• In 1990, Gary Erickson lived in a garage with his dog.

• In 2000, Clif Bar was nearly sold to Quaker Oats for $120 million—Erickson backed out of the deal when

he experienced panic attacks about the sale. The company has tripled in size since.

• Clif Bar currently has 230 employees and revenue of $150 million.

1. Earnings during the pay period, length of pay period, marital status, number of allowances.

3. Fair Labor Standards Act sets the minimum hourly rate of pay and maximum hours of work per week. It is

also referred to as the Wage and Hour Law.

5. Salaried employees who hold supervisory or managerial positions, not subject to maximum hours and

overtime.

7. No, levied on the employer only.

9. To provide medical care for the employee and the employee’s spouse after each has reached 65 years of

age.

11. Funds are automatically deposited in the employee’s account from the employer’s bank.

13. Withholding tables

15. One depends solely on the number of hours worked each week; the other is a fixed amount per month, per

week, or other pay period.

Note to instructor: These questions are designed to check students’ understanding of new concepts, and

procedures presented in the chapter.

Discussion Questions

Chapter Opener: Thinking Critically

PAYROLL COMPUTATIONS, RECORDS, AND PAYMENT

CHAPTER 10

Students might mention benefits like the company’s commitment to the environment and the appeal of a non-

traditional environment that boasts climbing walls and yoga classes.

Fast Facts

Managerial Implications: Thinking Critically

Answers will vary, but students may suggest payroll audits, monitoring of cards, and division of labor for

payroll tasks.

EXERCISE 10.1

EMPLOYEE

NO.

HOURLY

RATE

HOURS

WORKED

GROSS

EARNINGS

EXERCISE 10.2

HOURLY

RATE

OVERTIME

RATE

REGULAR

HOURS

WORKED

OVERTIME

HOURS

WORKED

REGULAR

PAY

OVERTIME

PAY

GROSS

PAY

EXERCISE 10.3

EMPLOYEE

NO.

DECEMBER

SALARY

YEAR TO DATE

EARNINGS

THROUGH

NOVEMBER 30

SOC. SEC.

TAXABLE

EARNINGS

DECEMBER

SOCIAL

SECURITY

TAX

6.20%

EXERCISE 10.4

MEDICARE

TAXABLE

EARNINGS-

DECEMBER

EMPLOYEE

NO.

DECEMBER

SALARY

MEDICARE

TAX 1.45%

EXERCISE 10.7

POST.

REF.

