• The Best Buy family of brands and partnerships collectively generates more than $45 billion in

annual revenue and includes brands such as Best Buy; Audiovisions; The Carphone Warehouse;

Future Shop; Geek Squad, Jiangsu Five Star; Magnolia Audio Video; Napster; Pacific Sales; and

The Phone House.

• Best Buy employs more than 155,000 associates worldwide.

• Best Buy donated a combined $33.4 million in fiscal 2009 to improve the vitality of the

communities where its employees and customers live and work.

• Net sales were $49.6 billion in 2010.

1. Similar items are grouped, then computed at their cost and their market values. The lower of total

2. The item-by-item method should almost always yield the lowest value.

4. The cost flows used in valuing inventories are not intended to reflect actual physical flow of

5. Detailed records are kept of all factors affecting the selling price of merchandise available for sale.

6. Goods destroyed by fire or stolen; a quick estimate is needed for planning.

7. The goal is to provide physical protection of inventory at all times. Keeping accurate records of

Discussion Questions

Chapter Opener: Thinking Critically

MERCHANDISE INVENTORY

CHAPTER 17

Students should realize that In-Store Pickup provides Best Buy with merchandising data. The company

can generate reports on which products are in high demand in different geographic areas, improving

product selection in each store location.

Fast Facts

Managerial Implications: Thinking Critically

periodic physical count.

Neither. The gross profit and retail methods are intended as supplements, not replacements, for the

Discussion Questions (continued)

10. No. A physical count of inventory should be made at least once a year to verify accuracy of

perpetual records.

12. If there are few items in the inventory, each with significant cost and an individual identifying part

number or serial number, specific identification is logical.

14. The first in, first out assumption is that (for costing purposes only) the costs of merchandise should

15. Market is the current cost of acquiring identical items on the open market in normal quantities

purchased.

