• HVP has assisted in the development of over 80 ambulatory care centers representing over $400

million in value.

• HVP has worked with over 200 hospitals nationwide.

• HVP is an employee-owned company. The founders of HVP personally fund the company. All

senior-level employees of HVP enjoy a degree of ownership and share in the success of HVP.

• Name, location, and nature of business

• Starting date of the agreement

• Life of the partnership

• Rights and duties of each partner

• Capital to be contributed by each partner

• Drawings of the partners

• Fiscal year and accounting method

• Method of allocating income or loss

• Dissolution and liquidation procedures

1. For each partner, and in total for all partners: beginning balances of capital, share of net income

or loss for the year, withdrawals for the year, and ending capital balance.

3. The capital account of the partner selling the interest is debited for the fractional share of the

4. A dissolution is the termination of the contract between the existing partners. Business operations

5. Skills, experience and reputation brought to the new business; time to be spent; amount of capital

Discussion Questions

Chapter Opener: Thinking Critically

ACCOUNTING FOR PARTNERSHIPS

CHAPTER 19

Students should recognize that partners carry some responsibility for the debts of the partnership and

benefit directly from company profits. Since partners benefit directly from the profits of the company,

they have a vested interest in making sure all the firm’s clients are satisfied with the products and

services they receive.

Fast Facts

Managerial Implications: Thinking Critically

Discussion Questions (continued)

6. a. The accounting records are closed and the net income or net loss is recorded and transferred to the

7. The drawing account for each partner is charged for cash withdrawn for any purpose (including salary

allowances), and other assets (such as merchandise taken by the partner from the business).

9. Each partner is empowered to act as an agent for the partnership, binding the firm by those acts if they

are within the normal scope of the partnership’s activities.

11. No. Salaries of the partners are only a factor in the allocation of net income or net loss.

13. The equity accounts are different. Individual capital and drawing accounts must be maintained for

each partner.

14. Records must be kept of all amounts owed to the sole proprietor because they are (usually) transferred

16. No. However, the individual partners pay income tax on their shares of the partnership’s income.

18. Unlimited liability of general partners; mutual agency; lack of continuity and difficulty of transfer of

ownership.

EXERCISE 19.1

PAGE

POST.

REF.

1 2013 1

EXERCISE 19.2

PAGE

POST.

REF.

1 2013 Accounts Receivable 12000000 1

2 Merchandise Inventory 9600000 2

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

EXERCISE 19.3

4800000

10800000

Joan Clay, Capital 5400000

17200000

James Dear, Capital

Total Liabilities and Partners’ Equity

Cash

The Leisure Room

Balance Sheet

May 1, 2013

Assets

EXERCISE 19.4

Chanda

Salary $96,000

Interest (10% × $408,000) 40,800

50% of net income after allowances (19,800)

Total share of net income to Chanda $117,000

Jones

EXERCISE 19.5

Reagan

Interest (10% × $120,000) $12,000

60% of balance after interest 135,360

EXERCISE 19.6

Raymond Zeidan

Salary $84,000

60% of balance after salary allowances 97,680

Total net income to Zeidan $181,680

Allocation of Net Income

Allocation of Net Income

EXERCISE 19.7

PAGE

POST.

REF.

1 2013 1

2 Dec. 31 Income Summary 9600000 2

12 To close Ferguson’s drawing account 12

EXERCISE 19.8

PAGE

POST.

REF.

