Chapter Opener: Thinking Critically

Fast Facts

•

•

•

Managerial Implications: Thinking Critically

Discussion Questions

1.

2.

4.

5.

7.

9.

Note to instructor: These questions are designed to check students’ understanding of new terms,

concepts, and procedures presented in the chapter.

Assets = Liabilities + Owner’s Equity

Southwest Airlines opened in 1971 with three planes flying between Houston, Dallas, and San

Antonio. Southwest Airlines currently flies almost 100 million passengers a year to 63 cities all

across the country.

For the fiscal year 2009, the company’s net income was $99 million while its total operating

revenue was $10.4 billion.

Beginning-of-period capital balance, additional investments, net income/loss for period, less

withdrawal ending capital balance

f. assets increase, liabilities increase

CHAPTER 2

ANALYZING BUSINESS TRANSACTIONS

In 2009 Southwest served 63.2 million cans of soda, juices, and water; 14.3 million alcoholic

beverages; 14 million bags of pretzels; 90 million bags of peanuts; 17.7 million Select-A-Snacks;

and 33.5 million other snacks.

Answers will vary. Students should mention total assets and the type of assets, the liabilities the business

would be responsible for, and whether the business is making a profit.

Answers will vary but students should recognize that happy employees are more productive and present

a positive image to the company. Happy employees are also loyal which leads to lower employee

turnover, and lower training and recruiting expenses. Happy employees are much less likely to steal from

the company, and of course, happy employees mean happy customers who become repeat customers.

Firm name, title of statement, date of statement or the period of time covered

b. one asset increase and another decrease; no change in total assets

e. assets decrease, owner’s equity decrease

c. assets decrease, liabilities decrease

d. assets increase, owner’s equity increase

Outflow of money/assets for costs used to produce revenue

a. assets increase, owner’s equity increase

Revenue and expenses; net income or loss

Discussion Questions (continued)

10.

12.

EXERCISE 2.1

EXERCISE 2.2

1. $21,740

EXERCISE 2.3

Assets = Liabilities +

1. I I = Increase D = Decrease

EXERCISE 2.4

=+

1. Cash $12,500

2. Dental Supplies 3,150 = Accounts Payable $21,680 + Donna Wells, Capita

l

$26,520

Owner’s EquityLiabilitiesAssets

Transaction

Increases owner’s equity

Assets, liabilities, and owner’s equity.

Owners’ Equity

I

EXERCISE 2.5

= Liabilities +

Cash +

Accounts

Receivable + Equipment =

Accounts

Payable +

Amos

Roberts

Capital + Revenue – Expenses

1. +$50,000 +$50,000

2. +$17,000 +$17,000

EXERCISE 2.6

Net income of $20,000

Revenue

Repair Fees …………………………………

…

$45,150

Expenses

…

EXERCISE 2.

7

1. Services were performed for cash.

Owner’s EquityAssets

Revenue

Fees Income 7280000

Expenses

Advertising Expense 550000

Salaries Expense 1500000

EXERCISE 2.9

Net loss of $950

Revenue

Service Revenue …………………………………………..

