Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-61

PPT 20-19

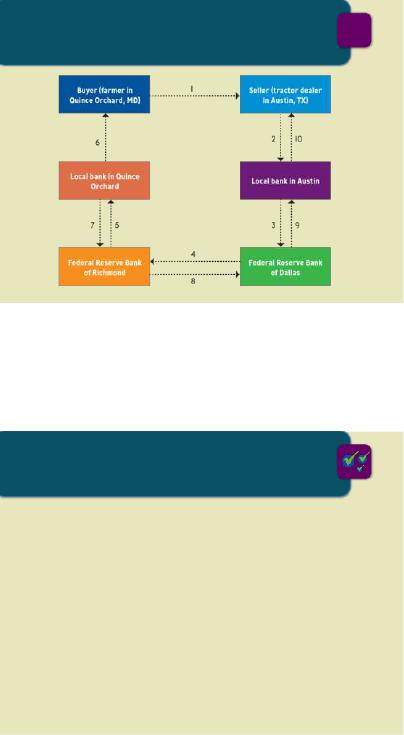

Check-Clearing Process through the

Federal Reserve

CHECK-CLEARING PROCESS

THROUGH the FEDERAL RESERVE

20-19

LO 20-2

PPT 20-20

Test Prep

TEST PREP

20-20

• What is money?

• What are the five characteristics of useful money?

• What is Bitcoin?

• What is the money supply, and why is it important?

• How does the Federal Reserve control the money

supply?

• What are the major functions of the Federal

Reserve? What other functions does it perform?

1. Money can be anything that people accept as pay-

ment for goods and services.

2. The five characteristics of useful money are: Porta-

bility, divisibility, stability, durability, and unique-

ness.

3. The money supply is the amount of money availa-

ble for people to buy goods and services. It is im-

portant to manage the money supply, since too

much money could cause inflation and too little

money may cause deflation.

4. To control the money supply the Federal Reserve

can increase or decrease the reserve requirement,

buy or sell government securities, or change the

discount rate.

5. The Federal Reserve is responsible for creating an

environment that fosters stable prices and full em-

ployment. It attempts to manage these two goals

with monetary policy. The Federal Reserve is also

responsible for the clearing of checks.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-62

PPT 20-21

The Establishment of the Federal

Reserve System

• A cash shortage problem in 1907 led to the

creation of the Federal Reserve System.

The ESTABLISHMENT of the

FEDERAL RESERVE SYSTEM

20-21

LO 20-3

• Under the Federal

Reserve Act of 1913,

all federally chartered

banks had to join the

Federal Reserve.

State banks were also permitted to join.

PPT 20-22

Largest Bank Failures

LARGEST BANK FAILURES

20-22

Bank Year Assets

Washington Mutual Bank 2008 $307 Billion

Continental Illinois NB&T 1984 $67 Billion

First Republic Bank Corp 1986 $49 Billion

IndyMac Bank 2008 $32 Billion

American Savings & Loan Assn 1988 $30 Billion

Colonial Bank 2009 $25 Billion

Source: FDIC.gov, accessed November 2014.

LO 20-3

1. This slide highlights the largest bank failures in

U.S. banking history.

2. Three of these failures are a direct result of the

financial crisis that started in 2008.

3. Ask students: Why didn’t the Washington Mutual

and IndyMac Bank failures create a total loss of

confidence in the United States banking system

like we saw during the Great Depression? (Stu-

dents should be able to recognize the stepped up

role of the US government including the creation

of the FDIC insurance program and the increase

in FDIC coverage from $100,000 to $250,000.

PPT 20-23

The U.S. Banking System

The U.S. BANKING SYSTEM

20-23

LO 20-4

• Commercial banks

• Savings and loan

associations

• Credit unions

• Nonbanks

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-63

PPT 20-24

Commercial Banks

COMMERCIAL BANKS

20-24

LO 20-4

• Commercial Bank — A profit-seeking organization

that receives deposits from individuals and

corporations in the form of checking and savings

accounts and uses those funds to make loans.

