Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

PROBLEM 21.3B

PAGE

POST.

REF.

1 2013 1

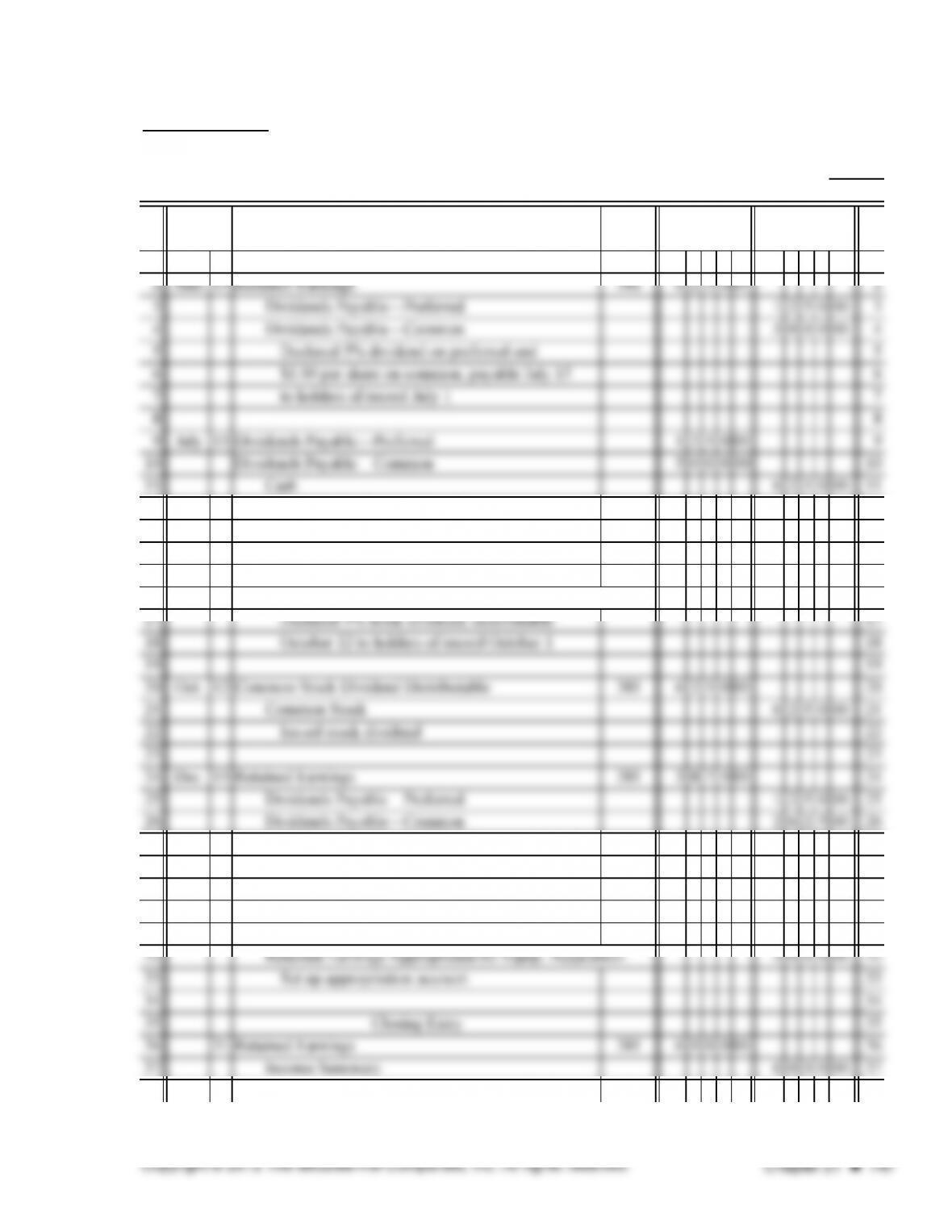

12 Paid dividends on preferred 12

13 13

14 Sept. 15 Retained Earnings 381 750000 14

15 Common Stock Dividend Distributable 625000 15

16 Paid-in Capital in Excess of Stated Value—Common 125000 16

27 Declared 5% dividend on preferred and $0.50 27

28 per share on common, payable Jan. 15 to 28

29 holders of record Dec. 31 29

30 30

31 15 Retained Earnings 381 500000 31

36 31 Retained Earnings 381 600000 36

37 Income Summary 600000 37

GENERAL JOURNAL 6

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 21.3B (continued)

ACCOUNT Retained Earnings ACCOUNT NO.

