PROBLEM 18.9A (continued)

PAGE

POST.

REF.

37 31 Impairment of Intangibles—Goodwill 3000000 37

GENERAL JOURNAL 1

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 18.1B

1. Land

Purchase of land $375,000

Demolition of building $30,000

Less salvage (17,000) 13,000

Attorney fees 9,000

2. Building

3. Land Improvements

Paving of sidewalks and curbs $90,000

PROBLEM 18.2B

Year

Acquisition

Cost

Salvage

Value Useful Life

Annual

Depreciation

Accumulated

Depreciation

STRAIGHT-LINE METHOD

PROBLEM 18.2B (continued)

Year Fraction

Cost Less

Salvage

Annual

Depreciation

Accumulated

Depreciation

Year

Beginning

Book Value Rate

Annual

Depreciation

Accumulated

Depreciation

PROBLEM 18.3B

Year

Acquisition

Cost

Salvage

Value Useful Life

Annual

Depreciation

Accumulated

Depreciation

SUM-OF-THE-YEARS’-DIGITS METHOD

DOUBLE-DECLINING-BALANCE METHOD

STRAIGHT-LINE METHOD

PROBLEM 18.3B (continued)

Year

Acquisition

Cost

Salvage

Value

Total Expected Units

of Production

Actual Unit

s

of Production

Cost per

unit

Annual

Depreciation

Accumulated

Depreciation

2013 $880,000 $80,000 3,200,000 320,000 $0.25 $80,000 $80,000

PROBLEM 18.4B

1. Depreciation of computer:

2. MACRS recovery of computer:

3. Depreciation of van:

4. MACRS recovery of van:

2013—($36,000 × .20) = $7,200

UNITS-OF-PRODUCTION METHOD

PROBLEM 18.5B

PAGE

POST.

REF.

