Student Name:

Class:

2,900

100

3,000 <–Correct!

2,900

90

2,990 <–Correct!

2,600

240

2,840 <–Correct!

2,600

240

2,840 <–Correct!

2,200

2,560 <–Correct!

2,560 <–Correct!

Equivalent production for labor and overhead in completion department

Work in process

Labor and Overhead: Units transferred to finished goods

Equivalent production for materials in completion department

Work in process

Equivalent production for materials in molding department

Work in process

Equivalent production for labor and overhead in assembly department

Labor and Overhead: Units transferred to assembly department

Instructor

Work in process

Labor and Overhead: Units transferred to completion department

Materials: Units transferred to assembly department

Equivalent production for materials in assembly department

Work in process

Materials: Units transferred to completion department

Equivalent production for labor and overhead in molding department

Assembly Department

Work in process

Problem 28.01A

McGraw-Hill/Irwin

Molding Department

Month Ended December 31, 2013

Equivalent Production Computations

GOING GREEN INC.

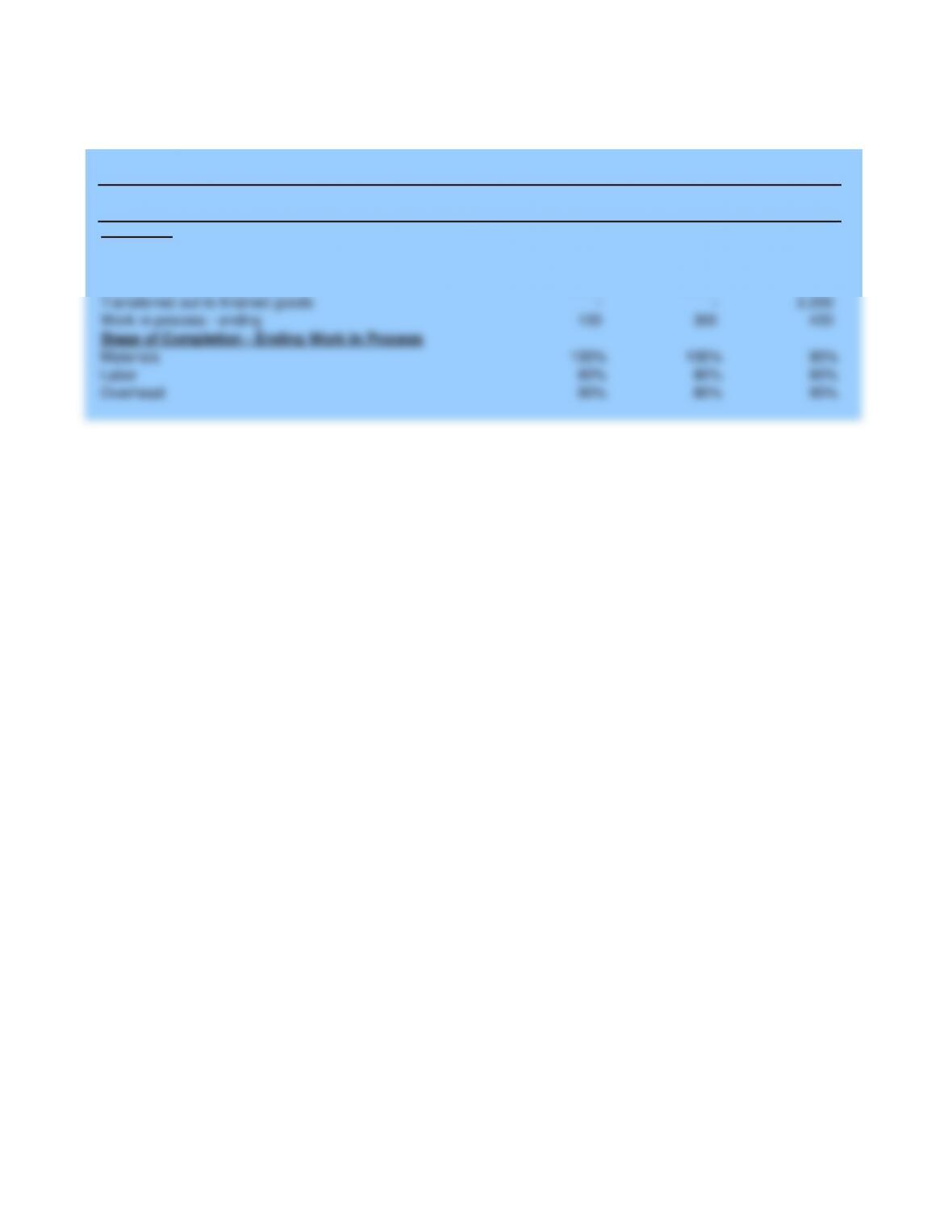

Materials: Units transferred to finished goods

Completion Department

Molding Assembly Completion

Department Department Department

3,000 – –

– 2,900 2,600

2,900 2,600 –

– – 2,200

100 300 400

100% 100% 90%

90% 80% 90%

90% 80% 90%

Work in process – ending

Transferred out to finished goods

Transferred out to next department

Overhead

Labor

Materials

Stage of Completion – Ending Work in Process

Transferred in from prior department

Started in production – current month

Quantities

Given Data P28.01A

Monthly Production Report for December, 2013

GOING GREEN INC.

Student Name:

Class:

