Bonus Chapter D – Managing Personal Finances

D-31

a. Banks, savings and loan, credit unions, and

insurance companies all have IRA savings

plans.

b. If you can accept more risk, put your IRA

funds into stocks, bonds, mutual funds, or

precious metals.

c. Mutual funds have multiple options and allow

you to switch from fund to fund.

8. Opening an IRA account may be one of the wis-

est investments you make.

D. SIMPLE IRAs

1. Companies with 100 or fewer employees can

provide their workers with a SIMPLE IRA.

2. Employees can contribute a large part of their

income annually, and the company matches the

contribution.

E. MyIRA PLANS are a Roth IRA-type retirement sav-

ings plans for low- to middle-income individuals.

F. 401(k) PLANS

1. A 401(K) PLAN is a saving plan that allows you

to deposit pretax dollars and whose earnings

compound tax free until withdrawal, when the

money is taxed at ordinary income tax rates.

a. 401(k) plans now account for half of Ameri-

ca’s private pension savings.

b. Only 70% of eligible employees make any

contribution—a huge mistake.

2. 401(k) plans have three BENEFITS:

a. The money you put in REDUCES YOUR

Bonus Chapter D – Managing Personal Finances

D-32

PPT D-28

Individual Retirement Accounts

INDIVIDUAL

RETIREMENT ACCOUNTS

D-28

LO D-4

• Roth IRA — Does not give an up-front tax deduction

but earnings grow tax-free and are tax-free when they

are withdrawn.

• MyIRA — A new Roth IRA-type retirement savings

plan for low– and middle-income individuals.

PPT D-29

401(k) Plans

401(k) PLANS

D-29

LO D-4

• 401(k) Plan — An

employer-sponsored

savings plan that allows you

to deposit a set amount of

pretax dollars and collect

compounded earnings tax-

free until withdrawal.

Bonus Chapter D – Managing Personal Finances

D-33

PRESENT TAXABLE INCOME.

b. TAX IS DEFERRED on the earnings.

c. Employers often MATCH part of your depos-

it.

3. About 61% of employers match your contribu-

tion—often 50 cents on a dollar.

4. You can usually select HOW THE MONEY IS

INVESTED (stocks, bonds, and real estate).

a. Don’t invest all your money in the company

where you work.

b. As with any investment, it is best to DIVER-

SIFY your 401(k) funds.

5. There is a simple 401(k) plan for those firms with

100 or fewer employees.

G. KEOGH PLANS

1. KEOGH PLANS are retirement plans for small–

business people who do not have the benefit of

a corporate retirement system.

2. The maximum amount you can invest in Keogh

plans, $52,000 per year, is higher than for an

IRA.

3. Like IRAs, Keogh funds are NOT TAXED UNTIL

WITHDRAWN, nor are the returns the funds

earn.

4. As with IRAs, there is a 10% penalty for early

withdrawal.

H. FINANCIAL PLANNERS are people who assist in

Bonus Chapter D – Managing Personal Finances

D-34

PPT D-30

Benefits of 401(k) Plans

BENEFITS of 401(k) PLANS

D-30

LO D-4

• Three benefits of

401(k) plans:

1. Contributions

reduce your present

taxable income

2. Tax is deferred on

the earnings

3. Many employers

will match your

contributions.

PPT D-31

Keogh Plans

KEOGH PLANS

D-31

LO D-4

• Keogh plans allow self-employed people to

establish their own retirement plans.

• Keogh plans are like IRAs for entrepreneurs.

• Keogh plans can be withdrawn in a lump sum or

spread out over years.

Bonus Chapter D – Managing Personal Finances

D-35

developing a comprehensive program that covers

investments, taxes, insurance, and other financial

matters.

1. Many people claim to be financial planners; find

one who is a CERTIFIED FINANCIAL PLAN-

NER (CFP).

2. ONE-STOP FINANCIAL CENTERS, or financial

supermarkets, provide a variety of financial ser-

vices in one place.

3. Most financial planners begin with LIFE INSUR-

ANCE, usually term insurance, and add health

insurance plans.

4. Financial planning covers all aspects of invest-

ing, all the way to retirement and death.