2013

Jan. 1 Balance ✔43 0 0 0 00

June 15 J6 6 2 5 0 00 36 7 5 0 00

DESCRIPTION

POST.

REF. DEBIT

GENERAL LEDGER

381

CREDIT

BALANCE

DEBIT CREDITDATE

PROBLEM 21.3B (continued)

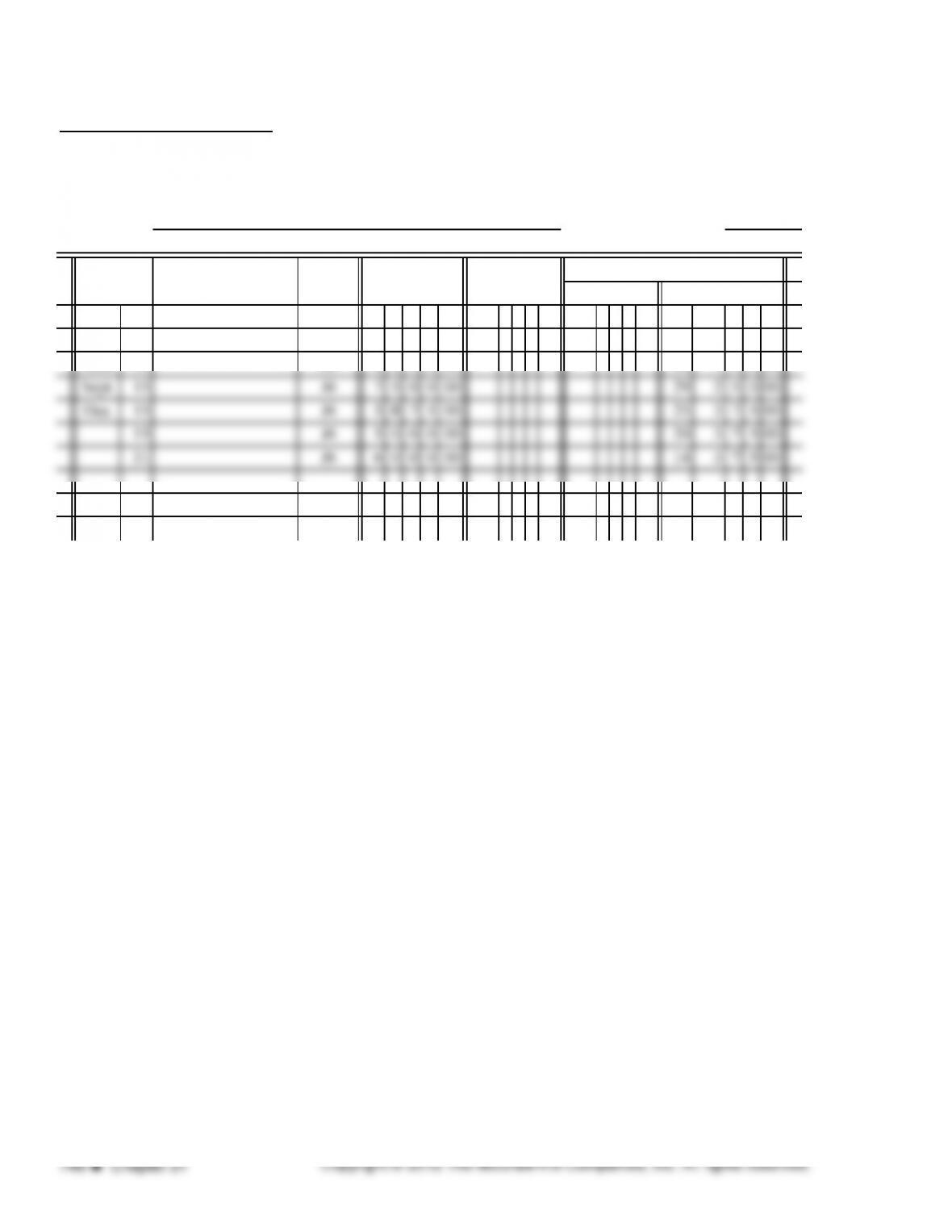

Unappropriated Retained Earnings

Balance, January 1, 2013 4300000

Deductions:

Appropriated Retained Earnings:

Appropriated for Equipment Acquisition:

Balance, January 1, 2013 ─0─

Add Appropriation for the Year 500000

Toy Hut Corporation

Statement of Retained Earnings

December 31, 2013

PROBLEM 21.4B

PAGE

POST.

