Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-76

PPT 19-41

Understanding Stock Quotations

UNDERSTANDING STOCK

QUOTATIONS

19-41

LO 19-6

Stock quotations are now readily available on numerous

websites.

PPT 19-42

Top Financial News and Research

Sites

TOP FINANICIAL NEWS and

RESEARCH SITES

19-42

LO 19-6

• Yahoo Finance

• DailyFinance

• MSN Money

• Forbes

• Dow Jones & Co.

1. Financial information is now readily available online.

This slide lists some of the sites where information can

be easily gathered.

2. If time allows, encourage students to visit these web

sites and evaluate their usefulness.

3. Ask students: Which of these web sites was the best?

Why would it be a good idea to consult more than one

of these web sites before deciding to invest?

PPT 19-43

Important Bond Questions

IMPORTANT BOND QUESTIONS

19-43

• Junk Bonds — Bonds that are high-risk and have

high default rates.

LO 19-7

• First-time bond investors generally ask two

questions:

– Do you have to hold a bond until the maturity date?

– How can I assess the investment risk of a particular

bond issue?

A junk bond has a rating of BB or less.

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-77

PPT 19-44

Understanding Bond Quotations

UNDERSTANDING BOND

QUOTATIONS

19-44

LO 19-7

PPT 19-45

Investing in Mutual Funds and

Exchange-Traded Funds

INVESTING in MUTUAL FUNDS

and EXCHANGE-TRADED FUNDS

19-45

LO 19-8

• Mutual Fund — An organization the buys stocks and

bonds and then sells shares in those securities to the

public. The fund pools investors

’

money and buys

stocks according to the fund

’

s purpose.

• Exchange-Traded Fund (ETF) — Collections of

stocks and bonds that are traded on securities

exchanges, but are traded more like individual stocks

than mutual funds.

PPT 19-46

What Mutual Funds Can Learn from

KaChing

WHAT MUTUAL FUNDS CAN

LEARN FROM KaChing

Source: Fast Company, www.fastcompany.com, accessed November 2014. 19-46

LO 19-8

1. Reform the ratings

system

2. Give information for

free

3. Cut out useless fees

4. Be transparent

5. Share insights

1. KaChing is a web site where professional investors

share everything about their portfolios.

2. Fast Company shows how KaChing can help investors

understand what they’re getting into.

3. The magazine uses the example of Morningstar and

how most of its portfolio managers didn’t invest in

their own funds. Potential investors would like to

know information like that!

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-78

PPT 19-47

Percentage of Households Owning

Mutual Funds

PERCENTAGE of HOUSEHOLDS

OWNING MUTUAL FUNDS

Source: Investment Company Institute Factbook. 19-47

Year % of Households

1980 5%

1990 24%

2000 43%

2005 42%

2010 48%

LO 19-8

1. This slide presents the percentage of US households

owning mutual funds over the past 30 years.

2. Ask the students: Do you or your parents own mutual

funds? How did they get involved in purchasing them,

and what type of research do they do before buying

them? Did they develop investment objectives or was

it based on some tip or advice?

3. It should be pointed out to the students that people

may get into investing for the right reasons and with

right intentions (retirement, savings for college, vaca-

tions, home buying, etc.). However, it is very im-

portant to maintain discipline. Many people, if not

most, deviate from these investment objectives and

start to invest based on the so-called “hot tip.” Mutual

funds should be treated as investments which you

commit to based on researched information and not

hot tip or quick hit gambling.

PPT 19-48

Varieties of ETFs

VARIETIES of ETFs

Source: Schwab and E*Trade. 19-48

ETF Description

Traditional

Most common; include large U.S.

stocks, small U.S. stocks,

international stocks, or investment-

grade bonds.

Niche

Focus on an individual sector like

healthcare, high-yield bonds, or a

single country.

Exotic

Invest in unusual, more volatile

sectors such as commodities like

gold and concepts like clean

technology.

LO 19-8

1. This slide lists three varieties of ETFs that are availa-

ble.

