Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-46

PPT 20-36

Smart Cards

SMART CARDS

20-36

LO 20-6

• Smart Card — A

combination of a credit card,

debit card, phone card,

driver’s license, and more.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-47

a. Transfer funds from one account to another.

b. Pay bills.

c. Check account balances.

d. Apply for a car loan or mortgage.

e. Buy and sell stocks and bonds.

2. Internet banks such as E*Trade Bank offer online

banking only, not physical branches.

a. They can offer slightly higher interest rates

and lower fees.

b. Some people are nervous about online securi-

ty and fear putting their money into online

banks.

c. Others want to talk to a banking professional

in person.

learning objective 7

Evaluate the role and importance of international banking, the World Bank,

and the International Monetary Fund.

VII. INTERNATIONAL BANKING AND BANKING

SERVICES

A. Banks help businesses conduct business in other

countries by providing three services.

1. A LETTER OF CREDIT is a promise by the bank

to pay the seller a given amount if certain condi-

tions are met.

2. A BANKER’S ACCEPTANCE is a promise that

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-48

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-49

the bank will pay some specified amount at a par-

ticular time.

3 CURRENCY EXCHANGE is the exchange of one

country’s currency for another country’s currency.

4. ATMs now may provide foreign currency.

B. LEADERS IN INTERNATIONAL BANKING

1. In the future, many crucial financial issues will be

international in scope.

2. Today’s money markets form a GLOBAL MAR-

KET SYSTEM.

a. Large international banks make investments

in any country where they can earn maximum

return.

b. World economies are linked into ONE IN-

TERRELATED SYSTEM with NO REGULA-

TORY CONTROL.

c. American firms must compete for funds with

firms all over the world.

3. Banking is no longer a domestic issue—it is an in-

ternational issue.

4. The world economy has evolved, financed by in-

ternational banks.

C. THE WORLD BANK AND THE INTERNATIONAL

MONETARY FUND (IMF)

1. The World Bank and the IMF are twin intergov-

ernmental pillars that support the structure of the

world’s banking community.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-50

PPT 20-37

Making Transactions in Other

Countries

MAKING TRANSACTIONS in

OTHER COUNTRIES

20-37

LO 20-7

• Letter of Credit — A promise by the bank to pay the

seller a given amount if certain conditions are met.

• Banker’s Acceptance — A promise the bank will

pay some specified amount at a particular time.

• Money exchange allows companies to go to a

bank and exchange currencies to use in a

particular country (i.e. dollars for euros).

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-51

2. The WORLD BANK is the bank primarily re-

sponsible for financing economic development; it

is also known as the INTERNATIONAL BANK

FOR RECONSTRUCTION AND DEVELOP-

MENT.

a. Today, most of the money is lent to develop-

ing nations to raise productivity and raise the

standard of living.

b. Recently, the World Bank has received con-

siderable criticism regarding human rights,

AIDS, and the environment.

c. Some want the bank to forgive the debts of

less developed countries or stop making

loans until the country makes economic re-

forms.

3. The INTERNATIONAL MONETARY FUND

(IMF) is an organization that assists the smooth

flow of money among nations.

a. About 185 countries are voluntary members

of the IMF.

b. It requires members to allow their own mon-

ey to be exchanged for foreign currencies

freely and keep the IMF informed about

changes in monetary policy.

c. The IMF is not primarily a lending institution,

rather an OVERSEER of member countries

monetary and exchange rate policies.

d. The IMF has allowed some countries like

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-52

PPT 20-38

Leading Institutions in International

Banking

LEADING INSTITUTIONS in

INTERNATIONAL BANKING

20-38

LO 20-7

• World Bank — Lends most of its

money to less-developed nations to

improve their productivity and help

raise standards of living and quality of

life.

• International Monetary Fund

(IMF) — Fosters cooperative

monetary policies that stabilize the

exchange of one national currency for

another. About 188 countries are a

part of the IMF.

REACHING BEYOND

our borders

PPT 20-39

New Day, New Issues Across the

Globe

NEW DAY, NEW ISSUES

ACROSS the GLOBE

20-39

• The IMF and the World Bank are both trying to come up

with answers to the global issues that have become very

serious.

• Christine Lagarde, managing director of the IMF, fears

the financial crisis did lasting harm to the potential pace

of growth in many global economies.

• The IMF and World Bank are both trying to solve key

global issues before there is another serious crisis.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-53

Brazil, South Korea, and Turkey to put up

barriers to protect their currencies from infla-

tion.

VIII. SUMMARY

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-54

test

prep

PPT 20-40

Test Prep

TEST PREP

20-40

• What are some of the causes for the banking

crisis?