REF.

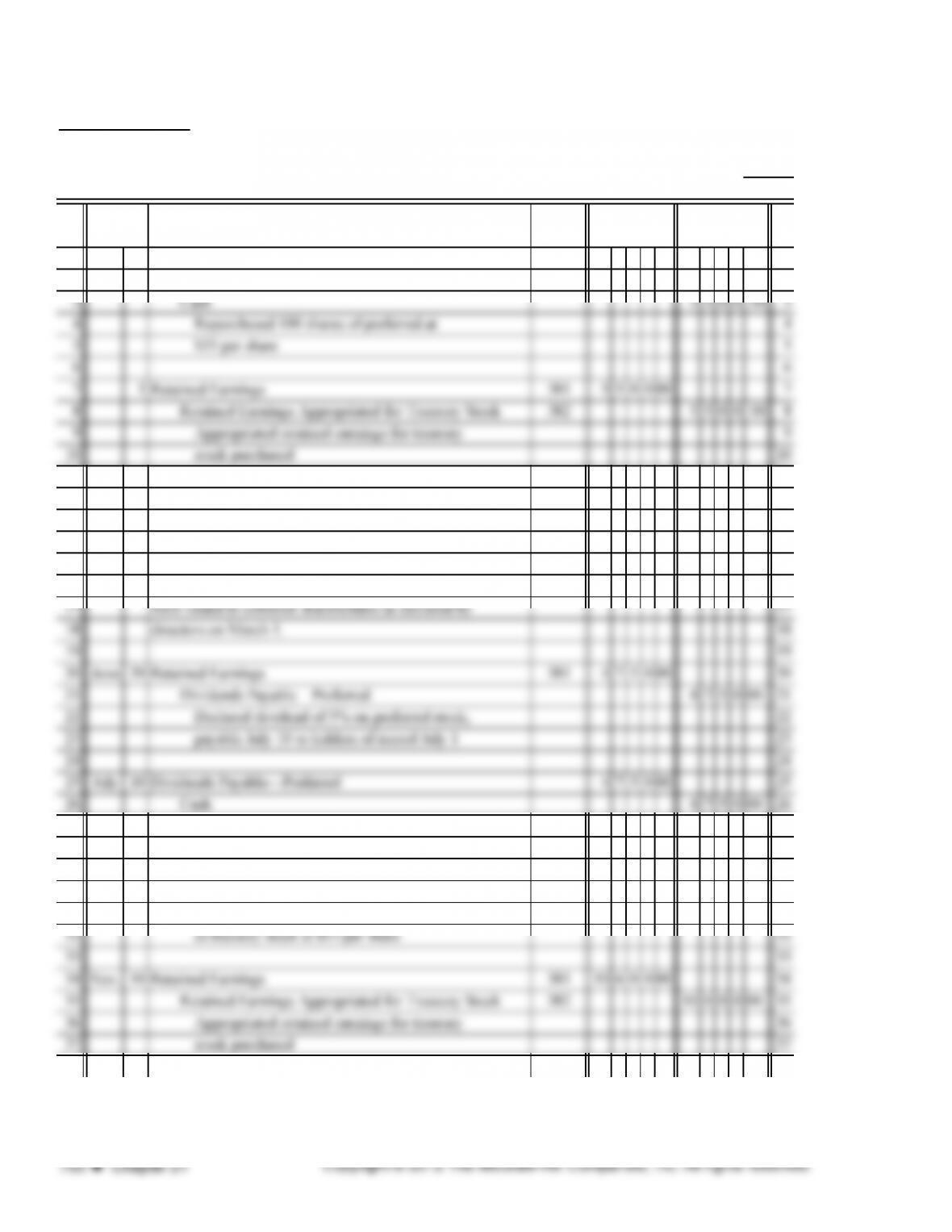

1 2013 1

2 Feb. 1 Treasury Stock—Preferred 372 550000 2

11 11

12 Mar. 1 On this date the board of directors declared a 2-for-1 12

13 stock split and reduced stated value of common to $12.50 13

14 per share. Total outstanding shares will be 7,200 shares. 14

15 15

16 April 1 On this date 3,600 additional shares of common stock 16

27 Payment of dividends on preferred 27

28 28

29 Nov. 10 Treasury Stock—Preferred 372 10 6 0 0 00 29

30 Cash 10 6 0 0 00 30

31 Purchased 200 shares of preferred stock 31

GENERAL JOURNAL 1

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 21.4B (continued)

PAGE

POST.

REF.

