Chapter 18 – Financial Management

18-61

PPT 18-33

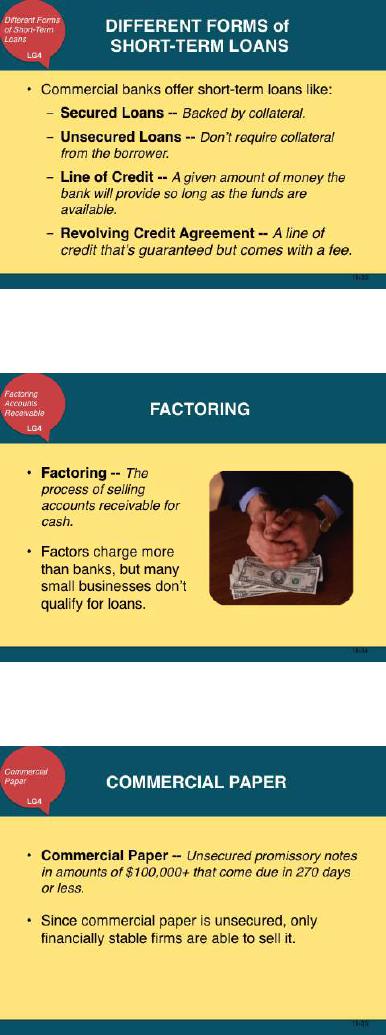

Different Forms of Short-Term Loans

PPT 18-34

Factoring

PPT 18-35

Commercial Paper

1. The commercial paper market is an important

source of funding for financially stable companies.

2. During the financial crisis which started in 2008,

this important market completely shut down, forc-

ing the Federal Reserve to step in and assist many

companies with their short-term financing by pur-

chasing their commercial paper.

Chapter 18 – Financial Management

18-62

PPT 18-36

Credit Cards

PPT 18-37

Ways to Raise Start-Up Capital

1. This slide profiles some of the unique methods

businesses can use to raise capital.

2. Trade credit and factoring are two of the oldest

methods of raising capital. To start a discussion

with students ask the advantages and disadvantages

of using each of these methods.

3. Peer–to-peer lending involves individuals loaning

money to other individuals or businesses thus by-

passing traditional lending outlets.

4. For more information on this new method use loan

statistics from www.lendingclub.com.

PPT 18-38

Progress Assessment

1. 2/10 net 30 means a firm can receive a 2% discount

if the bill is paid within 10 days. If they choose not

to take the discount, the net amount is due in 30

days.

2. Trade credit is buying goods and services now and

paying for them later, while a line of credit is a

given amount of unsecured short term funds a bank

will lend a business, provided the funds are readily

available.

3. A secured loan requires collateral, while an unse-

cured loan doesn’t not.

4. Factoring is the process of sell accounts receivable

for cash. Things to consider in establishing the dis-

count rate are: age of the accounts receivable, the

nature of the business, and the condition of the

economy.

Chapter 18 – Financial Management

18-63

PPT 18-39

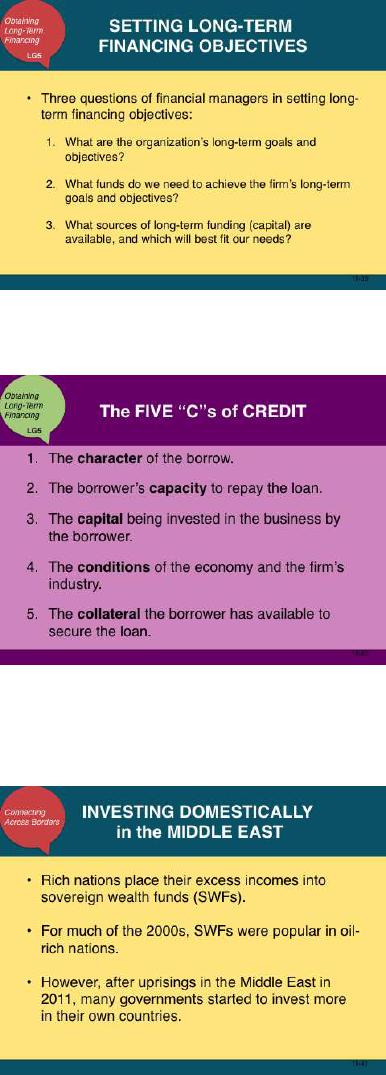

Setting Long-Term Financing

Objectives

PPT 18-40

The Five Cs of Credit

1. This slide highlights the 5 “C”s of credit that lend-

ers use to make decisions.