2. ETFs have numerous benefits when compared to mu-

tual funds. If time permits, have students prepare a list

of and/or discuss the advantages of ETFs. (Transpar-

ent pricing, lower fees, and returns at least equal to the

index that the ETF tracks, are just some of the ad-

vantages students might discuss.)

3. Traditional ETFs include: SPY which tracks the S&P

500 and TIP which tracks inflation protected govern-

ment bonds.

4. Niche ETFs include: IXJ which tracks the S&P Glob-

al Healthcare Sector.

5. Exotic ETFs include: FXA which tracks the Australi-

an Dollar and GLD which tracks the price of gold.

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-79

PPT 19-49

Understanding Mutual Fund Quotations

UNDERSTANDING

MUTUAL FUND QUOTATIONS

19-49

LO 19-8

The price per share for a mutual fund is referred to as the

net asset value or NAV.

PPT 19-50

Comparing Investments

COMPARING INVESTMENTS

19-50

LO 19-8

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-80

PPT 19-51

Test Prep

TEST PREP

19-51

• What is a stock split? Why do companies

sometimes split their stock?

• What does buying stock on margin mean?

• What are mutual funds and ETFs?

• What is the key benefit to investors in investing in

a mutual fund or ETF?

1. When a company splits its stock 2 for 1 the sharehold-

ers receive two shares of stock for each share they

own. The current share price is cut in half, so the num-

ber of shares increases, the total value of the invest-

ment remains the same. The board may decide to split

a company’s stock 2 for 1, 3 for 2 or any other ratio

they determine is appropriate. The reason that a com-

pany splits its stock is to reduce the price of the stock

which will hopefully increase the demand.

2. When an investor buys on margin, they use money

borrowed from their broker to purchase stock.

3. A mutual fund is an investment fund that buys stocks

and bonds then sells shares in those securities to the

public. The pooling of funds allows small investors to

invest in a broader selection of stocks and bonds.

Most mutual funds are professionally managed. ETFs

are similar to mutual funds, but are traded on exchang-

es like individual stocks and are passively managed.

4. The key benefit to investing in a mutual fund or ETF is

that the investor gets instant diversification.

PPT 19-52

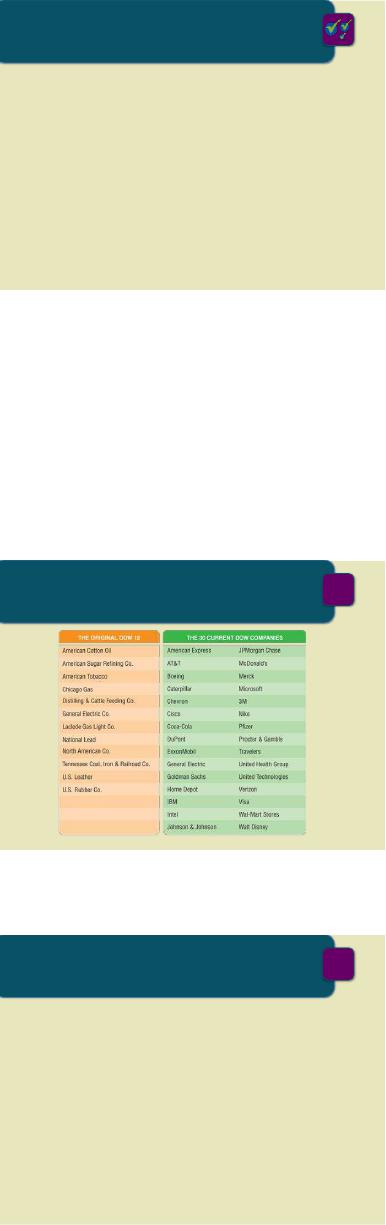

The Dow

The DOW

19-52

LO 19-9

PPT 19-53

Key Stock Market Indicators

KEY STOCK MARKET

INDICATORS

19-53

LO 19-9

• Dow Jones Industrial Average — The average

cost of 30 selected industrial stocks.

• Critics say the 30-company Dow is too small a

sample and suggest following the S&P 500.

• S&P 500 tracks the performance of 400

industrial, 40 financial, 40 public utility, and 20

transportation stocks.