1 2013 1

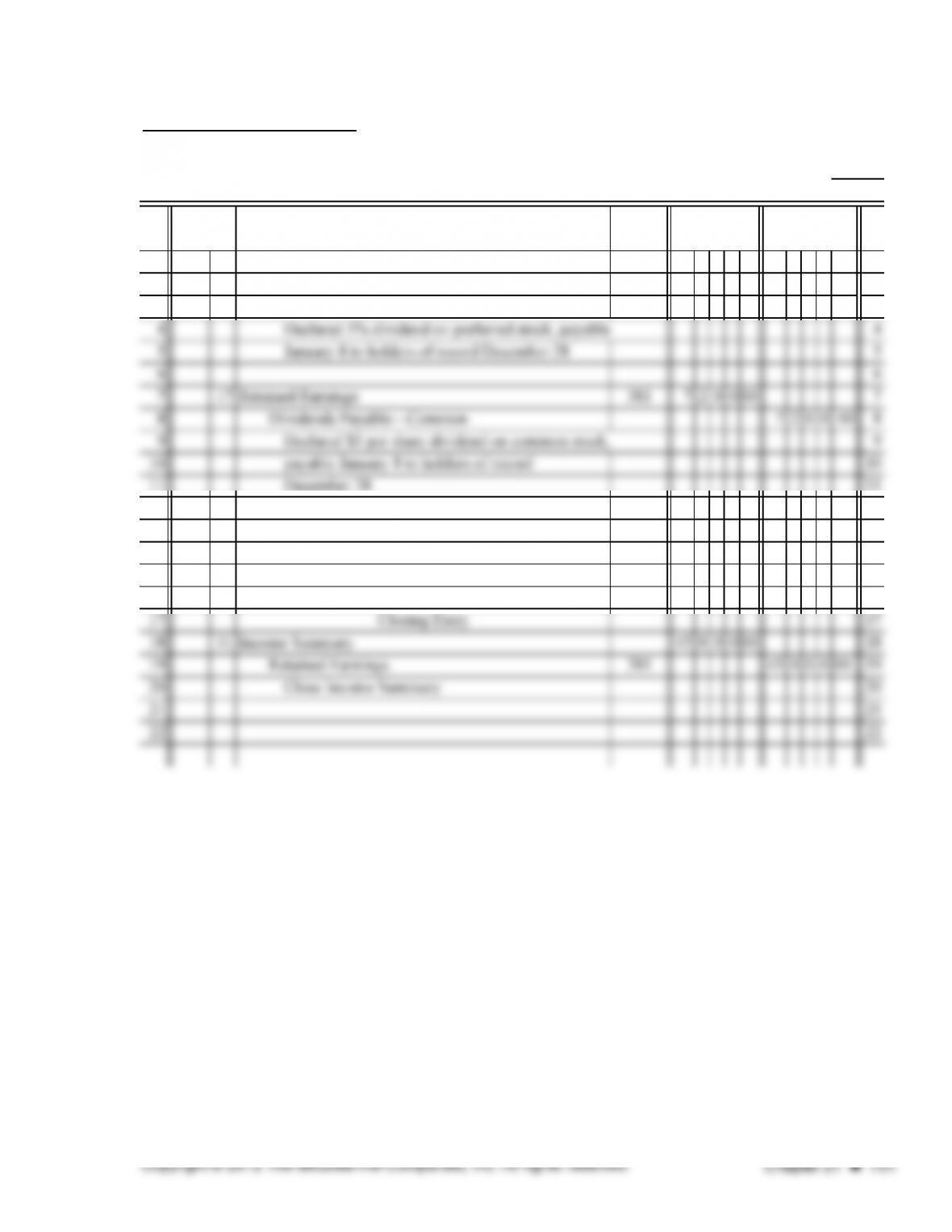

2 Dec. 17 Retained Earnings 381 425000 2

3 Dividends Payable—Preferred 4250 00 3

12 12

13 15 Land 75 0 0 0 00 13

14 Donated Capital 371 75 0 0 0 00 14

15 Donation of land for building site 15

16 16

18 31 Income Summary 45 0 0 0 00 18

19 Retained Earnings 381 45 0 0 0 00 19

20 Close Income Summary 20

21 21

22 22

GENERAL JOURNAL 2

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 21.4B (continued)

ACCOUNT 10% Preferred Stock, $50 Par ACCOUNT NO.

2013

ACCOUNT Paid-in Capital in Excess of Par Value-Preferred ACCOUNT NO.

2013

ACCOUNT Common Stock, No-Par, Stated Value, $25 ACCOUNT NO.

2013

Jan. 1 Balance ✔90 0 0 0 00

ACCOUNT Paid-in Capital in Excess of Stated Value-Common Stock ACCOUNT NO.

2013

315

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

311

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

305

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

GENERAL LEDGER

301

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

PROBLEM 21.4B (continued)

ACCOUNT Donated Capital ACCOUNT NO.

2013

ACCOUNT Treasury Stock—Preferred ACCOUNT NO.

2013

ACCOUNT Retained Earnings ACCOUNT NO.

2013

Jan. 1 Balance ✔165 4 5 0 00

Feb. 1 J1 550000 15995000

ACCOUNT Retained Earnings Appropriated for Treasury Stock ACCOUNT NO.

2013

Feb. 1 J1 550000 550000

371

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

372

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

381

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

382

DATE DESCRIPTION

POST.

REF. DEBIT CREDIT

BALANCE

DEBIT CREDIT

PROBLEM 21.4B (continued)

Stockholders’ Equity

Paid-in Capital

Preferred Stock (10%, $50 par value, 20,000 shares authorized)

Issued 2,000 shares (of which 300 shares are held as treasury stock) 10000000

Paid-in Capital in Excess of Par Value—Preferred 350000 10350000

Common Stock (no-par, $12.50 stated value, 20,000 shares authorized)