I. ESTATE PLANNING

1. The first step is to SELECT A GUARDIAN for

your minor children, someone with a genuine

concern for your children.

a. You should leave sufficient resources to

raise your children, often through life insur-

ance.

b. Choose a contingent guardian in case the

first choice is unable to perform the func-

tions.

2. The second step is to PREPARE A WILL.

a. A WILL is a document that names the

guardian for your children, states how you

want your assets distributed, and names the

Bonus Chapter D – Managing Personal Finances

D-36

lecture enhancer D–7

THE TROUBLE WITH SUING YOUR

BROKER

The recent market crash left investors feeling misled by their

most trusted financial advisors. Many want to seek legal ac-

tion, but that might not be a possibility. (See the complete lec-

ture enhancer on page D.57 of this manual.)

PPT D-32

Planning for Those Who Will Inherit

PLANNING for THOSE

WHO WILL INHERIT

D-32

LO D-4

• Estate planning for those who will inherit money

from you may start with life insurance.

• Will — A document that names the guardian for minor

children, states how you want your assets distributed

and names the executor for your estate.

• Executor — Person who assembles and values your

estate, files income and other taxes, and distributes

assets.

Bonus Chapter D – Managing Personal Finances

D-37

executor for your estate.

b. The EXECUTOR is a person who assembles

and values your estate, files income and

other taxes, and distributes assets.

3. A third step is TO PREPARE A DURABLE

POWER OF ATTORNEY.

a. This document gives an individual you name

the power to take over your finances if you

become incapacitated.

b. A DURABLE POWER OF ATTORNEY FOR

HEALTH CARE delegates power to make

health decisions for you.

4. A financial planner can help you do the planning

needed to preserve and protect your invest-

ments and your children and spouse.

V. SUMMARY

Bonus Chapter D – Managing Personal Finances

D-38

test

prep

PPT D-33

Test Prep

TEST PREP

D-33

• What are three advantages of using a credit card?

• What kind of life insurance is recommended for

most people?

• What are the advantages of investing through an

IRA? A Keogh account? A 401(k) account?

• What are the main steps in estate planning?

Bonus C – Managing Personal Finances

D-39

PowerPoint slide notes

PPT D-1

Chapter Title

Copyright © 2015 by the McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin

Managing

Personal

Finances

BONUS CHAPTER D

PPT D-2

Learning Objectives

LEARNING OBJECTIVES

D-2

1. Outline the six steps for controlling your assets.

2. Explain how to build a financial base, including

investing in real estate, saving money, and

managing credit.

3. Explain how buying the appropriate insurance

can protect your financial base.

4. Outline a strategy for retiring with enough money

to last a lifetime.

PPT D-3

Alexa von Tobel

ALEXA VON TOBEL

LearnVest

D-3

• Started LearnVest after graduating

from Harvard and jobs with Morgan

Stanley and Drop.io.

• Von Tobel believed the cost

structure for financial plans were too

pricey for most consumers.

• She focuses on the 50/20/30

formula.

– 50% of pay goes to essentials

– 20% of pay is saved

– 30% of pay goes to lifestyle

Bonus C – Managing Personal Finances

D-40

PPT D-4

Name That Company

NAME that COMPANY

D-4

One way to save money is to use your credit cards

wisely. There are organizations that can help you

compare credit cards to get the most out of

them.

Name one of those organizations!

Companies: CardRatings.com or CreditCards.com

PPT D-5

Six Steps to Control Your Finances

SIX STEPS to CONTROL YOUR

FINANCES

D-5

LO D-1

1. Take an inventory of your

financial assets

2. Keep track of all your

expenses

3. Prepare a budget

4. Pay off your debts

5. Start a savings plan

6. Borrow only to buy assets

that increase in value

PPT D-6

Managing Your Household Budget

MANAGING YOUR HOUSEHOLD

BUDGET

D-6

LO D-1

• A household budget generally

includes:

– Mortgage or rent

– Food and clothing

– Vehicles and furniture

– Insurance needs

– Other expenses

Bonus C – Managing Personal Finances

D-41

PPT D-7

Possible Cost-Saving Choices

POSSIBLE COST-SAVING

CHOICES

D-7

LO D-1

Living frugally is not about doing without but rather mak-

ing wise choices.