1 2013 1

2 Dec. 31 Income Summary 2400000 2

EXERCISE 19.9

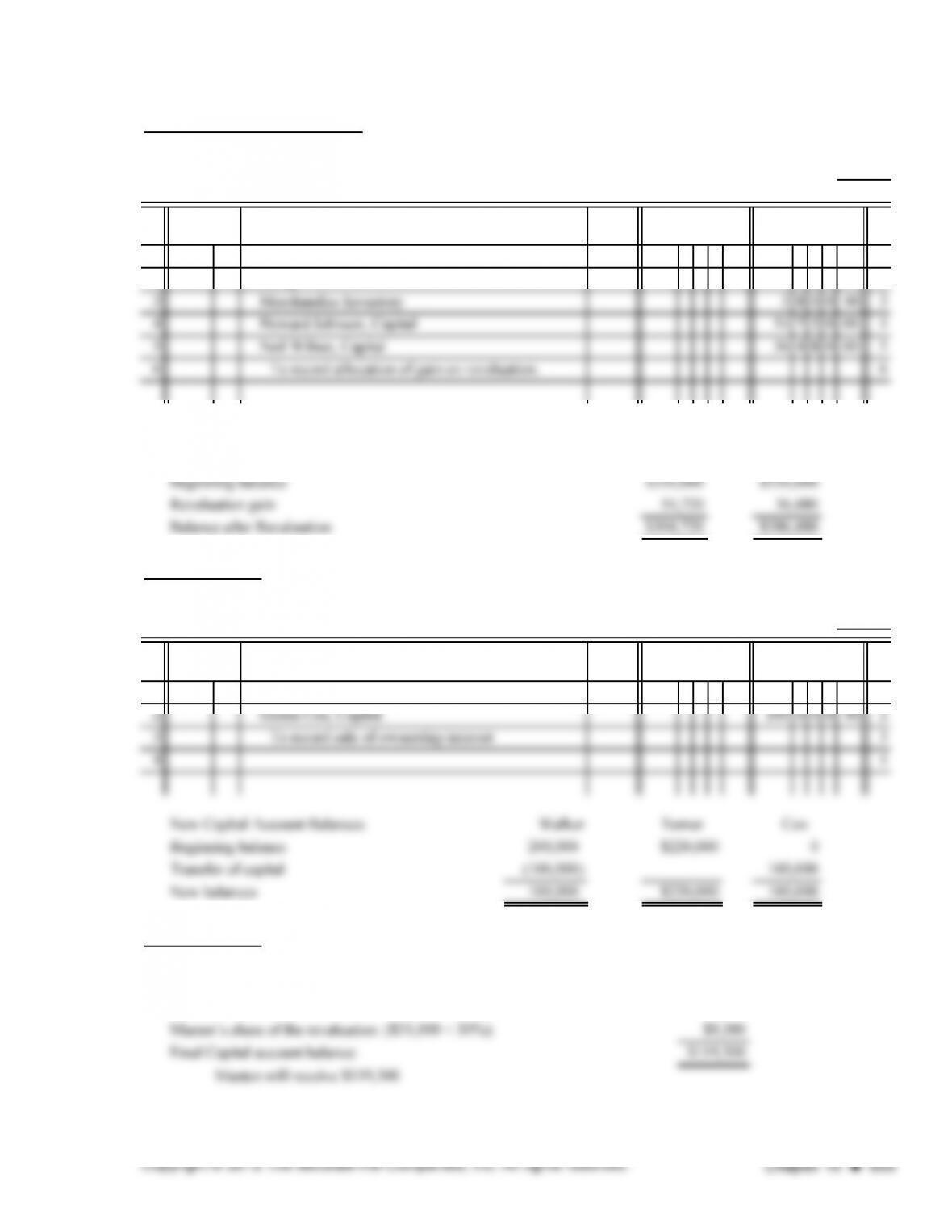

EXERCISE 19.10

Effect of revaluation: ($3,800)

Merchandise Inventory: 95,000

DATE DESCRIPTION DEBIT CREDIT

DATE DESCRIPTION

GENERAL JOURNAL

DEBIT

GENERAL JOURNAL

CREDIT

EXERCISE 19.10 (continued)

(1)

PAGE

POST.

REF.

1 2013 1

2 Dec. 31 Building 95 0 0 0 00 2

(2)

New Capital Account Balances

EXERCISE 19.11

PAGE

POST.

REF.

1 2013 James Walker, Capital 100 0 0 0 00 1

EXERCISE 19.12

The increase in net assets as a result of the revaluation is $31,000

Masten’s capital account balance before revaluation:

$110,000

DATE DEBIT CREDIT

GENERAL JOURNAL

GENERAL JOURNAL

DESCRIPTION

DESCRIPTIONDATE DEBIT CREDIT

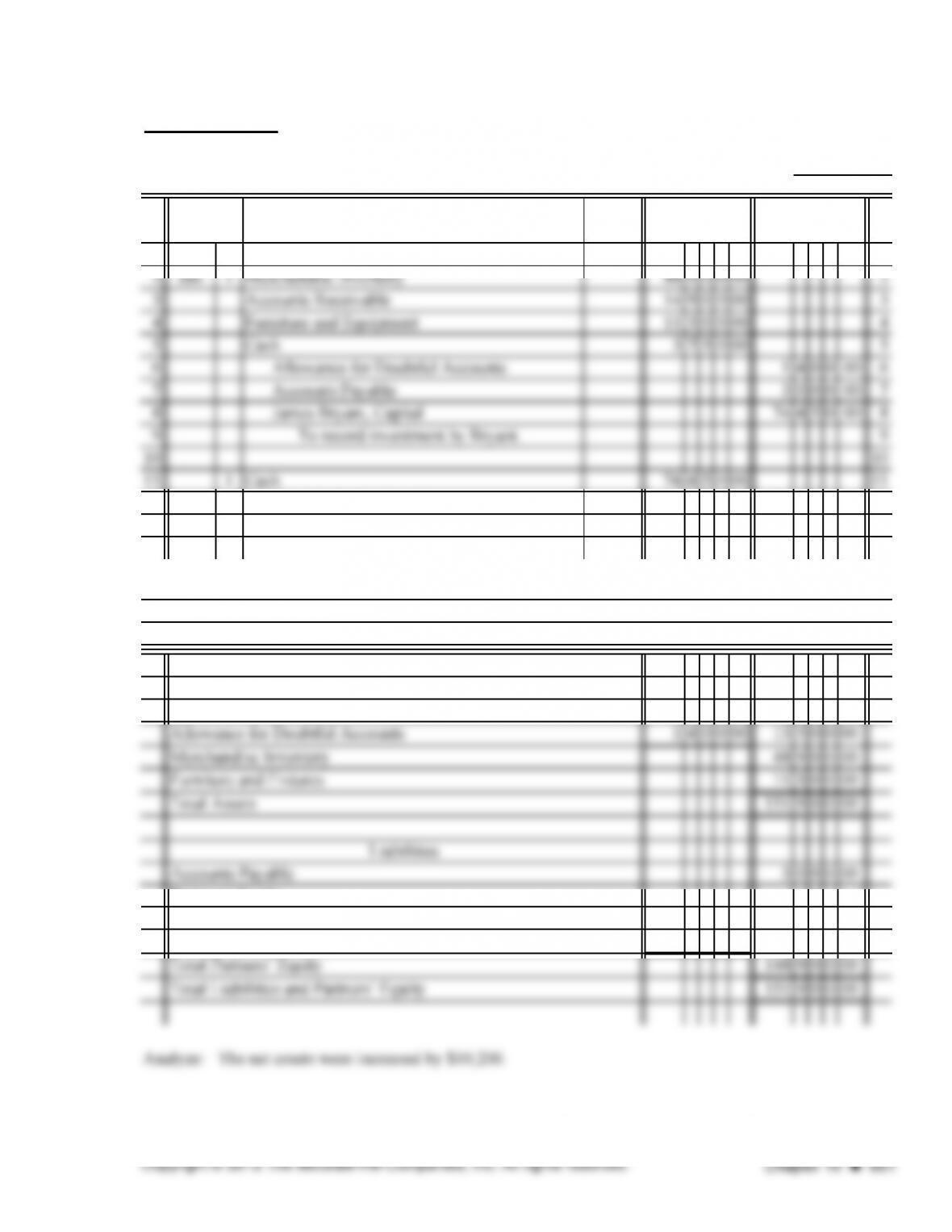

Johnson Wilner

PROBLEM 19.1A

PAGE

POST.

REF.

1 2013 1

12 1 Cash 42320000 12

13 Reginald Pittman, Capital 423200 00 13

14 14

15 Pittman in Contemporary Computing 15

Cash 46320000

Accounts Receivable 11600000

Re

g

inald Pittman, Ca

p

ital 42320000

Total Partners’ E

q

uit

y

95220000

GENERAL JOURNA

L

DATE ACCOUNTS DEBIT CREDIT

To record investment of Reginald

Balance Sheet

January 1, 2013

Assets

Contemporary Computing

PROBLEM 19.2A

PAGE

POST.

REF.