• A commercial bank has two types of customers:

1. Depositors

2. Borrowers

PPT 20-25

Commercial Banks’ Services

COMMERICAL BANKS’

SERVICES

20-25

LO 20-4

• Demand Deposit — The technical name for a

checking account; money is available on demand

from the depositor.

• Time Deposit — A savings account; a bank can

require a prior notice before you make a withdrawal.

• Certificate of Deposit — A savings account that

earns interest, to be delivered on the certificate

’

s

maturity date.

Commercial banks also offer credit cards, financial coun-

seling, automatic payment of bills, brokerage services,

safe-deposit boxes, travelers checks, and individual re-

tirement accounts (IRAs).

PPT 20-26

Would You Tell the Teller?

WOULD YOU TELL the TELLER?

20-26

• The bank teller mistakenly gives you $320 instead

of the $300 you asked for.

• You bring the error to her attention, but she

disagrees she miscounted the money.

• You wonder whether to just keep the extra $20

even though you know her accounts will not

balance at the end of the day.

• What are your alternatives? What do you do?

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-64

PPT 20-27

Savings and Loan Associations

SAVINGS and

LOAN ASSOCIATIONS

20-27

LO 20-4

• Savings and Loan Associations (S&Ls) — A

financial institution that accepts both savings and

checking deposits and provides home mortgage

loans.

• Often known as thrift institutions because their

original purpose was to promote customer thrift

and home ownership.

PPT 20-28

Credit Unions

• Credit Unions —

Nonprofit, member-owned

financial cooperatives that

offer the full variety of

banking services to their

members.

CREDIT UNIONS

20-28

LO 20-4

• As nonprofits, credit

unions enjoy an

exemption from federal

income taxes.

Due to their exemption from federal income taxes, credit

unions: fees are typically less and the interest rates paid

on deposits are often higher.

PPT 20-29

Nonbanks

NONBANKS

20-29

– Life insurance companies

– Pension funds

– Brokerage firms

– Commercial finance

companies

– Corporate financial

services

LO 20-4

• Nonbanks — Financial institutions that accept no

deposits, but offer many of the services provided by

regular banks. Nonbanks include:

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-65

PPT 20-30

Taking a Bite Out of the Sharks

TAKING a BITE OUT of the SHARKS

20-30

• Dealstruck is a new type of alternative,

nonbank lender.

• It uses a peer-to-peer model where

wealthy investors provide capital for

the loans.

• Interest rates range from 8 to 24% for

loans up to $250,000 and can stretch

for a period of three years.

PPT 20-31

What Attracts Customers to Online

Banking

WHAT ATTRACTS CUSTOMERS

to ONLINE BANKING

Source: comScore, www.comscore.com, accessed November 2014. 20-31

LO 20-4

• Free identity theft

protection

• Free credit score

monitoring

• Personal financial

management

• Instant messaging service

• Bank’s blog

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-66

PPT 20-32

Test Prep

TEST PREP

20-32

• Why did the U.S. need a Federal Reserve Bank?

• What is the difference between a bank, a savings

and loan association, and a credit union?

• What is a consumer finance company?

1. The Federal Reserve emerged after the banking cri-

sis of 1907 and was organized originally to be a

lender of last resort.

2. After bank deregulation, the services offered by

banks and S&Ls are now similar. They both offer

many of the same services. Credit Unions are tax-

exempt member-owned cooperatives that operate

like banks.

3. Consumer finance companies offer short-term loans

to those who cannot meet the credit requirements of

regular banks.

PPT 20-33

The Banking Crisis

The BANKING CRISIS

20-33

LO 20-5

• Almost 5 million households suffered through

housing foreclosures since 2007.

• Since the banks owned the mortgages, their profits

declined.

• This led to a banking crisis

and the government had to

help the banks out.

• Assigning blame to only one

agency is not possible, but it

had to be fixed.