Deduct Treasury Stock—Preferred 1610000

Total Stockholders’ Equity 44965000

December 31, 2013

Houston Corporation

Balance Sheet (Partial)

CRITICAL THINKING PROBLEM 21.1

2. 10,000 shares: ($750,000 − $500,000 ) ÷ $25 per share = 10,000 shares

4. 500 shares: ($90,000 − $65,000) ÷ $50 per share = 500 shares

7. $90,000: 30,000 shares × $3 per share = $90,000

CRITICAL THINKING PROBLEM 21.2

1. A board of directors may decide to declare a stock dividend rather than a cash dividend if the corporation is

2. The total book value is the same after the stock dividend as before. The book value per share decreased

from $45 to $37.50. The book value before the stock dividend = Total Stockholders’ Equity ÷ Number of

$37.50 = $540,000).

3. The book value of each share is found by dividing total stockholders’ equity by the number of shares

outstanding. Book value represents the amount of net assets associated with each share of stock. Market

$1.33 = $19,152. Rosa will receive only $48 less in cash dividends as she would have had the stock

dividend not been declared.

5. The reduction in market price does not represent a loss because the total value of the investment remains

the same: Value of Rosa’s shares prior to stock dividend = 12,000 shares × $60 per share = $720,000;

6. If Lowe Tech had maintained the same level of dividends per share ($1.60) while increasing the number of

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

1. A regular corporation. Subchapter S, regular partnership, limited liability partnership, a limited liability

company.

4. Issue a stock split.

Ethical Dilemma:

It is recorded as a credit to the capital account, Donated Capital, and a debit to the asset account, Land.

Part A True-False

2. FALSE 10. TRUE

4. TRUE 12. TRUE

6. FALSE 14. FALSE

8. FALSE

Part B Completion

2. g

4. b

6. a

7. d

Part C Exercises

1. Book value before stock dividend:

2. Entry to record dividend declaration:

2013

SOLUTIONS TO PRACTICE TEST