1 2014 1

12 Camille Willis, Capital 74450 00 12

13 To record investment by Willis 13

Cash 7820000

Accounts Receivable 1490000

Partners’ Equity

James Bryant, Capital 7445000

Camille Willis, Capital 7445000

Balance Sheet

January 1, 2014

Assets

Bryant and Willis Angler’s Outpost

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

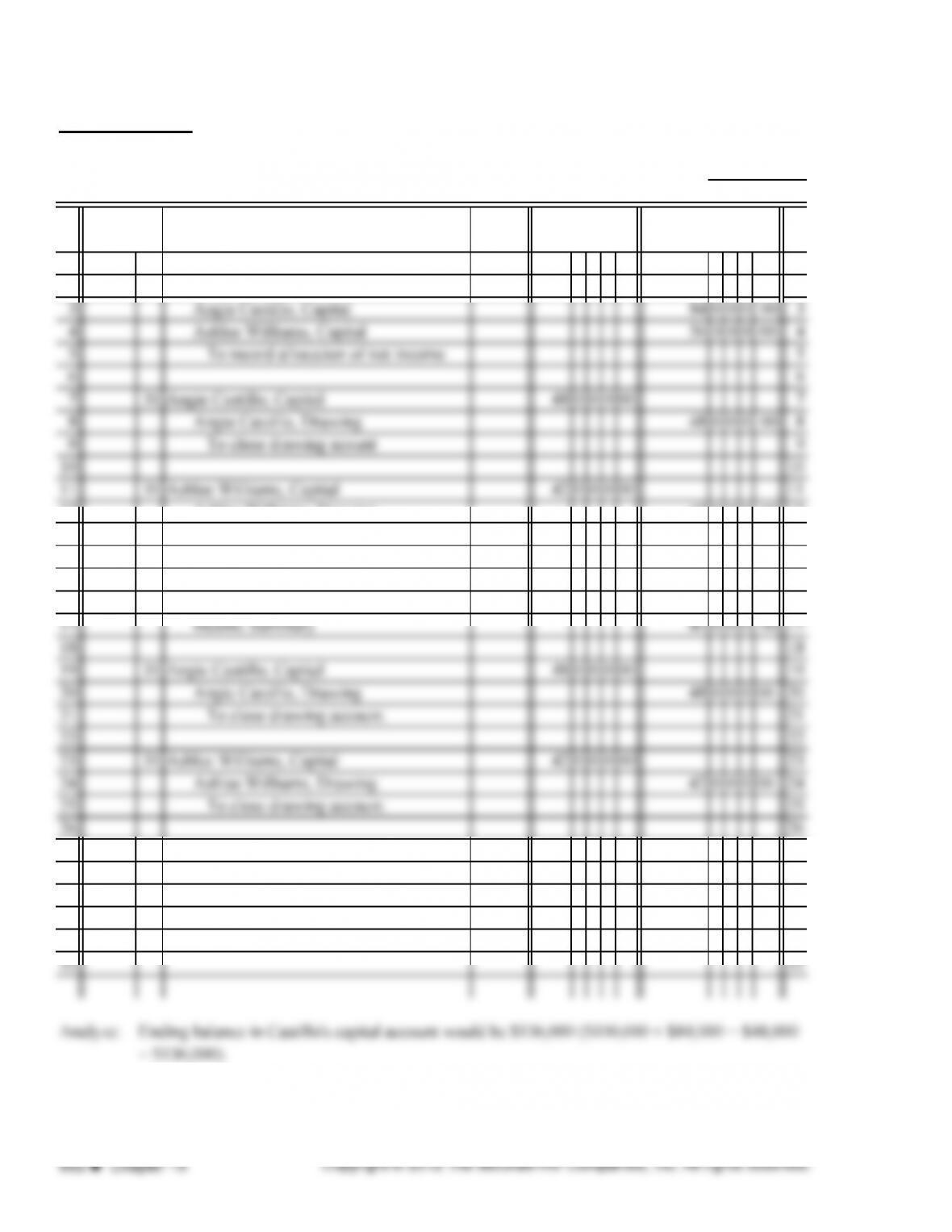

PROBLEM 19.3A

PAGE

POST.

REF.