1 2013 1

2 July 31 30 5 5 8 46 2

38041543

20

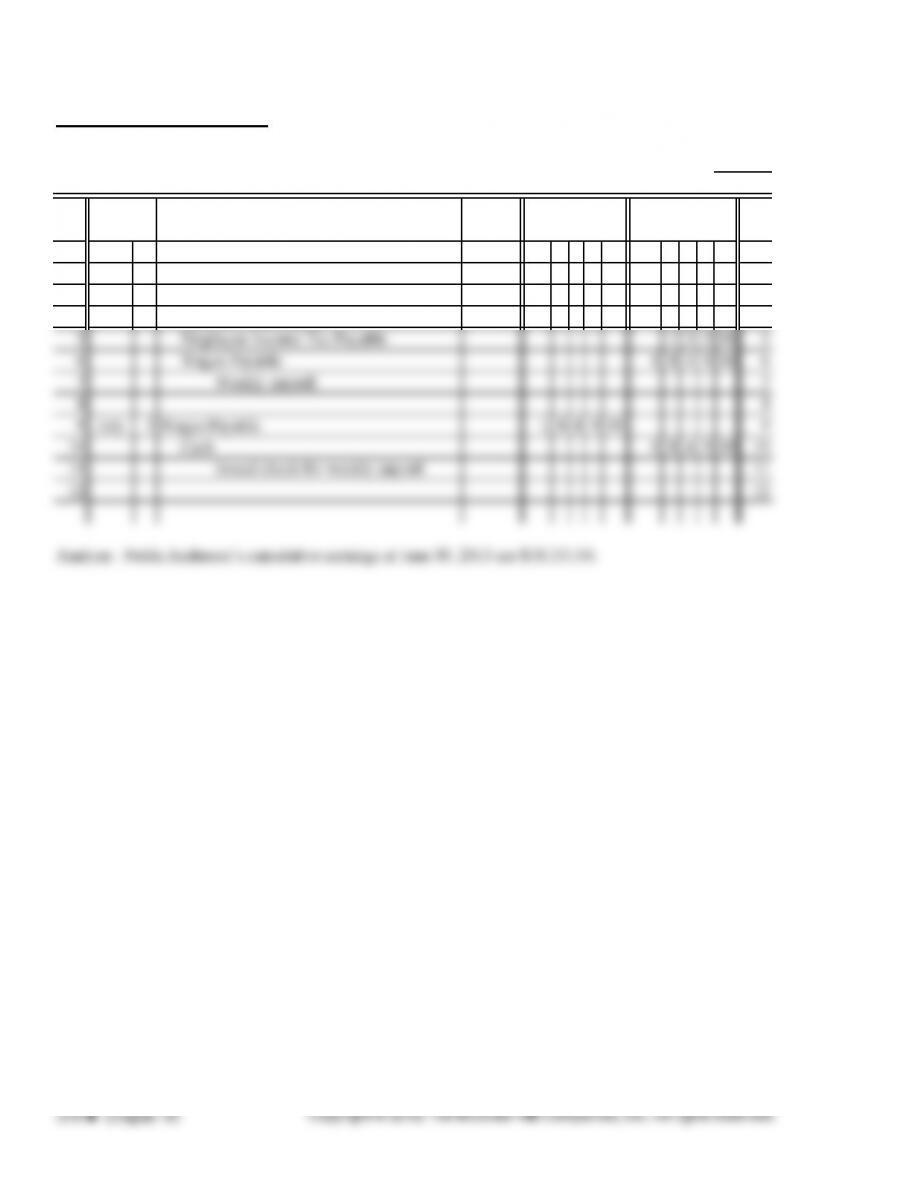

Sales Salaries Expense

DEBIT CREDIT

GENERAL JOURNAL

Office Salaries Expense

DATE DESCRIPTION

PAGE

PROBLEM 10.1A

1.

HOURS

WORKED

48

Gross Pay $667.68

2. PAGE

2

POST.

REF.

1 2013 1

GENERAL JOURNAL 54

CREDITDATE DESCRIPTION DEBIT

$12.84

OVERTIME

EARNINGS

GROSS

EARNINGS

REGULAR

TIME

EARNINGS

REGULAR

HOURS,

HOURLY

RATE

EMPLOYEE

NO.

Kathy Burnett $667.68$154.08$513.60

PROBLEM 10.1A (continued)

Analyze: Kathy earned overtime pay of $1,960.48, calculated as follows:

Cumulative earnings, prior to December 31 payroll $28,000.00

PROBLEM 10.2A

PAYROLL REGISTER WEEK BEGINNING

Nelda Anderson 1 M 17 5 4 0 00 48 $11.75 4 7 0 00 1 4 1 04 6 1 1 04 18 1 5 1 04

NO. OF

HRS. RATE

EARNINGS

June 24, 2013

NAME

NO. OF

ALLOW.

MARITAL

STATUS

CUMULATIVE

EARNINGS

CUMULATIVE

EARNINGS

REGULAR

TIME

EARNINGS

OVERTIME

EARNINGS

GROSS

AMOUNT

PROBLEM 10.2A (continued)

AND ENDING PAID

CHECK

NO.

61 104 611 04 3788 886 4600 51830 61104

SOCIAL

SECURITY MEDICARE FUTA

SOCIAL

SECURITY MEDICARE

INCOME

TAX

NET

AMOUNT

WAGES

EXPENSE

June 30, 2013 July 3, 2013

TAXABLE WAGES DEDUCTIONS DISTRIBUTION

PROBLEM 10.2A (continued)

POST.

REF.