2. It is essential that lenders make good decisions

when deciding whether or not to loan capital to po-

tential borrowers.

3. Go through each of the C’s and have students eval-

uate how important each one is. Are they equally

important for the lenders to consider? Why or why

not?

4. Ask students: Can you think of any other things the

lenders should consider before loaning money?

(Note: these do not have to be words that start with

C)

PPT 18-41

Investing Domestically in the Middle

East

In 2012, Middle Eastern nations spent less on foreign in-

vestments than they had in years. Instead, they put their

money into improving infrastructure, education and salaries

for workers in their own nations.

Chapter 18 – Financial Management

18-64

PPT 18-42

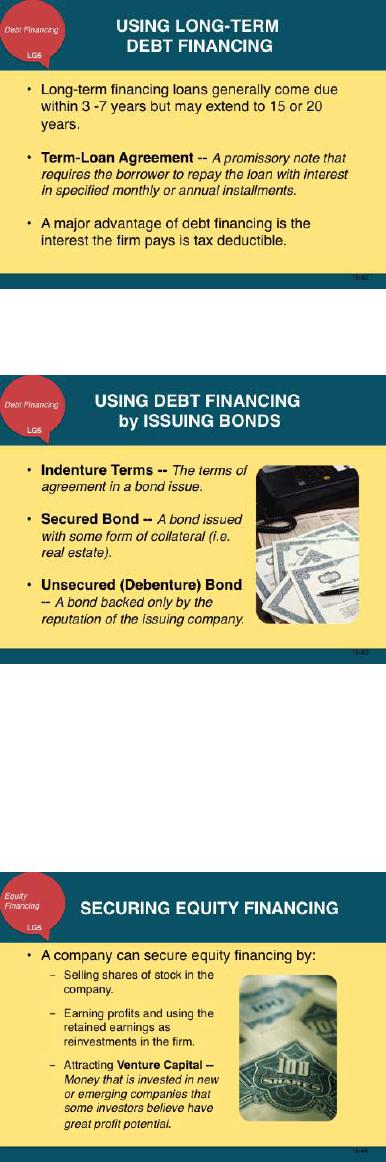

Using Long-Term Debt Financing

Lenders may also require certain restrictions to force the

firm to act responsibly.

PPT 18-43

Using Debt Financing by Issuing Bonds

1. It is critical that students understand bonds are a

form of debt issued by companies.

2. The terms debt, bond, and loan are all four letter

words and basically mean the same thing.

3. Students should walk away from this discussion

knowing that the government and private industry

compete insofar as the sale of bonds to the invest-

ing public. The issue of investor security can easily

be addressed here, as well as the differences in in-

terest rates paid on specific bonds depending on the

issuer. Students should understand that U.S. Gov-

ernment bonds are considered the safest investment

in the bond market. There is a high probability that

students will be familiar with U.S. Government

Savings Bonds, and may in fact have received such

a bond as a gift. They clearly need to understand

the difference between such bonds and issues in-

volving investments in corporate bonds.

PPT 18-44

Securing Equity Financing

Chapter 18 – Financial Management

18-65

PPT 18-45

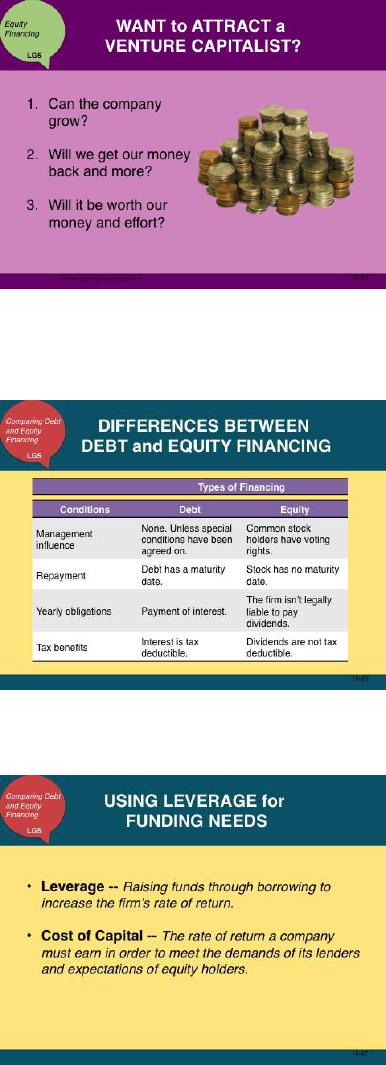

Want to Attract a Venture Capitalist?