1 2013 1

2 Dec. 31 Income Summary 14000000 2

12 Ashlee Williams, Drawing 42000 00 12

13 To close drawing account 13

14 14

15 31 Angie Castillo, Capital 2400000 15

16 Ashlee Williams, Capital 1600000 16

27 27

28 28

29 29

30 30

31 31

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 19.4A

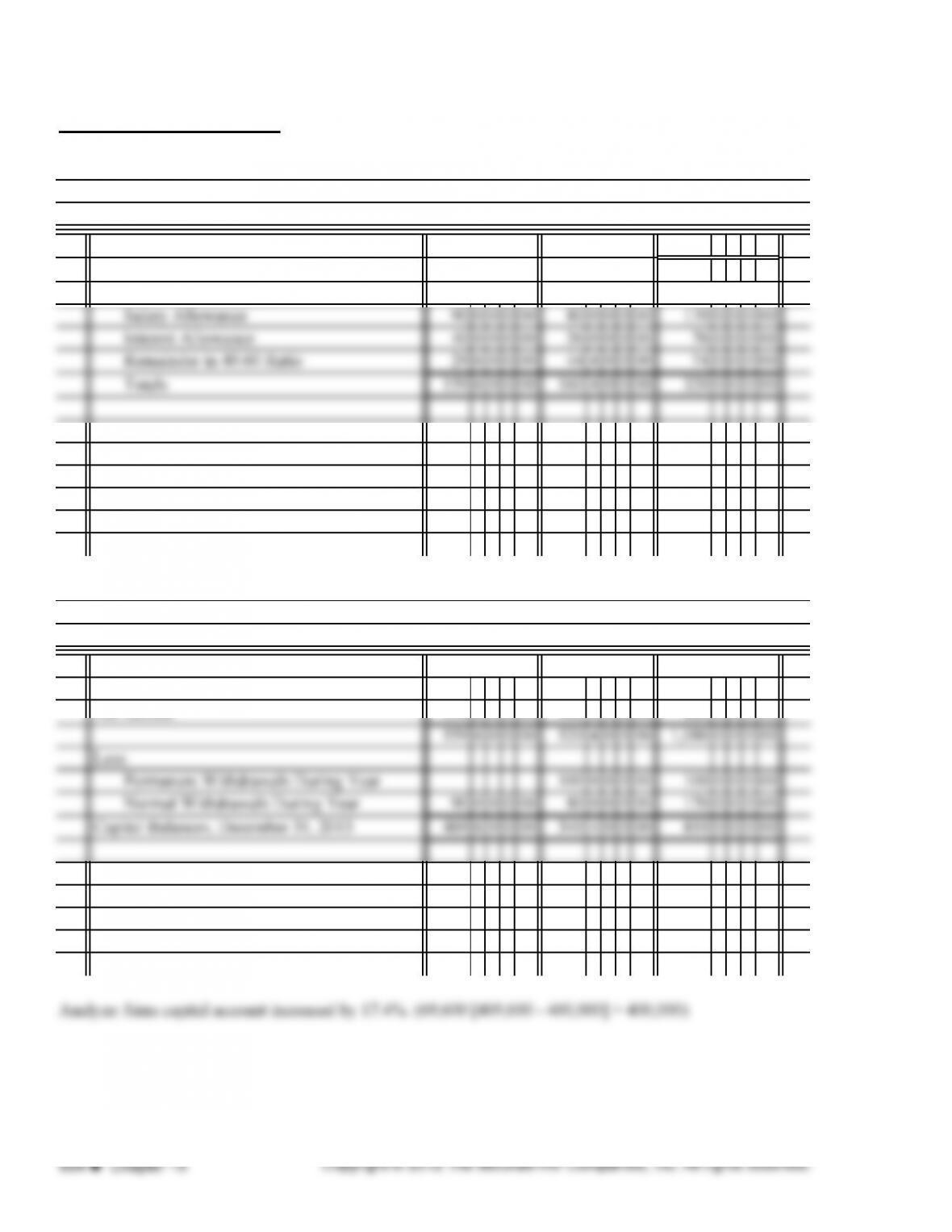

PAGE

POST.

REF.

1 2013 1

12 31 Income Summary 7600000 12

13 Larry Sims, Capital 40 0 0 0 00 13

14 Larry Thomas, Capital 36000 00 14

15 Interest allowances for year 15

16 16

17 31 Income Summary 7400000 17

25 To close drawing account 25

26 26

27 31 Larry Thomas, Capital 8000000 27

28 Larry Thomas, Drawing 8000000 28

29 To close drawing account 29

30 30

31 31

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 19.4A (continued)

Net Income for Year 32000000

Distribution of Net Income

Capital Balances, January 1, 2013 40000000 36000000 76000000

Net Income 15960000 16040000 32000000

Larry’s Antiques

Statement of Partners’ Equities

Year Ended December 31, 2013

Larry Sims Larry Thomas Total

Larry’s Antiques

Income Statement

Year Ended December 31, 2013

Larry Sims Larry Thomas Total

PROBLEM 19.5A

PAGE

POST.

REF.

