Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

• Teva Pharmaceutical is among the top 15 pharmaceutical companies in the world and the leader in

generic pharmaceuticals.

• Trend analysis. Analyze net income, cost of goods sold, and gross profit. Compare the percentage

of gross profit to sales for the five-year period.

1. Comparison of each Income Statement item with net sales for the period.

3. Yes. Increasing both figures by 12 percent will cause gross profit to also increase by 12 percent,

the same percentage increase as sales.

5. Total assets (or total equities).

7. Measures profitability of stockholders’ investment in the company.

9. Acid test ratio uses only cash and near cash items as the numerator, whereas current ratio uses all

current assets.

11. Measures effectiveness of the credit and collection function.

These questions are designed to check students’ understanding of new terms, concepts, and procedures

presented in the chapter.

Discussion Questions

CHAPTER 23

FINANCIAL STATEMENT ANALYSIS

Chapter Opener: Thinking Critically

Answers will vary, though should include references to the price to earnings ratio and the current ratio as

key financial ratios that indicate a company’s financial health.

Fast Facts

Managerial Implications: Thinking Critically

EXERCISE 23.1

EXERCISE 23.2

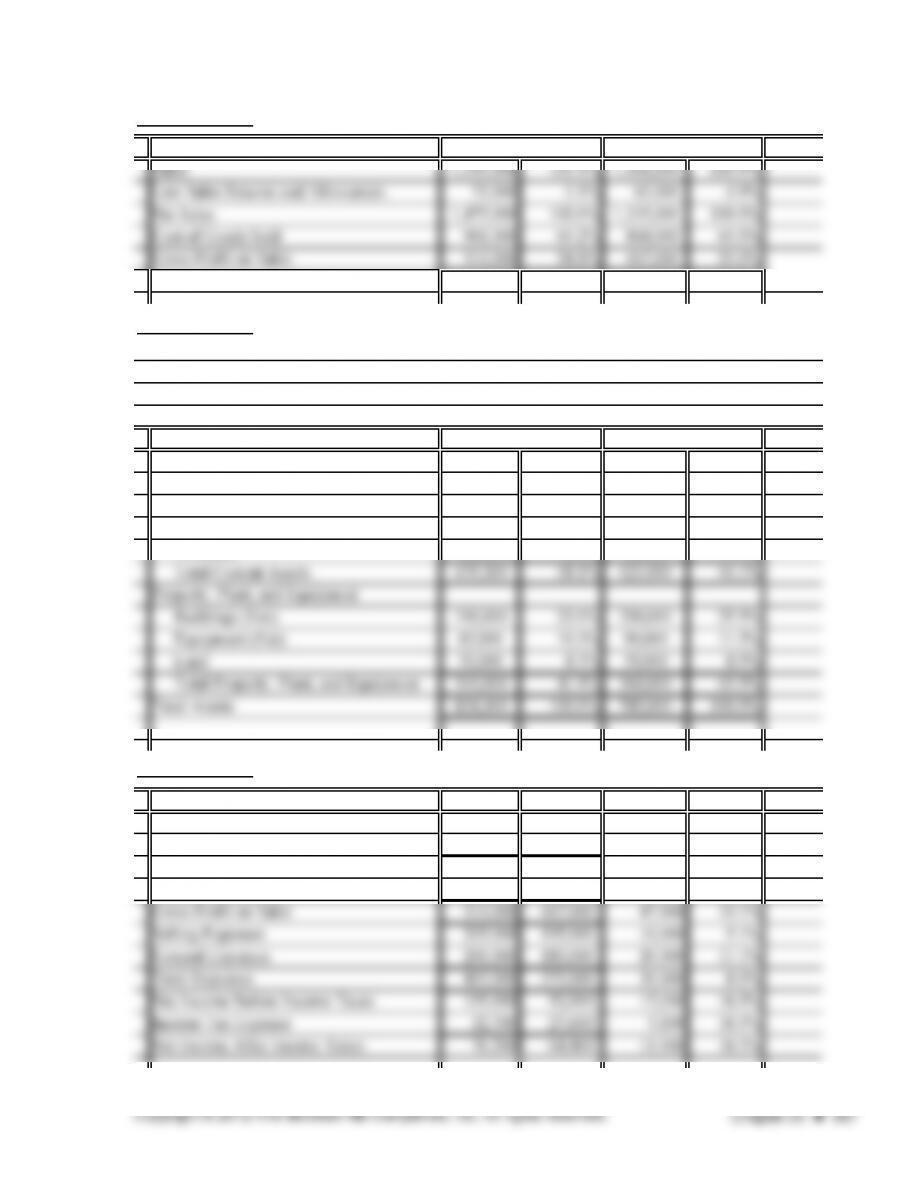

Current Assets

Cash 165,300 20.1% 160,000 20.4%

Accounts Receivable (Net) 194,000 23.5% 175,000 22.3%

Inventory 120,000 14.6% 90,000 11.5%

EXERCISE 23.3

2013 2012 Change Percent

Sales 1,550,000 1,400,000 150,000 10.7%

Less Sales Returns and Allowances 75,000 65,000 10,000 15.4%

Net Sales 1,475,000 1,335,000 140,000 10.5%

Cost of Goods Sold 961,000 868,000 93,000 10.7%

2013 2012

Assets

Orlando, Inc.