1. The Dow Jones Industrial Average is the oldest index

which was originally created in 1896 by Charles Dow

and Edward Jones.

2. The original average had twelve companies, one of

which, GE, is still in the Dow Jones Industrial average

after all these years.

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-81

PPT 19-54

Market Turmoil

• The stock market has its shares of ups and

downs:

MARKET TURMOIL

19-54

LO 19-9

– October 29, 1929 – Black

Tuesday; the market lost 13% of

its value.

– October 19, 1987 – The market

suffered its worst one-day drop

when it lost 22% of its value.

– October 27, 1997 – Fears of an

economic crisis in Asia cause

widespread panic and losses.

PPT 19-55

Turmoil in the 2000s

TURMOIL in the 2000s

19-55

LO 19-9

• The market collapsed into a deep decline in

2000-2002 when the dot-com bubble burst.

– Investors lost $7 trillion in market value.

• Starting in 2008, the collapse of the real estate

market sent financial markets into panic.

– The U.S. government made significant investments in

private banks and offered a large stimulus package to re–

energize the economy.

PPT 19-56

The Wall Street of Now

The WALL STREET of NOW

Source: Bloomberg Businessweek, www.businessweek.com, accessed November 2014. 19-56

Then Now

Town Car Transportation Uber

21 Club Restaurant Subway

The Penthouse Club After Hours Dave & Buster’s

Johnny Walker Blue

($200) Drink Bud Light

($5)

American Express

Black Card Metrocard

Bottle Service Pastime Trivia Night

LO 19-9

1. Since the economic crisis hit, Wall Street has taken

many cuts.

2. This slide shows how Bloomberg Businessweek sees

the new way for Manhattan bankers to unwind.

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-82

PPT 19-57

The Ups and Downs of the Market

The UPS and DOWNS

of the MARKET

19-57

LO 19-9

• Program Trading — Giving instructions to

computers to automatically sell if the price of a stock

dips to a certain point to avoid potential losses.

• Analysts believe program trading caused the

turmoil in 1987.

• The exchanges created mechanisms to restrict

program trading.

1. The downturn of 1987 prompted the U.S. exchanges to

create mechanisms called curbs and circuit breakers to

restrict program trading whenever the market moves

up or down by a large number of points in a trading

day. A key computer is turned off and program trading

is halted.

2. If you watch programming on CNBC or MSNBC,

you’ll see the phrase “curbs in” appear on the screen.

PPT 19-58

Who’s at Fault for the Economic Crisis?

WHO’S at FAULT for the

ECONOMIC CRISIS?

Source: Fortune Magazine, www.fortune.com, accessed November 2014. 19-58

LO 19-9

• Wall Street – Issued exotic securities; paid excessive

compensation based on bonuses; and investment banks got

the SEC to relax capital requirements.

• Main Street – Americans lived beyond their means;

lenders gave favorable loans to homebuilders; greedy

homeowners took out equity loans; and teaser mortgage

rates let people live large.

• Washington – Gramm-Leach-Billey Act allowed

commercial and investment banks to partner; housing

interest rates were kept low; and Community Reinvestment

Act forced lending to people with bad credit.

1. This slide reviews some of the players in the economic

crisis.

2. Like all complex problems, one group did not cause

this crisis.

3. You could actually include another culprit (not listed

on this slide): worldwide saving surplus. Gulf States,

China, Japan and Brazil all reinvested export earnings

in US dominated assets, primarily government bonds.

This had the effect of keeping interest low, thus allow-

ing consumers and the United States Government (as

well as many state and local governments) to spend

beyond their means, racking up massive consumer and

federal debt.

4. To discuss the crisis ask students: Who’s at fault for

the economic crisis? (When discussing this highly

charged topic it is important to make sure students un-

derstand that the fault lies not just with Wall Street

and Washington, but with consumers including them-

selves.)

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-83

PPT 19-59

Cleaning Up the Street

CLEANING UP the STREET

19-59

LO 19-9

1. Dodd-Frank represents the most sweeping change in

financial regulation since the Great Depression.