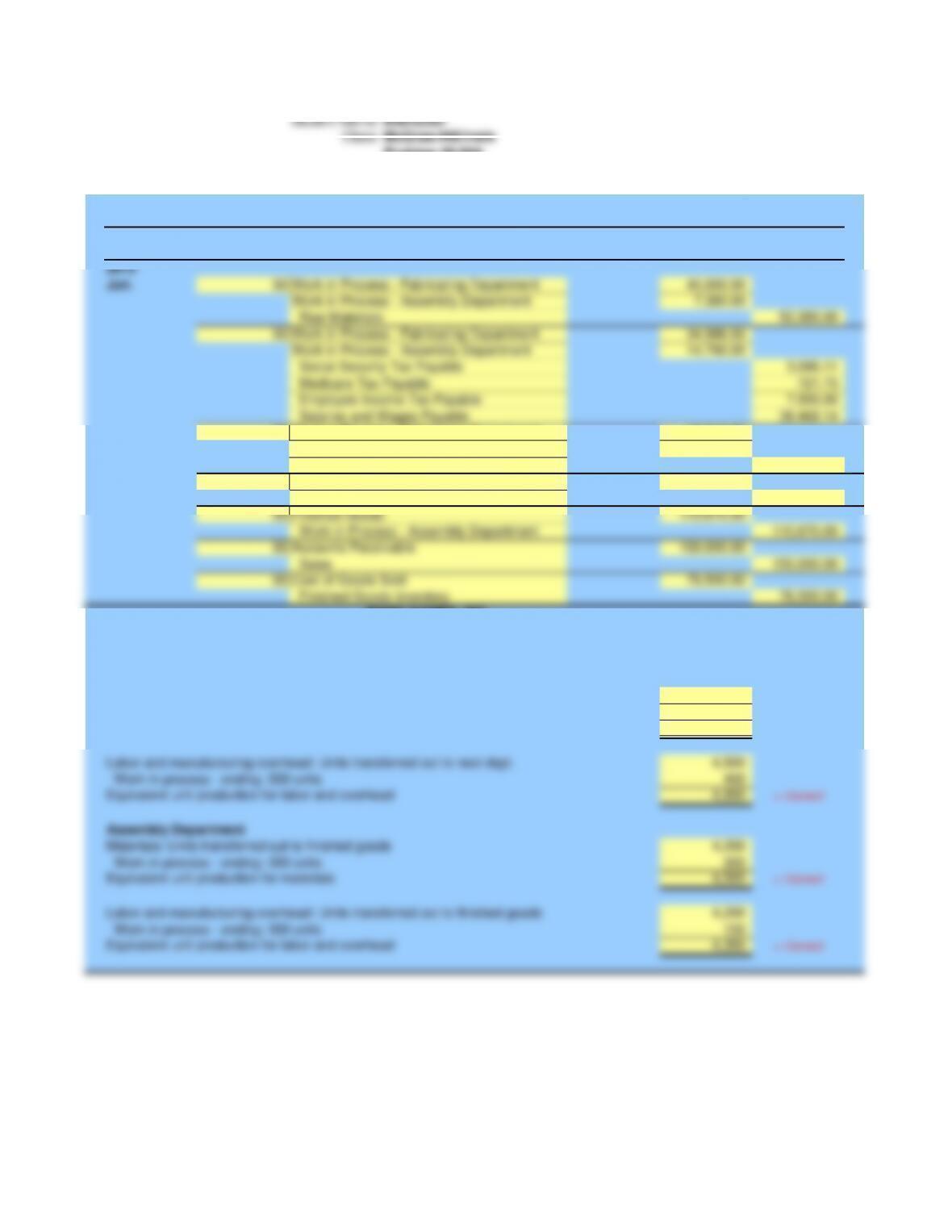

Post

Date Description Ref Debit Credit

2013

Jun. 30 45,000.00

7,380.00

52,380.00

30 34,986.00

14,790.00

3,086.11

721.75

7,500.00

38,468.14

30 16,513.00

7,830.00

24,343.00

30 87,795.00

87,795.00

30 110,670.00

110,670.00

30 150,000.00

150,000.00

30 76,500.00

76,500.00

4,500

500

5,000 <–Correct!

4,500

400

4,900 <–Correct!

4,200

300

4,500 <–Correct!

4,200

150

4,350 <–Correct!

Labor and manufacturing overhead: Units transferred out to next dept.

Work in process – ending: 500 units

Fabricating Department

Materials: Units transferred out to next department

RAHC GAMES, INC.

Manufacturing Overhead

Work in Process – Assembly Department

Equivalent unit production for materials

Labor and manufacturing overhead: Units transferred out to finished goods

Work in process – ending: 300 units

Equivalent unit production for labor and overhead

Equivalent unit production for labor and overhead

Assembly Department

Materials: Units transferred out to finished goods

Equivalent unit production for materials

RAHC GAMES, INC.

Sales

Work in Process – Assembly Department

Salaries and Wages Payable

Employee Income Tax Payable

Medicare Tax Payable

Work in Process – Fabricating Department

Raw Materials

Work in Process – Fabricating Department

Social Security Tax Payable

Work in process – ending: 300 units

Work in process – ending: 500 units

Work in Process – Assembly Department

Work in Process – Assembly Department

Month Ended June 30, 2013

Computation of Equivalent Unit Production

Finished Goods Inventory

Cost of Goods Sold

Work in Process – Fabricating Department

Accounts Receivable

Work in Process – Assembly Department

GENERAL JOURNAL

Finished Goods

Work in Process – Fabricating Department

Instructor

McGraw-Hill/Irwin

Problem 28.02A

UNITS

5,000

5,000

Correct!

4,500

500

5,000

Correct!

TOTAL COST E.P. UNITS UNIT COST

45,000 5,000 9.00

34,986 4,900 7.14

16,513 4,900 3.37

96,499 19.51

Correct!

87,795 4,500 19.51

4,500 500 9.00

2,856 400 7.14

1,348 400 3.37

–

8,704

96,499

Correct!

UNITS

4,500

4,500

Correct!

4,200

300

4,500

Correct!