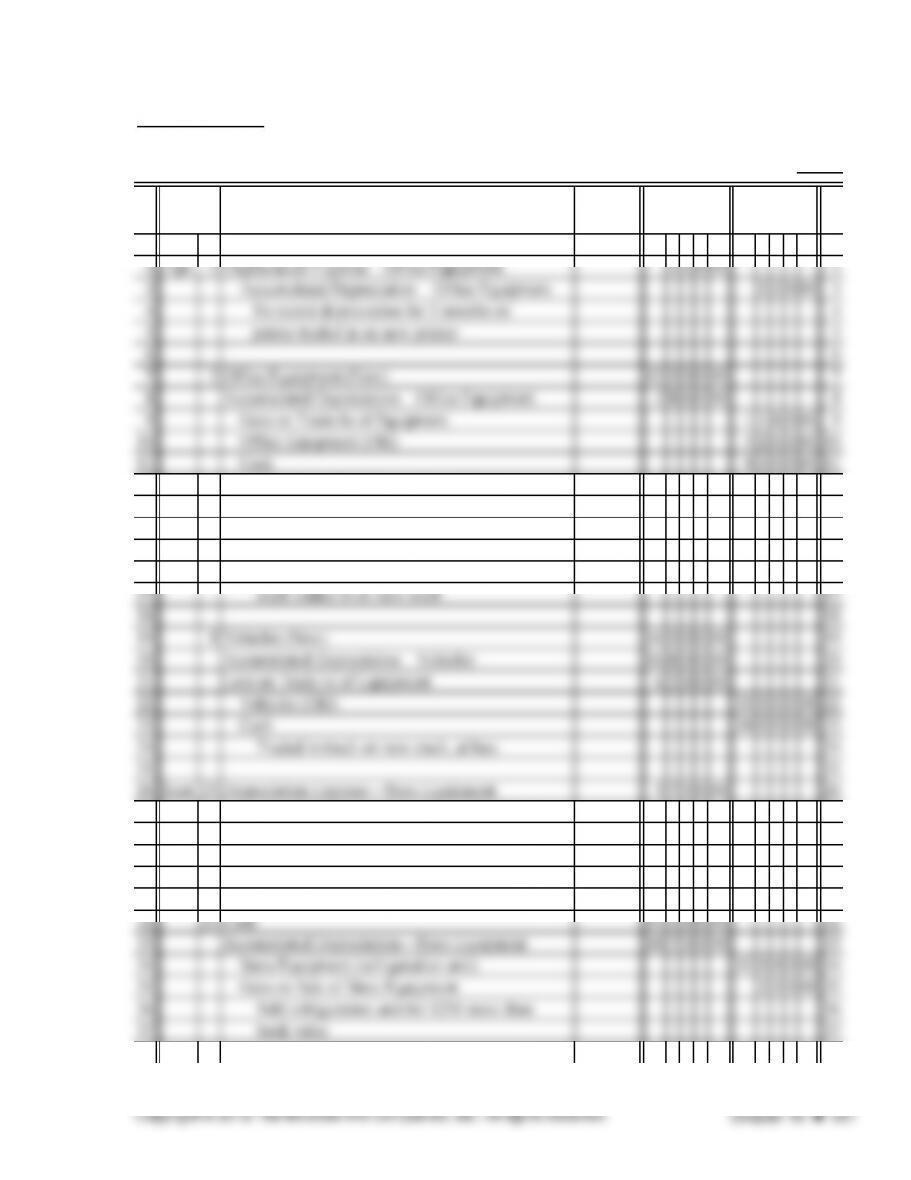

1 2013 1

12 Traded in old copier on new copier 12

13 13

14 July 8 Depreciation Expense—Vehicles 280000 14

15 Accumulated Depreciation—Vehicles 28000015

16 To record depreciation for six months on 16

27 Accumulated Depreciation—Store Equipment 37500027

28 To record depreciation for nine months 28

29 on refrigeration unit sold 29

30 30

31 Case A: Unit is sold for $13,500 31

GENERAL JOURNAL 1

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 18.5B (continued)

PAGE

POST.

REF.

