• The company is divided into three business segments: Girls, Boys, and Infant/Preschool divisions.

• The company’s first products were picture frames. A side business of dollhouse furniture made from

picture frame scraps led the company into the toy business.

• In 1955, Mattel, Inc. became the first year-round sponsor of a TV show with “The Mickey Mouse Club.”

• Headquartered in El Segundo, California, Mattel produces 800 million toys annually, its products reach

150 countries.

• Using the contribution margin would allow a business to evaluate a manager on performance and costs

that are controllable by the manager.

1. Managerial accounting focuses on profitability issues of a business. Financial accounting focuses on

reporting results of business operations from a historical perspective.

3. Reports financial data by segments/departments to tie managerial responsibility to operational results.

5. To track profitability of each department.

7. Departmental: reports income for each department, summarizes all departments for total business income.

9. Square footage of departments; charge to department where item located; allocated on basis of net sales.

These questions are designed to check students’ understanding of new terms, concepts, and procedures presented

in the chapter.

Discussion Questions

CHAPTER 25

DEPARTMENTALIZED PROFIT AND COST CENTERS

Chapter Opener: Thinking Critically

Answers will vary. Mattel, Inc. may have measured the profitability of each business line individually, assessing

the contribution made by each to the overall profits of the company. Company managers may have evaluated

how new business lines complement or add value to the core toy business.

Fast Facts

Managerial Implications: Thinking Critically

ALLOCATION

ALLOCATION

PERCENT ALLOCATION

$600,000

$6,000

$594,000

0.5%

$2,970

PERCENT

DEPARTMENT

DEPARTMENT

CREDIT

SALES

BASIS: TOTAL SALES

BASIS: BOOK VALUE

OF INVENTORY AND

EQUIPMENT

TOTAL

INSURANCE

EXPENSE

BASIS: NET

CREDIT SALES

TOTAL OFFICE

EXPENSE

DEPARTMENT PERCENT

CREDIT SALES

RETURNS AND

ALLOWANCES

EXERCISE 25.4

Gross Profit 285500 194 500 48 0000

Direct Expenses 134600 95 400 23 0000

Cazle Company

Income Statement (Partial)

For Year Ended December 31, 2013

KITCHEN

DEPARTMENT

BATH

DEPARTMENT TOTAL

EXERCISE 25.5

Other questions to address could include the following:

1. Would closing Department 1 cause customers of Department 2 to stop buying from the store?

2. Does Department 1 have products that complement Department 2?

3.

EXERCISE 25.6

Net Sales $600,000

EXERCISE 25.7

Management must consider the fact that Department 1 has a positive contribution margin, although it is smaller

than Department 2. Because it has a positive contribution margin, the department is helping to meet the indirect

expenses. If Department 1 is closed, Department 2 would have to pick up the $45,000 of indirect expenses.

Do you have suppliers that provide you with products for both departments? If so, would losing part of their

sales cause your prices to go up?

Department 1 should not be closed. It would reduce net income by 80 percent if it were discontinued. The