1. This slide shows how venture capitalists assess the

many pitches they receive all year.

2. Venture capitalists want to ensure that not only will

they get their money back, but that they will also

earn more than their investment.

3. Why is a question like “Will it be worth our money

and effort?” important to venture capitalists? (VCs

want to make sure there is a large return on their

investment so they can make money and continue

investing in other companies.)

PPT 18-46

Differences between Debt and Equity

Financing

1. This slide is based on Figure 18.6.

2. Financial managers must evaluate the benefits of

issuing debt or equity and then weigh those bene-

fits with the drawbacks.

PPT 18-47

Using Leverage for Funding Needs

Chapter 18 – Financial Management

18-66

PPT 18-48

Lessons of the Financial Crisis

PPT 18-49

Progress Assessment

1. A company could issue and sell bonds or they

could borrow from financial institutions and indi-

viduals.

2. The primary difference between debt financing and

equity financing is that debt must be repaid at ma-

turity while there is no obligation to repay equity

financing. Interest must be paid on debt, while the

company is under no obligation to issue dividends

on equity financing. The interest paid is tax de-

ductible, while dividends are not. Finally, debt

holders do not have the right to vote on company

matters, while equity holders usually do have vot-

ing rights.

3. A business can obtain equity financing from the

sale of company stock, from retained earnings, or

from venture capital firms.

4. Leverage is borrowing funds to invest in expan-

sion, major asset purchases, or research and devel-

opment. Firms use leverage in an effort to increase

the firm’s profit.

Chapter 18 – Financial Management

18-67

lecture

enhancers

“True genius resides in the capacity for evaluation of uncertain, hazardous, and

conflicting information.”

Winston Churchill

“Careful planning is no substitute for dumb luck.”

Dunn’s Law

“Money is made by discounting the obvious and betting on the unexpected.”

George Soros

lecture enhancer 18-1

LEARNVEST TEACHES THE FINANCIAL BASICS

Although women’s average salary still falls short of men’s in the United States, in some major U.S.

cities young women are significantly outearning males. For 20-something women in Dallas, the pay gap

stretches to as much as 20%. As it is for any ambitious person, responsible personal finance management is a

must in order to sustain that success. However, some women reached the highest levels of business only to

realize they didn’t know enough about what to do with their money.

Such was the case for Alexa von Tobel. A Harvard graduate, von Tobel landed a job with Morgan

Stanley shortly after finishing college. As she spent the day managing huge sums of cash and pulling in a

healthy salary, von Tobel became unnerved at how little she knew about tending to her own financial needs.

After all, how could she broker million-dollar deals every day, but lack the knowledge to plan for her own re-

tirement or pay down her debt? Drawing on a wealth of resources and her valuable education, von Tobel even-

tually solved her financial quandary. However, her struggle made her think about all the other women out there

who were just as intelligent and career-minded, but were nonetheless clueless about personal finance.

Recognizing a niche, von Tobel left her big bank job to found LearnVest.com, a website aimed at

making financial literacy relevant and exciting for young women. In her mind female business gurus like Suze

Orman and their $25 advice tomes didn’t resonate with today’s professional females. LearnVest provides in-

formation on everything from mortgages to investing, all filtered through a female-oriented design meant to

echo the stylish pages of Vogue combined with a point-tracking program akin to Weight Watchers. The site

personalizes each user’s experience. The website first asks visitors about their financial goals. If they want to

be better savers, the site provides the fundamentals as well as a series of checklists so the users can track their

progress. After less than a year in operation, LearnVest is attracting a dedicated following. With 350,000 hits a

month, the site has also amassed $5.5 million in venture capital to expand the brand to the nation’s growing

number of career-minded women.i

Chapter 18 – Financial Management

18-68

lecture enhancer 18-2

THE EXPANDING ROLE OF THE CFO

The role of chief financial officer (CFO) is changing, expanding to that of strategist, venture capi-

talist, and chief communicator. Bean counters need not apply. Today businesses need someone to fill a

much broader role than just supervising transactions and keeping tabs on employee expense reports. He or

she needs to be a strategist, communicator, dealmaker, and financier as well as an expert in information

technology and risk management. CFOs increasingly step outside the accounting role and focus on bigger

issues, and they are gaining more power and respect.