Expenses

Advertising Expense…………… $2,600

EXERCISE 2.10

Alexander Parker, Capital, September 1, 2013 2570000

Net Income for September 5160000

Parker Investment Services

Income Statement

Month Ended September 30, 2013

EXERCISE 2.8

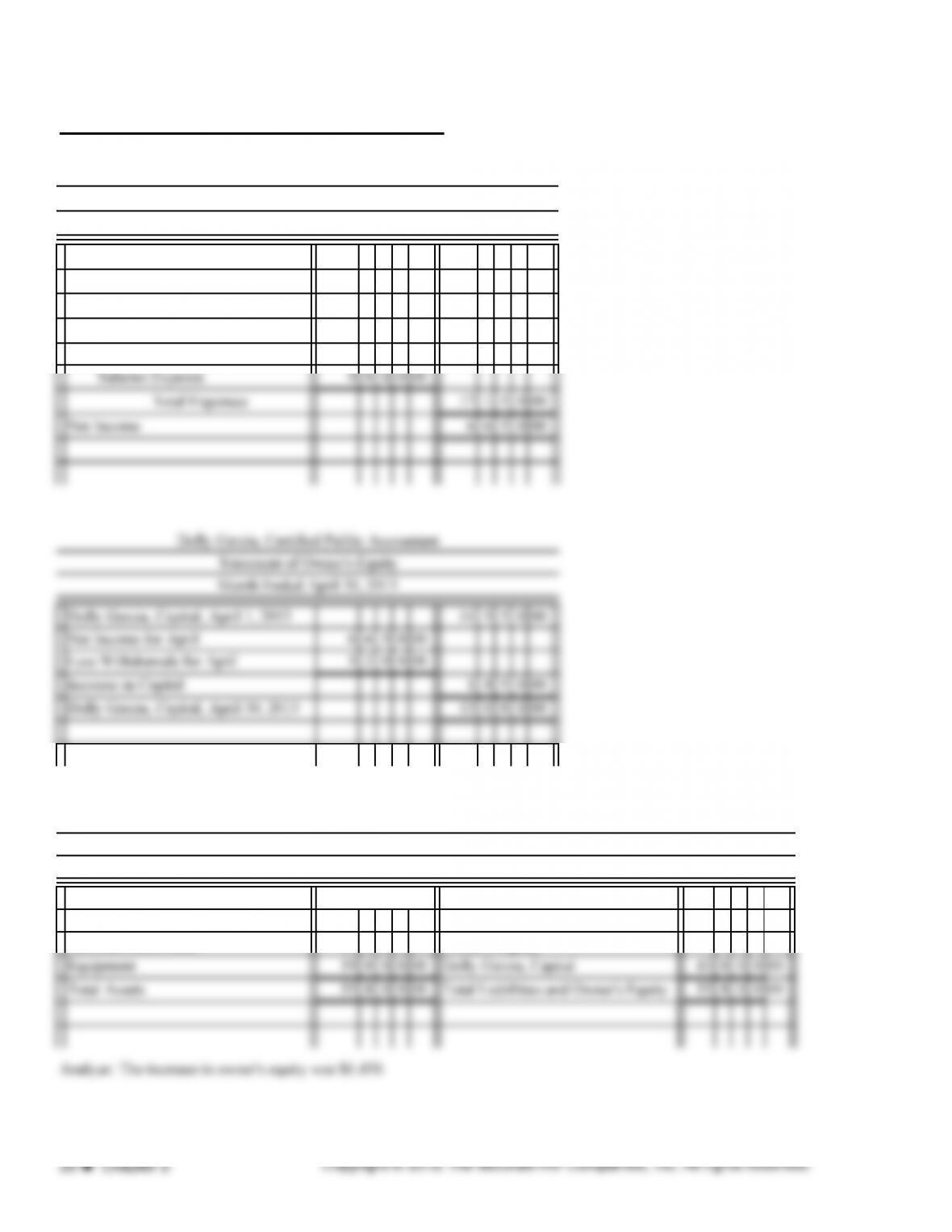

Statement of Owner’s Equity

Month Ended September 30, 2013

$4,800

Parker Investment Services

Assets Liabilities

Cash 3210000 Accounts Payable 470000

EXERCISE 2.10 (continued)

Parker Investment Services

Balance Sheet

Month Ended September 30, 2013

y

Accounts

Payable +

Owner’s

Capital

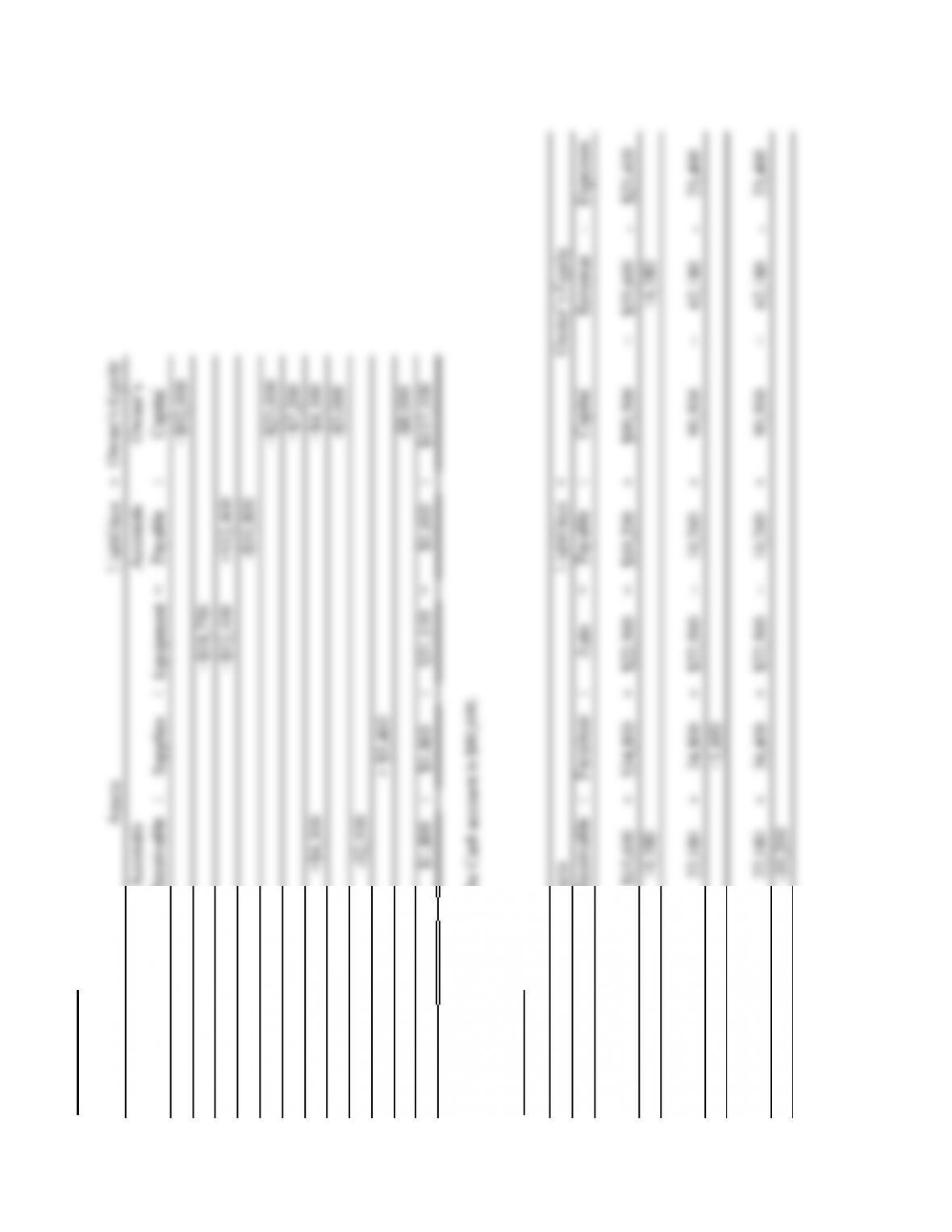

PROBLEM 2.2A (continued)