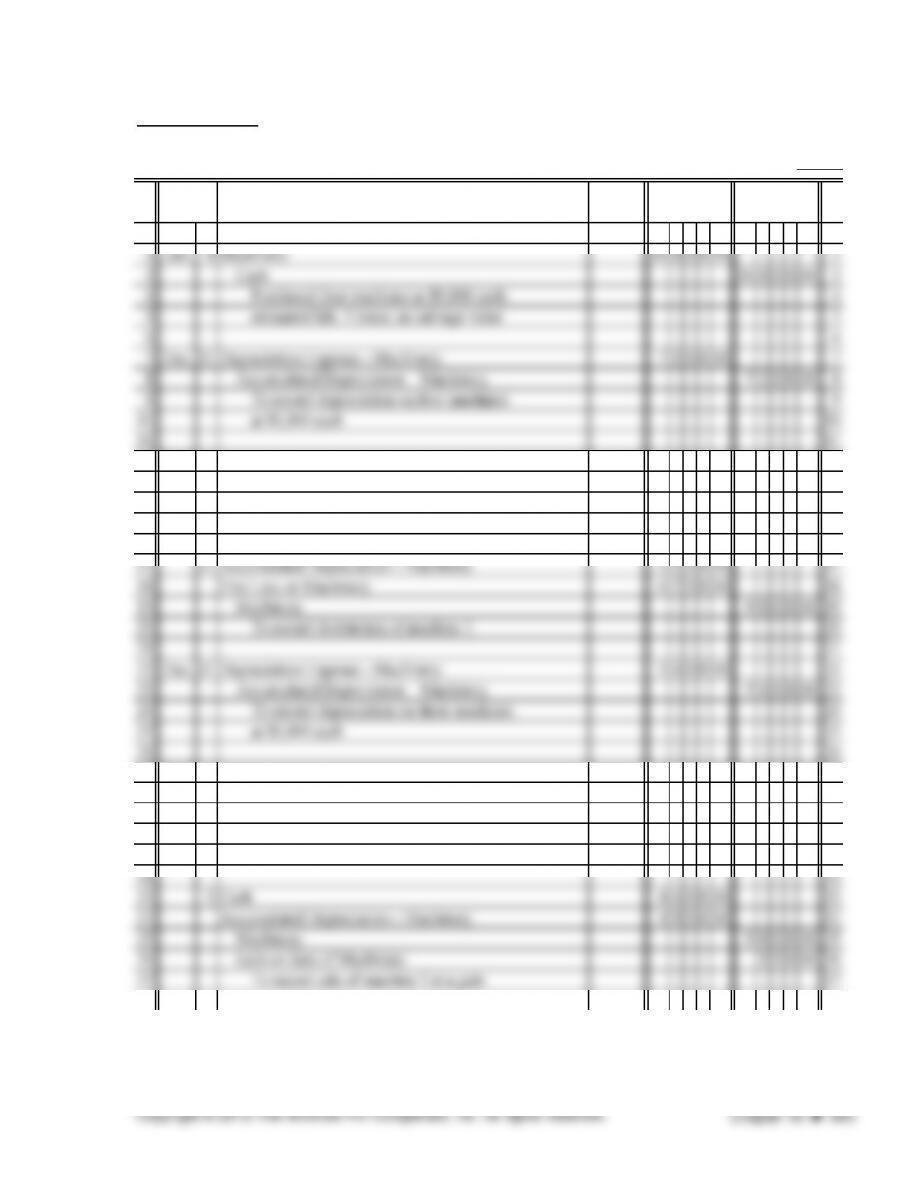

38 Case B: Unit is sold for $10,200 38

39 23 Cash 1020000 39

GENERAL JOURNAL 1

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 18.6B

PAGE

POST.

REF.

1 2013 1

12 2014 12

13 Mar. 31 Depreciation Expense—Machinery 45000 13

14 Accumulated Depreciation—Machinery 45000 14

15 Three months’ depreciation on destroyed machine 15

16 16

27 2015 27

28 Oct. 2 Depreciation Expense—Machinery 135000 28

29 Accumulated Depreciation—Machinery 135000 29

30 To record depreciation for nine months for 30

31 machine 2, which was sold 31

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

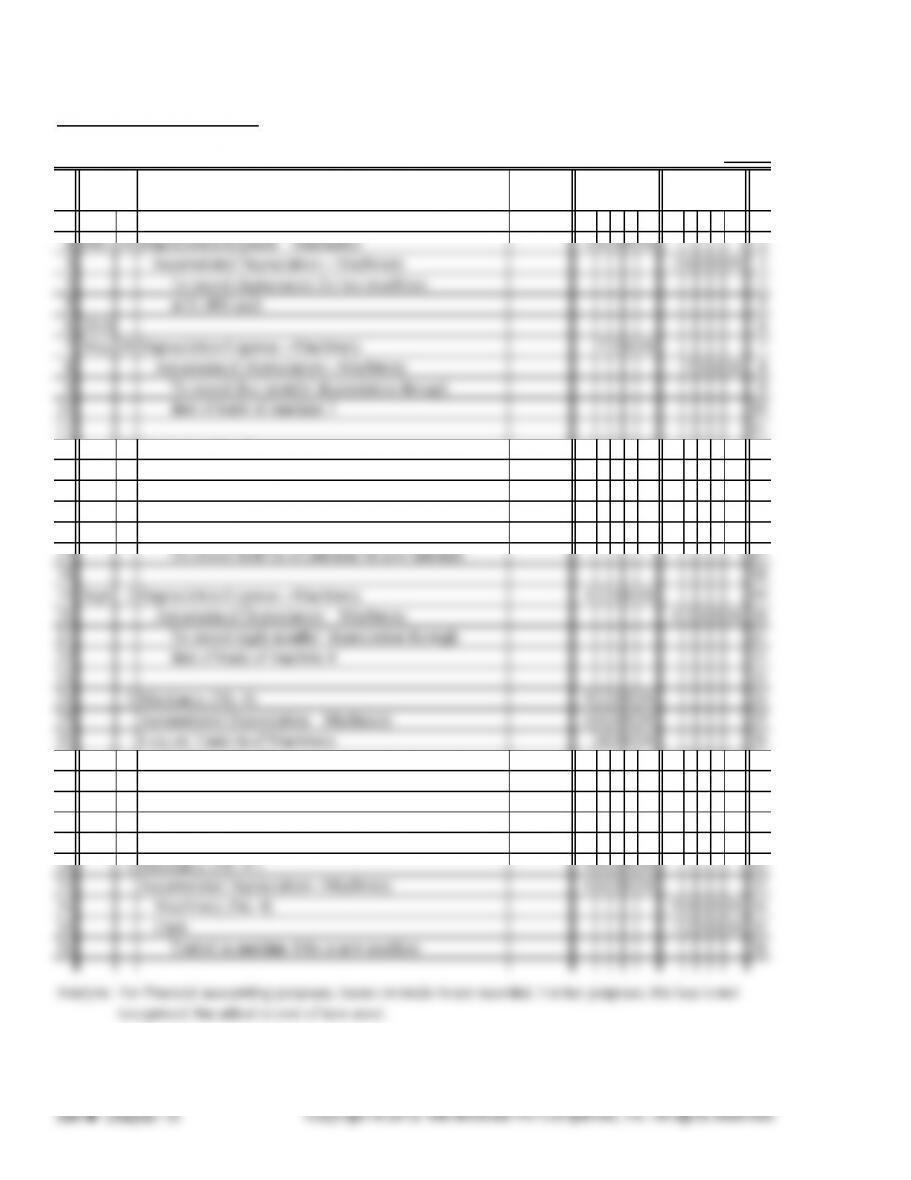

PROBLEM 18.6B (continued)

PAGE

POST.

