Bonus B – Managing Risk

C-29

PPT C-7

How to Deal with Pure Risk

HOW to DEAL with PURE RISK

C-7

LO C-2

1) Reduce the risk

2) Avoid the risk

3) Self-insure against the risk

4) Buy insurance against the

risk

PPT C-8

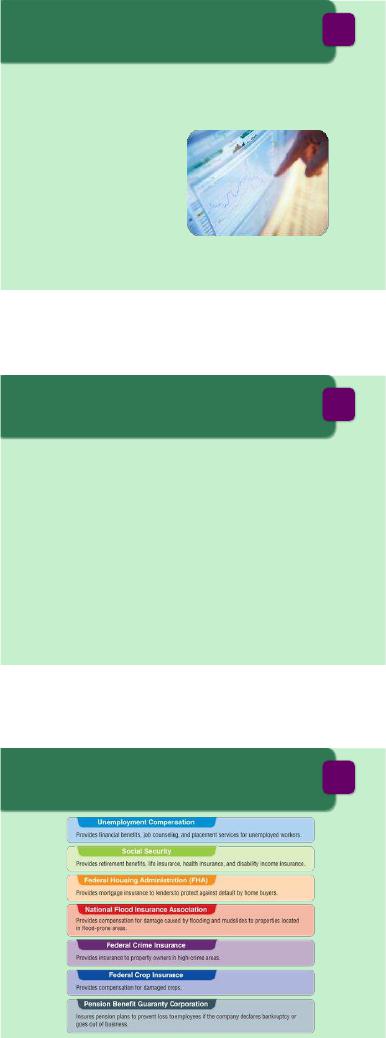

Most Costly Disasters

MOST COSTLY DISASTERS

DisasterYear Losses

Hurricane Katrina 2005 $122 Billion

Central U.S. Drought 1988 $76.4 Billion

Superstorm Sandy 2012 $65.7 Billion

Northridge California Earthquake 1994 $40 Billion

Hurricane Ike 2008 $35 Billion

Hurricane Andrew1991 $28 Billion

9-11 Terrorist Attacks 2001 $21.37 Billion

Source: NOAA, www.noaa.gov, accessed November 2014.

C-8

LO C-2

1. This slide presents the costliest disasters in billions of

dollars.

2. We don’t yet know the economic impact of the 2011

earthquake and tsunami in Japan.

3. Ask the students, How many of these disasters do

you remember? (Most of them should identify the

9/11 terrorist attacks and Hurricane Katrina as the

most talked-about events.)

4. From a risk standpoint, ask the students, How can a

business prepare for such disasters? (Taking precau-

tionary actions by ensuring appropriate types and

coverage of insurance, employee preparedness, etc.

should be absolutely essential. The companies need

to protect their people, property, data and infor-

mation, and finances.)

PPT C-9

What’s Self Insurance?

• Self-Insurance — The practice of setting aside

money to cover routine claims and buying only

“

catastrophe

”

insurance policies to cover big losses.

WHAT’S SELF INSURANCE?

C-9

LO C-2

• Companies that self-

insure can “go bare”

and pay claims from

their operating budgets

or set up special funds

to pay for claims.

Many large companies use self-insurance as a means of risk

management.

Bonus B – Managing Risk

C-30

PPT C-10

What Risks Are Uninsurable?

WHAT RISKS are

UNINSURABLE?

C-10

LO C-2

• Uninsurable Risk — A risk that no insurance

company will cover. Risks can include:

– Market risks

– Political risks

– Personal risks

– Operational risks

PPT C-11

What Risks Are Insurable?

WHAT RISKS are INSURABLE?

C-11

LO C-2

• Insurable Risk — A risk that the typical insurance

company will cover, using the following guidelines:

1) The policyholder must have an insurable interest.

2) The loss must be measurable.

3) The chance of loss must be measureable.

4) The loss must be accidental.