PPT D-8

How Money Grows

HOW MONEY GROWS

D-8

LO D-1

The time value of money and compound interest are the

saver’s best friend.

PPT D-9

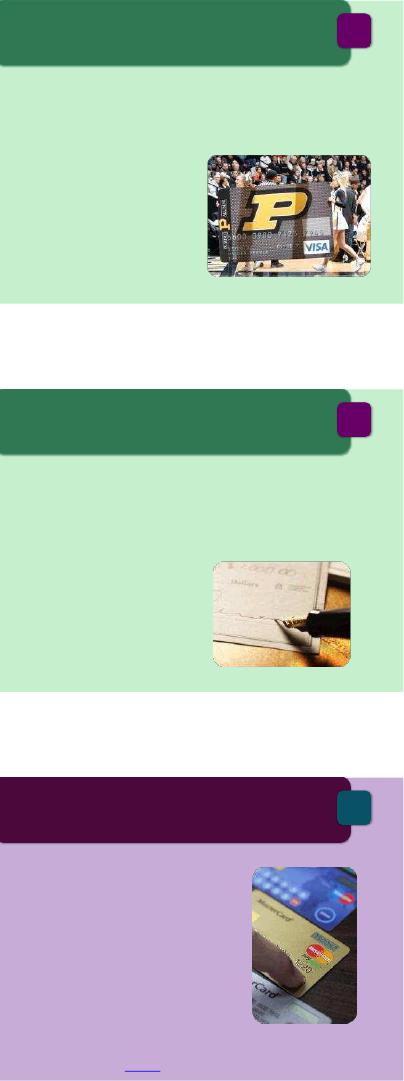

Easy-ish Budget Cuts

EASY-ish BUDGET CUTS

Source: Kiplinger’s Personal Finance. D-9

LO D-1

1. Cut back on gourmet

groceries and use coupons.

2. Cut down your cell phone bill.

3. Cut out the cable television.

4. Cut down on nights out.

5. Cut the clutter in your house.

1. This slide shows the student how to trim the fat of their

monthly budget.

2. Cutting cable! Shock! Horror! Many shows are available

through free sites like Hulu.com, a lot of people are going

cable-less.

3. Encourage students to visit free budgeting sites (like

Mint.com) so they can track their spending. This might

surprise them.

Bonus C – Managing Personal Finances

D-42

PPT D-10

Billionaire’s Tab

BILLIONAIRE’s TAB

Insights into a Lux Lifestyle

Source: Forbes, www.forbes.com, accessed November 2014. D-10

Perk New York

Billionaire

Los Angeles

Billionaire

Dinner for Two $550 at Per Se $700 at Urasawa

Hotel for Two Nights $70,000 at Four

Seasons

$30,000 at Four

Seasons

Haircut $200 at Sally

Hershberger $750 at Fekkai

Club Table Service $525+ at The Box $1,200+ at Voyeur

Massage $225 at Four

Seasons

$215 at Beverly Hills

Hotel

LO D-1

1. And you thought Fekkai’s shampoo was expensive! This

slide shows students what two billionaires in two Ameri-

can cities pay for services.

2. Ask students: What do these services give the person

above what others can afford? Is it really worth it to pay

this much?

PPT D-11

Building Your Financial Base

BUILDING YOUR

FINANCIAL BASE

D-11

LO D-2

• Live frugally. If married,

try to live on one income.

• Your first major

investment might be a

low-priced home.

• Buy for the long term and

don’t live beyond your

means.

PPT D-12

Five Rules of Frugality

FIVE RULES of FRUGALITY

Source: AARP, October 2010. D-12

1. Don’t give up what you love.

2. Find inexpensive forms of entertainment.

3. Cut back on non-crucial things.

LO D-2

4. Never go shopping

without knowing exactly

what you’re buying.

5. Shop around for good

deals!

1. This slide shows five steps to saving money.

2. Explain these are easy steps. Many think you have to

give up all fun if you want to live frugally. This slide

shows you just need to spend time thinking before you

buy instead of being impulsive.

3. Ask students: How many of you attend free concerts in-

stead of paying top-dollar for big acts?

Bonus C – Managing Personal Finances

D-43

PPT D-13

Financial Benefits of Buying a Home

• A home is an investment you can live in.