Comparative Balance Sheet

2013 2012

December 31, 2013 and 2012

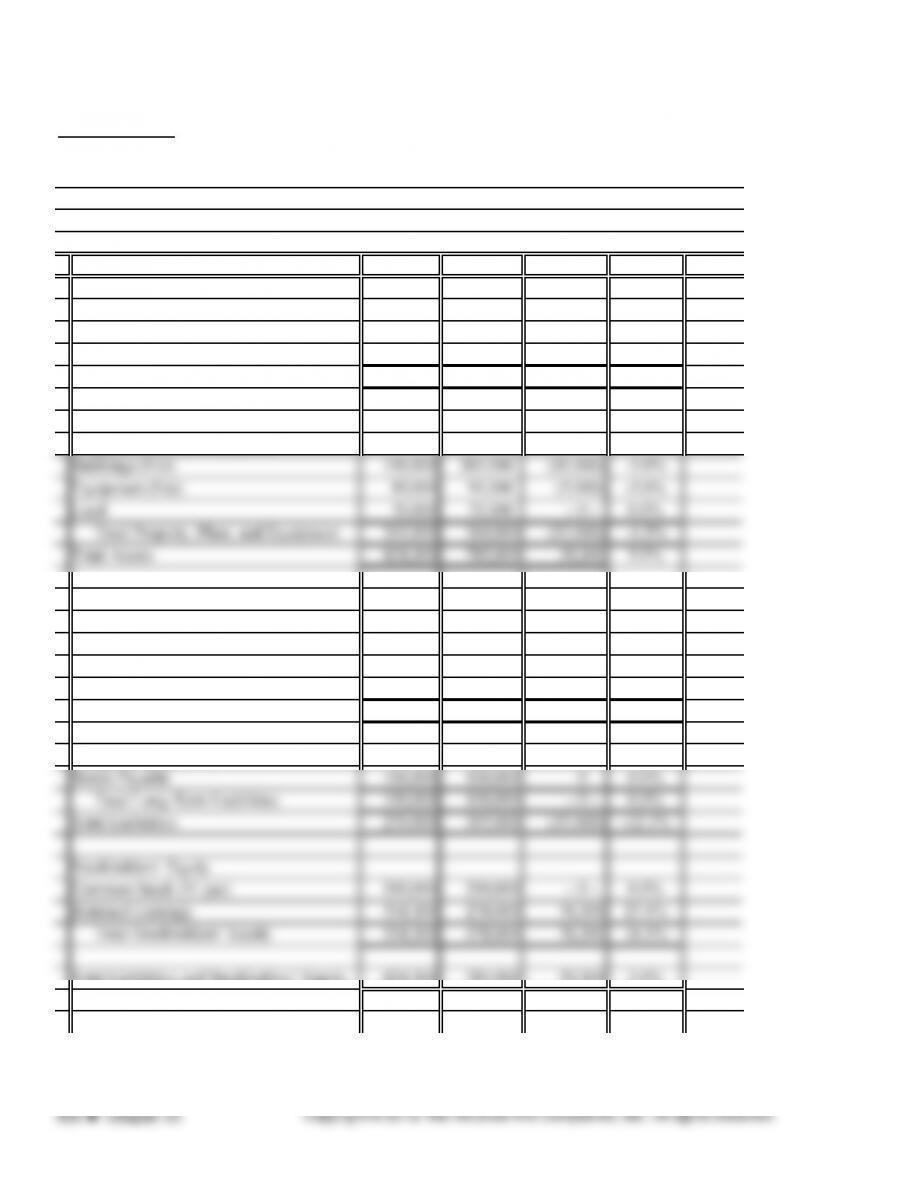

EXERCISE 23.4

2013 2012 Difference Percent

Current Assets 165,300 160,000 5,300 3.3%

Cash 194,000 175,000 19,000 10.9%

Accounts Receivable (Net) 120,000 90,000 30,000 33.3%

Inventory 479,300 425,000 54,300 12.8%

Total Current Assets

Property, Plant, and Equipment

Liabilities

Current Liabilities

Accounts Payable 140,000 165,000 (25,000) -15.2%

Other Current Liabilities 30,000 42,000 (12,000) -28.6%

Total Current Liabilities 170,000 207,000 (37,000) -17.9%

Long-Term Liabilities

Total Liabilities and Stockholders’ Equity 824,300 785,000 39,300 5.0%

Orlando, Inc.