5) The insurance company’s risk should be dispersed

among different areas.

6) The insurance company can set standards for accepting

risks.

PPT C-12

Public Insurance

PUBLIC INSURANCE

C-12

LO C-2

Bonus B – Managing Risk

C-31

PPT C-13

Test Prep

TEST PREP

C-13

• Why are companies more aware now of the need

to manage risk?

• What is the difference between pure risk and

speculative risk?

• What are the four major options for handling risk?

• What are some examples of uninsurable risk?

1. Hurricanes, terrorist threats, identity theft, and an un-

stable economy have all contributed to additional risk

and the need for greater risk management.

2. Pure risk is the threat of loss with no chance for prof-

it, such as the threat from a fire. If your house burns

to the ground you lose money, but if it does not you

gain nothing. Speculative risk can result in either

profit or loss. An entrepreneur’s chance to make a

profit is considered speculative risk.

3. The four major options for handling risk are (1) re-

duce the risk, (2) avoid the risk, (3) self-insure

against the risk, and (4) buy insurance against the

risk.

4. Examples of uninsurable risk include market risk, po-

litical risk, personal risk, and some risk of operation.

PPT C-14

Insurance Policies

INSURANCE POLICIES

C-14

LO C-3

• Insurance Policy — A written contract between the

insured and an insurance company that promises to

pay for all or part of the loss by the insured.

• Premium — The fee the insurance company

charges, the cost of the policy to the insured.

• Claim — A statement of loss that the insured sends to

the insurance company to request payment.

PPT C-15

Basics of Insurance Policies

• Law of Large Numbers — If a large number of

people or organizations are exposed to the same risk,

a predictable number of losses will occur during a

given period of time.

BASICS of

INSURANCE POLICIES

C-15

LO C-3

• Rule of Indemnity —

An insured person or

organization can

’

t collect

more than the actual loss

from an insurable risk.

Bonus B – Managing Risk

C-32

PPT C-16

Types of Insurance Companies

• Stock Insurance Company — Owned by

stockholders, just like any other investor-owned

company.

TYPES of

INSURANCE COMPANIES

C-16

LO C-3

• Mutual Insurance

Company — An

organization owned by its

policyholders.

PPT C-17

Stock and Mutual Insurance

Companies

STOCK and MUTUAL

INSURANCE COMPANIES

Stock Insurance

Companies

Hartford Life

Metropolitan Life

Prudential Life

Mutual Insurance

Companies

Mass Mutual

New York Life

Northwestern Mutual

C-17

LO C-3

1. This slide profiles some of stock insurance compa-

nies and mutual insurance companies.

2. If time permits, have students examine some of the

differences among the stock and mutual insurance

companies listed on this slide.

PPT C-18

Progress Assessment

TEST PREP

C-18

• What is the law of large numbers?

• What is the rule of indemnity?

1. The law of large numbers means that if a large num-

ber of people or organizations are exposed to the

same risk, a predictable number of losses will occur

during a period of time.

2. The rule of indemnity says an insured person or or-

ganization cannot collect more than the actual loss

from an insurable act.

Bonus B – Managing Risk

C-33

PPT C-19

Heath Insurance Changes

HEALTH INSURANCE CHANGES

C-19

LO C-4

• The Affordable Care Act has the government much

more involved in the health insurance process.

• We are likely to see many variations of health

coverage in the future.

PPT C-20

Other Types of Insurance

OTHER TYPES of INSURANCE

C-20

LO C-4

• Disability insurance replaces

part of your income if you

become disabled and cannot

work.

• Worker’s compensation

insurance guarantees

payment of wages, medical

care and rehabilitation for

employees injured on the

job.

Employers in all 50 states are required to provide workers’

compensation insurance.

PPT C-21

Getting the Most out of Life Insurance

GETTING the MOST out of

LIFE INSURANCE

C-21

Source: Entrepreneur, www.entrepreneur.com, accessed November 2014 .