1 2013 1

2 June 30 2 1 4 8 35 2

313319 3

4 3 1 16 4

GENERAL JOURNAL

Social Security Tax Payable

Medicare Tax Payable

Wages Expense

15

DATE DESCRIPTION DEBIT CREDIT

PAGE

PROBLEM 10.3A

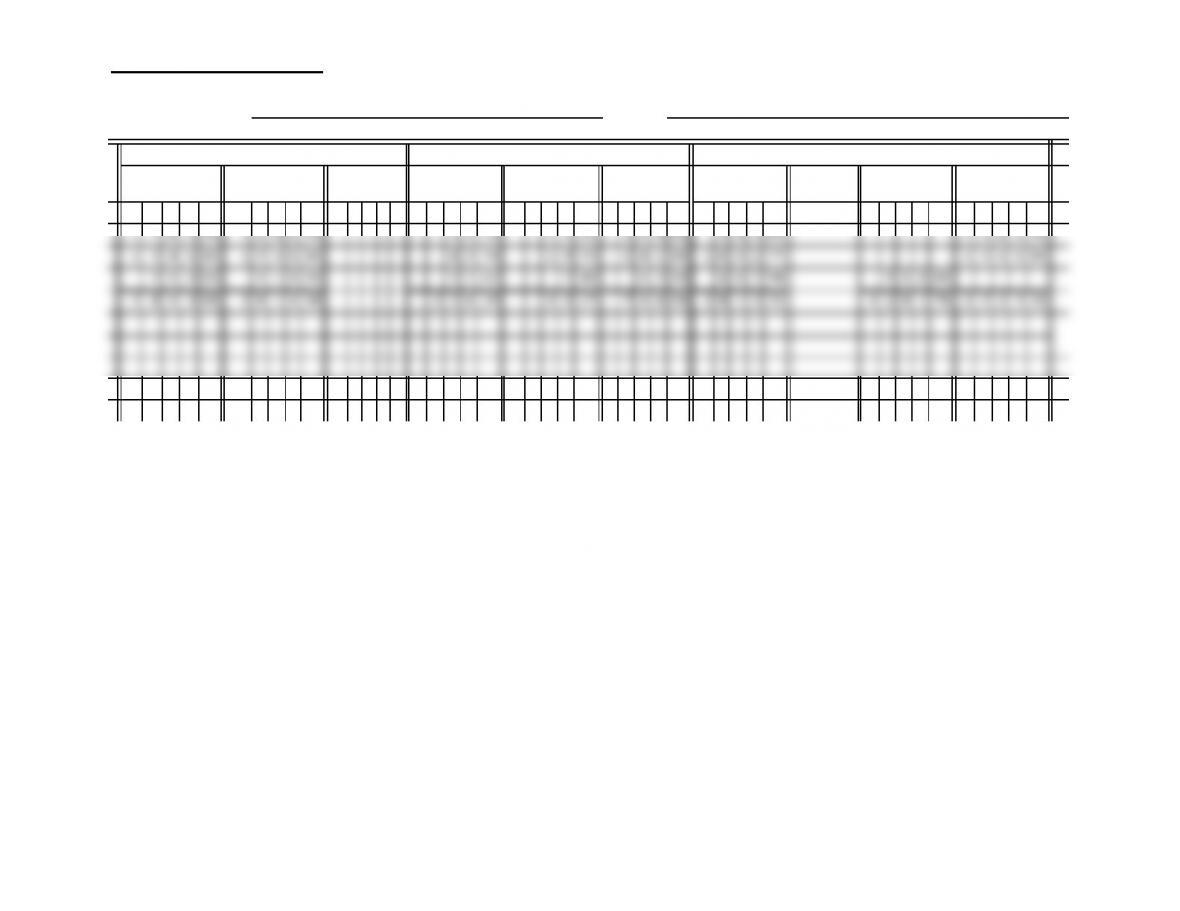

PAYROLL REGISTER WEEK BEGINNING

Gloria Bahamon 4 M 32 7 6 0 00 46 $15.75 6 3 0 00 1 4 1 78 7 7 1 78 33 5 3 1 78

CUMULATIVE

EARNINGS

REGULAR

TIME

EARNINGS

OVERTIME

EARNINGS

GROSS

AMOUNT

December 15, 2013

NAME

NO. OF

ALLOW.

MARITAL

STATUS

CUMULATIVE

EARNINGS

N

O. OF

HRS. RATE

EARNINGS

PROBLEM 10.3A (continued)

AND ENDING PAID

CHECK

NO.

77 178 77178 4785 1119 10300 60974 77178

TAXABLE WAGES DEDUCTIONS DISTRIBUTION

MEDICARE

INCOME

TAX

SOCIAL

SECURITY MEDICARE FUTA

SOCIAL

SECURITY

NET

AMOUNT

December 21, 2013 December 23, 2013

OFFICE

WAGES

DELIVERY

WAGES

PROBLEM 10.3A (continued)

POST.

REF.