TOTAL COST E.P. UNITS UNIT COST

87,795 4,500 19.51

7,380 4,500 1.64

14,790 4,350 3.40

7,830 4,350 1.80

30,000 6.84

5,853 300 19.51

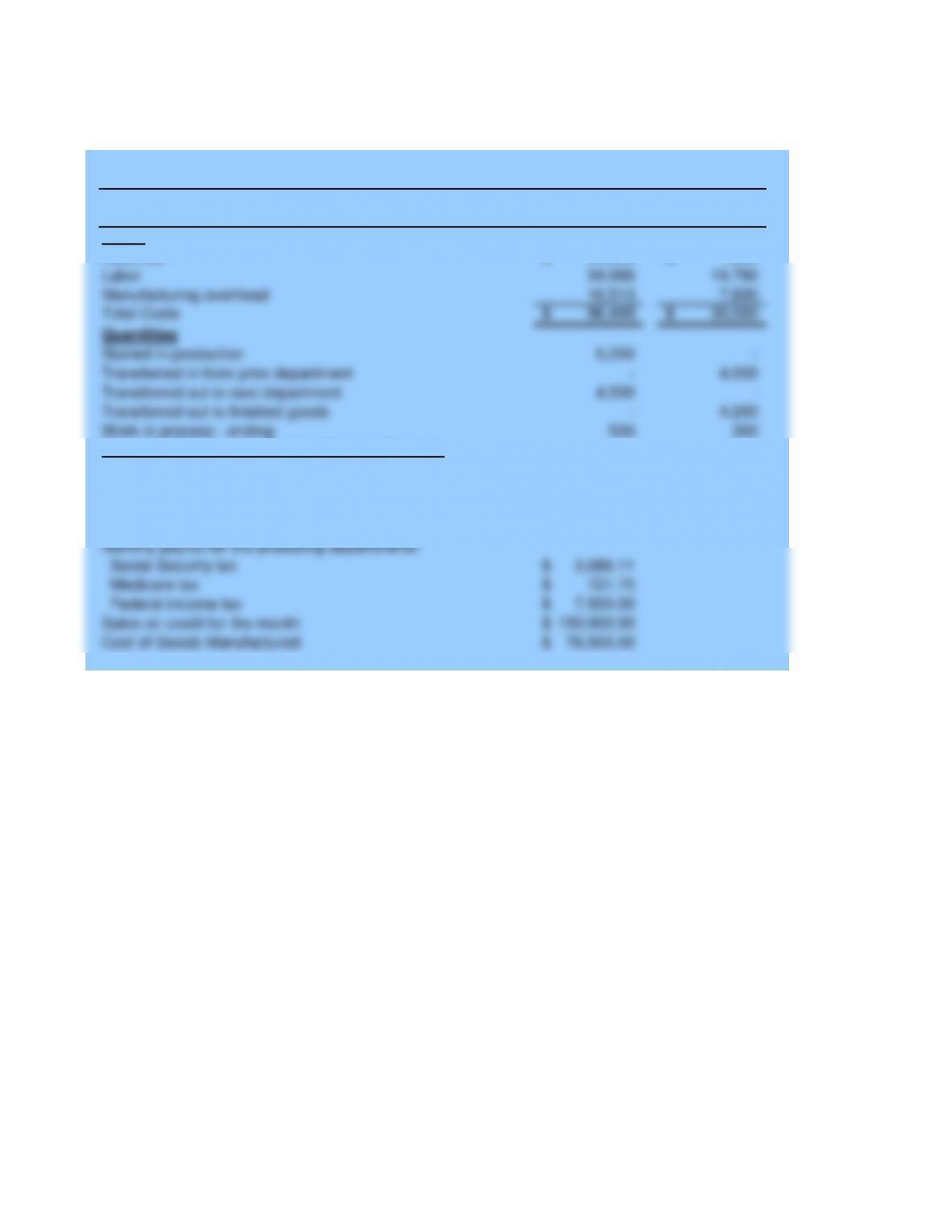

Labor

Work in process – ending

Transferred out to finished goods

Costs accounted for

Cumulative cost total

Total current department costs

Manufacturing Overhead

Materials

Costs in current department

Costs in prior department

Costs in current department

Costs in prior department

Costs in current department

Costs to be accounted for

COST SCHEDULE

Month Ended June 30, 2013

Total accounted for

Work in process – ending

Cost of Production Report – Fabricating Department

RAHC GAMES, INC.

RAHC GAMES, INC.

Cost of Production Report – Assembly Department

Month Ended June 30, 2010

Total accounted for

Work in process – ending

Transferred out to finished goods

Quantity accounted for

Total to be accounted for

Transferred in from prior department

Work in process – ending

Transferred out to next department

Total costs accounted for

Total work in process – ending

Rounding adjustment

Manufacturing Overhead

Costs accounted for

Total to be accounted for

Started in production

Cumulative cost total

