PROBLEM 10.1B

1.

HOURS

WORKED

48

Gross Pay $660.40

Less:

Social Security Tax 40.94

2.

POST.

REF.

6 6

OVERTIME

EARNINGS

$152.40

GROSS

EARNINGS

$660.40

REGULAR

TIME

EARNINGS

REGULAR

HOURS,

HOURLY RATE

$508.00

EMPLOYEE

NO.

$12.70Jacob Sandoval

CREDITDATE DESCRIPTION DEBIT

GENERAL JOURNAL 18 PAGE

PROBLEM 10.1B (continued)

Analyze: Jacob earned overtime pay of $2,244.40, calculated as follows:

Cumulative earnings, prior to December 31 payroll $28,000.00

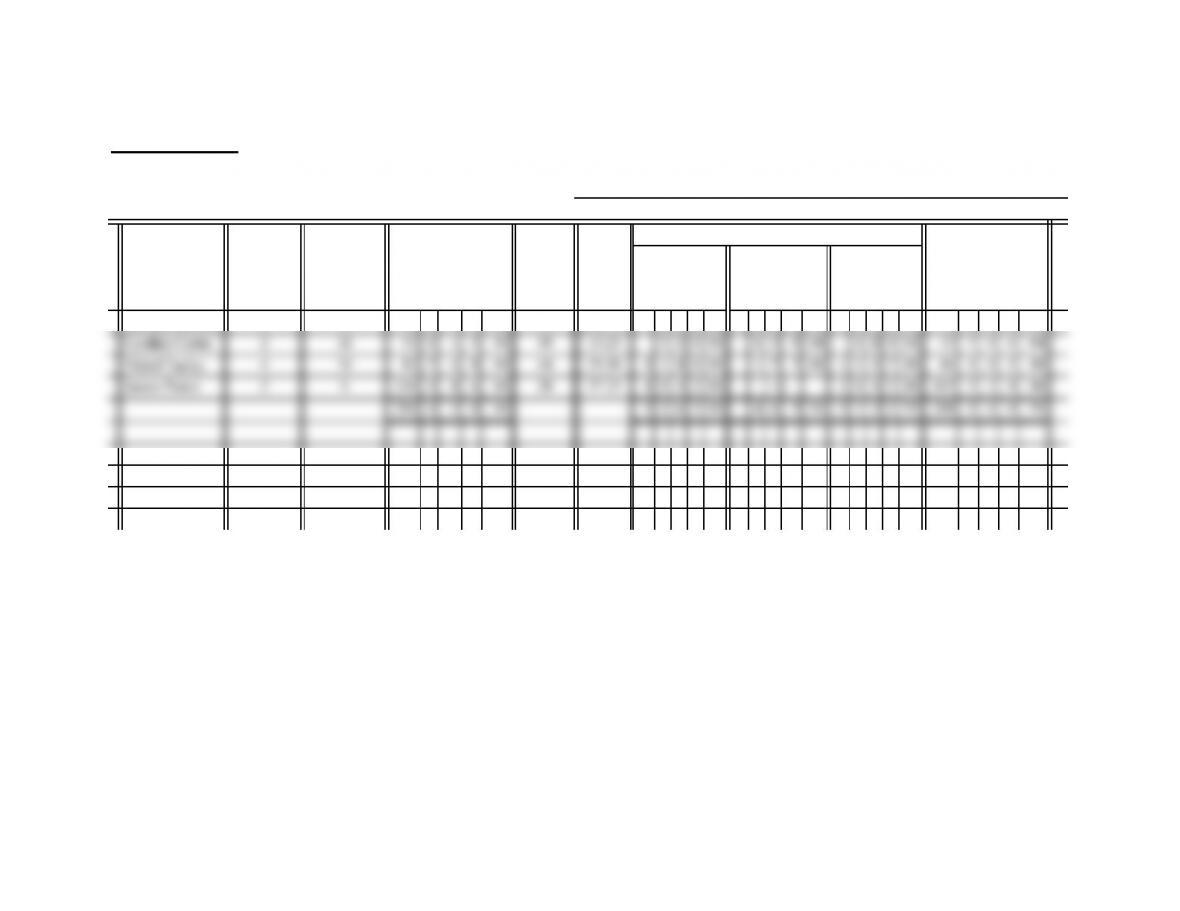

PROBLEM 10.2B

PAYROLL REGISTER WEEK BEGINNING

Barbara Brooks 3 M 44 1 7 9 00 47 $12.75 5 1 0 00 1 3 3 91 6 4 3 91 44 8 2 2 91

NO. OF

HRS. RATE

EARNINGS

CUMULATIVE

EARNINGS

REGULAR

TIME

EARNINGS

OVERTIME

EARNINGS

GROSS

AMOUNT

December 25, 2013

NAME

NO. OF

ALLOW.

MARITAL

STATUS

CUMULATIVE

EARNINGS

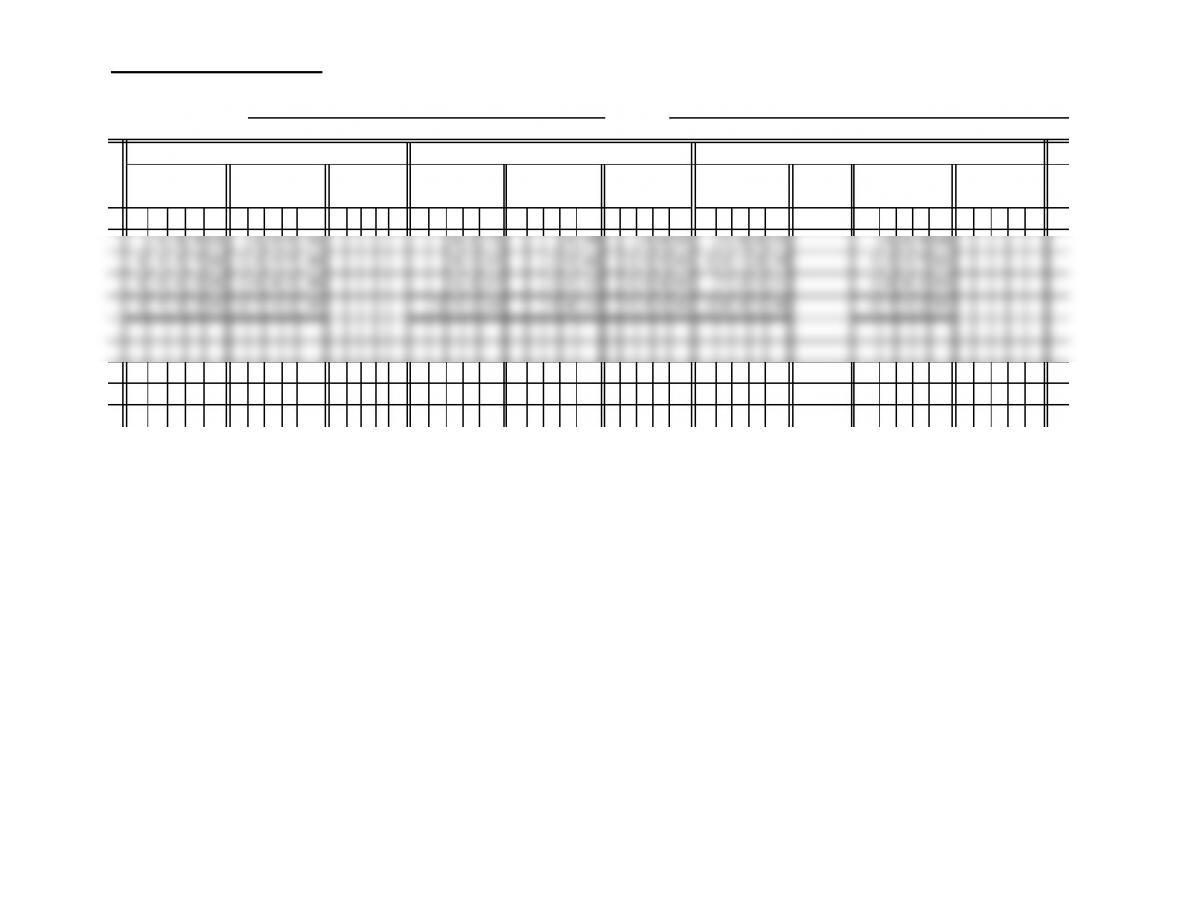

PROBLEM 10.2B (continued)

AND ENDING PAID

CHECK

NO.