PPT 20-34

Protecting Depositors’ Money

PROTECTING

DEPOSITORS’ MONEY

20-34

LO 20-5

• The Federal Deposit Insurance Corporation

(FDIC) — An independent agency of the U.S.

government that insures bank deposits up to

$250,000.

• The Savings Association Insurance Fund

(SAIF) — Insures holders of accounts in savings and

loan associations.

• The National Credit Union Administration

(NCUA) — Provides up to $250,000 coverage per

individual depositor per institution.

The amount of depositors’ insurance was increased to

$250,000 create confidence in the banking system.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-67

PPT 20-35

Technological Advancements in Banking

TECHNOLOGICAL

ADVANCEMENTS in BANKING

20-35

LO 20-6

• Electronic Funds Transfer

System — Messages about a

transaction are sent from one

computer to another so funds can

be transferred quickly and more

economically.

• Debit Card — Serves the same

function as a check; it

withdrawals funds from a

checking account.

PPT 20-36

Smart Cards

SMART CARDS

20-36

LO 20-6

• Smart Card — A

combination of a credit card,

debit card, phone card,

driver’s license, and more.

PPT 20-37

Making Transactions in Other Countries

MAKING TRANSACTIONS in

OTHER COUNTRIES

20-37

LO 20-7

• Letter of Credit — A promise by the bank to pay the

seller a given amount if certain conditions are met.

• Banker’s Acceptance — A promise the bank will

pay some specified amount at a particular time.

• Money exchange allows companies to go to a

bank and exchange currencies to use in a

particular country (i.e. dollars for euros).

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-68

PPT 20-38

Leading Institutions in International

Banking

LEADING INSTITUTIONS in

INTERNATIONAL BANKING

20-38

LO 20-7

• World Bank — Lends most of its

money to less-developed nations to

improve their productivity and help

raise standards of living and quality of

life.

• International Monetary Fund

(IMF) — Fosters cooperative

monetary policies that stabilize the

exchange of one national currency for

another. About 188 countries are a

part of the IMF.

Both the World Bank and the IMF were created to rebuild

the world economy after World War II.

PPT 20-39

New Day, New Issues Across the Globe

NEW DAY, NEW ISSUES

ACROSS the GLOBE

20-39

• The IMF and the World Bank are both trying to come up

with answers to the global issues that have become very

serious.

• Christine Lagarde, managing director of the IMF, fears

the financial crisis did lasting harm to the potential pace

of growth in many global economies.

• The IMF and World Bank are both trying to solve key

global issues before there is another serious crisis.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-69

PPT 20-40

Test Prep

TEST PREP

20-40

• What are some of the causes for the banking

crisis?

• What is the role of the FDIC?

• How does a debit card differ from a credit card?

• What is the World Bank and what does it do?

• What is the IMF and what does it do?

1. After the Internet bubble of the late 1990s, the Fed-

eral Reserve lowered interest rates creating a situa-

tion in which mortgage rates were low thus fueling

a housing boom. Banks relaxed their underwriting

standards and created mortgage-backed securities

and sold them to organizations throughout the

world. The government did not regulate these

transactions well and banks collapsed as housing

values fell and individuals defaulted on their loans.

2. The role of the FDIC is to insure bank deposits if a

bank were to fail. Bank deposits are currently in-

sured up to $250,000.

3. Unlike a credit card a debit card functions as a

check, withdrawing funds directly from a checking

account. The debit card only allows you to spend

money that is in your account; once the balance is

zero the card cannot be used. If the card is used

with a zero balance, it will result in overdrafts.

4. The World Bank, also called the International Bank

for Reconstruction and Development, is responsible

for financing economic development.

5. The IMF was established to assist the smooth flow

of money among nations. Nations must join the

IMF and allow for flexible exchange rates, inform

the IMF of changes in a country’s monetary policy,

and to modify policies on the advice of the IMF.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-70

lecture

enhancers

“Money is power, freedom, a cushion, the root of all evil, the sum of all blessings.”