EXERCISE 17.1

Description

Number of

Units Unit Cost Total Cost

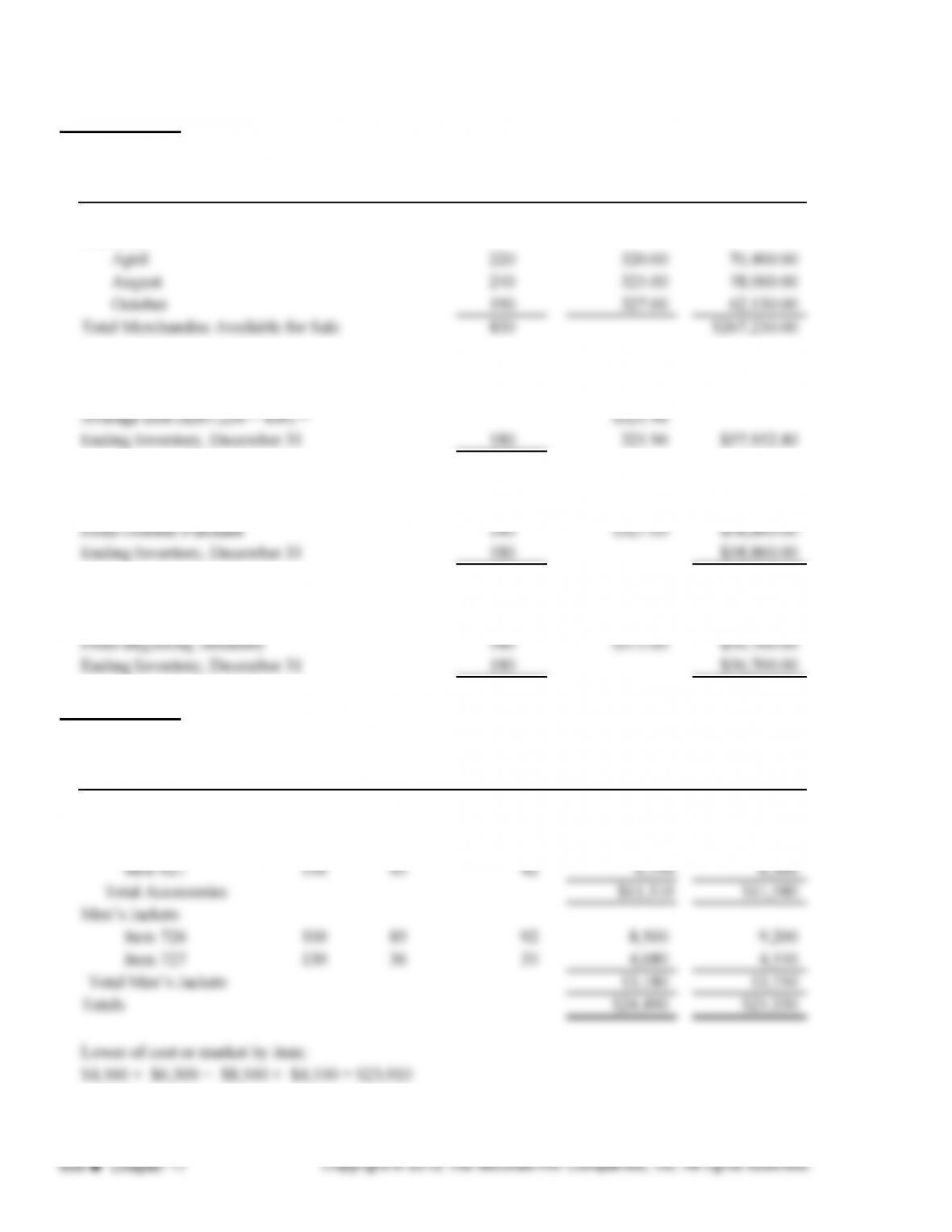

Beginning Inventory, January 1 180 $315.00 $56,700.00

Purchases:

1. Average Cost Method

2. FIFO Method

3. LIFO Method

EXERCISE 17.2

Description Quantity Unit Cost Market Value Total Cost Total Market

1. Item by Item

Accessories

240 $19 $22 $4,560 $5,280

Item 620

EXERCISE 17.2 (continued)

2. Total Cost or Total Market Value of Ending Inventory

3. By Groups

EXERCISE 17.3

EXERCISE 17.4

Beginning Inventory, January 1

$220,000

PROBLEM 17.1A

Description Number of Units Unit Cost Total Cost

Beginning Inventory, January 1 90 $103.00 $9,270.00

Purchases:

January 6 60 102.00 $6,120.00

a. Average Cost Method

b. FIFO Method

From January 22 Purchase 35 $96.00 $3,360.00

c. LIFO Method

From Beginning Inventory 88 $103.00 $9,064.00

PROBLEM 17.2A

1.

Description Number of Units Unit Cost Total Cost

Beginning Inventory, January 1 170 $107.00 $18,190.00

PROBLEM 17.2A (continued)