6 4 3 91 6 4 3 91 3 9 92 9 34 3 3 00 5 6 1 65 6 4 3 91

December 31, 2013December 31, 2013

TAXABLE WAGES DEDUCTIONS DISTRIBUTION

INCOME

TAX

NET

AMOUNT

SOCIAL

SECURITY MEDICARE FUTA

OFFICE

WAGES

WAGES

EXPENSE

SOCIAL

SECURITY MEDICARE

PROBLEM 10.2B (continued)

POST.

REF.

1 2013 1

2 Dec. 31 3 7 3 2 95 2

3231 44 3

18

DATE DESCRIPTION DEBIT CREDIT

GENERAL JOURNAL PAGE

Wages Expense

Social Security Tax Payable

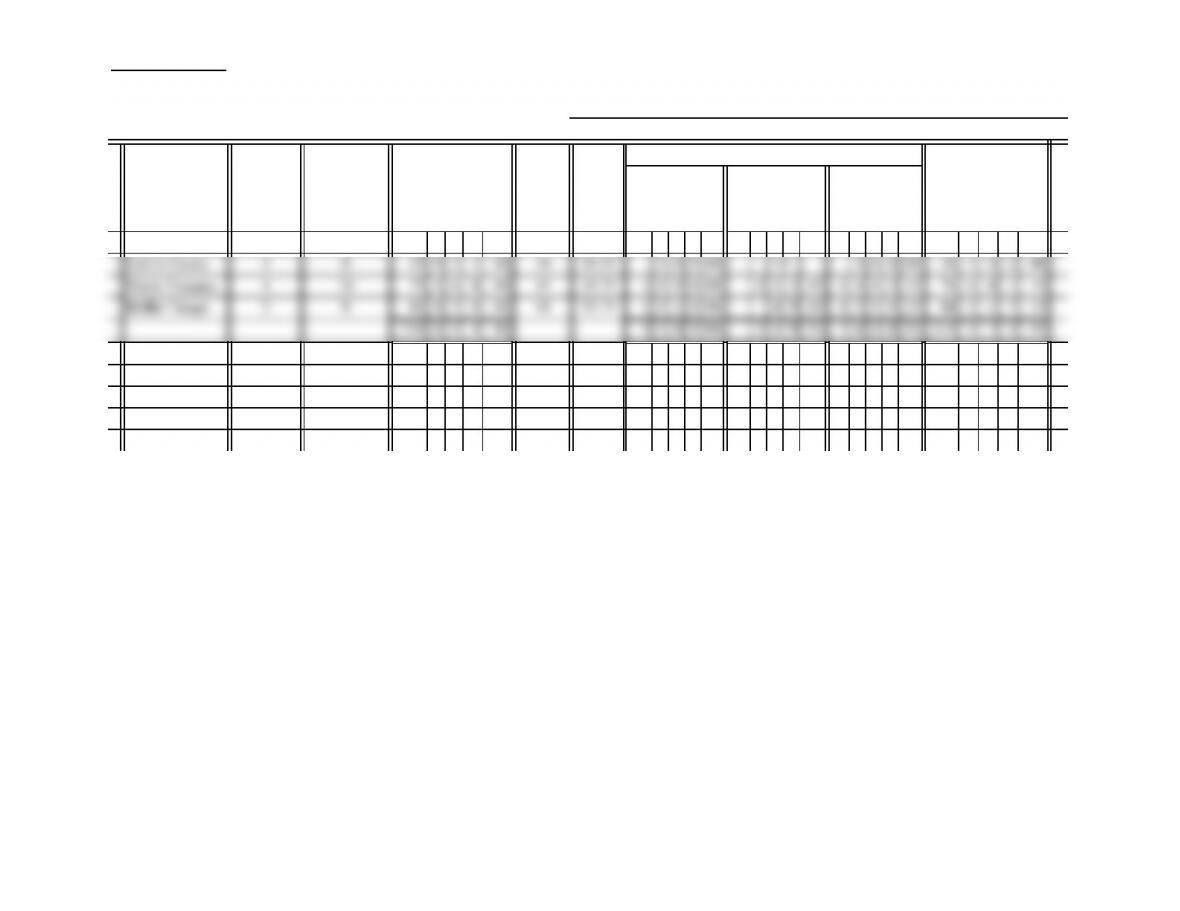

PROBLEM 10.3B

PAYROLL REGISTER WEEK BEGINNING

Kathryn Allen 3 M 26 5 6 5 00 43 10.50 4 2 0 00 4 7 25 4 6 7 25 27 0 3 2 25

CUMULATIVE

EARNINGS

REGULAR

TIME

EARNINGS

OVERTIME

EARNINGS

GROSS

AMOUNT

November 6, 2013

NAME

NO. OF

ALLOW.