Carl Sandburg

“A fool and your money are soon partners.”

Mark’s Law of Monetary Equalization

lecture enhancer 20-1

FIXED ASSETS, OR WHY A LOAN IN YAP IS HARD TO ROLL OVER

On the tiny South Pacific island of Yap, Micronesia, life is easy and the currency is hard. Else-

where, the world’s troubled monetary system creaks along, and devaluations are commonplace. But on

Yap, the currency is as solid as a rock. In fact, it is rock—limestone, to be precise.

For nearly 2,000 years, the Yapese have used large stone wheels to pay for major purchases, such

as land, canoes, and permission to marry. Yap is a U.S. trust territory, and the dollar is used in grocery

stores and gas stations. But reliance on stone money, called rai stones, continues.

The people of Yap have been using stone money ever since a Yapese warrior named Anagumang

first brought the huge stones over from limestone caverns on neighboring Palau, some 1,500 to 2,000

years ago. Inspired by the moon, he fashioned the stones into large circles. The residents of Palau required

Yapese to pay in beads, coconuts, and copra for the privilege of quarrying. Yap has no limestone, and it

was viewed by the Yapese as an exotic luxury, much like gold and diamonds are to the rest of the world.

Every village chief wanted a bigger stone than his rivals.

The discs took years to carve, and the journey to bring such massive objects back to Yap, in

wooden canoes through rough seas, was an extremely dangerous one. Many boats sank. Sailors drowned,

and hundreds of enormous rocks sunk to the ocean floor.

Human nature being what it is, the danger only increased the demand. The worth of stone money

doesn’t depend on size. Instead, the pieces are valued by how hard it was to get them to the island. The

earliest stones, brought by war canoe by Anagumang and his descendants, are the most precious because

they cost so many lives to bring in. Although the heavily laden Yapese canoes were fitted with outriggers,

they often capsized during the 280-mile ocean voyage from Palau.

Next in value are some stones cut on Palau in the 1870s by David Dean O’Keffe, a shipwrecked

American sailor who escaped from the island and returned later with a Chinese junk. O’Keffe, who

helped transport the boulders in return for Yapese help in processing dried coconut, ultimately ran the

island as a self-styled emperor. Finally, there are a few mechanically chiseled stone wheels brought in

without problems by German traders in the late 1800s and early 1900s. But the value of these is much

lower than the older stones. The Yapese can tell the difference—many of the stones had (and still have)

individual names.

Rai stones are used in social transactions like marriages, inheritance, political deals, even ransom

in battle. The largest are 10 feet in diameter and weigh 4 tons. Some of the smaller stones are about the

size of a saucer. These smaller “coins” are everyday money, used to buy fish and pigs.

Yapese lean the stone wheels against their houses or prop up rows of them in village “banks.”

Each has a hole in the center so it can be slipped onto a tree trunk and carried. It takes 20 people to lift

some wheels.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-71

By custom, the stones are worthless when broken. Rather than risk a broken stone, Yapese tend to

leave the larger stones where they are and make a mental accounting that the ownership has been trans-

ferred—much as gold bars used in international transactions change hands without leaving the vault of the

New York Federal Reserve Bank.

There are some decided advantages to using massive stones for money. They are immune to

black-market trading, are impossible to counterfeit, and pose formidable obstacles to pickpockets. With

only about 6,600 stone wheels remaining on the island, the money supply stays level. Stone wheels don’t

make good pocket money, so for small transactions, Yapese use other forms of currency. In addition to

U.S. dollars, beer is widely used for trading.

Stone money has its limits. Most of the island’s few retail stores won’t accept it for general mer-

chandise. But stone money remains and important part of Yapese traditions. There are instances in Yap

where you cannot use U.S. money. One is the settling of disputes. If a Yapese wants to settle an argument,

he brings his adversary stone money as a token. The apology is accepted without question.