Description

Number of

Units Unit Cost

Inventory

Valuation

Cost Of

Goods Sold

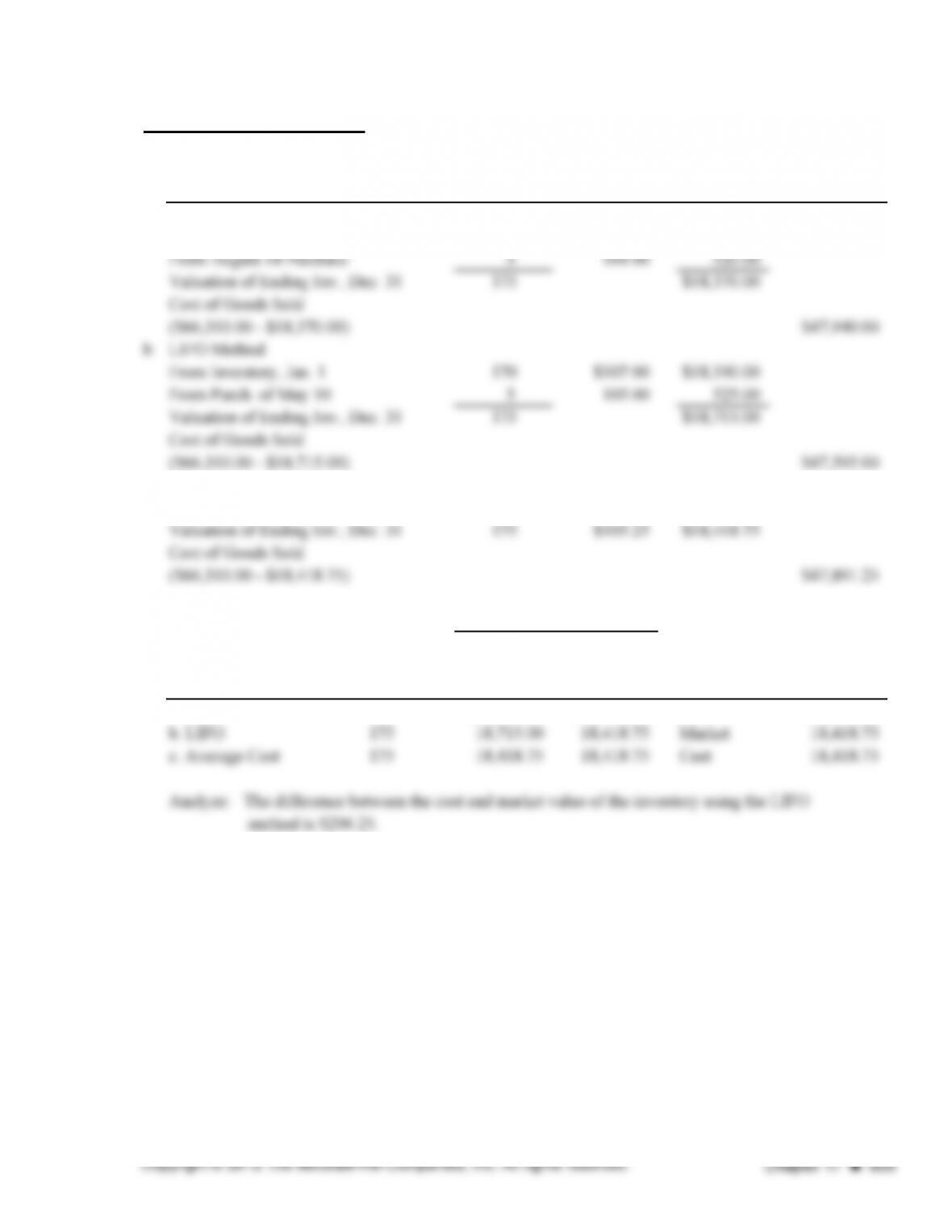

a. FIFO Method

From October 1 Purchase 170 $105.00 $17,850.00

c. Average Cost Method

Avg. cost per unit ($66,310.00 ÷ 630) $105.25

2.

Lower of

Cost

or Market

a. FIFO 175 $18,370.00 $18,418.75 Cost $18,370.00

Valuation Based on:

Method

Number of

Units Cost Market

Valuation

Basis

PROBLEM 17.3A

Description Quantity Unit Cost

Market

Value Total Cost

Total

Market

Lower of

Cost or

Market

Printer Cartridges

Item 119 50 $16.00 $16.50 $800.00 $825.00 $800.00

Item 120 60 17.25 17.10 1,035.00 1,026.00 1,026.00

Item 121 90 23.00 23.50 2,070.00 2,115.00 2,070.00

Total Cartridges $3,905.00 $3,966.00 $3,896.00

Fax Machines

Item 210 15 $86.00 $89.00 $1,290.00 $1,335.00 $1,290.00

Item 211 10 192.00 186.00 1,920.00 1,860.00 1,860.00

Item 212 9 225.00 210.00 2,025.00 1,890.00 1,890.00

Total Fax Machines $5,235.00 $5,085.00 $5,040.00

Grand Totals $9,140.00 $9,051.00 $8,936.00

Inventory Valuations Lower of Cost or Market

1. Lower of cost or market by individual items

2. Lower of total cost or total market

3. Lower of total cost or total market by groups

Total inventory by groups

Analyze: The valuation method that will yield the highest net income is the lower of cost or market by total.