1 2013 1

2 Dec. 21 1 2 8 1 78 2

32529303

423629 4

DATE DESCRIPTION DEBIT CREDIT

PAGE

GENERAL JOURNAL

Delivery Wages

32

Office Wages

Social Security Tax Payable

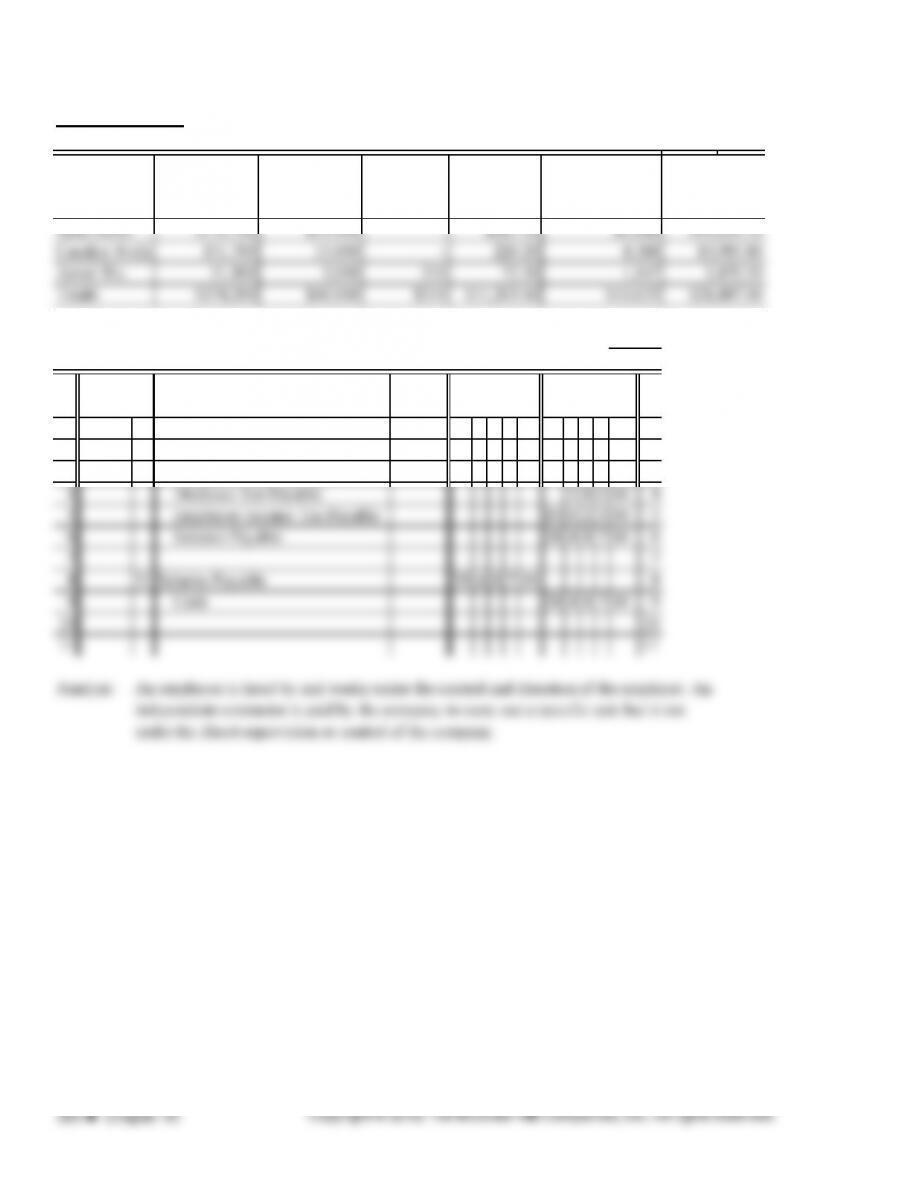

PROBLEM 10.4A

MONTHLY

PAY

PAGE

POST.

REF.

1 2013 1

2 Oct. 31 Salaries Expense 4000000 2

3 Social Security Tax Payable 3 1 0 00 3

4 Medicare Tax Payable 5 8 0 00 4

5 Employee Income Tax Payable 1062300 5

6 Salaries Payable 2848700 6

7 7

8 31 Salaries Payable 2848700 8

9 Cash 2848700 9

10 10

11 11

Analyze: An employee is hired by and works under the control and direction of the employer. An

independent contractor is paid by the company to carry out a specific task but is not

under the direct supervision or control of the company.

MEDICARE

SOCIAL

SECURITY

EMPLOYEE

NAME.

EMPLOYEE

INCOME TAX

WITHHOLDING

CUMULATIVE

EARNINGS

NET PAY

CREDITDATE DESCRIPTION DEBIT

GENERAL JOURNAL 22