• What is the role of the FDIC?

• How does a debit card differ from a credit card?

• What is the World Bank and what does it do?

• What is the IMF and what does it do?

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-55

PowerPoint slide notes

PPT 20-1

Chapter Title

Copyright © 2015 by the McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Money,

Financial

Institutions,

and the Federal

Reserve

CHAPTER 20

PPT 20-2

Learning Objectives

LEARNING OBJECTIVES

20-2

1. Explain what money is and what makes money

useful.

2. Describe how the Federal Reserve controls the

money supply.

3. Trace the history of banking and the Federal

Reserve System.

4. Classify the various institutions in the U.S. banking

system.

PPT 20-3

Learning Objectives

LEARNING OBJECTIVES

20-3

5. Briefly trace the causes of the banking crisis, and

explain how the government protects your funds

during such crises.

6. Describe how technology helps make banking more

efficient.

7. Evaluate the role and importance of international

banking, the World Bank, and the International

Monetary Fund.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-56

PPT 20-4

Janet Yellen

JANET YELLEN

Federal Reserve

20-4

• The first female chair of the

Federal Reserve.

• Earned her doctorate in

economics from Yale and

was appointed to the Federal

Reserve Board of Governors

by President Clinton.

• Almost every factor related to

the economy is influenced by

the decisions she makes.

PPT 20-5

Name That Company

NAME that COMPANY

20-5

This company recently opened an online store using

a new form of money.

Name that company and what currency it uses!

Company: Mango

PPT 20-6

What’s Money?

• Money — Anything people generally accept as

payment for goods and services.

WHAT’S MONEY?

20-6

LO 20-1

• Barter — The direct trading of

goods or services for other

goods or services.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-57

PPT 20-7

Standards for a Useful Form of Money

STANDARDS for a

USEFUL FORM of MONEY

20-7

LO 20-1

• Portability

• Divisibility

• Stability

• Durability

• Uniqueness

The new $100 bill has features like a 3-D ribbon, as well

as ink with microscopic flakes that shift color.

PPT 20-8

The Bitcoin is in the Mail

The BITCOIN is in the MAIL

20-8

• Bitcoin is a digital currency

created in 2008.

• It is attractive to many users

because there is no central

regulating authority.

• Transactions are between only

two people without middlemen.

• This, however, makes valuing

Bitcoin difficult.

PPT 20-9

The Money Supply

The MONEY SUPPLY

20-9

LO 20-2

• Money Supply — The amount of money the Federal

Reserve makes available for people. The money

supply is referred to as:

– M1 — Money that can be accessed quickly (coins,

paper money, travelers

’

checks, etc.).

– M2 — M1 + money that may take a little time to

obtain (savings accounts, mutual funds, etc.).

– M3 — M2 + big deposits like institutional money

market funds.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-58

PPT 20-10

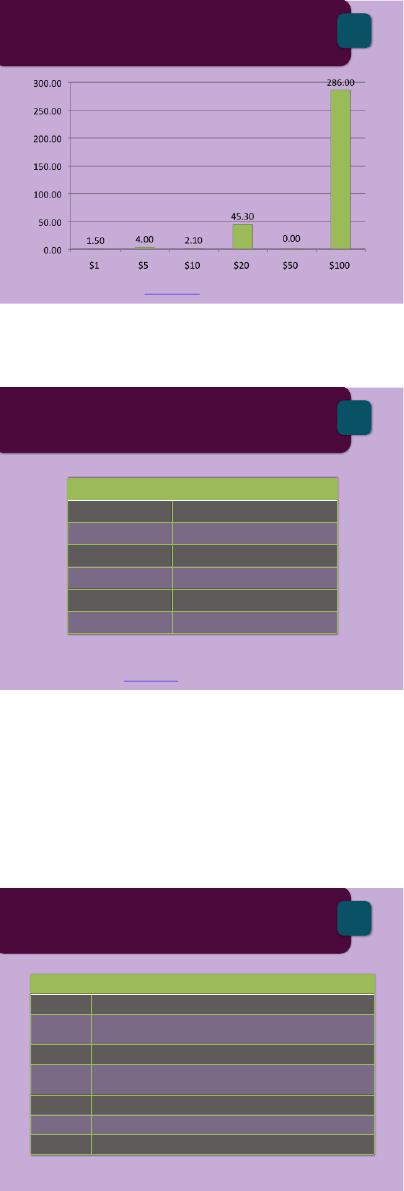

New Money

NEW MONEY

Paper Money Printed in 2010 (In $ Billions)

Source: Bloomberg Businessweek, www.businessweek.com, accessed November 2014. 20-10

LO 20-2

1. This slide shows the value of different bills printed

in 2010.