MARITAL

STATUS

CUMULATIVE

EARNINGS

N

O. OF

HRS. RATE

EARNINGS

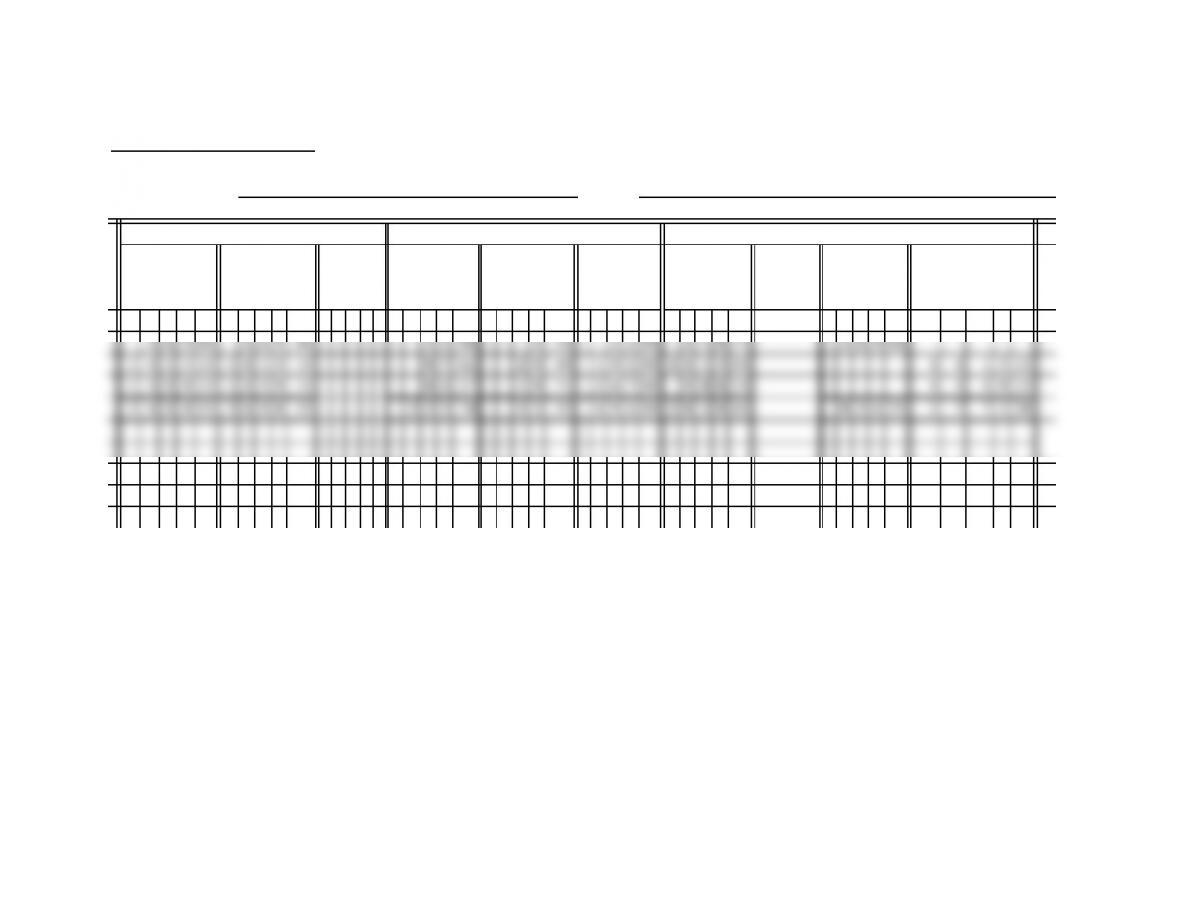

PROBLEM 10.3B (continued)

AND ENDING PAID

CHECK

NO.

4 6 7 25 4 6 7 25 2 8 97 6 78 1 3 00 4 1 8 50 4 6 7 25

TAXABLE WAGES DEDUCTIONS DISTRIBUTION

MEDICARE

SOCIAL

SECURITY MEDICARE FUTA

SOCIAL

SECURITY

INCOME

TAX

NET

AMOUNT

November 12, 2013 November 12, 2013

OFFICE

WAGES

CONSULTING

WAGES

PROBLEM 10.3B (continued)

POST.

REF.

1 2013 1

2 Nov. 12 8 3 6 25 2

32772283

422374 4

9 9

10 15 2 8 3 8 46 10

11 Cash 283846 11

12 12

13 13

14 14

Analyze: Total deductions of $770.07 were taken from employee paychecks for the period

ended November 12.

Wages Payable

Paid payroll

Office Wages

Social Security Tax Payable

Consulting Wages

32

DATE DESCRIPTION DEBIT CREDIT

PAGE

GENERAL JOURNAL

PROBLEM 10.4B

NET PAY

$12,629.00

$261.00

MEDICARE

CUMULATIVE

EARNINGS

EMPLOYEE

INCOME TAX

WITHHOLDING

$5,110

SOCIAL

SECURITYEMPLOYEE NAME.

MONTHLY

PAY

Tony Constantino $180,000 $18,000

CRITICAL THINKING PROBLEM 10.1

MONTHLY

PAY NET PAY

EMPLOYEE

INCOME

TAX WITH

HOLDING

MEDICARE

SOCIAL

SECURITY

EMPLOYEE NAME

CUMULATIVE

EARNINGS

1. Some of the weaknesses in Tito’s Tacos payroll system include:

a. Managers are able to add new employees to the payroll without written authorization or

verification. There is no check on the qualifications of employees hired and managers

2. Since there are no checks on who the managers hire, it would be possible for a manager to