2. Although it’s not perfect, the Dodd-Frank Act at least

resolves some of the most pressing issues facing our

economy today, while setting the stage for a stronger

financial future.

PPT 19-60

Test Prep

TEST PREP

19-60

• What does the Dow Jones Industrial Average

measure? Why is it important?

• Why do the 30 companies comprising the Dow

change periodically?

• Explain program trading and the problems it can

create.

1. The Dow Jones Industrial Average is the average price

of 30 specific industrial stocks. It is important because

it allows followers of the market to track the general

direction of the stock market.

2. The Dow will delete and add new companies to the

Dow Jones Industrial Average to reflect increased

economic importance of a particular company or in-

dustry. Recently, Cisco and Travelers replaced Citi

and GM.

3. Program trading occurs when investors give instruc-

tions to their computers to execute a sell order if the

stock price dips to a certain point. Many attribute the

stock market crash of 1987 to program trading as

computer sell orders caused many stocks to fall to in-

credible levels.

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-84

lecture

enhancers

“Play the game for more than you can afford to lose . . . only then will you

learn the game.”

Winston Churchill

“You may know where the market is going, but you can’t possibly know

where it’s going after that.”

Heisenberg Principle of Investment

“Money is made by discounting the obvious and betting on the unexpected.”

George Soros

lecture enhancer 19-1

TWITTER’S IPO VICTORY

When Facebook launched its highly anticipated IPO last year, the upbeat mood among Wall

Street insiders transformed from fanfare to fiasco as the trading day wore on. Misplaced orders, a sky–

high valuation and glitches within the Nasdaq exchange sent the young stock on a downward spiral that

would continue for weeks. While Facebook’s share price has since evened out, the company’s IPO expe-

rience set a clear example of what not to do when debuting a social network on the stock exchange.

Judging from the way Twitter handled its IPO earlier this month the message was received loud

and clear. First of all, the company opted to trade on the New York Stock Exchange rather than the

Nasdaq. Although the latter is the preferred destination for many tech firms, Twitter’s decision paid off as

the NYSE got the stock off and running within 90 minutes of the opening bell. In Facebook’s case,

Nasdaq was late putting the stock up for sale, which caused it to debut with a higher price tag than most

traders had anticipated. Conversely, Twitter hit the market promptly at the expected price of $45.10 per

share and closed just twenty cents below at the end of the day.

But it’s when Twitter debuted that matters just as much as where. Facebook hit the scene in May

2012 when the stock market was undergoing a downturn. Twitter, on the other hand, landed on an ex-

change that had seen 25 percent growth over the year to that date. Furthermore, the company made the

wise decision to debut in November, which is traditionally one of the best months for gains in the market.

Twitter’s good timing goes beyond the macro level, though. Whereas Facebook had been a profitable

company with more than 1 billion users upon its debut, Twitter still held the image of a promising up–

and-comer to which stock speculators flock. All these factors together led to a single-day haul of more

than $2.1 billion in investments and a market capitalization of $25 billion for the San Francisco-based

company. Expect even more firms to follow Twitter’s template as they look for a similarly sized “pop” of

capital from their IPOs.i

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-85

lecture enhancer 19-2

THE TOKYO EXCHANGE TYPING ERROR

Computerized trading systems common on stock exchanges these days have reduced the trade er-

ror rate significantly. Yet, the computers’ infallibility is only as good as the accuracy of the person enter-

ing the information.

In December 2005, the Tokyo Stock Exchange was rocked by an erroneous trade that caused Mi-

zuho Securities to lose at least 27 billion yen ($225 million). The cause of the turmoil was eventually

traced to a trader at Mizuho Securities, who meant to sell 1 share of stock in J-Com Co., a job recruiting

company, for 610,000 yen ($5,041). The trader instead entered a trade of 610,000 shares at 1 yen (less

than a penny).