$8,990.00

$8,936.00

$9,051.00

$3,905.00

5,085.00

PROBLEM 17.4A

Beginning Inventory, January 1, 2013 $117,000.00

Purchases 1,170,000.00

PROBLEM 17.5A

Estimated Inventory Cost Retail

Beginning Inventory, August 1 $115,000.00

$80,000

PROBLEM 17.6A (continued)

2. Cost of items still on hand in ending inventory on August 31:

Item

28 ft. Starfish

3. Cost of Goods Sold during August:

30 ft. Holiday

PROBLEM 17.1B

Description Number of Units Unit Cost Total Cost

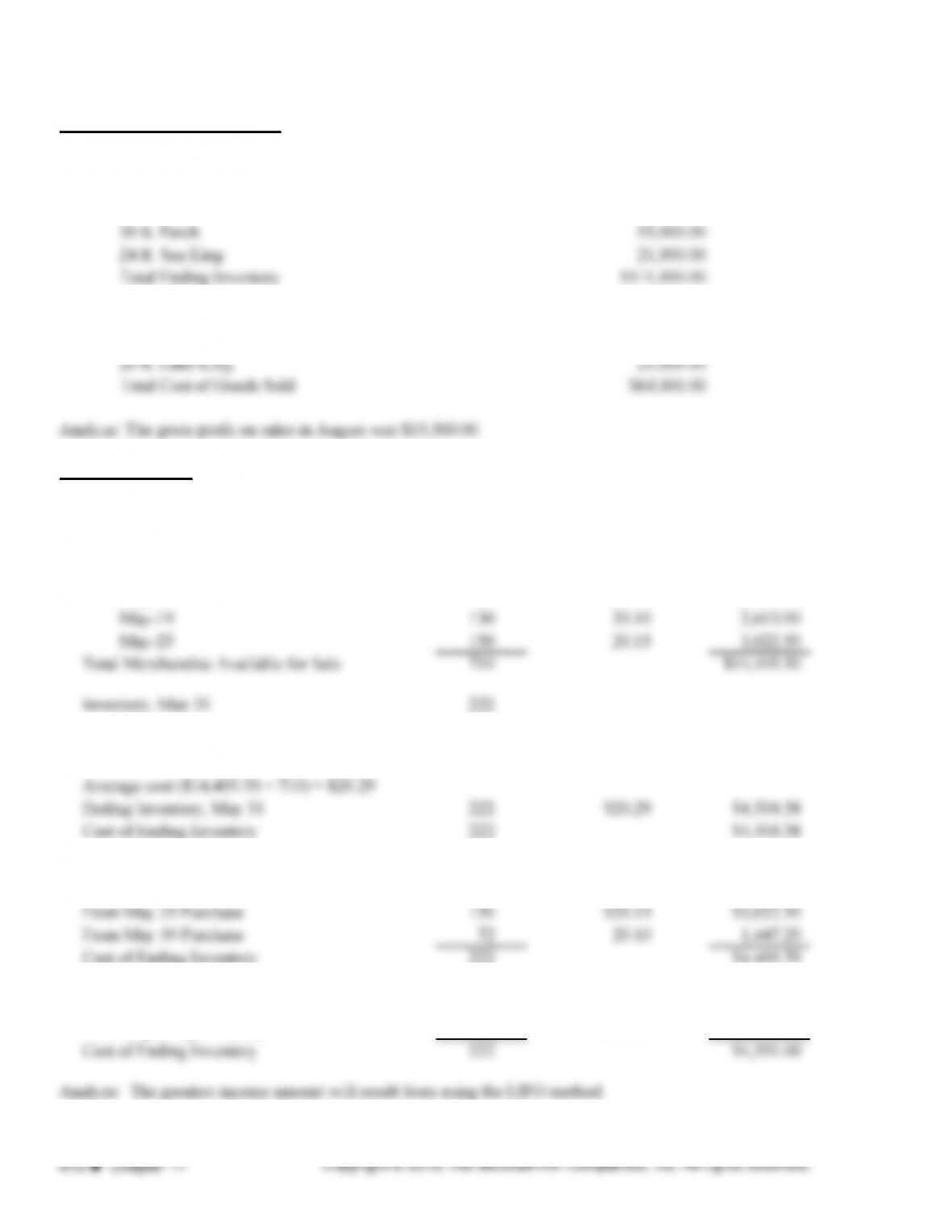

Beginning Inventory, May 1 250 $20.50 $5,125.00

Purchases:

May-10 180 20.25 $3,645.00

a. Average Cost Method

b. FIFO Method

c. LIFO Method

From Beginning Inventory 222 $20.50 $4,551.00

$41,000.00

Cost

$35,000.00

PROBLEM 17.2B

1.

Description Number of Units Unit Cost Total Cost

20 $2,580.00 $51,600.00

Description Unit Cost

Ending

Inventory

Cost

Cost Of

Goods Sold

a. FIFO Method

From November 19 Purchase $2,425.00 $38,800.00

Cost of Goods Sold:

($182,980.00 − $38,800.00) $144,180.00

2.