3. To prevent fictitious employees from being placed on the payroll:

a. New employees should not be added to the payroll without written authorization from

SOLUTIONS TO BUSINESS CONNECTIONS

Managerial Focus:

2. Paying by check would eliminate security risk and reduce work involved in preparing pay envelopes.

3. Various federal, state, and local payroll laws require that detailed payroll records be

4. Used by management to see that operations meet previously established goals and that

related outlays for wages are within previously established limits.

2. Increased by $134 million.

Teamwork:

Employee signs the time card and gives it to the manager. The manager approves the hours and gives it to the

p

ayroll clerk. The payroll clerk runs the payroll and prints the checks. The treasurer signs the checks and gives

them back to the payroll clerk who gives them to the manager. The controller enters any necessary adjusting

entry. The manager gives the check to the employee.

Experience necessary is 3 out of 5 years preceding the date of the exam. Exam is offered in April and October

at several testing sites. The fee for the CPP exam for the period September 11, 2010 to October 9, 2011 is

$360. Testing includes: Core Payroll Concepts (27.5%), Compliance (23%), Principles of Paycheck

Calculations (20%), Payroll Process and Systems (8.5%), Management and Administration (15%) and

SOLUTIONS TO PRACTICE TEST

Part A True-False

1. FALSE

Part B Matching

1. a