Stone money even figured in international diplomacy. Micronesia president Tosiho Nakayama

brought a stone disk when he visited the United States in 1984. Officials say Nakayama intended the

stone as Micronesia’s symbolic contribution toward reducing the U.S. budget deficit.

lecture enhancer 20-2

LEGISLATORS QUESTION THE PENNY’S NEED

There are many today who feel that the time has come to retire the penny even though it has been

a mainstay of American currency for centuries. The venerable Abraham Lincoln-emblazoned coin has

without a doubt seen better times. In 1913 it possessed 25 times more purchasing power than it does cur-

rently. The penny also used to be profitable to produce. In 1990 it cost 0.6¢ to make one of the copper-

coated coins, resulting in a yield of 0.4¢ per penny. Producing the penny hasn’t been profitable since

2006, however, and now each 1¢ coin costs 2¢ to mint.

In his 2013 budget, President Obama proposed that the government explore new ways to structure

currency so that the penny could be discontinued at last. He’s far from the first world leader to suggest

ditching the 1¢ piece. Canada ceased penny circulation on February 4 of this year while Australia has

been penny-free since 1990. The Canadian government estimates it will save $4 million a year by elimi-

nating the coin. After all, so many monetary transactions are conducted electronically these days that cash

itself is becoming increasingly obsolete. If a $20 bill isn’t as powerful as it used to be, what does that

mean for a coin with almost no practical value?

Still, the penny has its fair share of defenders, namely the minters who earn a lot of money pro-

ducing them. These companies and the lobbyists they fund argue that phasing out the 1¢ coin will inflict a

number of adverse effects on the economy. First of all, an unintentional “rounding tax” could occur as

many companies with prices that end in a 9 round their prices up to the nearest nickel. One controversial

1990 study claimed that this could end up costing consumers as much as $1.5 billion over five years.

However, another study in 2006 found that businesses would end up saving $730 million annually by

eliminating the time wasted dealing with the coin in cash transactions. But pro–penny activists do have

one compelling argument on their side. If the penny is phased out, then U.S. currency will become more

dependent on nickels. The 5¢ coin costs 10¢ to produce, negating any savings made by discontinuing the

penny. One solution devised by economists includes eliminating the nickel and rounding all prices to the

nearest dime, but that’s another argument entirely.i

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-72

lecture enhancer 20-3

EURO PORTRAITS

The euro is the currency of 15 European Union nations, but each country is able to customize one

side of the coins that they circulate. The images described below are on the 1–euro coin of the first 11 EU

countries:

Austria: Shows Mozart, who was born and raised in Salzburg

Belgium: Shows Albert II, king of the Belgians since 1993

Finland: Shows the whooper swan, the national bird of Finland

France: Features the motto “liberté, égalité, fraternité”

Germany: Features the eagle, an ancient symbol of the German state

Ireland: Shows a harp, which has been an Irish icon since medieval times

Italy: Shows Da Vinci’s Vitruvian Man, used to map proportion

Luxembourg: Shows Grand Duke Henri, ruler of the world’s last grand duchy

Netherlands: Shows Queen Beatrix, who succeeded her mother in 1980

Portugal: Shows the royal seal used by Portugal’s first king in 1144

Spain: Features King Juan Carlos, Franco’s successor

lecture enhancer 20-4

MONEY FACTS

What Are Pennies Made Of?

Contrary to popular opinion, pennies are no longer made of pure copper. From 1793 to 1837 pen-

Why Do Some Coins Have Grooves on the Edges?

The dollar, half-dollar, quarter, and 10-cent coins were originally produced from precious metals

(gold and silver). Grooved, or “reeded,” edges were added to deter counterfeiting and stop the filing down

Why Are Certain Presidents Chosen for Certain Coins?

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-73

The presidents who appear on the front side of circulating coins are all selected by Congress in

recognition of their service to the country. The Lincoln cent was issued in 1909 to commemorate the

birth. Following President John Kennedy’s assassination in 1963, the Treasury issued a new 50-cent

piece bearing his portrait in February 1964.

