Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

•

Americans drink an average of 2.6 cups of coffee per day.

• Green Mountain Coffee Roasters (GMCR) maintains two business units: the Specialty Coffee Business

Unit (Green Mountain Coffee® and Tully’s Coffee® brands) and the Keurig Business Unit which

produces single-serve coffee makers.

• The Company employs over 1,400 employees.

• The Company delivered double-digit net sales growth for 27 consecutive quarters.

• An investment of $100 in GMCR stock in September of 2004 was worth over $1,400 in 2010.

• Net income—low income could be due to accelerated depreciation on new assets.

• Assets—low asset value could be due to low historical cost, while the asset’s current market value may be

much higher.

1. The Securities and Exchange Commission and Financial Accounting Standards Board.

3. Any U.S. company with foreign-based operations will have to prepare statements under IFRS.

5. Comparability means that statements of one entity may be compared meaningfully with those of another

entity.

7. If the entity were not a going concern, showing an asset’s cost would be useless. If the entity is about to

8. In accounting for items that are not material, there may be justification for simply ignoring GAAP. This is

especially true when there are high costs associated with complying rigidly with GAAP.

9. If an item is immaterial, there is less justification for incurring substantial costs to comply with GAAP

regarding the item. The cost of compliance may outweigh the benefits. If an item is highly material, then

Discussion Questions

CHAPTER 14

ACCOUNTING PRINCIPLES AND REPORTING STANDARDS

Chapter Opener: Thinking Critically

The amount of revenue reported will change depending upon the method in which it is reported. Financial

statement users compare results to prior years. This comparison will be distorted and users misled if the change

in method is not disclosed.

Fast Facts

Managerial Implications: Thinking Critically

Discussion Questions (continued)

10.

The periodicity assumption is that income can and will be measured for accounting periods such as

a year or a quarter.

12. The concepts of conservatism and usefulness warrant the practice. In this case, the cost principle

becomes far less important.

13. Full disclosure is the concept that all facts that would, if disclosed, affect the statement user’s

interpretation of the statements should be disclosed. Full disclosure is a key principle in the eyes of

15. For revenues to be recognized, they must have been earned and they must have been realized.

EXERCISE 14.1

1.

2.

3.

EXERCISE 14.2

1.

He should report no income from the land. Under the realization principle, no revenue should be

HER should report no income from the project in 2013. The matching principle requires that

$200. The accounting principle of matching costs with revenues requires that only that part of the

The separate entity assumption applies here. Under this assumption, Wong’s business and personal

EXERCISE 14.3

1. This is correct accounting. The historical code principle requires that assets should be recorded at cost. In

2. This is correct accounting. The historical cost principle, the matching principle and the going-concern

assumption are all important. Assets should be recorded at cost. The machine will contribute to the

3. This is correct accounting. The matching principle calls for matching revenue and related expenses in the

same year. Since some part of sales of the current period are not expected to be collected, the resulting loss

should be recorded in the current year in order to match expenses with revenues in the same accounting

period. Also, conservatism requires that accounts receivable should not be overstated.

EXERCISE 14.4

1. Objectivity is the key factor. Under GAAP, expenses are recognized as soon as they occur if there is a

2. Materiality and consistency are important considerations. The amount of $3,500 is not material when

compared to net income of about $2.0 million. If the company follows this practice from year to year, the

3. Objectivity is the key factor. GAAP holds that expenditures should be expensed if they cannot be shown

objectively to benefit future operations. It would be very difficult to determine objectively the portion of

EXERCISE 14.5

EXERCISE 14.6

PROBLEM 14.1A

1. True

10. True

PROBLEM 14.2A

Proper Presentation

1. The personal money-market account

of the owner should not be included

in the assets of the business because

it is assumed that a business is an

entity separate and apart from its

owner.

or be able to pay, her debt. It should

be charged off and matched against

current income.