At many firms, the CFO is helping build new businesses from within, by acting as the company

venture capitalist. Increasingly, CFOs head up incubators and venture capital arms within their own com-

panies. Dell Computer’s former CFO Thomas Meredith recently became the managing director of Dell

Ventures, which has invested around $700 million in almost 90 companies.

Now that the Internet is reshaping how companies create value, investors are demanding more

and better information. As financial markets become more global, this skill becomes more important.

Today you can get a computer program to do a lot of the more mundane accounting tasks. That

frees up the CFO to become more involved in strategic planning and information. Enterprise Software

Products already has programs that allow many accounting and financial-modeling tasks to be performed

in a fraction of the time it took just a few years ago. The sophistication of these programs will only in-

crease. One expert calls the new technology “CFO–in-a-box.”

At Oracle Corporation, a leading innovator in enterprise software itself, expense reports are filed

on the company’s intranet, eliminating paperwork and labor costs. It allows reimbursements to be paid

directly into bank accounts a week faster than was possible back when it used old–fashioned forms.

Another traditional CFO task that is being revolutionized is the reporting of a company’s finan-

cials and periodic closing of the books. Ultimately, financial information will be available in real-time

fashion, making it possible to close the books almost instantaneously. Cisco Systems CFO Larry Carter

and CEO John T. Chambers are credited with developing the “virtual close.” Cisco is the first company to

generate hourly updates on revenues, product margins, discounts, and bookings. It takes Cisco just one

day to close its books, while it takes most companies five days and some companies as many as fourteen.

lecture enhancer 18-3

IVY LEAGUE ENDOWMENT DIFFICULTIES

From countless investment magazines to television personalities like Mad Money’s Jim Cramer,

Americans have plenty of places to turn for financial advice. But just because financial “experts” are re-

spected enough to be given a voice in journals or on television shows, they aren’t infallible. The business

world is a volatile and ever-changing entity that defies the expectations of even the industry’s brightest

minds. So when it comes to investing, seeking expert advice is a must, but potential investors also have to

be careful not to follow their financial advisors blindly.

For instance, from the mid-1980s up until the eve of the financial crisis, Yale’s endowment man-

ager David Swensen was the Ivy League’s investment guru. Over the course of more than two decades,

Swensen poured billions into real estate, private equity, hedge funds, and other nontraditional assets.

Swensen’s clever investing yielded substantial returns, expanding Yale’s endowment at an average annual

rate of 16.3% in the decade preceding the credit crunch. Dozens of other wealthy universities copied

Swensen’s investment strategy, especially Ivy rival Harvard, which boasted a $36.6 billion endowment at

the end of fiscal 2008.

Chapter 18 – Financial Management

18-69

But the other shoe dropped with a resounding thud in October 2008. The stock market meltdown

left investment-centric colleges with billions tied up in various failing ventures but with little cash on

hand to actually run their schools. As a result, 15 wealthy colleges, Harvard and Yale among them, bor-

rowed $7.2 billion between 2008 and 2009. Harvard now spends $87.5 million a year on interest pay-

ments to debtors alone. As a result of Harvard’s 27.3% endowment nosedive, university officials cut costs

at the student level. School administrators nixed hot breakfasts from student dining halls, reduced shuttle

bus service, and offered buyouts to professors in an effort to close budget gaps.ii

lecture enhancer 18-4

CROWDFUNDING BEYOND KICKSTARTER

Crowdfunding websites like Kickstarter and Indiegogo have raised hundreds of millions of dollars for

businesspeople and artists looking for quick injections of cash. But what has it done for the people who actual-

ly contributed to these campaigns? While many crowdfunding drives offer prizes and gifts to their donors, they

don’t provide participants with ownership stakes like other methods of investment. That’s why a new wave of

crowdfunding platforms are coming on the scene to make this burgeoning financing strategy more like tradi-

tional equity purchases.