PROBLEM 25.1A

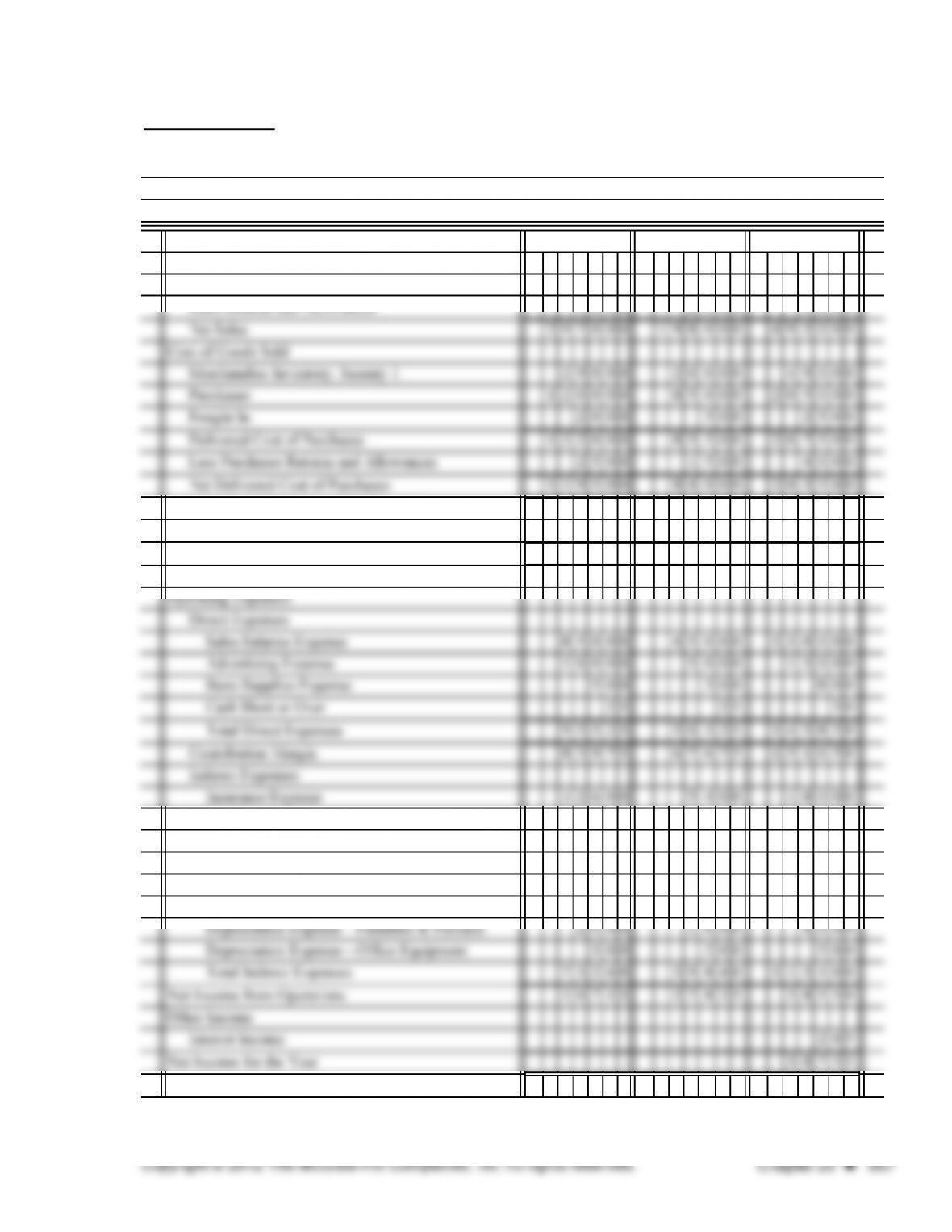

Operating Revenues

Sales 536250 288 750 82 50000

Sales Returns and Allowances 4200 2 800 70000

Net Delivered Cost of Purchases 199000 115 000 31 40000

Total Merchandise Available for Sale 244000 130 000 37 40000

Less Merchandise Inventory, December 31 41000 11 000 5 20000

Cost of Goods Sold 203000 119 000 32 20000

Gross Profit on Sales 329050 166 950 49 60000

Rent Expense 27000 9 000 3 60000

Utilities Expense 4500 1 500 60000

Office Salaries Expense 26000 14 000 4 00000

Other Office Expenses 9 1 0 4 9 0 14000

Uncollectible Accounts Expense 3250 1 750 50000

New2U

Income Statement

Year Ended December 31, 2013

DEPARTMENT A DEPARTMENT B TOTAL

PROBLEM 25.1A (continued)

1. Department A ($130,000 ÷ $200,000) × $15,000 = $9,750

Department B (1,500 sq. ft. ÷ 6,000 sq. ft.) × $36,000 = $9,000

3. Department A ($536,250 ÷ $825,000) × $40,000 = $26,000

Department B ($288,750 ÷ $825,000) × $40,000 = $14,000

4. Department A ($532,050 ÷ $818,000) × $5,000 = $3,252

5. Department A ($30,000 ÷ $50,000) × $6,000 = $3,600

Uncollectible Accounts Expense

Depreciation Expense—Furniture and Fixtures

Other Office Expenses

ALLOCATION OF INDIRECT EXPENSES

Insurance Expense

Office Salaries Expense

PROBLEM 25.2A

1.

Sales 126750 75 500 5 0400 252650

Less Sales Returns and Allowances 1 7 5 0 5 0 0 4 0 0 2 6 5 0

Net Sales 125000 75 000 5 0000 250000

Cost of Goods Sold

Indirect Expenses 9 6 0 0 5 4 0 0 5 0 0 0 20000

Net Income (Loss) from Operations 35800 5 300 (7100) 34000

PROBLEM 25.2A (continued)

Net Sales 125000 75 000 5 0000 250000

Percent of Total Net Sales 5 0 3 0 2 0

Times Total Indirect Expenses 20000 20 000 2 0000

3.

departments.