Cash + Accounts + Office + Auto = Payable +Capital + Revenue – Expenses

68,600 + 11,980 + 36,400 + $22,500 = 10,200 + 90,500 + 62,180 – 23,400

4. -780 +780

67,820 + 11,980 + 36,400 + $22,500 = 10,200 + 90,500 + 62,180 – 24,180

5. -2,500 -2,500

65,320 + 11,980 + 36,400 + $22,500 = 7,700 + 90,500 + 62,180 – 24,180

6. -8,700 +8,700

56,620 + 11,980 + 36,400 + $22,500 = 7,700 + 90,500 + 62,180 – 32,880

7. -1020 +1020

55,600 + 11,980 + 36,400 + $22,500 = 7,700 + 90,500 + 62,180 – 33,900

8. +9,500 +9,500

65,100 + 11,980 + 36,400 + $22,500 = 7,700 + 90,500 + 71,680 – 33,900

9. -2,250 +2,250

62,850 + 11,980 + 36,400 + $22,500 = 7,700 + 90,500 + 71,680 – 36,150

10. + +11,500 +11,500

$62,850 + $23,480 + $36,400 + $22,500 = $7,700 + $90,500 + $83,180 – $36,150

Analyze: Total assets equal $145,230.

New

Balances

New

Balances

New

Balances

New

Balances

Assets Owner’s Equity

New

Balances

New

Balances

New

Balances

New

Balances

Assets

Cash 3330000 2300000

Supplies 538000

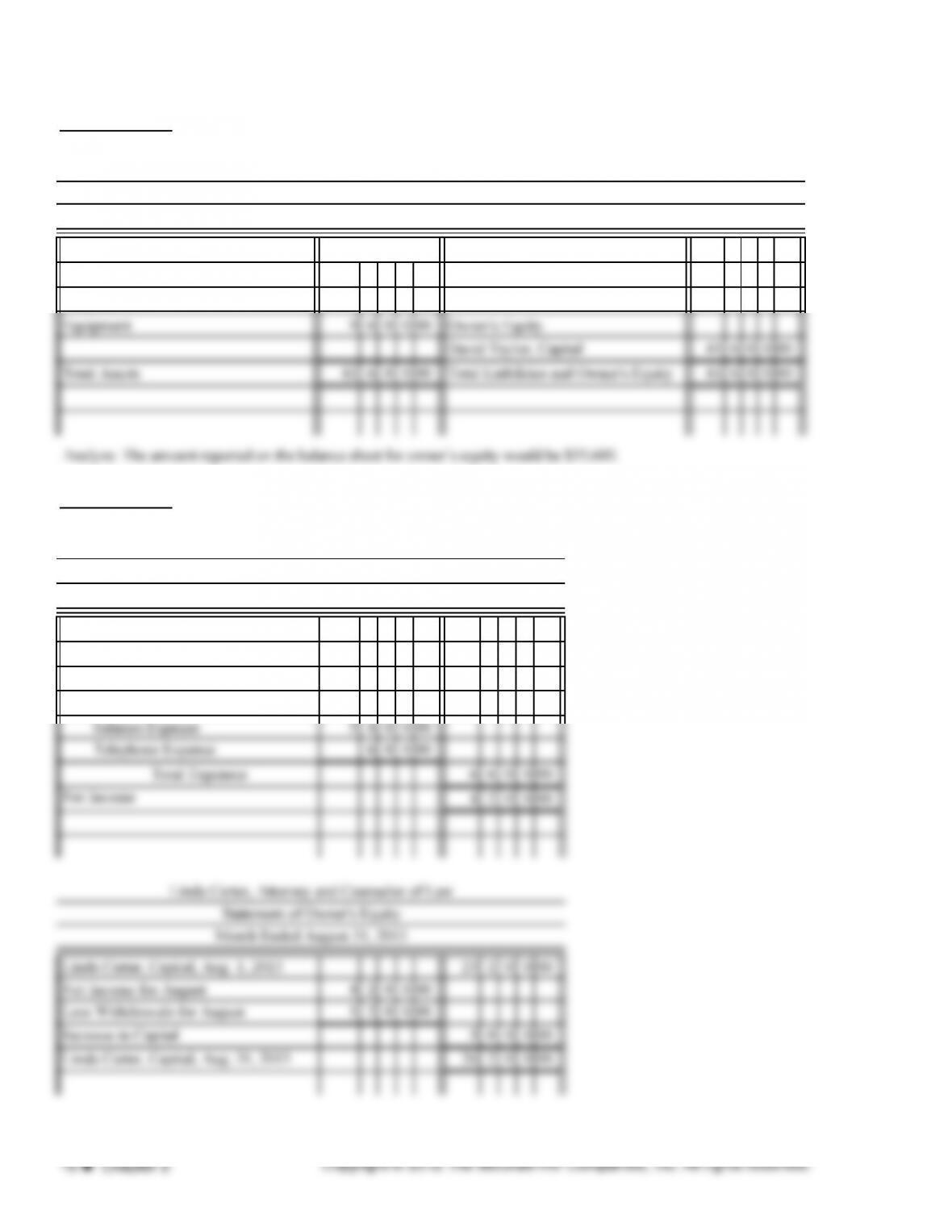

Balance Sheet

PROBLEM 2.3A

Valdez Equipment Repair

February 28, 2013

Liabilities

Accounts Payable

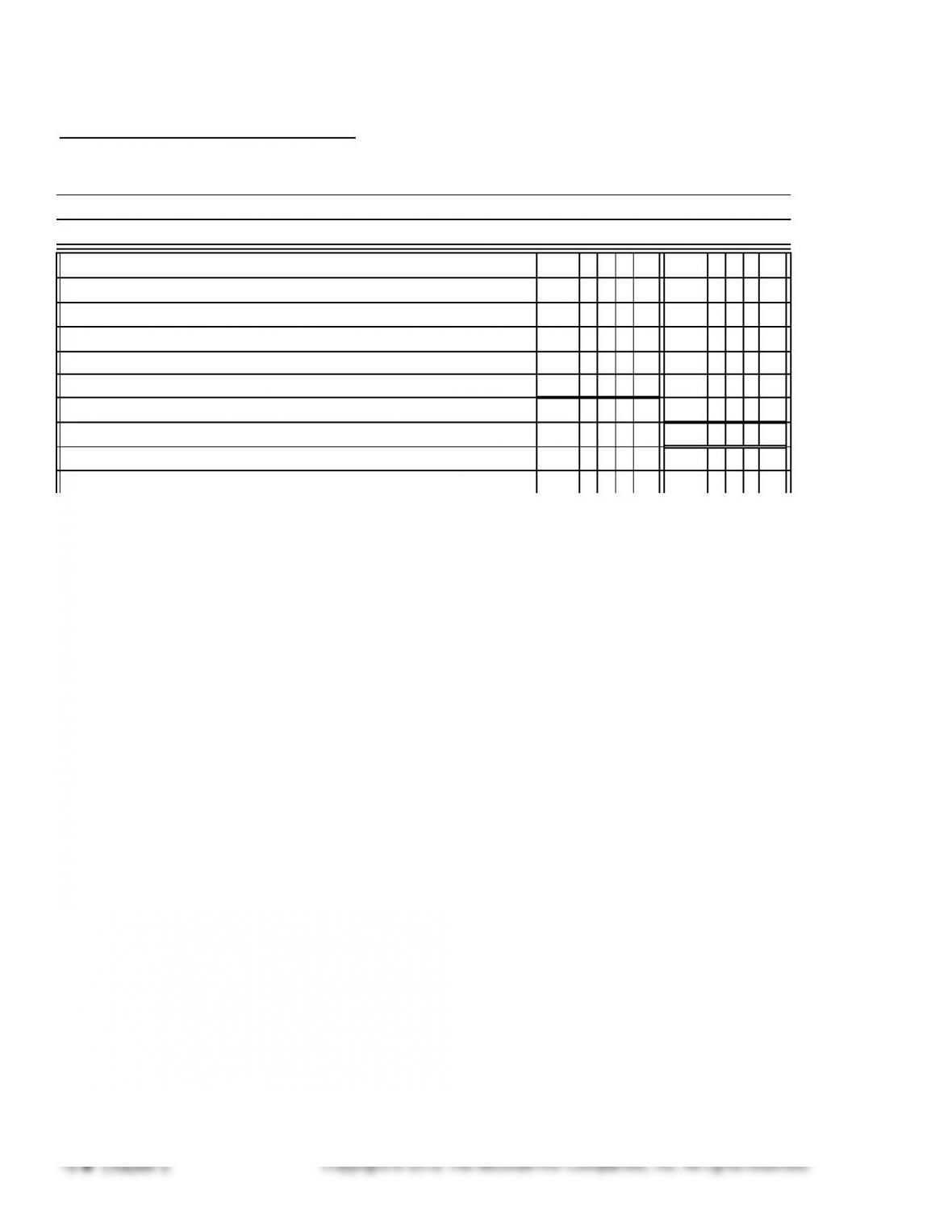

PROBLEM 2.4A (continued)