Microventures, for instance, serves as a kind of online marketplace for startups to hook up with

wealthy investors. Entrepreneurs create profiles and plead their cases on the social network just like they

would on Kickstarter. Unlike that site, however, backers receive an equity stake in the venture commensurate

with their investment. Although this is no different than the way startups already seek out seed cash, the digital

platform allows entrepreneurs to meet interested parties online without hopping from meeting to meeting. So

far the company has handled more than $8 million in investments through 25 different campaigns with six

more currently in development.

While Microventures is useful for established entrepreneurs, it fails to serve the up-and-coming indi-

viduals who normally utilize crowdfunding sites. Fortunately, that’s where Upstart comes in. This new crowd-

funding venture provides young entrepreneurs with sizable investments from reputable sources in exchange for

stakes in future profits. Unlike Kickstarter, which acts as a funding platform for ideas, Upstart is focused on

people. For example, Omri Mor graduated from the University of Wisconsin with just $182 in his bank ac-

count and an idea for an independent music marketplace in his mind. Through Upstart he received $50,000 to

spend on whatever he wanted. In return he would pay his backers a percentage of his future income over the

course of a decade. This method grants entrepreneurs the freedom to pursue their goals at their own pace with-

out fretting about that first failure. Investors, on the other hand, can receive a windfall if their wards manage

to hit it big.iii

lecture enhancer 18-4

THE NUMBERS SPEAK WHEN DEALING WITH YOUR BANKER

With a few quick calculations, a banker can tell a lot about your company’s financial health. If

you’re in the market for a bank loan, you’d better pay close attention to what your financial statements are

telling prospective lenders. Do you have enough cash to repay the loan if sales start to drop? Are you

overleveraged? The answers are all there in black and red. By evaluating some key financial ratios from

your balance sheet and income statement, a banker can take your company’s financial pulse and deter-

mine whether it qualifies for the loan request.

Chapter 18 – Financial Management

18-70

Financial ratios, which we studied in Chapter 17, allow bankers to weigh one part of your compa-

ny’s balance sheet against another, such as debt against equity or assets against liabilities. The resulting

figures might show that you’re carrying too much debt to take on another loan or that your cash flow isn’t

sufficient to meet the payment terms. The ratios also allow bankers to compare your company’s financial

status with that of others in your industry.

Of course, plain numbers never tell the whole story. As much as the loan review process seems

like an exact science to nonbankers, it isn’t. So even if your numbers aren’t perfect, other factors will play

a role in the overall decision to grant credit. In bank terms, loan requests are measured by the three Cs of

credit: namely, the character of the borrower, the collateral the company brings to the table, and its ca-

pacity to repay the loan.

Every banker uses both objective criteria and subjective judgment to evaluate these factors. At the

beginning of the loan review process, he or she is likely to ask these seven questions:

1. Does the loan meet the bank’s market focus and lending policies?

2. What size loan and repayment term are being requested?

3. What is the proposed use of the funds?

4. What is the company’s capacity to repay the funds?

5. What is the default risk of this loan?

6. How can the risks be controlled?

7. What loan terms, if any, should we offer?

With those questions in mind, a banker will turn to the numbers on your financial statements,

which can sometimes reveal as much about a company’s past and future as can its CEO. Here are some of

the financial ratios your banker may evaluate:

Leverage Ratio

This ratio tells bankers how much debt your company is carrying in relation to its capital.

In other words, the ratio measures how many dollars you have in the company versus how many

your creditors have. Assets, liabilities, and owners’ equity all are evaluated to determine whether

your company can survive bumps in the road and still repay the loan.

Obviously, if your company has more debt than its capital can meet—for example, a debt-

to-equity ratio of more than 2:1—your chances of receiving a loan may decrease greatly. Or, at

the very least, the bank may try to minimize the risk of making such a loan by asking for other

guarantors or requiring the participation of a third party, such as a municipal or state government

agency.

Current Ratio

This figure tells bankers whether your company has enough liquid assets to repay a short-

term loan, which generally must be repaid in one year. The ratio is calculated by dividing current

assets (cash, accounts receivable, and inventory) by current liabilities (debts and obligations due

within one year). The standard for the current ratio often is set at 2:1. The higher your ratio, the

greater your chances of receiving a short-term loan.

Quick Ratio

Like the current ratio, a quick ratio gives bankers a look at your company’s ability to pay

short-term debt. The difference is that the quick ratio doesn’t include inventory in its tally of

current assets. This helps bankers determine how much of the company could be converted into

cash immediately. The quick ratio is especially relevant for service companies, such as law firms

and personnel agencies, which don’t carry tangible inventory such as raw materials, lumber, or

sheet metal.