LO C-4

1. Quit smoking, lose weight

and go to the gym!

2. Figure out how much

insurance you need.

3. Pick a good insurance

company.

4. Find a good financial

planner.

The cost of life insurance increases if you smoke or are

overweight, so addressing these issues will reduce your pre-

miums.

Bonus B – Managing Risk

C-34

PPT C-22

Liability Insurance

LIABILITY INSURANCE

C-22

PhotoCredit:PaulWilson

LO C-4

• Professional liability insurance

covers people found liable for

professional negligence; also

known as malpractice

insurance.

• Product liability insurance

covers liability arising out of

products sold.

PPT C-23

Home-Based Businesses

HOME-BASED BUSINESSES

C-23

LO C-4

• Homeowners’ policies

usually do not provide

protection for home-based

businesses.

• For more coverage, you

may need to add a rider to

your homeowner’s policy.

• Cyber risk insurance can

help a business in case of

hacking.

PPT C-24

Home Matters

HOME MATTERS

What You Need to Know About Home Insurance

C-24

Source: Money, www.money.com. accessed November 2014.

LO C-4

1. Not all policies cover

home-based businesses.

2. Don’t buy too much

coverage.

3. Small claims can add up.

4. The home’s history

matters.

Bonus B – Managing Risk

C-35

PPT C-25

Test Prep

TEST PREP

C-25

• Why should someone buy disability insurance?

• How many different kinds of private insurance can

you name?

1. Disability insurance is important, because a young

person is more likely to become disabled than to die.

2. The kinds of private insurance include life insurance

(whole and term), medical insurance, property insur-

ance, renter’s insurance, professional liability insur-

ance, disability, and workers’ compensation.

Bonus B – Managing Risk

C-36

lecture

enhancers

“Insurance covers everything except what happens.”

Miller’s Law of Insurance

“If the lion didn’t bite the tamer every once in a while, it wouldn’t be exciting.”

Darrell Waltrip

“The probability of anything happening is in inverse proportion to its

desirability.”

Guperson’s Law

lecture enhancer C-1

THE FOUR FACETS OF RISK

While many companies are doing a better job of cataloging their risks, many industry insiders

think an entirely new approach may be needed. Most businesses approach risk within a “silo structure,”

where different risks are handled by different departments. As the business grows, everyone has a good

understanding of the risks in their part of the business but not in other parts of the firm. If businesses co-

ordinated all the parts, risk could be managed more efficiently.

This is why risk experts recommend a more integrated system: enterprise-level risk management

(ERM). ERM is a way to get the big picture—how risks interact and affect the enterprise as a whole—

then use this knowledge to minimize risk and maximize return.

Not all risks are equal, or equally probable. A successful risk management strategy requires com-

panies to understand the different types of risk they face, and create a strategy for transferring or control-

ling each of them.

The risk of an earthquake damaging or destroying a factory is a hazard risk. The best course of

action is to transfer the risk by insurance. The risk that the price of oil will increase is a financial risk.

The company can hedge against this risk by purchasing options in the commodity market, creating a ceil-

ing on the price of oil. An example of an operational risk would be a computer virus putting IT systems

out of action. The best course of action would be to control the risk by investing in antivirus software.

For many companies, risk management stops with these three facets—hazard risk, financial risk,

and operational risk. But business must also consider a fourth facet of risk—strategic risk. This is the

most dangerous type of threat businesses face. Strategic risk isn’t as easy to define or protect against as an

earthquake or the fluctuating price of oil. Strategic risk is an external bad thing that can happen to your

business model, like the collapse of your brand’s reputation or the risk of a new technology overtaking

your own. Strategic risk is not only the most dangerous type of risk, but also the most prevalent, account-

ing for 60 to 70% of a business’s risk.