Assets

Cash 569600 440000

Liabilities

Accounts Payable

West Cleaning Service

Balance Sheet

May 31, 2013

PROBLEM 2.1B

Cash +

Accounts

Receivable + Supplies + Equipment =

Accounts

Payable +

Owner’s

Capital

1. +$36,000 +$36,000

2. -$16,000 +$16,000

3. +$6,000 +$6,000

4. -$3,000 -$3,000

5. +$6,000 +$6,000

6. +$4,200 +$4,200

7. +$3,650 +$3,650

8. -$2,600 -$2,600

9. +$2,500 -$2,500

10. -$3,150 + $3,150

11. -$5,000 -$5,000

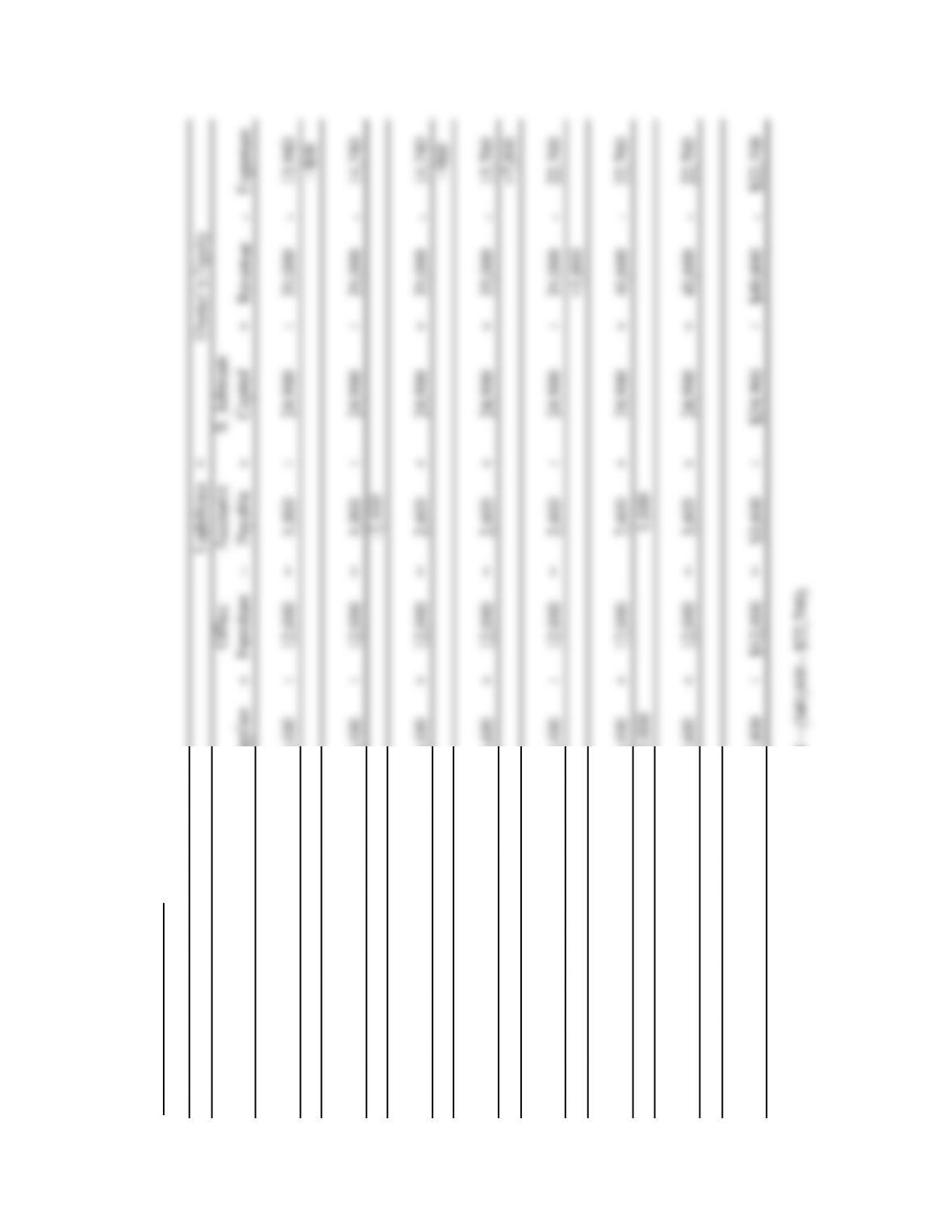

Totals $18,950 + $1,150 + $3,150 + $22,000 = $3,000 + $42,250

Analyze: Transaction 3 increased the Company’s debt by $6,000.

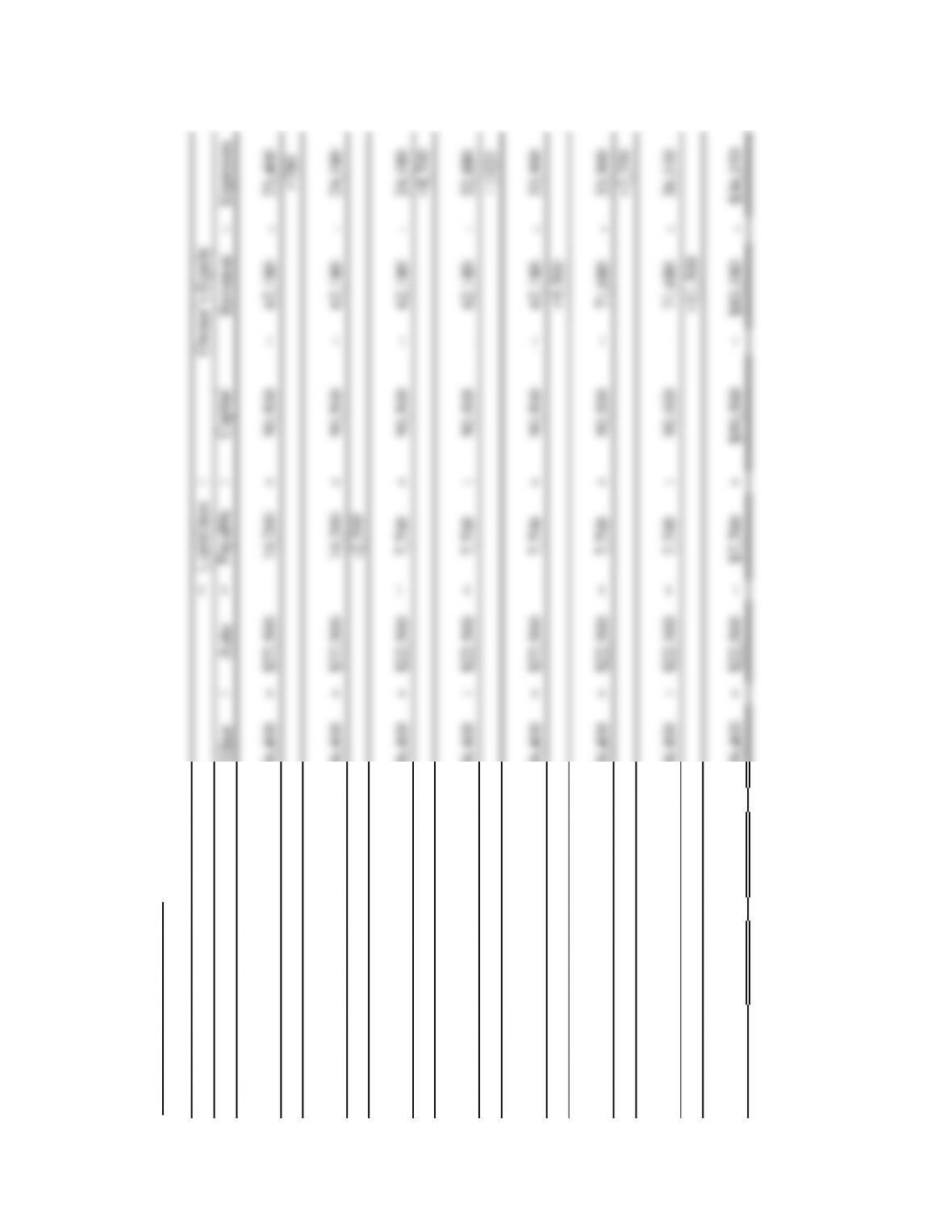

PROBLEM 2.2B

Cash +

Accounts

Receivable +Supplies +

Office

Furniture =

Accounts

Payable +

R. Johnson

Capital + Revenue – Expenses

$19,000 + $6,000 + $6,400 + $12,000 = $5,000 + $24,900 + $26,000 – $12,500

1. +4,000 +4,000

19,000 + 10,000 + 6,400 + 12,000 = 5,000 + 24,900 + 30,000 – 12,500

2. -1,440 +1,440

17,560 + 10,000 + 6,400 + 12,000 = 5,000 + 24,900 + 30,000 – 13,940

3. +5,000 +5,000

Assets

Assets Owner’s Equity

Beginning

Balances

New

Balances

New

Balances

PROBLEM 2.2B (continued)