Chapter 18 – Financial Management

18-71

Again, a quick ratio of more than 1:1 boosts your chances of getting a loan. But remember,

other factors may come into play as well. Consider the Smith Jones Law Firm, which recently re-

quested a loan to upgrade its computer equipment and thereby increase efficiency. The law firm’s

quick ratio is a positive 1:5. Yet, when the banker looks at its assets more closely, he finds that

the firm has only two major clients.

This issue, called “business concentration,” frequently arises with start-ups and other rela-

tively young companies. It can present a great risk for the bank, even if a company’s financial ra-

tios are favorable. Could the law firm, for example, repay the loan if one of its clients sought le-

gal counsel elsewhere or started dragging out its payments? Quite possibly, the firm may be able

to overcome this obstacle by providing evidence that its business is growing, perhaps in the form

of new contracts.

Cash Flow Analysis

By analyzing your company’s cash flow, a banker can see how it uses money and how

much, if any, it needs to borrow. The cash flow analysis includes a number of pieces, each of

which helps paint an overall picture of your ability to service new debt. Some of the key factors

reviewed:

• Funds from operations. This includes your company’s net income and noncash charges,

such as depreciation and amortization.

• Net operating capital. This is the amount your company spends or takes in to operate the

business during a given period. It can include increases—or decreases—in receivables, in-

ventories, accounts payable, accrued expenses, and the like.

• Net cash throw-off. This is the combined sum of your funds from operations and net op-

erating capital. The surplus or deficit shows how much cash the company has available for

its current needs.

• Other financing required. If your company’s net cash throw-off shows a deficit, you

may need other financing such as a short- or long-term loan or an equity investment. This

factor helps determine how much—and what type—of capital is needed.

Most important, the cash flow analysis shows bankers whether you have enough funds to

support a loan. Suppose, for example, that ABC Clothing Store requests a $100,000 loan to fi-

nance new clothing display equipment. The banker walks through the numbers and sees that ABC

has a surplus net cash throw-off. The problem: After accounting for financing from other lenders

and investors, ABC shows a net cash change, or remaining cash, of only $38,000.

Though ABC’s initial cash flow ratios look promising, its current debt demands could af-

fect its ability to repay a loan and still have sufficient cash for operations. Although the banker

could try to make the loan work by changing the amount or the terms, the truth is that it may not

be in ABC’s best interest to take on the debt. Too much debt can limit a company’s future busi-

ness options and hamper its ability to develop the type of positive financial history that banks

look for.

Sensitivity Ratio

This is not a formal financial ratio, but rather the banker’s subjective, gut-level judgment of

whether a loan should be made. But don’t take it lightly: In some cases, it’s the most important

factor at play because it encompasses a variety of vital issues, including the credibility of the

management team, the business’s ability to generate accurate numbers, and the risks inherent to

the industry.

Chapter 18 – Financial Management

18-72

The sensitivity ratio becomes especially important when a banker is on the fence about

your loan. In the end, he or she wants to see more than ratios and financial statements; the banker

also wants to know that you understand how your business makes money, how it will grow, and

how you’ll manage future hurdles. With the sensitivity analysis, a banker might decide to control

its risk by securing the loan with collateral, asking for guarantors, or seeking the participation of a

third party such as the SBA.

In some cases, of course, there may not be an immediate solution. But if you’re turned down for a

loan, don’t give up. Good bankers want to develop long-term relationships, and they may be able to help

you pursue other financing solutions, such as nonbank lenders or equity investors. Or, the banker may

direct you to an accountant or business consultant who can help you focus the business and package a

loan request that will be more successful.

Finally, as tedious as it may be, the loan review process itself can help prepare a company for

some ups and downs by forcing it to look more closely at its strategies and better plan for the future. As a

result, your company may take its first steps toward financial health and open the doors to loans down the

road.

lecture enhancer 18-6

AMERICA’S DANGEROUS LACK OF FINANCIAL FACTS

When the credit crunch came to a head in 2008, not even the financial world’s leading experts

could make sense out of all the confusion. A jumble of credit default swaps (CDSs), derivatives, and

faulty mortgages cluttered the marketplace in multitrillion-dollar heaps. Banks didn’t know what they

owned, who owed them money, or how much they had lost.