However, once strategic risk is identified, several tools can be used to handle it. If the risk affects

a particular industry, companies may be able to collaborate and cooperate. When the aircraft industry

faced declining profits in the 1970s, several companies combined to form the joint venture Airbus. There

is also a risk when two technologies are competing for acceptance. The best approach could be double–

betting, or investing in both. In the 1980s, Microsoft embraced both Windows and OS/2 until one system

prevailed. In both these cases, the companies not only managed their risk, they also grew their businesses.

Bonus B – Managing Risk

C-37

There are also numerous examples of companies that didn’t identify and deal with strategic risk.

By staying too long with analog phones, instead of double-betting on both analog and digital models,

Motorola opened the way for Nokia to dominate the digital side. The music industry also failed to antici-

pate the significance of the Internet distribution model and handed a lucrative opportunity to Apple’s

iTunes stores.

Companies have become successful at cataloging and managing traditional risks, like earth-

quakes, tornados, currency fluctuations, and failing IT systems. However, most are still ignoring 60 to

70% of their risks. With an enterprise-wide risk management program, they can to put the same efforts

into cataloging and managing the most important one: strategic risks.i

lecture enhancer C-2

RISK PERCEPTION: ANALYTICAL VERSUS INTUITIVE

Washington Post writer Joel Achenbach recalls the man he encountered on the morning of Sep-

tember 11, 2001. In the hours after terrorists flew a plane into the Pentagon, Achenbach joined the hasty

evacuation near the Federal Reserve. He came across a man sitting calmly on a park bench reading a

newspaper. The man had no interest in the evacuation or even listening to the news bulletins. He told

Achenbach that he figured the danger was over and went back to his stock listings.

The man’s reaction illustrates the two components of perceived risk—logic and emotion—two

very dissimilar elements. The man could have reasoned through the situation carefully and determined it

was safe to go back to the newspaper. That would be the logical and analytical approach to risk. But he

could also be using his gut instinct to know that the danger was over.

The intuitive and emotional system is based on images burned into our brains during past experi-

ences, and it often trumps the analytical one. Gut instinct warns us when something in the familiar envi-

ronment doesn’t seem right. Over the course of human evolution, that instinct has kept the human species

alive. However, the intuitive instinct may not warn us of dangers from unfamiliar sources, such as air-

planes descending from the sky to bring down skyscrapers.

Feelings can also cause us to make illogical decisions. A 1993 experiment offered people a

chance to win a dollar by drawing a red jellybean from one of two bowls. One bowl had 200 beans, 7 of

them red. The other had 10 beans, only 1 red. Many people preferred the bowl with the 7 red beans, even

though they knew the odds were worse. However, they said they felt as if they had a better chance.

Another experiment highlights the emotional, intuitive element in decision making. Clinicians at

a mental hospital were more likely to release a patient from a hospital if told he had a 20% chance of be-

coming violent than if told 20 out of 100 such patients would become violent. The visual image of the

second scenario was more frightening, although the two risks were actually equivalent.

A risk taker analyzes both the emotional and analytical systems to make good decisions. Says

psychologist Paul Slovic of the University of Oregon, “You need your feelings to put a cross-check on

your analysis, and you need analysis to keep your feelings in check.”ii

lecture enhancer C-3

THE ECONOMIC IMPACT OF A CATASTROPHE

The chief concern after the devastating earthquake and tsunami that rocked Japan in March 2011

was preserving lives. With a death toll in the tens of thousands and a leaking nuclear reactor, Japan still

had many tragedies to overcome before the nation could turn its eyes to the future. Like many of the

earthquake’s grisly consequences, the long-term economic outlook for Japan is uncertain. But as a poten-

Bonus B – Managing Risk

C-38

tial $235 billion rebuilding price tag looms overhead, the fiscal future of Japan is worth examining at least

to find out if this disaster could push Japan into a debt crisis.