REF.

1 2015 1

12 28 Machinery (No. 5) 880000 12

13 Accumulated Depreciation—Machinery 615000 13

14 Loss on Trade-In of Machinery 5 0 00 14

15 Machinery (No. 3) 900000 15

16 Cash 600000 16

27 Machinery (No. 4) 900000 27

28 Cash 720000 28

29 Traded in machine 4 for a new machine 29

30 30

31 Income Tax Method: 31

GENERAL JOURNAL

DATE DESCRIPTION DEBIT CREDIT

PROBLEM 18.7B

1. Depletion for financial accounting purposes.

2013: $900,000 ÷ 1,000,000 barrels = $.90 per barrel

2. a. Cost depletion for tax purposes in 2013 would be same as for financial accounting, $3,600.00

b. The company could deduct $3,600 of depletion on its 2013 tax return.

Cost depletion = $3,600 as computed above.

Percentage depletion in 2013 would be $800:

Sales $160,000 × 0.15 = $24,000,

e. $720,000 ($4,800,000 × .15) Percentage depletion can continue to be taken even though the total

amount of percentage depletion may be many times greater then the cost of the minerals.

PROBLEM 18.8B

1. The steps in assessing and measuring impairment have been taken: (1) There have been

indications that impairment may exist. (2) An examination has been made that shows that

3. The necessary entry would be to debit Impairment of Aircraft or some similar account and

Analyze: An examination should be made to determine whether the planes currently used are