Cash

+ Accounts

Receivable

+

Supplies +

Office

Furniture =

Accounts

Payable +

R. Johnson

Capital + Revenue – Expenses

22,560 + 10,000 + 6,400 + 12,000 = 5,000 + 24,900 + 35,000 – 13,940

4. -800 +800

21,760 + 10,000 + 6,400 + 12,000 = 5,000 + 24,900 + 35,000 – 14,740

5. -2,400 -2,400

19,360 + 10,000 + 6,400 + 12,000 = 2,600 + 24,900 + 35,000 – 14,740

6. -960 +960

18,400 + 10,000 + 6,400 + 12,000 = 2,600 + 24,900 + 35,000 – 15,700

7. -7,000 +7,000

11,400 + 10,000 + 6,400 + 12,000 = 2,600 + 24,900 + 35,000 – 22,700

8. +5,600 +5,600

17,000 + 10,000 + 6,400 + 12,000 = 2,600 + 24,900 + 40,600 – 22,700

9. +1,000 +1,000

17,000 + 10,000 + 7,400 + 12,000 = 3,600 + 24,900 + 40,600 – 22,700

10. +3,000 + -3,000

$20,000 + $7,000 + $7,400 + $12,000 = $3,600 + $24,900 + $40,600 – $22,700

Analyze: Owner’s Equity balance is $42,800; $24,900 + ($40,600 – $22,700).