12013 1

12 31 Cash 12000000 12

13 Kathryn Thomas, Capital 12000000 13

14 To record investment by K. Thomas 14

15 15

16 31 Cash 12000000 16

27 Kathryn Thomas, Capital 12000000 27

28 To record investment by K. Thomas 28

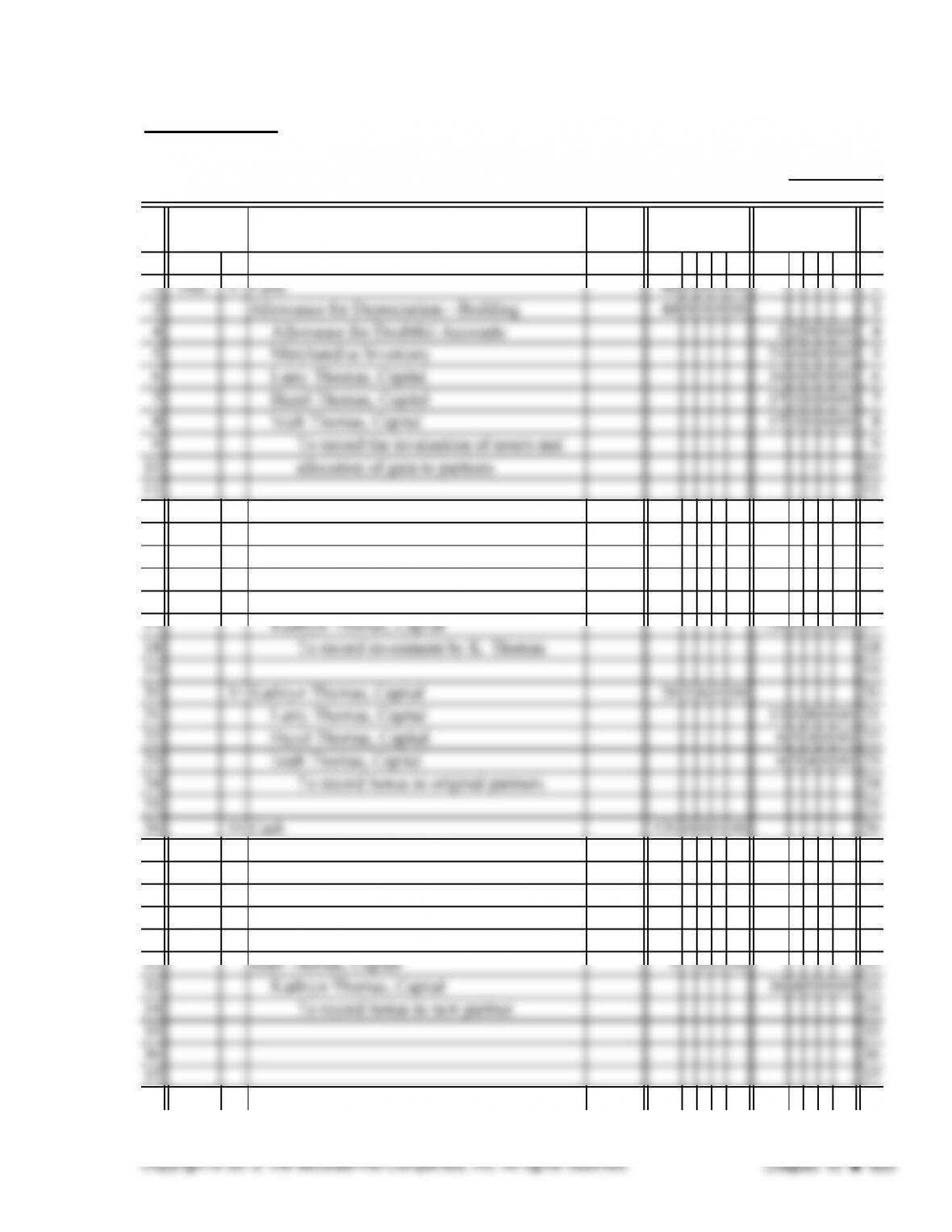

29 29

30 31 Larry Thomas, Capital 1820000 30

31 Hazel Thomas, Capital 910000 31

GENERAL JOURNAL

DATE ACCOUNTS DEBIT CREDIT