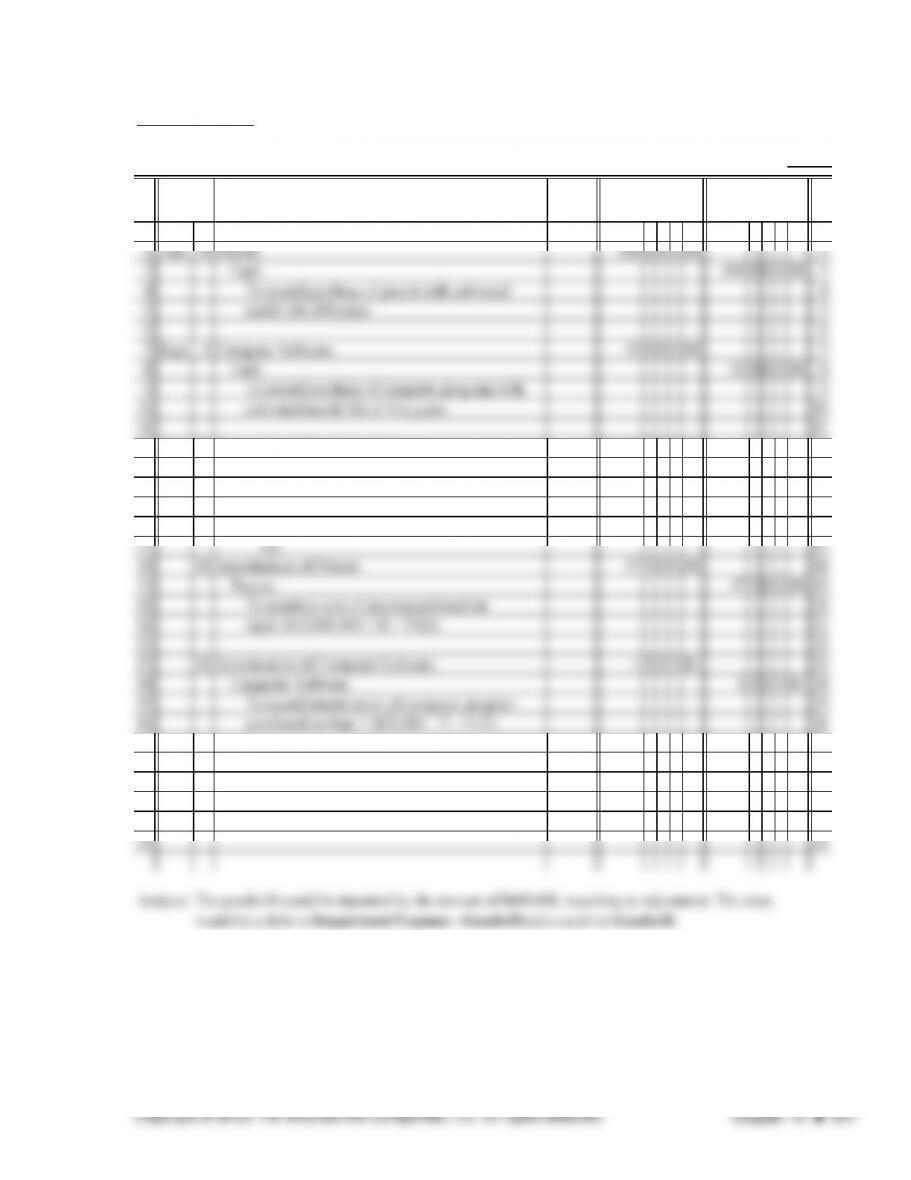

PROBLEM 18.9B

PAGE

POST.

REF.

12013 (1) 1

12 Dec. 31 Research and Development Expenses 3,000 00000 12

13 Cash 3,000 00000 13

14 To record expenditures in R&D 14

15 activities for year 15

16 16

27 27

28 (3) 28

29 Note Goodwill is not amortized. No entry is required 29

30 if an assessment has been made that there 30

31 is no impairment of the balance in the account. 31

GENERAL JOURNAL 25

DATE DESCRIPTION DEBIT CREDIT

CRITICAL THINKING PROBLEM 18.1

1. There are no rigid requirements that a business use any specific depreciation method for financial

accounting purposes. The method used must be “generally acceptable.” The usual methods are

2. Depreciation for financial accounting purposes may (and usually does) differ materially from the

“cost recovery” deducted under the Internal Revenue’s MACRS cost recovery system, which is

used instead of the traditional depreciation methods. This is because financial accounting strives

to match costs of an asset with the revenues the asset generates, to the extent possible.

3. The entity will deduct smaller amounts of MACRS as the assets get older. This means that if all

other factors were constant, income taxes would get higher as the assets get older. The result

4. Essentially, management is responsible for the choice of depreciation methods. Usually the chief

accounting officer and the chief financial officer are the critical players. In the case of firms

using outside auditors, the auditors may also play a key role.

CRITICAL THINKING PROBLEM 18.2

PAGE

POST.

REF.

1 2014 (Instruction 1) 1

10 the straight-line depreciation 10

11 11

12 31 Depreciation Expense—Sidewalks and Parking 130000 12

13 Accumulated Depreciation—Sidewalks and Parking 130000 13

2. a. (Furniture and fixtures are in the MACRS 7-year cost recovery class.)

2014: MACRS cost recovery for 2014 = $72,000 × 14.29% = $10,289

3. There is strong indication that the asset may be impaired. A development (investigation for possible

contamination because of existence of an old dump site) and the decline in business may suggest that

GENERAL JOURNAL 25

DATE DESCRIPTION DEBIT CREDIT

CRITICAL THINKING PROBLEM 18.2 (continued)

4. No. Unit-of-output depreciation is appropriate only where the asset’s useful life is affected directly by

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

2. Locking assets securely, assigning ID numbers, assign responsibility of asset to a person.

3. Recording assets at historical cost makes it easy to track the assets. Historical costs must be kept

for many purposes, such as for federal income tax purposes.

Ethical Dilemma:

It is an ethical transaction and the $100,000 would be included as Goodwill for Mr. Lopez. As long

Financial Statement Analysis:

Teamwork:

If the team has selected a machine, units of production would be the best method with a small

salvage value. For a building, straight-line would be best with a larger salvage value. Doubling the

Internet Connection:

The MACRS percent column for each year of the asset should be identical to the textbook. The

Part A True-False

1. FALSE 11. FALSE

3. TRUE 13. FALSE

5. TRUE 15. FALSE

7. TRUE 17. TRUE

9. TRUE 19. FALSE

10. TRUE 20. FALSE

Part B Matching

1. i

3. g

5. f

7. j

9. e

Part C Exercise

1. Depreciation for 2013 = ($44,000 – $4,000) ÷ 8 years = $5,000

Depreciation for 2014 = ($44,000 – $4,000) ÷ 8 years = $5,000

SOLUTIONS TO PRACTICE TEST