The enormity of the error should have raised red flags through the exchange. The number of

shares in the order was 41 times greater than the number of J–Com’s shares actually outstanding, but the

Tokyo Stock Exchange processed the order anyway. Mizuho says another trader tried to cancel the order

three times, but the exchange’s policy is not to cancel transactions even if they are executed on erroneous

orders. By the end of the day, Mizuho Financial Group had lost at least 27 billion yen.ii

lecture enhancer 19-3

RATINGS AGENCY DOWNGRADES FRANCE

Credit rating agencies like Standard & Poor’s (S&P) and Moody’s help investors determine the likelihood

that a debtor will be able to repay their debts. These appraisals can make or break the reputations of cor-

porations and even nations. After all, America’s financial clout took a hit when S&P downgraded the

country’s credit to AA+ from AAA. At least the U.S. isn’t alone in its shame, though. Several other prom-

inent countries have had to endure downgrades due to their habits of over-borrowing in the days before

the economic downturn.

Then there are strange cases like France. S&P notched the European nation down to AA+ as well, but not

because it was borrowing beyond the budget. Instead, the agency downgraded France’s credit due to the

policies of its president Francois Hollande. Rather than cutting government spending, the socialist head of

state has elected to fight economic stagnation by raising taxes, especially on corporations and the rich. In

the eyes of S&P, this does nothing but hurt the nation’s efforts towards growth. “We believe the French

government’s reforms to taxation, as well as to product, services, and labor markets, will not substantially

raise France’s medium-term growth prospects,” S&P said. “Furthermore, we believe lower economic

growth is constraining the government’s ability to consolidate public finances.”

While S&P says the downgrade stems from fiscal circumstances, critics like economist Paul

Krugman see it as a political attack. The trend among most ailing European nations has been to adopt aus-

terity policies in order to balance the budget. Rather than cut key social services, however, President Hol-

lande is keeping them afloat with increased tax revenue. Although some in the country have protested the

new policy, the current economic data indicates that France is performing just as well as most of its

neighbors. In fact, the budget deficit has continued its two-year slide downward, and the IMF has predict-

ed France’s GDP will remain relatively stable for the next five years. There are several other countries

with far less attractive statistics that have retained their AAA ratings.iii

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-86

lecture enhancer 19-4

THE DANGERS OF ETFS

It’s no secret that the stock market is an unpredictable entity. Nevertheless, every day savvy in-

vestors the world over try to find a way to consistently and safely earn money through clever investing.

But on the New York Stock Exchange, nothing is assured and even the safest bets have their dark sides.

For instance, exchange-traded funds (ETFs) are bundles of stocks, bonds, or other investments that trade

like a single stock. Many different companies and funds comprise an ETF, but normally they all fall under

one central industry or commodity, such as oil or gold. In this way, ETFs ideally provide an easy and

profitable way to diversify a portfolio.

ETFs have been a hot item on the stock market for the past few years, growing at rate of $1.5 bil-

lion a week and totaling to an estimated $838 billion overall. But as their popularity grows, Wall Street is

increasingly issuing misleading ETFs that contradict the funds’ safe reputation. For one, ETFs are closing

at an alarming rate, with 140 shutting down since 2008. In the 15 years before then, only 10 had closed.

An ETF needs at least $50 million to generate a profit and many disappear due to a lack of investor inter-

est. Although investors don’t lose their money once a fund closes, those looking for ETFs as a solid di-

versification tool instead find themselves saddled with commissions and transfer fees for a new invest-

ment.

Sometimes ETFs fail to perform the same way as the indices or products they track. For example,

an ETF called the PowerShares FTSE RAFI Emerging Markets Portfolio rose 67% in 2009. A solid return

to be sure, except that the collection of stocks it tracked rose 78%. While such tracking errors can occur in

some funds from time to time, they’re becoming especially common in ETFs, which differ from their in-

dices by an average of 1.25%. So although ETFs are still about as safe a bet as one can make on Wall

Street, their reputation is being polluted by the day thanks to miscalculations and increasingly convoluted

bundles of securities.iv

lecture enhancer 19-5

LINEUP CHANGES ON THE DOW JONES

The Dow Jones Industrial average is often considered a bellwether for the economy. This stock

index of 30 large publicly traded American companies offers a snapshot of the nation’s fiscal wellbeing

for analysts and day traders alike. Regardless of its popularity, however, the Dow is hardly perfect. Decid-

ing which companies comprise the index is a delicate process that sometimes omits major players. For

instance, a couple years ago we shared a story in the newsletter about Apple’s absence from the Dow, a

matter that some found inconceivable for a company valued at $415 billion.