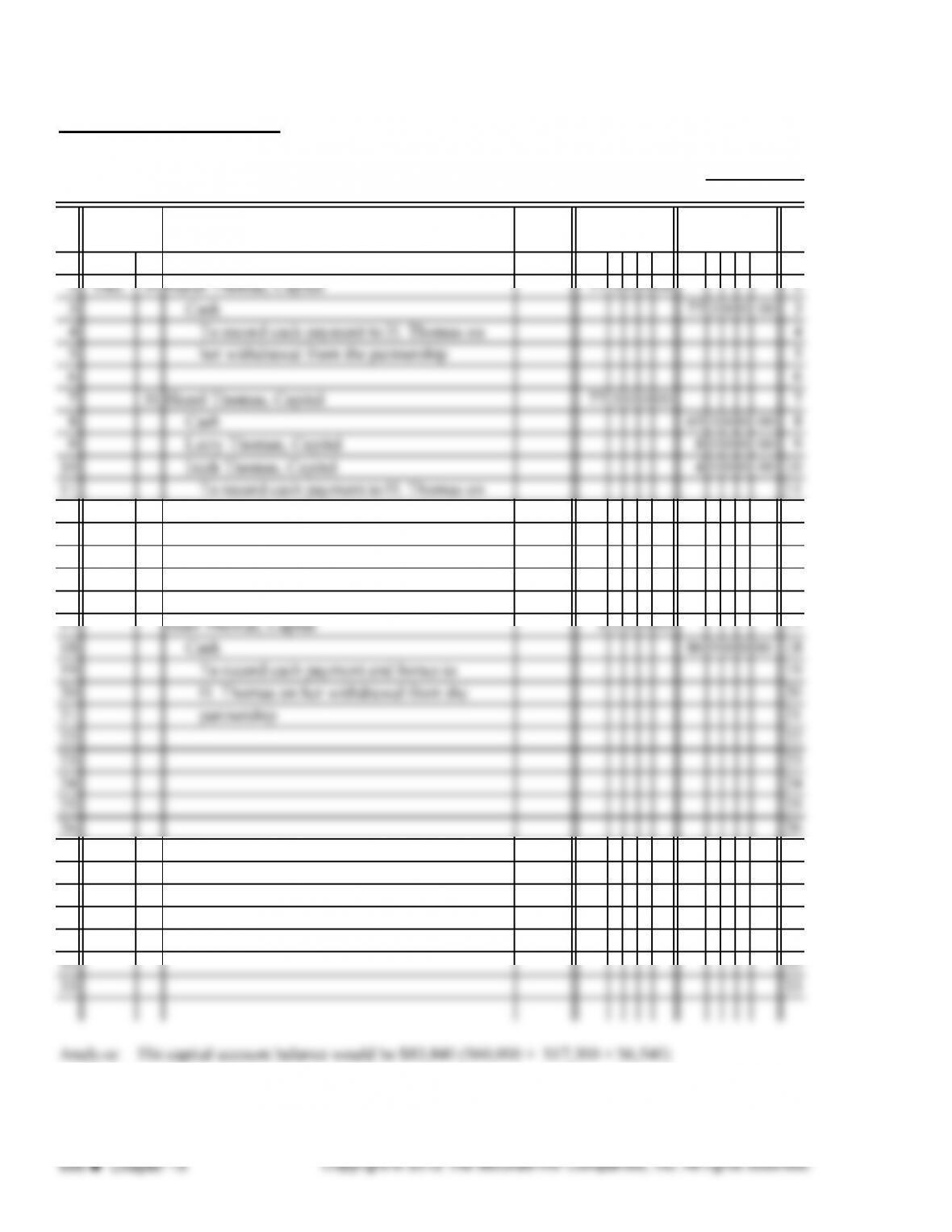

PROBLEM 19.5A (continued)

PAGE

POST.

REF.

1 2013 1

12 her withdrawal from the partnership and 12

13 bonus to remaining partners 13

14 14

15 31 Hazel Thomas, Capital 77 3 0 0 00 15

16 Larry Thomas, Capital 640000 16

27 27

28 28

29 29

30 30

31 31

CREDIT

14GENERAL JOURNAL

DATE DESCRIPTION DEBIT

PROBLEM 19.6A

PAGE

POST.

REF.