How Many Coins Are Minted Each Year?

The total number of coins minted in 2005 is given below:

• 1¢ 7,700,050,500

• 50¢ 7,300,000

• $1 5,040,000

How Much Gold Is Stored in Fort Knox?

The U.S. Bullion Depository at Fort Knox, Kentucky, currently holds 147.3 million ounces. The

highest gold holdings occurred in December 1941—649.6 million ounces. The only gold that is ever re-

moved is a small sample used to test the purity of the gold in routine audits. The gold is held as an asset

of the United States and has a book value of $42.22 per ounce. Each gold bar is 7 inches by 3 5/8 inches

(Critical Thinking Exercise 20-2, “Test Your Knowledge of Money,” on page 20.80 also deals

with this topic.)

lecture enhancer 20-5

THE ENDURING POWER OF THE DOLLAR

The stock market crash of 2008 sent shockwaves across the world’s economies, leading many to

speculate about the future of American financial policy on the global stage. In the eyes of many experts at

the time, the U.S. dollar was especially at risk of losing its decades-long dominance. After all, the inferno

of the financial crisis spread so fast because many nations measure their own currency against the dollar.

When its value plummeted, so did countless other currencies.

The debacle led to a drastic loss of faith in the almighty dollar. Leaders in Beijing, Moscow and

other developed nations vowed to find a replacement for it, fearing that America’s ailing economy would

continue to infect the entire world if the dollar remained dominant. Emerging economies echoed the sen-

timent as well. With its reputation suffering and value dropping fast, the outlook for the greenback was

not looking good.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-74

Fast forward six years later, however, and the dollar remains the world’s most powerful banknote.

In fact, its value compared to other currencies recently hit a four-year high as most nations continue to

depend on the dollar for their reserve cash. What’s more, policymakers who initially called for a change

have more or less ignored their own advice. China, for instance, now holds $1.27 trillion in U.S. Treasury

securities, a 75 percent jump from 2008. While the dollar’s resurgence can be partly credited to robust

economic growth, the simple truth is that no other currency could feasibly replace it. While the euro was

once tapped as a possible successor, the currency lost many supporters amidst the chaos of the continent’s

sovereign debt crisis. In terms of the future, China and Russia plan to increase the value of their curren-

cies by conducting more trade in yuan and rubles, respectively. The dollar could take some damage if

more nations adapt similar policies, but even then the effects of those plans would not be felt for many

years. So at least for the moment, the color of much of the world’s money will remain green.iii

lecture enhancer 20-6

WRENCHING INFLATION OUT OF THE ECONOMY

The Federal Reserve’s primary function is to control the money supply. It uses its tools to in-

crease or decrease the money supply in response to changing economic conditions. When the economy is

slowing, the Fed increases the money supply, which results in lower interest rates and more investment.

When the economy is overheated, the Fed takes money out of circulation, driving up interest rates.

But during the late 1970s, the economic conditions were more complicated. The economy was

less than robust—the decade saw a series of economic dips—but at the same time, inflation was driving

up prices at an alarming rate. The combination became known as “stagflation.” In 1979, the inflation rate

was 14.6%. A dollar at the beginning of the year would be worth less than 85cents by the end of the year.

Prices increased rapidly, followed by wages. Because of the declining value of money, consumers rushed

out to buy products before prices increased. More money chasing a fixed amount of goods drove inflation

up still further.

During the 1970s, the Fed managed the economy with an eye on interest rates. If interest rates in-

creased, the Fed put more money into circulation. The goal was a stable interest rate to provide equilibri-

um in nation’s economy.

In 1980, President Jimmy Carter appointed Paul Volcker as chair of the Federal Reserve with a

mandate to stabilize inflation. Volcker brought a radical new philosophy to the Fed leadership. Instead of

using interest rates to control the economy, he believed that the only hope for stopping inflation was to

control inflation’s fuel—the money in circulation.