Number

of

Lower of

Cost

Method Units or Market

a. FIFO 16 $38,640.00 Market $38,640.00

Analyze: Because the market cost is used for both the LIFO and FIFO, they will show

same gross incomes. Both show a higher ending inventory than the average cost method, so

their gross incomes are higher.

$38,800.00

Valuation Based on:

Beginning Inventory, January 1

Number

of Units

Purchases:

Cost Market

Valuation

Basis

16

PROBLEM 17.3B

Description Quantity Unit Cost Market Value Total Cost Total Market

Lower of

Cost or

Market

Motor Bike Department

Model 705 15 $9,800.00 $9,675.00 $147,000.00 $145,125.00 $145,125.00

Model 766 25 10,250.00 11,390.00 256,250.00 284,750.00 256,250.00

Model 815 12 12,475.00 12,800.00 149,700.00 153,600.00 149,700.00

Total Motor Bikes $552,950.00 $583,475.00 $551,075.00

Boat Department

Model BX12 8 $5,290.00 $5,395.00 $42,320.00 $43,160.00 $42,320.00

Model BX14 7 7,125.00 6,980.00 49,875.00 48,860.00 48,860.00

Model BX16 6 5,100.00 5,325.00 30,600.00 31,950.00 30,600.00

Total Boats $122,795.00 $123,970.00 $121,780.00

Grand Totals $675,745.00 $707,445.00 $672,855.00

Inventory Valuations

1. Lower of cost or market by individual items

2. Lower of total cost or total market

3. Lower of total cost or total market by groups

Motor Bikes

Boats

Total inventory by groups

Analyze: The lower of total cost or total market method yields the same inventory valuation as the lower of cost or

market by group. Both of these would yield higher income than lower of cost or market by individual items.

$672,855.00

Lower of Cost or Market

$675,745.00

$552,950.00

122,795.00

$675,745.00

PROBLEM 17.4B

Beginning Inventory, January 1, 2013

Purchases

PROBLEM 17.5B

Estimated Inventory Cost

Beginning Inventory, April 1

1. Ending Inventory at Retail

2. Ending Inventory, April 30, at Cost

PROBLEM 17.6B

1. Specific identification. Each item is easily identified and has high value.

575,717

$866,000

$ 410,000.00

4,160,000.00

$918,000

$1,340,000

Retail

PROBLEM 17.6B (continued)

2. Cost of items still on hand in ending inventory:

Item Cost

Unit #06-92 $ 790,000.00

3. Cost of Goods Sold during August:

Unit #06-94 $ 873,000.00

Unit #06-95 1,900,000.00

CRITICAL THINKING PROBLEM 17.1

Estimated Inventory Retail

Beginning Inventory, January 1 $80,000.00 $107,560.00

Purchases, January 1–March 18 240,000.00 320,500.00

Freight in 8,200.00

Because the accounting records have been preserved, the retail inventory method may be used to

estimate the inventory destroyed in the fire. The approximate cost is $59,848.60 computed as

CRITICAL THINKING PROBLEM 17.2

The gross profit method may be employed. By examining the income statement for the past few years,

the rate of gross profit on sales and the percentage of cost of goods sold to sales can be determined for

those years. This rate can be applied to sales for the period from the first of the year to the date of the

fire to estimate cost of goods sold for that period. The cost of goods available for sale during the

period is available from records of beginning inventory, purchases, purchase returns and allowances,

freight in, etc. By subtracting the estimated cost of goods sold for the period from the cost of goods

available for sale, the estimated cost of ending inventory (inventory destroyed by the fire) can be

estimated.

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

2.

4.

6.

Ethical Dilemma:

Use the retail method to estimate inventory cost.

May perceive that the perpetual inventory system will require too much record keeping

and paperwork.

If strong inventory control systems are in place, the manager is probably correct. A

Nancy has been giving away baby clothes to her friends, thus reducing the inventory. No sales

Part A True-False

2. TRUE

4. FALSE

6. TRUE

8. TRUE

10. TRUE

12. FALSE

Part B Matching

1. d (markdown)

5. g (specific identification)

SOLUTIONS TO PRACTICE TEST