Comparative Balance Sheet

December 31, 2013 and 2012

Assets

Liabilities and Stockholders’ Equity

EXERCISE 23.5

2013 2012

$76,300 $64,400

Net Sales $1,475,000 $1,335,000

5.2% 4.8%

EXERCISE 23.6

Rate of Return on Sales = Net Income After Taxes

=

=

EXERCISE 23.10

EXERCISE 23.11

2013 2012

EXERCISE 23.12

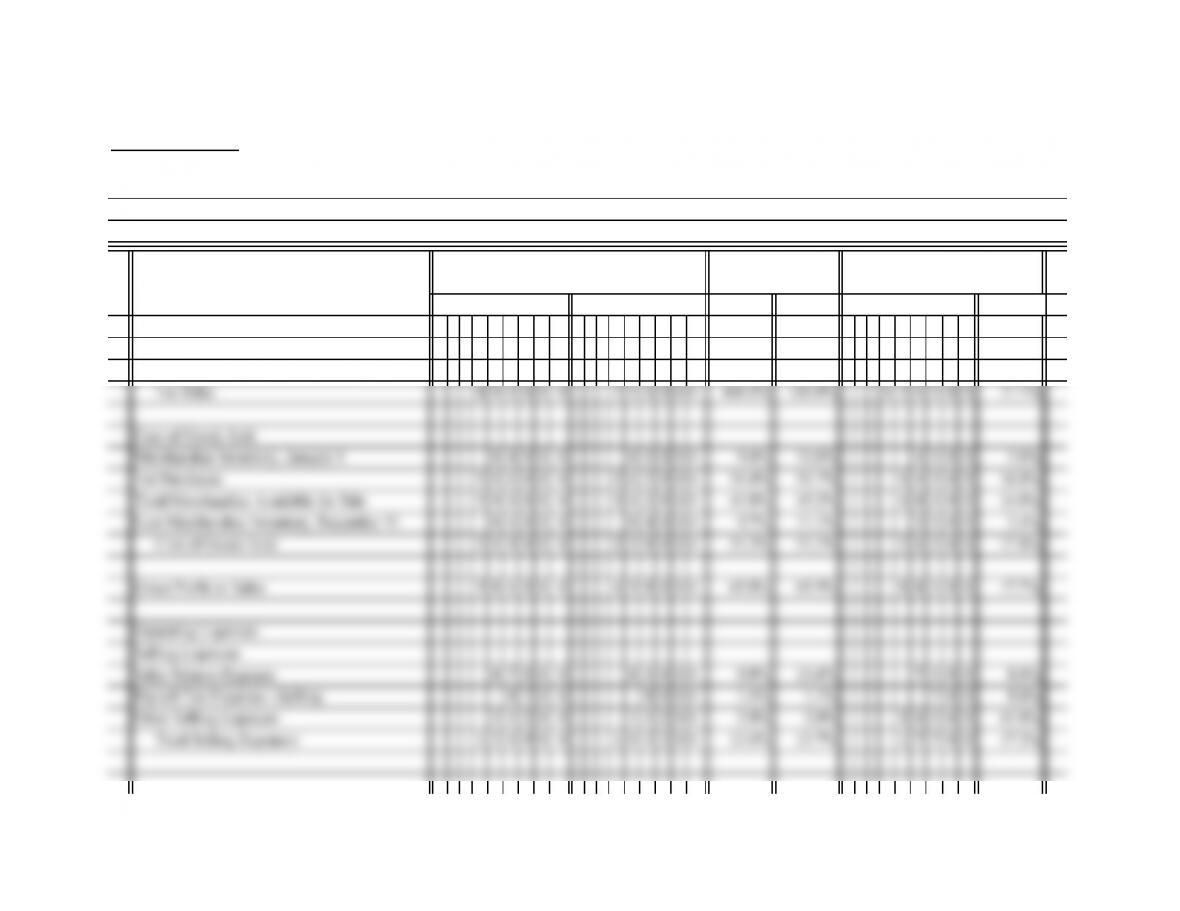

PROBLEM 23.1A

1.

2013 2012 PERCENT

Revenue

Sales 90500 0 765000 101.7% 101.2% 1 4 0 0 0 0 18.3%

Less Sales Returns and Allowances 1500 0 9000 1.7% 1.2% 6 0 0 0 66.7%

The LACAL Company

Comparative Income Statement

For Years Ended December 31, 2013 and 2012

ACCOUNT NAME

AMOUNTS

PERCENT OF NET

SALES INCREASE OR (DECREASE)

2013 2012 AMOUNT

PROBLEM 23.1A (continued)

2013 2012 PERCENT

General and Administrative Expenses

Officers Salaries Expense 13000 0 110000 14.6% 14.6% 2 0 0 0 0 18.2%

Payroll Tax Expense—Administrative 1300 0 11000 1.5% 1.5% 2 0 0 0 18.2%

Depreciation Expense 8 2 5 0 8 2 5 0 0.9% 1.1% −0−0.0%

The LACAL Company

Comparative Income Statement (continued)

For Years Ended December 31, 2013 and 2012

ACCOUNT NAME

AMOUNTS

PERCENT OF NET

SALES INCREASE OR (DECREASE)

2013 2012 AMOUNT

PROBLEM 23.1A (continued)