The Fed immediately put the brakes on the money supply. Then it relied on basic laws of supply

and demand to set the price of the fixed amount of money in circulation. With less money created, the

existing money in circulation became more valuable. In order to secure financing, businesses had to pay

more for the money they needed and the cost of money (the interest rate) soared.

By 1981, the prime interest rate peaked at 21.5%. The high interest rate dramatically affected all

businesses activity, but the housing market was hit especially hard. The difference between a mortgage at

8% and a mortgage at 14% amounted to hundreds of dollars a month in increased mortgage expense.

Realtors and homeowners scrambled to find creative financing options to move property. The high inter-

est rates also brought business expansion to a halt, throwing the economy into recession.

Volcker’s Fed held fast to its fixed money philosophy. By 1982, it succeeded in reducing the in-

flation rate to 3.9%, but the cost was high. The U.S. unemployment rate that year climbed to 9.7%. Al-

most 1 in 10 workers was out of a job.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-75

The economy gradually stabilized, and interest rates dropped steadily. The public had learned the

lesson—they no longer expected prices to soar, and pressure on wages gradually decreased. Although

President Reagan has been credited with reining in inflation, the true credit goes to Fed chair Paul

Volcker, appointed by the previous Democratic president.

lecture enhancer 20-7

GOLDSMITH BANKING

Many economists believe that modern money and banking have their roots in medieval Europe.

Toward the end of the Middle Ages, Europe was a dangerous place to live, especially if one had gold and

silver coins so attractive to bandits. Most villages had only one institution that could safely store precious

metal—the village goldsmith. The goldsmiths, makers and sellers of plate and jewelry, flourished in the

1500s after the monasteries were dissolved, increasing the available supplies of gold.

Many goldsmiths developed strong connections with the monarchy, and most began to take in

valuables for safekeeping in their vaults. The locals also brought their gold and silver to the goldsmith’s

vault. In exchange, the goldsmith would write a receipt stating that Joe Nobleman had 15 gold coins on

deposit. When local sales transactions were made, the villager and merchant would go to the goldsmith

shop and withdraw the needed amount of coins. Often, the merchant would turn around and leave the

same coins with the goldsmith for safety.

Inevitably, the inconvenience of meeting and physically exchanging gold coins led villagers to

trade not coins, but rather the receipts for coins from the goldsmith. These receipts circulated in the area,

with all buyers and sellers aware that the paper could be traded at any time for the underlying precious

metal. Some enterprising goldsmith eventually noticed that the gold he had in storage rarely left the vault,

and one gold coin was like every other gold coin. From that point, it was a simple step to loan part of the

gold in storage to others, for a fee. In its earliest form, we have the first paper money and the first bank

loan with interest.

By 1677, there were 44 goldsmith bankers in London. Two of the oldest surviving banks, Coutts

& Co and Child & Co, which originated as goldsmith bankers, continue to operate as part of The Royal

Bank of Scotland Group today.

Incidentally, paper money was not developed first in Europe, but in China, probably during the

600s A.D. The Italian trader Marco Polo traveled to China in the 1200s and was amazed to see the Chi-

nese using paper money instead of coins.iv

lecture enhancer 20-8

CREDIT UNIONS BECOME MORE LIKE BANKS

The Great Recession soured millions of people’s relationships with traditional banks, driving

many to entrust their money with credit unions instead. Along with incessant media coverage of their

questionable dealings, banks at the time had to contend with consumer outrage about hidden fees and su-

persized overdraft penalties. As a result, credit unions appeared to be safe and sensible money managers

compared to their colossal, unscrupulous counterparts on Wall Street. Plus, credit unions offered perks

like free checking, friendly staff, and financial services not available at many of the nation’s troubled in-

stitutions.

Nearly five years on, however, credit unions are beginning to behave more and more like tradi-

tional banks. In 2010 78 percent of credit unions offered free checking. Today that number stands at 72

percent and dropping. The change can be partly blamed on a similar drop in credit unions themselves. 105