Handled Properly? Basic Concept

No Separate entity

PROBLEM 14.3A

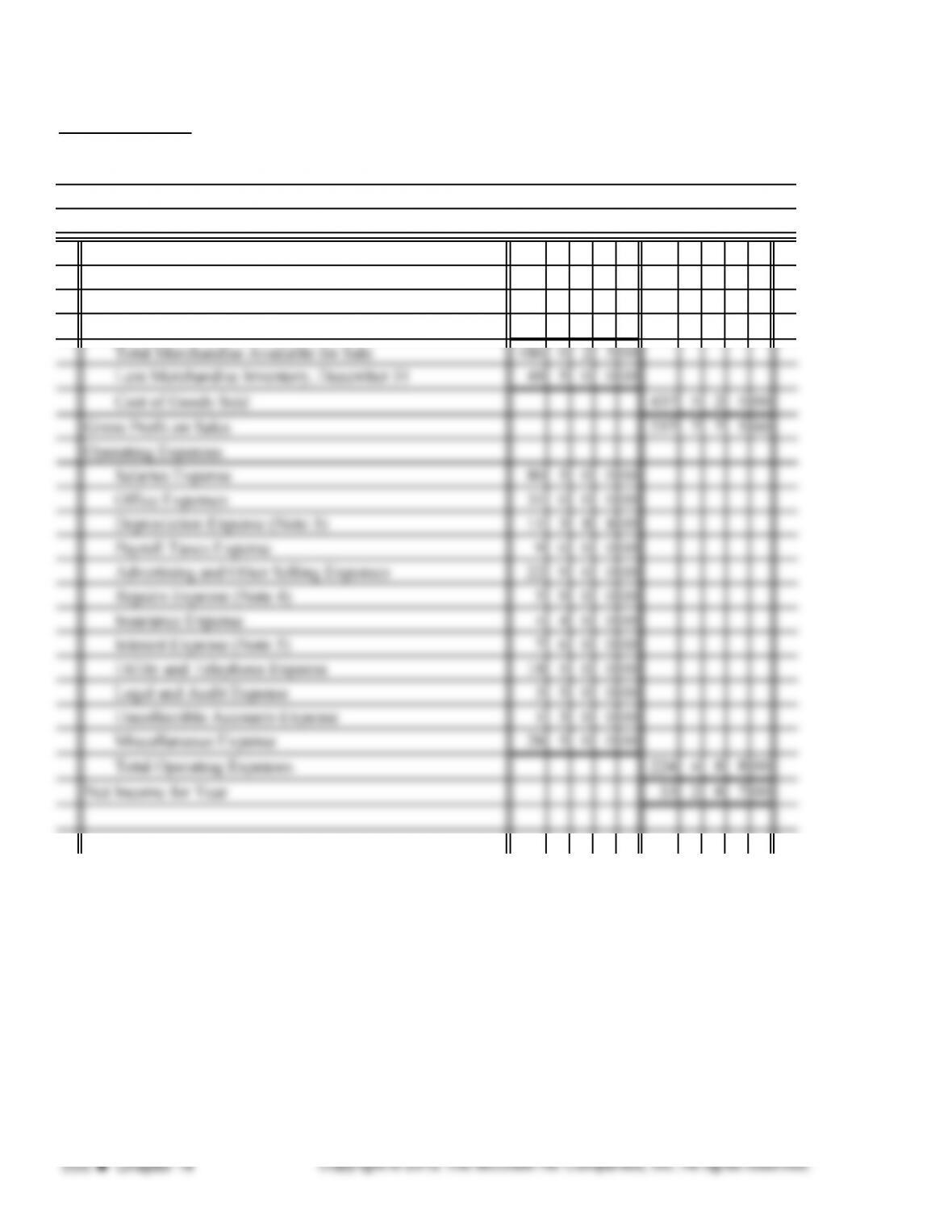

Sales (Note 1) 695 3 0 0 00

Cost of Goods Sold

Merchandise Inventory, January 1 44 8 0 0 00

Purchases (Note 2) 441 2 2 5 00

Cortez Video Center

Income Statement

Year Ended December 31, 2013

PROBLEM 14.3A (continued)

COMPUTATIONS

Note 1 : Computation of Sales:

Cash Receipts for Year $689,000

Accounts Receivable, December 31 33,000

PROBLEM 14.4A

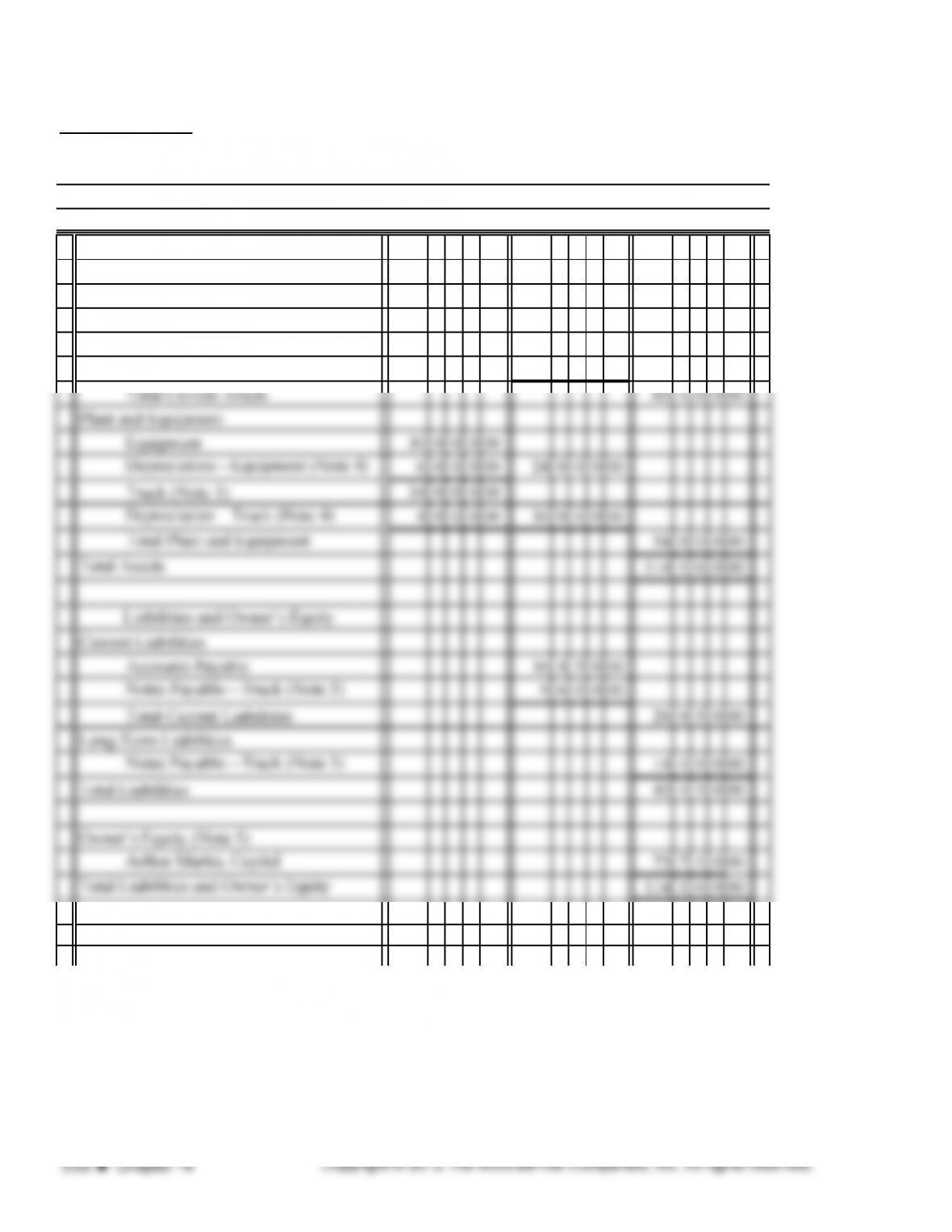

10 2 0 0 00

16 0 0 0 00

206000

31 9 0 0 00

The Art Haven

Balance Sheet

December 31, 2013

Cash (Note 2)

Current Assets

Inventory (Note 1)

Accounts Receivable

Supplies

Assets

PROBLEM 14.4A (continued)

1. The inventory should be shown at cost under the cost principle and not at the selling price.

2. Under the separate entity assumption, the cash of the owner should not be shown with the cash of the

3. Although the truck is not paid for, it is an asset of the business and should be shown on the balance sheet

4. The equipment and truck should be shown at their original costs, less accumulated depreciation.

5. The owner’s personal residence, the family auto, notes payable on the family car, and the mortgage on the

house should not be shown on the balance sheet of the business under the separate entity concept. The

PROBLEM 14.5A

1. Violation of the matching concept. Assets are overstated and income for some years has been overstated.

The company should adopt the allowance method.