First of all, Japan has the consolation of its wealth. Traditionally, the richer the country, the less

one event can significantly affect its GDP. Although the quake likely destroyed many businesses and in-

frastructure, Japan has ample resources to draw upon for rebuilding. But Japan’s robust GDP doesn’t tell

the whole story. For all intents and purposes, Japan is already mired in a credit crisis. Public debt ac-

counts for an astronomical 228% of GDP, compared to 144% for Greece and 77% for the United States.

Government officials rarely mention the problem publicly, and the low interest rates that keep businesses

borrowing only make the problem worse.

Given these circumstances, any fiscal hit taken from the earthquake would be just another drop in

a very deep bucket. So far the government allotted $12 billion for recovery in the 2011 budget and will

likely increase that amount over the coming years. And unlike the debt crisis, business leaders are at least

addressing the aftermath of the earthquake head on. A Japanese business lobby recently gave the govern-

ment its blessing to scrap plans for a corporate tax cut to ensure that recovery efforts have as much fund-

ing as possible.iii

lecture enhancer C-4

RECONSIDERING FLOOD INSURANCE

After Hurricane Katrina devastated the Gulf Coast in 2005, shocked residents and businesspeople

called their insurance companies. Many found out—too late to do anything about it—that their losses

weren’t covered by insurance.

Nature can be cruel, and disasters occur with alarming frequency. Floods are more confined and

predictable than other disasters, but their scale is sometimes so huge that private insurers have been

scared away. That’s why Congress created the National Flood Insurance Program (NFIP) four decades

ago.

Since then, the federal government has made flood insurance available to property owners, filling

a gap left by private carriers, which generally decline to write the coverage. The program has grown con-

troversial over the years. Critics have argued that it encourages Americans to build on beaches, flood

plains, and other sites that shouldn’t be built on—and wouldn’t be if the government wasn’t willing to

compensate owners when such homes and vacation spots are washed away.

The insurance can be immensely valuable. Policies under the NFIP will pay up to $250,000 for

residential buildings, plus another $100,000 for contents that are lost. It will also pay up to $500,000 for

nonresidential buildings and $500,000 for their contents.

The premiums average around $400 a year for $100,000 of coverage—higher in very flood-prone

areas. That’s very reasonable, considering the risks. Many mortgage lenders require it, at least for proper-

ty located within a flood-prone area. Fannie Mae, for example, requires coverage of 80% of the replace-

ment cost of the home, or the program limit of $250,000, whichever is less.

The federal flood insurance program has about 4.6 million policies in place, covering more than

$743 billion in assets. Annual premium collections run about $2 billion. Still, the program is not as popu-

lar as you might expect. On the Mississippi Gulf Coast devastated by Katrina, just one in four homes

were covered. The national average is 10 to 20%. It is much higher in New Orleans, where it covers about

half the homes.

Bonus B – Managing Risk

C-39

The hurricanes of 2005 created staggering losses and focused attention and concern on the federal

flood program. From 1978 through 2005, the program paid $31.6 billion to 1.5 million policyholders na-

tionwide. Louisiana’s share, thanks to Hurricanes Katrina and Rita, was $14.9 billion. Next came Florida,

at $3.3 billion; Texas, at $2.8 billion; and Mississippi, at $2.7 billion. Pennsylvania and New Jersey’s

losses were far less, though each topped $600 million.

Previously, the premiums collected have kept the program self-sustaining. But according to Rob-

ert Hunter, former head of the federal flood insurance program, the 2005 hurricane season will throw the

program into deficit. According to Hunter, Hurricane Katrina is the first disaster in which flood claims

exceed those for wind, which are typically paid by private insurers or state-run risk pools.

Hunter also sees an interesting question developing among claims adjusters—Who pays for what

damage? The federal program uses private insurers and their adjusters to evaluate claims, and “company

X may say, ‘I can’t tell if this is flood or wind, so it looks like flood because they pay it and we don’t,’”

Hunter said.iv

Bonus B – Managing Risk

C-40

endnotes