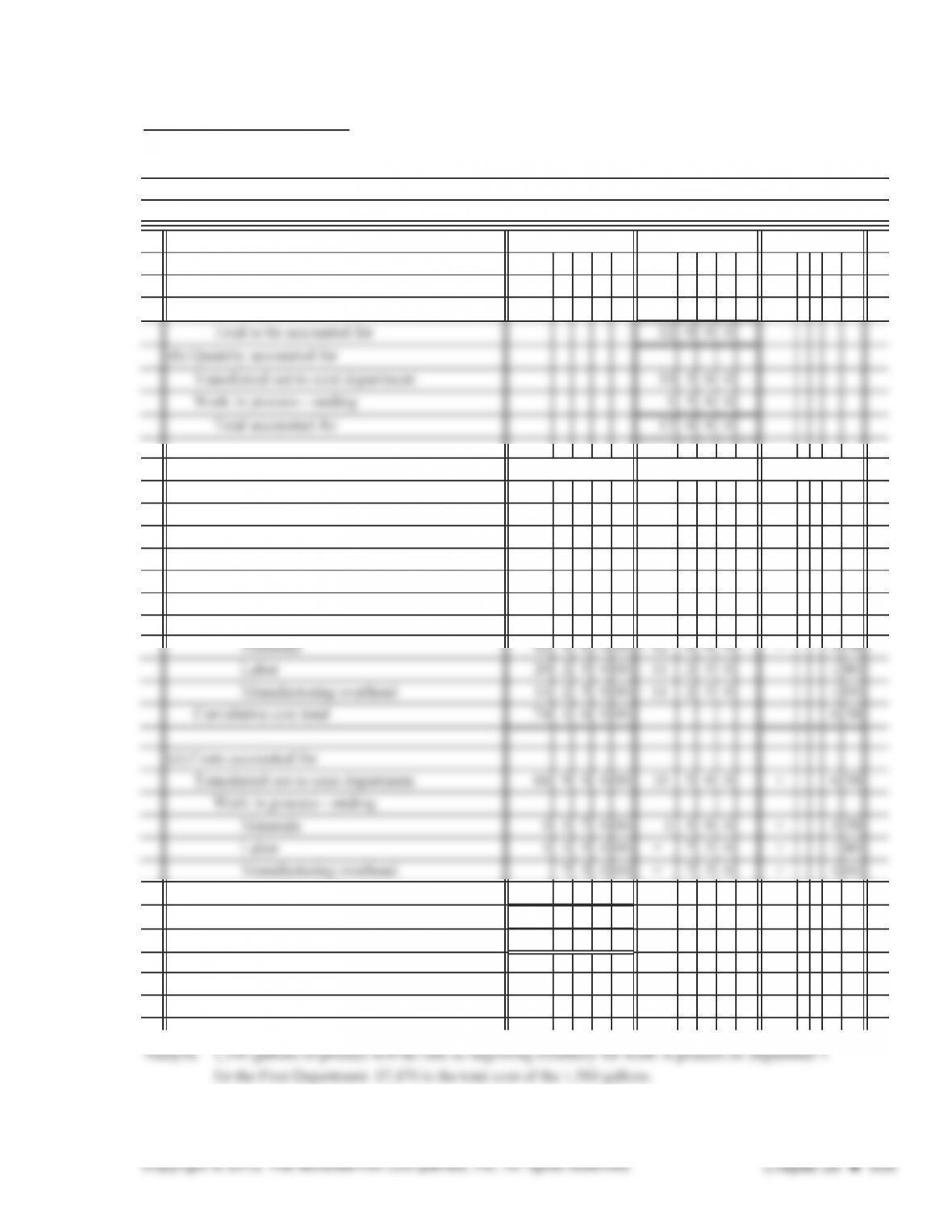

PROBLEM 28.2A (continued)

QUANTITY SCHEDULE

(a) Quantity to be accounted for

Transferred in from prior department 4500

Total to be accounted for 4500

(b) Quantity accounted for

COST SCHEDULE

(c) Costs to be accounted for

Costs in prior department 87 7 9 5 00 = 4 5 0 0 1 9 51

Costs in current department

Materials 738000÷ 4 500= 164

Labor 14 7 9 0 00 ÷ 4 3 5 0 = 3 40

Manufacturing overhead 783000÷ 4 350= 180

Total current department costs 30 0 0 0 00 6 84

Rahc Games, Inc.

Cost of Production Report—Assembly Department

Month Ended June 30, 2013

UNITS

TOTAL COST E.P. UNITS* UNIT COST

PROBLEM 28.3A

First Department

Materials: Units transferred out to next department: 100% × 10,500 units 10 5 0 0

Work in process: 100% × 1,500 units 1 5 0 0

Equivalent Unit Production Computations

Month Ended August 31, 2013

Jasper Corporation

PROBLEM 28.3A (continued)

QUANTITY SCHEDULE

(a) Quantity to be accounted for

Work in process—beginning 1000

Started in production 11000

COST SCHEDULE

(c) Costs to be accounted for

Costs in current department

Work in process—beginning

Materials 796000

Labor 530000

Overhead 275000

Rounding adjustment 0 00

Total work in process—ending 747000

Total costs accounted for 7446000

*Equivalent Production Units or

Equivalent Units of Production

Jasper Corporation

TOTAL COST E.P. UNITS* UNIT COST

Cost of Production Report

Month Ended August 31, 2013

UNITS

PROBLEM 28.1B

Molding Department

Materials: Units transferred to next department 4 5 0 0

Work in process (500 units × 100%) 5 0 0

Equivalent production for materials in assembly department 4500

Labor and Overhead: Units transferred to finishing department 4300

Work in process (200 units × 80%) 1 6 0

Equivalent production for labor and overhead in assembly department 4460

Finishing Department

Month Ended August 31, 2013

Clair Company

Equivalent Production Computations