While Apple remains too unwieldy for the Dow, strategists at the index determined three compa-

nies that nonetheless reflect growing portions of America’s economy. On September 20 the Dow added

Nike, Visa and Goldman Sachs to its prestigious roster. In order to make room for the new guys, though,

the index decided to ditch Bank of America, Hewlett-Packard and Alcoa on account of their underper-

forming stocks. As the Dow is weighted by price, that means the companies with the highest valued

stocks hold the most sway over the benchmark. The three outgoing companies comprised only 3 percent

of the total average, making their impact on the index as a whole minimal.

Besides booming stock prices, the Dow’s freshman entrants also diversify the index to include a

better mix of industries. But for the companies on the way out, the change merely serves to highlight

Chapter 19 – Using Securities Markets for Financing and Investing Opportunities

19-87

greater problems. Alcoa, a Dow fixture for more than 50 years, left the index after falling 7 percent this

year and selling at a paltry average of about $8 per share. The move represents the Dow’s biggest shakeup

since 2004 when AT&T, Kodak and International Paper made way for Verizon, Pfizer and AIG. Still,

while no doubt a major change, this latest substitution is unlikely to have much of an effect on prices of

individual stocks. “Despite the popularity of the Dow Jones Industrial Average in the press, it’s a lot less

significant than an addition to the Russell 2000 or an addition to the S&P 500, because it‘s just not an in-

dex that institutions benchmark to,” says an analyst at Credit Suisse Group.v

lecture enhancer 19-6

THE DAY THEY CALL “BLACK TUESDAY”

October 29, 1929, “Black Tuesday,” was the day the boom of the 1920s ended. The market slides

of 1987 and 1997 are often compared with this historical watershed.

Few suspected that the go-go era would end so abruptly. Between the spring of 1926 and the

spring of 1929, the Dow Jones Industrial Average had more than doubled. During the summer of 1929, it

increased another 25%. The national economy, while showing signs of weakness, did not discourage the

speculation boom. Investors with as little as 10% cash margin flocked into the market, lured by news of

steadily increasing prices. The DJIA reached a peak of 381 on September 3, 1929.

The Federal Reserve Board made a half-hearted attempt to slow down the expansion, jolting pric-

es down briefly during September, but it was not until October 24, a Thursday, that the slide became a

crash. On that day, nearly 13 million shares changed hands, 56% more than the previous record. As prices

dropped, brokers called investors for more margin, fueling more selling. Only when the nation’s top five

banks agreed to pool their resources to support the market did the hysteria lessen temporarily.

Monday the selling began again, dropping the Dow by one-day record 38 points, fully 13% of the

total market value. There was nothing the banks could do. The next day, Tuesday, October 29, the bottom

dropped out. The Dow dropped 31 more points, on a volume of 16.4 million shares. In two days, the mar-

ket lost almost 25% of its value. Tuesday’s volume record stood for nearly four decades. In five trading

days, the gains of the previous 16 months were wiped out.

By July, 1932, the DJIA had bottomed out at 41, a reduction of nearly 90% from its peak three

years previously. Investors lost more than $74 billion in the collapse. It was not until 1954 that the stock

market managed to regain the ground it lost in those three years.

lecture enhancer 19–

INVESTING IN COMMODITIES

Commodities can be high-risk investments for most investors. Investors willing to speculate in

commodities hope to profit handsomely from the rise and fall of prices of items such as coffee, wheat,

pork bellies (slabs of bacon), petroleum, and other articles of commerce (commodities) that are scheduled

for delivery at a given (future) date. Trading in commodities is not for the novice investor; it demands

much expertise. Small shifts in the prices of certain items can result in significant gains and losses. It’s

estimated, in fact, that 75 to 80% of the investors who speculate in commodities lose money in the long

term.