New

Balances

New

Balances

New

Balances

New

Balances

Assets Owner’s Equity

New

Balances

New

Balances

New

Balances

New

Balances

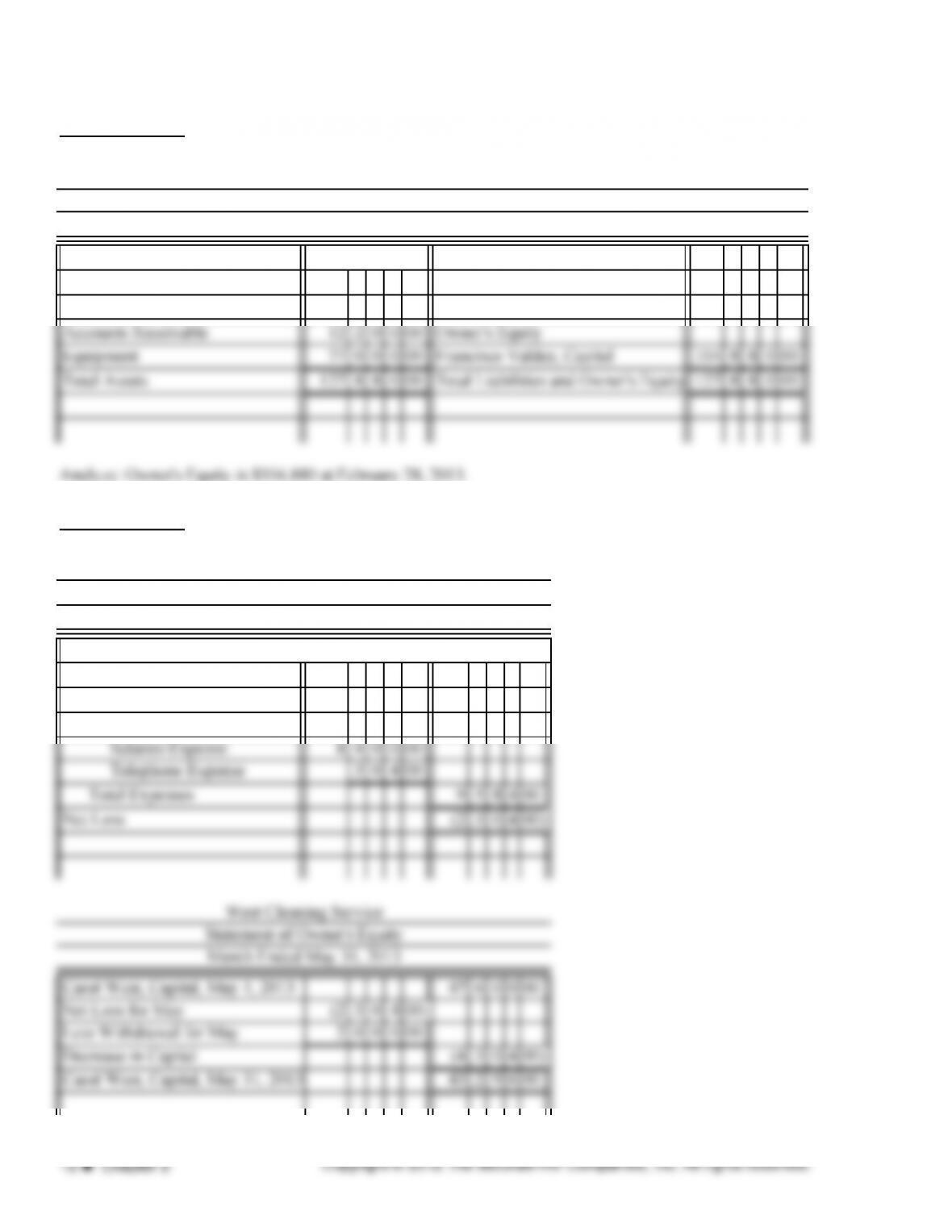

Assets

Cash 24 0 0 0 00

Furniture 800000

Revenue

Fees Income 10 8 0 0 00

Expenses

Utilities Expense 6 0 0 00

Linda Carter, Capital, Aug. 1, 2013 23 2 0 0 00

Net Income for August 420000

Less Withdrawals for August 120000

Increase in Capital 300000

Linda Carter, Capital, Aug. 31, 2013 26 2 0 0 00

Linda Carter, Attorney and Counselor of Law

Income Statement

Month Ended August 31, 2013

PROBLEM 2.4B

Liabilities

PROBLEM 2.3B

Taylor’s Tax Service

Balance Sheet

December 1, 2013

PROBLEM 2.4B (continued)

Assets

Cash 480000 60000

Accounts Receivable 660000

Analyze: Net income of $4,200 was transferred from the income statement.