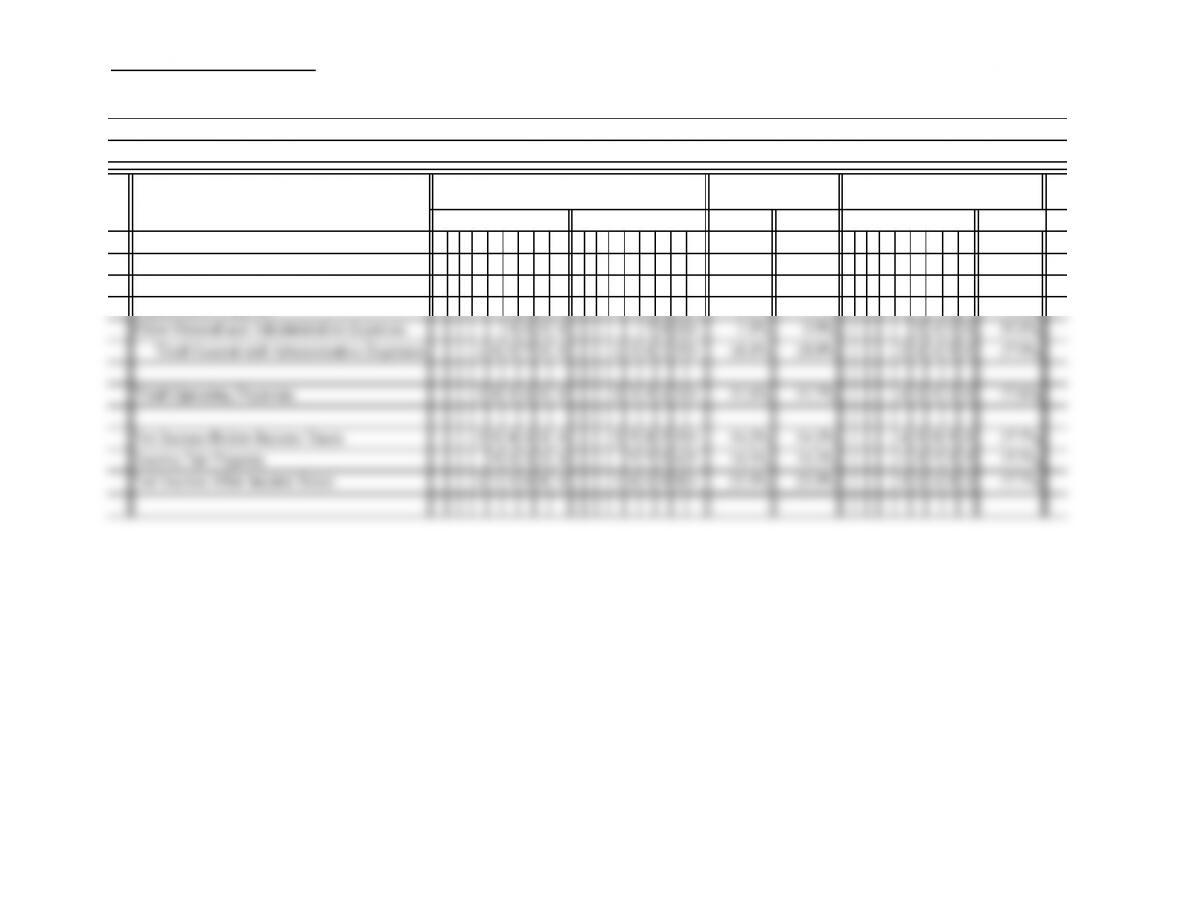

2013 2012 PERCENT

Current Assets

Cash 1 11022 46275 26.0% 13.0% 6 4 7 4 7 139.9%

Accounts Receivable 95000 87500 22.2% 24.6% 7 5 0 0 8.6%

Assets

PERCENT OF

TOTAL ASSETS INCREASE OR (DECREASE)

2013 2012 AMOUNT

THE LACAL COMPANY

Comparative Balance Sheet

December 31, 2013 and 2012

AMOUNTS

PROBLEM 23.1A (continued)

2013 2012 PERCENT

Current Liabilities

Accounts Payable 2700 0 57000 6.3% 16.0% (3 0 0 0 0) (52.6)%

Sales Tax Payable 1 0 0 0 3 0 0 0 0.2% 0.8% (2 0 0 0) (66.7)%

Payroll Taxes Payable 1 1 4 2 1 0 2 5 0.3% 0.3% 1 1 7 11.4%

AMOUNT

Liabilities and Stockholders’ Equity

THE LACAL COMPANY

Comparative Balance Sheet (continued)

December 31, 2013 and 2012

AMOUNTS

PERCENT OF

TOTAL ASSETS INCREASE OR (DECREASE)

2013 2012

PROBLEM 23.2A

PART I

Current assets

Net income after taxes

Net sales

7.

2013 2012

72.6%=

$427,222 $356,025

= 71.3% $258,550$304,400

Return on total

assets

= Net Income before interest and taxes

Total assets

4. Return on sales =

$213,080

$890,000

= 23.9% $180,985 = 23.9%

$756,000

10.0:1

3.4:1

$223,275 =

1. Current ratio = $302,722 =

PROBLEM 23.2A (continued)

PART II

1. The 2012 and 2013 ratios of 73.9% and 59.5% are both much better than average.

3. The company is below the industry average of 2.5 to 1.

4. Inventory turnover for this company is well below the industry average. Management may want to weigh

PROBLEM 23.3A

$82,875 $131,250

$795,000 $650,000

$120,500 $175,000

$350,000 $300,900

2,000 2,000

a.

b.

Number of shares common stock

per share

per share

58.16%

== 34.43%

common stock

Rate of return on net sales = Net income after taxes

Sales

Net income before taxes and interestRate of return on total

assets

=

Total assets

Five Inc. Six Inc.

= 10.42% = 20.19%

PROBLEM 23.3A (continued)

2.

3.

Six Inc. has better rate of return on sales and also a better balance sheet due to the lack of any long-

The long-term debt of Five Inc. could be a negative from an investment point of view. Six Inc. has

more net income on a smaller sales amount.