Manufacturing Overhead

Labor

Materials

Labor

Costs to be accounted for

COST SCHEDULE

Quantity to be accounted for

QUANTITY SCHEDULE

Quantity to be accounted for

QUANTITY SCHEDULE

Transferred out to next department

Quantity accounted for

Materials

492 300 1.64

510 150 3.40

270 150 1.80

–

7,125

117,795

Correct!

Total costs accounted for

Total Work in process

Rounding adjustment

Manufacturing Overhead

Labor

Materials

Fabricating Assembly

Department Department

45,000$ 7,380$

34,986 14,790

16,513 7,830

96,499$ 30,000$

5,000 –

– 4,500

4,500 –

– 4,200

500 300

100% 100%

80% 50%

80% 50%

3,086.11$

721.75$

7,500.00$

150,000.00$

76,500.00$

Given Data P28.02A

Cost of Goods Manufactured

Sales on credit for the month

Federal income tax

Medicare tax

Social Security tax

Monthly payroll for the producing departments:

Started in production

Manufacturing Overhead

Labor

Materials

Work in process – ending

RAHC GAMES, INC.

Data for June, 2013

Materials

Costs

Stage of Completion – Ending Work in Process

Quantities

Total Costs

Manufacturing overhead

Labor

Transferred out to finished goods

Transferred out to next department

Transferred in from prior department