2. The approach used by the accountant is correct because of the matching principle. However, the owner

PROBLEM 14.1B

1. False

PROBLEM 14.2B

Proper Presentation

1. The personal auto of the owner should not be included on the

balance sheet of the business, since it is assumed that a business is

an entity separate from its owners.

Handled Properly? Basic Concept

No Separate

Entity

PROBLEM 14.3B

Sales (Note 1) 402 2 5 0 00

Cost of Goods Sold

Merchandise Inventory, January 1 36 0 0 0 00

Purchases (Note 2) 314 2 5 0 00

Total Merchandise Available for Sale 350 2 5 0 00

Less Merchandise Inventory, December 31 45 0 0 0 00

Cost of Goods Sold 305 2 5 0 00

Gross Profit on Sales 97 0 0 0 00

Vanessa’s Beauty Supplies

Income Statement

Year Ended December 31, 2013

PROBLEM 14.3B (continued)

COMPUTATIONS

Note 1 : Computation of Sales:

Cash Receipts for Year 407,000$

Accounts Receivable, December 31 25,250

Note 2 : Computation of Purchases:

Payments to Creditors 300,000$

Note 3: Computation of Salaries Expense

Note 4 : Computation of Depreciation Expense:

Store equipment

Note 5 : Computation of Repairs Expense:

Analyze: The permanent accounts affected would be: Accounts Receivable, Allowance for Doubtful

Accounts, Owner’s Capital, Store Equipment, Accumulated Depreciation—Store Equipment.