The Yard Shop

Income Statement

PLANTS CHEMICALS TOOLS TOTAL

Year Ended December 31, 2013

PLANTS CHEMICALS TOOLS TOTAL

The effect on total sales if the decision is made to close the Tools Department and how that would impact the sales

PROBLEM 25.1B

Operating Revenues

Sales 300000 200 000 500000

Sales Returns and Allowances 3 0 0 0 2 0 0 0 5 0 0 0

Total Merchandise Available for Sale 148500 104 000 252500

Less Merchandise Inventory, Dec. 31 31000 24 000 55000

Cost of Goods Sold 117500 80 000 197500

Gross Profit on Sales 179500 118 000 297500

Rent Expense 21000 9 000 30000

Utilities Expense 4 2 0 0 1 8 0 0 6 0 0 0

Office Salaries Expense 30000 20 000 50000

Other Office Expenses 9 6 0 6 4 0 1 6 0 0

Uncollectible Accounts Expense 1 8 0 0 1 2 0 0 3 0 0 0

Sports Shop, LLC

Income Statement

Year Ended December 31, 2013

EQUIPMENT CLOTHES TOTAL

PROBLEM 25.1B (continued)

1. Equipment ($70,000 ÷ $100,000) × $18,000 = $12,600

2. Equipment (2,800 sq. ft. ÷ 4,000 sq. ft.) × $30,000 = $21,000

3. Equipment ($300,000 ÷ $500,000) × $50,000 = $30,000

Equipment ($300,000 ÷ $500,000) × $1,600 = $960

Equipment ($300,000 ÷ $500,000) × $500 = $300

ALLOCATION OF INDIRECT EXPENSES

Insurance Expense

Rent Expense

ALLOCATION OF INDIRECT EXPENSES

Office Salaries Expense

Other Office Expenses

Depreciation Expense—Office Equipment

PROBLEM 25.2B

1.

Sales 76900 44 250 3 0200 151350

Less Sales Returns and Allowances 9 0 0 2 5 0 2 0 0 1 3 5 0

Net Sales 76000 44 000 3 0000 150000

Cost of Goods Sold

Indirect Expenses 2 3 0 0 1 1 0 0 6 0 0 4 0 0 0

Net Income (Loss) from Operations 28900 (100) 5600 34400

2.

3.

The supplies department shows a net loss of $100, which is a minor loss in the overall scope of the business. Since

The concept of offering all items to customers may cause concern to the owners if the decision is made to close the

It’s All Paper

Income Statement

Year Ended December 31, 2013

PRINTING SUPPLIES CARDS TOTAL

CRITICAL THINKING PROBLEM 25.1

Wood Clothing Paper Close Close

Crafts Items Goods Totals Paper Goods Clothing Items

Sales 75,000 60,000 20,000 155,000 128,000 95,000

Cost of Goods Sold 27,000 39,500 12,000 78,500 63,500 39,000

2.

3. Advise the owner to keep all departments, but try to increase sales in paper goods.

Analyze: Wood

Crafts

Clothing

Items

Paper

Goods

CRITICAL THINKING PROBLEM 25.2

Using the contribution margin of a department would allow management to evaluate a manager on performance

and costs that are controllable by the manager. Another argument for using the contribution margin in evaluating

a department’s performance, is that even if the department were eliminated, the indirect expenses would still have

to be paid or absorbed by the remaining departments. As a result, most management decisions are based on the

contribution margin rather than net income by department. Management generally recognizes that many indirect

expenses are allocated in a rather arbitrary manner and that many are uncontrollable costs.

If the Clothing Items department is closed, the net income of the business will fall from $17,000 to $12,500.

Do not close the Clothing Items department

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

2. Indicates poor cash control procedures; investigate immediately.

4. Past experience; industry practices. Methods should be reasonable and fair.

Ethical Dilemma:

Financial Statement Analysis:

2. The revenue from sale of services was an increase of $500 million or 19% over FY 2008.

Teamwork:

Internet Connection:

Since indirect costs can alter the departmental profit and this profit determines the manager’s bonus, allocating

All production of food products require materials to be requisitioned from inventory and mixed together in a vat

General Motors provides income information by department. The reason General Motors (GMAC) Financial

department is reported separately is that it has a higher net income than its automotive department.

Part A True-False

1. TRUE 11. TRUE

3. TRUE 13. FALSE

5. FALSE 15. FALSE

7. FALSE 17. FALSE

9. TRUE 19. FALSE

Part B Matching

1. c

3. e

SOLUTIONS TO PRACTICE TEST