2. In 2010 over 1 billion $1 bills, 2 billion $20 bills,

and over 2 billion $100 bills were printed.

3. Most of the value of U.S. currency is $100 bills.

4. In 2010 the U.S. printed more bills in every catego-

ry but $1s and $50s when compared to 2009.

PPT 20-11

How Long Does Paper Money Last?

HOW LONG DOES

PAPER MONEY LAST?

Source: Federal Reserve, www.federalreserve.gov, accessed November 2014. 20-11

Bill How Long it Lasts

$1 21 Months

$5 16 Months

$10 18 Months

$20 24 Months

$50 55 Months

$100 89 Months

LO 20-2

1. This slide gives the students an idea of the life

span of paper money in circulation.

2. The largest denomination ever printed was a

$100,000 gold certificate.

3. Share with students some interesting facts regard-

ing U.S. currency:

• Originally, U.S. currency included denomi-

nations of $500, $1,000, $5,000, and

$10,000. No currency printed today is great-

er than $100.

• The percentage of U.S. counterfeit currency

in circulation is estimated to be .02%.

• U.S. currency bills are 2.61 inches wide, 6.14

inches long, and .0043 inch thick, and weigh

1 gram.

• It costs 4.2 cents to produce a U.S. bill.

PPT 20-12

Money Milestones

MONEY MILESTONES

20-12

Year Milestone

1956 Congress set the minimum wage at $1 an hour

1960 $10 million presidential campaign by candidate Richard Nixon

1985 $100,000 bottle of wine sold at auction at Christie’s

1995 $1 million cost for a 30-second commercial during Super Bowl XXIX

2001 $10 movie ticket in New York

2004 $100 million Picasso painting sold at Sotheby’s

2007 $1 billion stadium built in London (Wembley)

LO 20-2

1. This slide illustrates some interesting dates re-

garding U.S. money

2. Have students look through the dates. Which do

they find most interesting or surprising and why?

3. Ask students: How do some of the amounts listed

compare to today?

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-59

PPT 20-13

Money Facts

MONEY FACTS

What You Might Not Know About What’s in Your Wallet

Source: Fast Company, wwww.fastcompany.com, accessed November 2014. 20-13

LO 20-2

• In 2009, the U.S. printed 26,000,000 bills a day!

• Each penny costs 1.6¢ and each nickel costs 6¢

to make.

• The most-tracked bill on WheresGeorge.com has

travelled over 4,100 miles in 3 years!

• 2/3 of all U.S. $100 bills are outside the U.S.

• 90% of paper money has traces of cocaine!

PPT 20-14

Exchanging Money Globally

EXCHANGING MONEY GLOBALLY

20-14

LO 20-2

• Falling dollar value: The amount of goods and

services you can buy with a dollar decreases.

• Rising dollar value: The amount of goods and

services you can buy with a dollar increases.

• What makes the dollar fall or rise is the position of

the U.S. economy relative to other global

economies.

Since the United States abandoned the gold standard, the

U.S. dollar has depreciated by approximately 90%.

PPT 20-15

The Impact of a Falling Dollar

The IMPACT of a

FALLING DOLLAR

• Overseas demand for U.S. products rise.

• A favorable exchange rate for U.S. companies

increases profits in foreign markets.

20-15

LO 20-2

• U.S. tourism increases

which is good for hotels,

resorts, theme parks, and

retailers that serve

international travelers.

1. This slide highlights some of the issues related to a

falling dollar.

2. While these points are positive, the long term impli-

cations of a falling dollar are more serious.

3. A declining dollar will eventually result in the fol-

lowing:

• Higher interest rates on government and con-

sumer debt.

• Higher inflation due to a rise in the price of

imports, and commodity prices increase since

most are priced in terms of U.S. dollars.

Chapter 20 – Money, Financial Institutions, and the Federal Reserve

20-60

PPT 20-16

Five Major Parts of the Federal Reserve

System

FIVE MAJOR PARTS of the

FEDERAL RESERVE SYSTEM

20-16

LO 20-2

1. The Board of Governors

2. The Federal Open

Market Committee

3. 12 Federal Reserve

Banks

4. 3 Advisory Councils

5. The member banks of

the system

The Federal Reserve is a quasi-governmental agency not

under the direct control of the U.S. government.

PPT 20-17

The 12 Federal Reserve District Banks

The 12 FEDERAL RESERVE

DISTRICT BANKS

20-17

LO 20-2

PPT 20-18

Managing the Money Supply

MANAGING the MONEY SUPPLY

20-18

LO 20-2