Linda Carter, Attorney and Counselor at Law

Balance Sheet

August 31, 2013

Liabilities

Accounts Payable

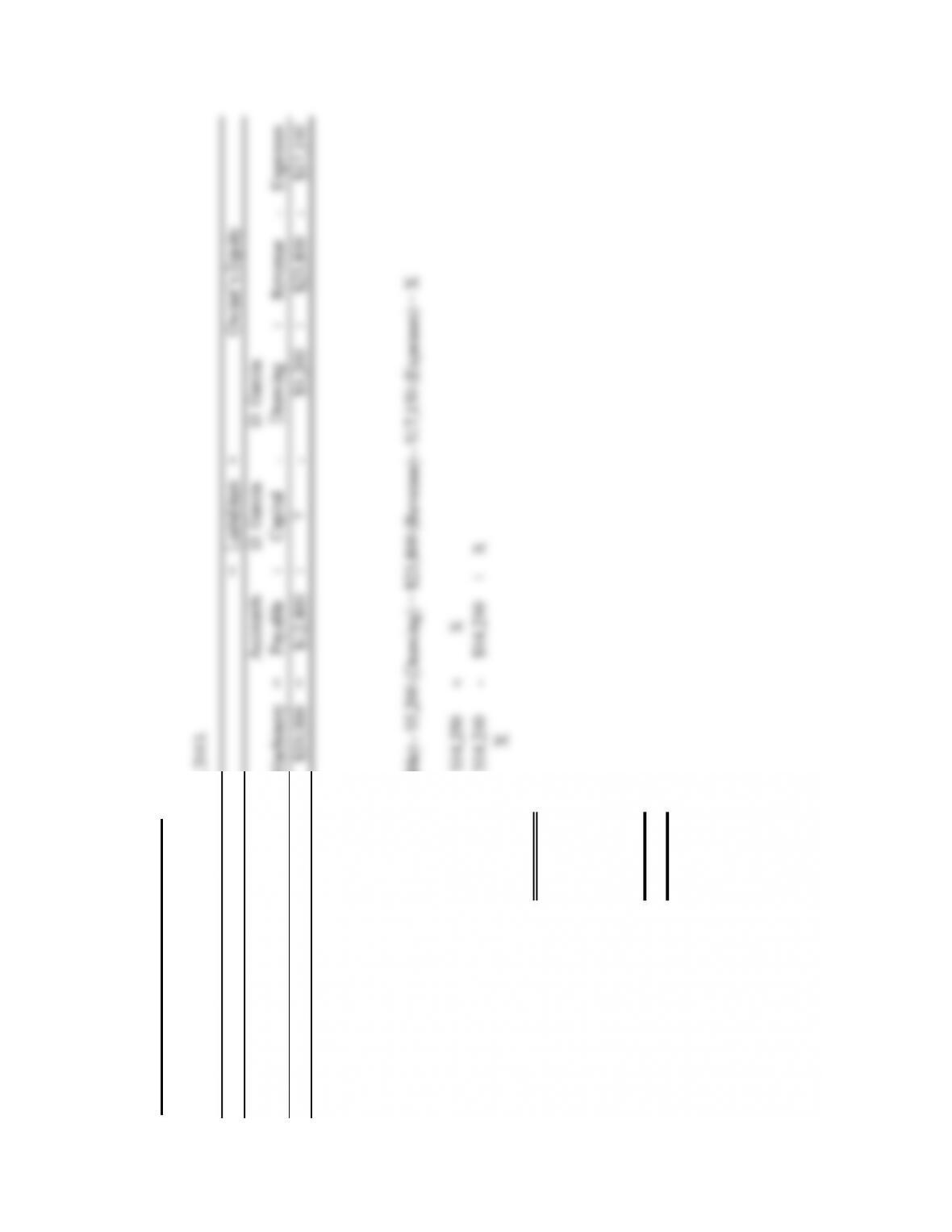

CRITICAL THINKING PROBLEM 2.1

Revenue

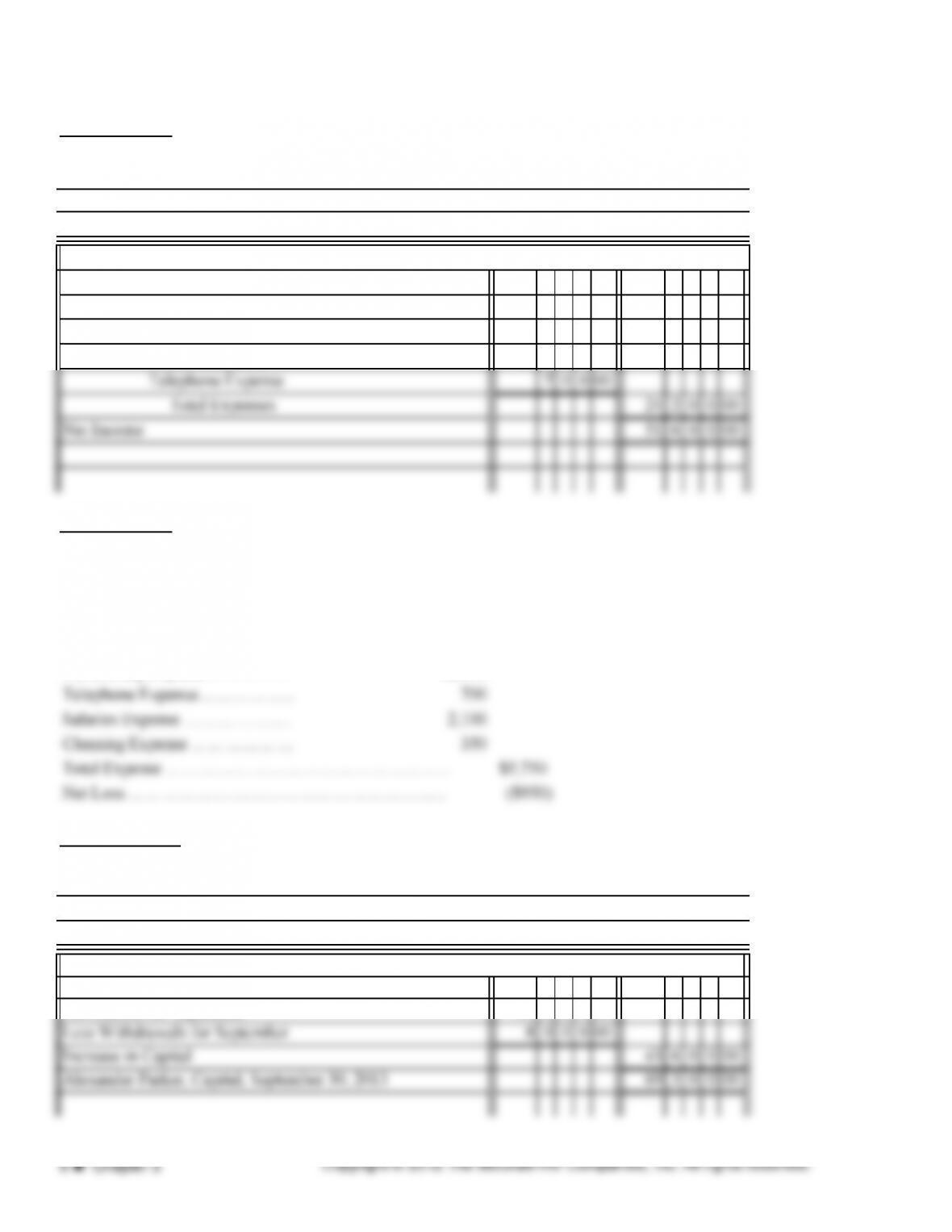

Fees Earned 9 7 6 0 00

Expenses

Rent Expense 800000

Cleaning Expense 210000

Advertising Expense 8 0 0 00

Total Expenses 10 9 0 0 00

Net Loss (1 1 4 0 00)

It is not unusual for new businesses to operate at a loss. James should project his income and expenses for

the next several months to determine how much new business he will need to earn an income. Students’

suggestions for improving the accounting system might include opening a business checking account, not

using a personal credit card for business expenses, setting up a filing system for business records, and

purchasing a computer to maintain financial records.

Body Builders Fitness Center

Income Statement

Month Ended November 30, 2013

Some students may include the warm-up suits as a business expense. If the suits are a type of uniform,

their inclusion is appropriate; if they are to be worn at home and at work, their cost is not a business

expense.

The parking ticket is a personal expense. The cleaning of the studio and the printing of the flyers are

business expenses. Payment of expenses with the owner’s personal credit card would be considered an

additional investment by the owner.

CRITICAL THINKING PROBLEM 2.2