12013 1

12 1 Cash 120 0 0 0 00 12

13 June Cho, Capital 120 0 0 0 00 13

14 Cash investment by Cho for 25% interest 14

15 15

16 1 June Cho, Capital 10 0 0 0 00 16

27 June Cho, Capital 920000 27

28 Bonus to new partner 28

29 29

30 30

31 31

CREDIT

GENERAL JOURNAL

DATE ACCOUNTS DEBIT

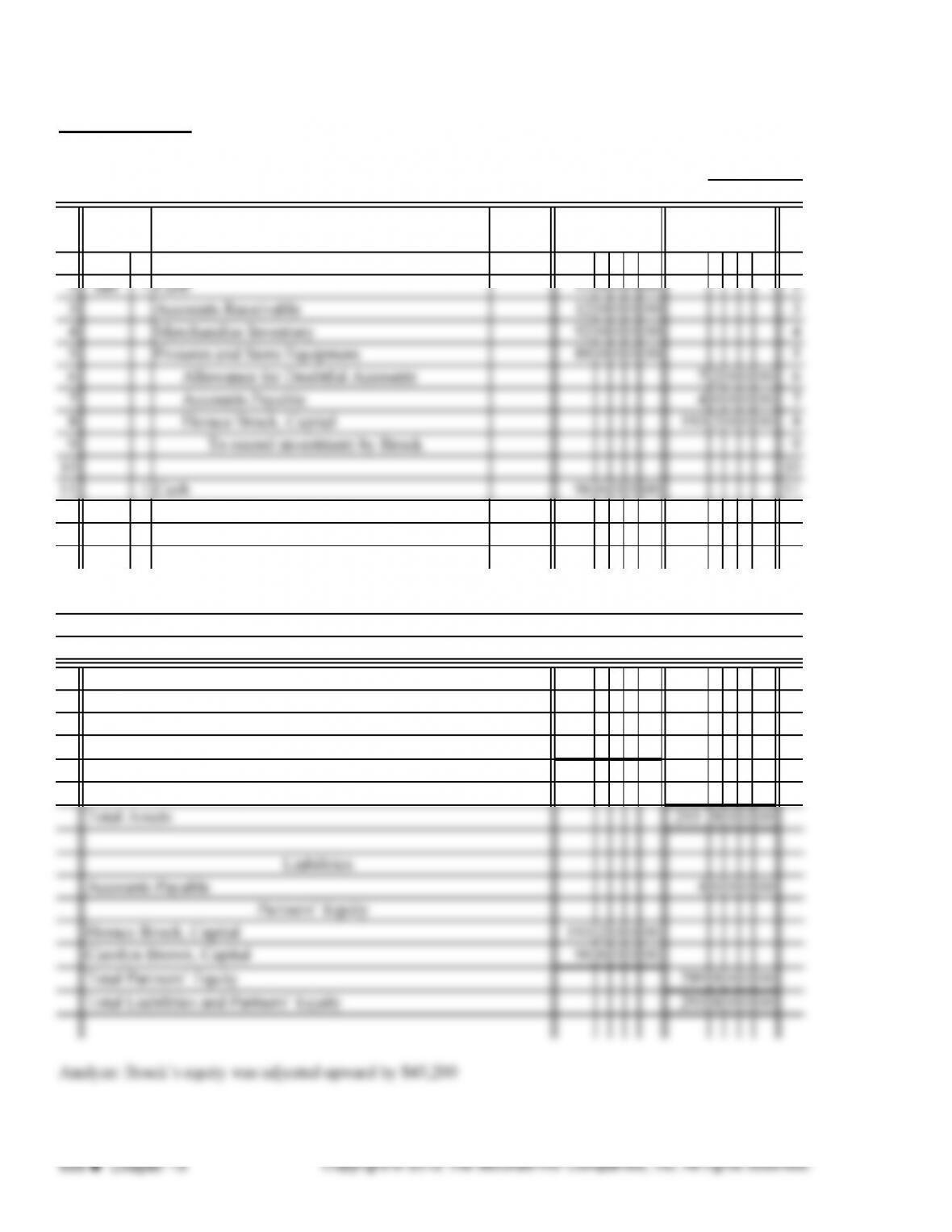

PROBLEM 19.1B

PAGE

POST.

REF.

1 2014 1

12 Carolyn Brown, Capital 9660000 12

13 To record investment by Brown 13

Cash 10900000

Accounts Receivable 1200000

Allowance for Doubtful Accounts 720000 480000

Merchandise Inventory 9200000

Furniture and Fixtures 8800000

Balance Sheet

January 1, 2014

Assets

Brock-Brown Broadcast Company

GENERAL JOURNAL

DATE ACCOUNTS DEBIT CREDIT