PROBLEM 14.4B

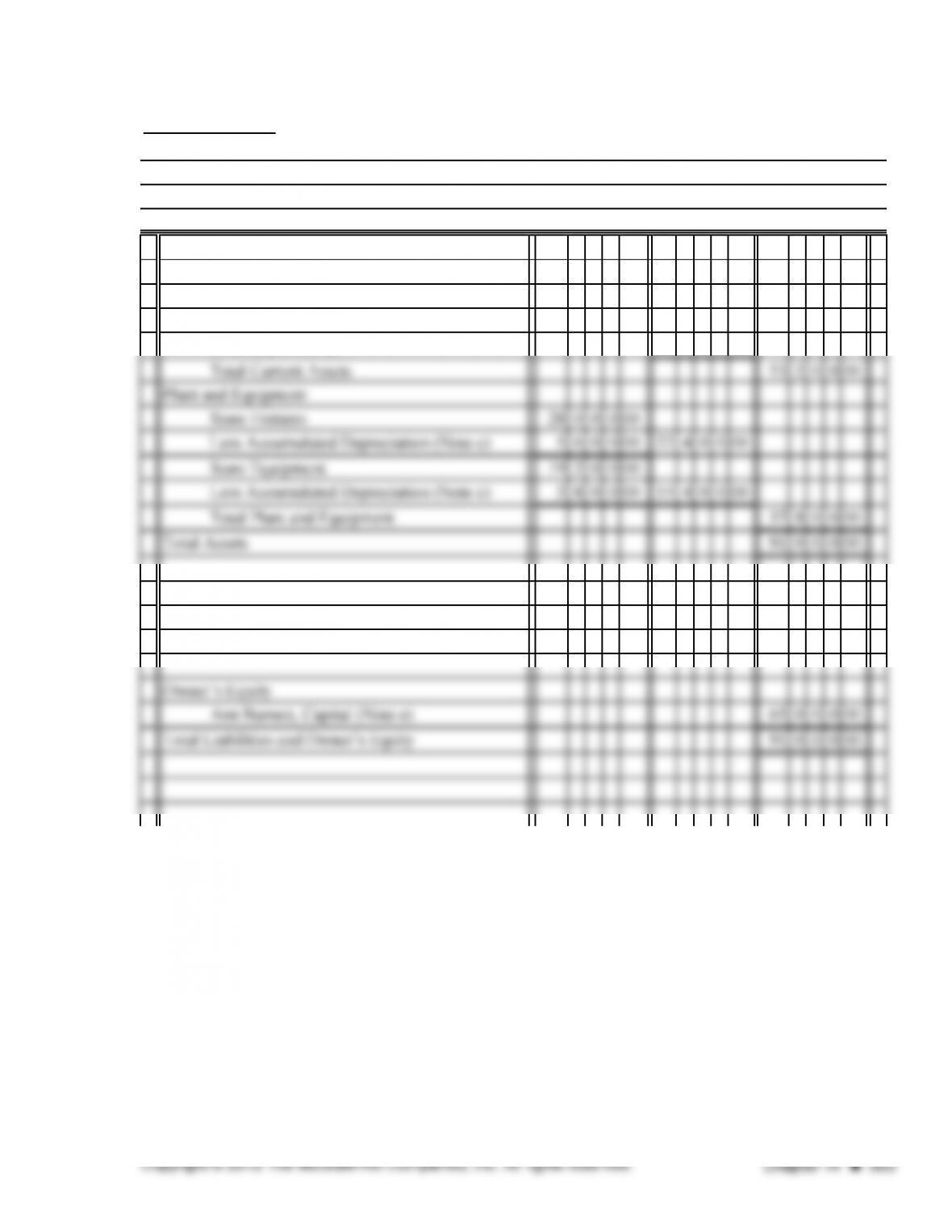

Current Assets

Cash (Note b) 11 0 0 0 00

Accounts Receivable 720000

Inventory (Note a) 35 0 0 0 00

Liabilities

Accounts Payable 26 0 0 0 00

Liabilities and Owner's Equity

City Kitchen—Country Cooks

Balance Sheet

December 31, 2013

Assets

PROBLEM 14.4B (continued)

a. The inventory should be shown at cost under the cost principle and not replacement cost. (As you will see

in Chapter 17, however, if replacement cost is less than actual cost, it may be appropriate to record the

asset at the replacement cost.)

PROBLEM 14.5B

1. No accounting entries are required that affect the amounts in the financial statements because no loss or

liability has been created. However, existence of the suit would be very important to the statement users,

so the full disclosure principle dictates that disclosure of the suit should be made in notes to the statements.

2. This procedure violates the cost principle and the realization concept. The parts should be recorded at their

Analyze: Yes. Based on the facts given, it would likely be appropriate to record the goodwill. The amount

paid for the other assets was their book values. The goodwill would be shown on the balance sheet as an

NOTES

CRITICAL THINKING PROBLEM 14.1

In this situation, it is very difficult to determine if there will be future benefit, and it is almost

impossible to measure those benefits. The matching principle requires that the contributions should

be charged to expense in the year made. This is not the same as a payment of $500,000 for an item

of equipment or a specific service or benefit, even though management may feel relatively sure

that construction of the new road will increase value of the property. In addition, the company

cannot be compelled to make the suggested contribution.

If, on the other hand, the local taxing authority imposes a tax to pay for the road, some would

argue that the special tax should be added to the cost of the land because of the almost certainty

that the land value will increase.

CRITICAL THINKING PROBLEM 14.2

1. This is appropriate under the matching concept. If no oil or gas is found, there are no future

benefits. If oil or gas is found, there are future benefits against which to match the costs.

2. This does not conform with GAAP. Under the realization principle, revenue should not be

3. There is no violation of generally accepted accounting principles in this case. Although the

5. This is inappropriate preparation of statements violating the principle of consistency. In order to

provide comparability between the statement, the period covered should be consistent for each

statement.

6.

The present approach used for the baskets conforms to GAAP. However, the concept of materiality

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

1. Personal judgment can be minimized but not completely eliminated. To aid in objectivity, consult

outside experts or use published guidelines.

3. If the entire entity is about to be sold, as in bankruptcy, or is being liquidated. (The assets will not

be used up in the normal course of business.)

4. To report income or loss, accountants must match revenues earned with costs incurred to earn

those revenues.

1. The statements are comparable in that you can compare these results with other companies in the

same industry. The account titles and presentation are very similar to other retail building supply

companies. The data is clearly understood. Merchandise Inventory is clearly identified, as are

other major areas of expenses. The assets and liabilities are also clearly labeled for comparison

Part A True-False

Part B Completion

1. consistency

15. Securities and Exchange Commission

16. stable monetary unit

Part C Exercise

1.

2.

assumptions, basic principles, and constraints.

SOLUTIONS TO PRACTICE TEST

No. The owner of a sole proprietorship is generally legally liable for the debts and other

obligations of the business as well as for personal debts.

ABC must use U.S. GAAP since it has not international reporting requirements.