Determine the balance for Dolly Garcia, April 30, 2013.

Cash +

Accounts

Receivable + Machinery =

Accounts

Payable +

D. Garcia

Capital –

D. Garcia

Drawing + Revenue – Expenses

$26,000 + $10,800 + $19,000 = $12,800 + ? – $5,200 + $23,800 – $17,150

Solving for X:

$55,800 = $14,250 + X

$55,800 – $14,250 = $14,250 – $14,250 + X

$41,550 = X

= $41,550

Advertising Expense $3,750

Maintenance Expense 4,400

Salaries Expense 9,000

Total Expenses $17,150

Dolly Garcia, Capital,

April 1, 2013

Assets Owner’s Equity

Let Dolly Garcia, Capital = X.

$55,800 (Total Assets) = $12,800 (Accounts Payable) – $5,200 (Drawing) + $23,800 (Revenue) – $17,150 (Expenses) + X

Revenue

Fees Earned 23 8 0 0 00

Expenses

Advertising Expense 375000

Maintenance Expense 440000

CRITICAL THINKING PROBLEM 2.2 (continued)

Dolly Garcia, Certified Public Accountant

Income Statement

Month Ended April 30, 2013

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

1.

3.

4.

Organized financial information can be used to evaluate operating efficiency and to make decisions

about current and future activities.

No. Early development is expensive, risky, and time consuming. Profits may not be achieved for a

year or more.

Not necessarily. Reinvestments in assets or use of cash to pay debts affect cash. In addition, sales or

revenue may have been “on account.”

Part A True-False

1.

2.

SOLUTIONS TO PRACTICE TES

T

TRUE

FALSE