• Paying for a home is a good way of forcing

yourself to save.

FINANCIAL BENEFITS of

BUYING a HOME

D-13

LO D-2

• Interest paid on your

home loan is tax

deductible.

• Three keys to optimal

return on your home

are: location, location,

location.

Although the housing crisis has dampened home prices,

historically real estate has been a sound investment.

PPT D-14

How Much House Can You Afford?

HOW MUCH HOUSE CAN YOU

AFFORD?

D-14

LO D-2

PPT D-15

Saving and Managing Credit

• Contrarian Approach — Buying stock whenever

everyone else is selling or vice versa.

• Credit cards serve useful purposes and are

important to own but must be used discriminately.

SAVING and MANAGING CREDIT

D-15

LO D-2

• Not all credit cards are

equal. Check sites like

CardRatings.com or

CreditCards.com to find a fit.

Warren Buffet is considered a contrarian investor.

Bonus C – Managing Personal Finances

D-44

PPT D-16

Credit Cards and Debt

• 50% of college students have four or more credit

cards.

• Only 17% report paying off their balance each

month.

CREDIT CARDS and DEBT

D-16

LO D-2

• If you feel managing a

credit card would be

too difficult, try a debit

card.

PPT D-17

Credit Card Act of 2009

• Created new consumer credit card protections

and went into effect in February 2010.

• New law allows card issuers to increase interest

rates for only a limited number of reasons.

CREDIT CARD ACT of 2009

D-17

LO D-2

• People must be over 21

or have an adult

cosigner to get a credit

card.

PPT D-18

Clean Credit

CLEAN CREDIT

Steps to Keep a Good Credit Score

Source: Money Magazine, money.cnn.com, accessed November 2014. D-18

PhotoCredit:RobertScoble

LO D-2

1. Always pay your bills on time!

2. Keep small balances on

multiple cards.

3. Don’t shift balances.

4. Don’t apply for too many cards

at once.

5. Don’t file for personal

bankruptcy.

1. This slide shows the student how to ensure they have a

good credit score.

2. Students don’t often understand the benefit of not just

paying the minimum amount due. Focus on paying bills

in full and on time.

Bonus C – Managing Personal Finances

D-45

PPT D-19

What’s Your Score?

WHAT’s YOUR SCORE?

How You Might Rate on a Credit Score

D-19

Range Rating

760 to 850 Excellent

700 to 759 Great

660 to 690 Fair

620 to 659 Poor

619 and under Very Poor

LO D-2

1. This slide shows the student what is a good credit score.

2. Scores range from 300 to 850.

3. Ratings also depend on a number of factors including:

credit payment history, current debt, length of credit his-

tory, credit type mix and frequency of application for new

credit.

PPT D-20

Test Prep

TEST PREP

D-20

• What are the six steps you can take to control

your finances?

• What steps should a person follow to build

capital?

• Why is real estate a good investment?

1. The six steps you can take to control your finances are:

(1) Take an inventory of your financial assets, (2) keep

track of all your expenses, (3) prepare a budget, (4) pay

off your debts, (5) start a savings plan, and (6) borrow

only to buy assets that increase in value or generate in-

come.

2. The steps a person should follow to build capital are:

Find a job, create a budget, and live frugally. Warren

Buffet became one of the worlds richest people but still

lives in the house he purchased in the 1950s! Invest

the money you save to generate more capital.

3. Historically real estate has been a sound investment. It

is the only investment you can live in. Also, the pay-

ments are fixed with the exception of taxes and utili-

ties. As your income increases, the house payments

get easier to make, while rent tends to increase over-

time.

PPT D-21

Insuring Your Life

INSURING YOUR LIFE

D-21

LO D-3

• Term Insurance — A pure insurance protection for a

given number of years that typically costs less the

younger you buy it.

• Whole Life Insurance — Combines pure insurance

with savings, so you buy both insurance and a

savings plan.

• Variable Life Insurance — A form of whole life

insurance that invests the cash value of the policy in

stocks or other high-yielding securities.

Nearly 1/3 of U.S. households are without life insurance

coverage. Due to the cost difference, many recommend the

purchase of term insurance rather than whole life.