According to the renowned economist Hernando de Soto, all this chaos could possibly have been

avoided if investors and regulators had access to genuine financial facts. For almost a century businesses

were required to keep all titles, balance sheets, and statements of accounts in a publically accessible

“memory system.” This way people knew exactly what assets a company held and just how well they

were performing. However, over the last two decades deregulation eroded many of these outlets for fi-

nancial facts, relying almost exclusively on the companies themselves to release the relevant data.

This unaccountability led to a series of massive miscommunications during the 2008 crash. For

instance, a number of banks have not been able to foreclose on some defaulted mortgages because they do

not possess the proof of ownership. Before the real estate bubble popped banks failed to record the names

of the mortgage owners, favoring instead to pool a bunch of mortgages together and trade them as securi-

ties. About 60% of the country’s residential mortgages are listed as owned by a company called MERS, a

shell company used to streamline trading of the mortgages. Now banks that have collected billions in tax-

payer money to recover their assets aren’t even sure of which assets they actually own.

The economy also suffered thanks to a practice called off–balance-sheet accounting. In the 1990s

governments around the world allowed ailing companies to recorded their debts off public balance sheets

and on to less accessible ones called special purpose entities. These SPEs allowed companies to game the

system by keeping their losses off the public record, thus making them seem healthier to investors. The

Dodd-Frank financial reform bill does not address unaccountable mortgage holdings, SPEs, or a number

of other maladies limiting our knowledge of the economic system. According to de Soto, without all the

necessary facts the world is poised for another wide-scale financial failure.iv

Chapter 18 – Financial Management

18-73

lecture enhancer 18-7

REAL ESTATE WOES FOR REGIONAL BANKS

Some of the nation’s largest banks have begun to pay back their federal bailout money, leading

some to believe that the financial world has already experienced the worst of the recession. While this

may be true for the big banks on Wall Street, it’s a different story for small regional banks across the na-

tion. Before the recession, regional banks lacked the clout or capital to diversify into stocks and bonds

like their multinational colleagues. As a result, regional banks turned to local commercial real estate to

expand their portfolios. But as commercial properties across the country continue to fall victim to de-

faults, regional banks have found themselves mired in a fiscal pickle that could keep them on government

support for a while.

In a study of the nation’s 35 largest regional banking institutions, lending for commercial proper-

ty like office parks and shopping malls made up for more than a third of all loans issued. Vacancies and

falling real estate prices have ravaged the values of these properties, ensuring that many banks will stay in

the red indefinitely. For example, Synovus, a Georgia-based financial services firm, has two-thirds of its

loans in commercial property and construction. The company has reported five consecutive quarterly

losses. Along with Synovus, eight other banks with more than a third of their holdings in commercial real

estate are projected to post steady losses.

Regional banks will also have a tougher time shedding the yoke of governmental control than

their Wall Street brethren. Since the big banks have far larger revenue streams and can amass capital

quicker, they’ve had an easier time obtaining federal permission to repay bailout funds. With cash flow

stagnant and losses piling up, most regional banks will retain a government presence for years to come.

That being the case, regional banks will not be able to declare dividends or make stock repurchases with-

out government approval. These limitations could make regional banks seem less attractive to consumer

borrowers than national banks, effectively hamstringing their chances for regrowth. Meanwhile, commer-

cial real estate will keep getting more toxic.v

Chapter 18 – Financial Management

18-74

critical

thinking exercises

Name: ___________________________

Date: ___________________________

critical thinking exercise 18-1

BUDGETARY CONTROL

The Weinstein Manufacturing Company prepared a budget for its production department as fol-

lows. At the end of the first month, the production manager compared actual results with budgeted

amounts and found that some were over and some were under. An expenditure is considered exceptional

if it varies by more than 10% from the budgeted amount.

Weinsten Manufacturing Company

Monthly Budgetary Control Worksheet

____________________________________________________________________________

Expense Budgeted Actual Difference

Category Amount Expenditure from Budget

____________________________________________________________________________

Labor $162,500 $195,000 _______________

Raw materials 172,500 151,500 _______________

Utilities 6,500 6,300 _______________

Maintenance 9,750 8,950 _______________

Other variable expenses 16,750 18,000 _______________

Fixed overhead expenses 25,000 25,000 _______________

Total Expenses $393,000 $404,750 _______________

___________________________________________________________________________________