Chapter 17 – Understanding Accounting and Financial Information

17-91

Wheatley International

Balance Sheet

December 31, 201X

ASSETS

Current Assets

Cash $ 72,000

Accounts Receivable 120,600

Notes Receivable 61,200

Inventory 126,600

Total Current Assets $380,400

Fixed Assets

Land $1,500,000

Buildings 1,050,000

Equipment & Vehicles 1,066,000

Depreciation − 400,000

Total Fixed Assets $3,216,000

Other Assets

Goodwill $90,000

Total Other Assets $90,000

TOTAL ASSETS $3,686,400

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current Liabilities

Accounts Payable $45,000

Short-Term Notes Payable 15,600

Total Current Liabilities $60,600

Long-Term Liabilities

Notes Payable (Long-Term) $210,000

Bonds 60,000

Total Long-Term Liabilities $270,000

Total Liabilities $330,600

Owner’s Equity

Common Stock $1,896,000

Retained Earnings 1,459,800

Total Owners’ Equity $3,355,800

TOTAL LIABILITIES AND

STOCKHOLDERS’ EQUITY $3,686,400

Chapter 17 – Understanding Accounting and Financial Information

17-92

Name: ___________________________

Date: ___________________________

critical thinking exercise 17-4

CALCULATING FINANCIAL RATIOS (ADVANCED)

You are considering investing in Acme Incorporated. The company has provided you with the

balance sheet and income statement for the previous year. The current price of one share of stock is

$46.25. Earning per share last year was $1.86.

1. Calculate the requested financial ratios:

a. Current ratio

b. Debt-to-equity ratio

c. Return on sales (use net income AFTER taxes)

d. Return on equity (use net income AFTER taxes)

e. Earnings per share (use net income AFTER taxes)

2. Would you invest in Acme Incorporated? Why or why not?

Chapter 17 – Understanding Accounting and Financial Information

17-93

Acme Incorporated

Statement of Income

FY 201X

REVENUES

Net Sales $4,090,970

Other Income +104,227

Total Revenue $4,195,197

COST OF GOODS SOLD $2,673,129

GROSS PROFIT (GROSS MARGIN) $1,522,068

OPERATING EXPENSES

Total Selling Expenses $333,300

Total General Expenses + 306,036

Total Operating Expenses $639,336

NET INCOME BEFORE TAXES $882,732

Income Tax Paid (25%) $220,683

NET INCOME AFTER TAXES $662,049

Chapter 17 – Understanding Accounting and Financial Information

17-94

Acme Incorporated

Balance Sheet

December 31, 201X

ASSETS

Current Assets

Cash $280,928

Marketable Securities 514,800

Accounts Receivable 108,694

Notes Receivable 855,771

Inventories 218,156

Prepaid Expenses and Other 88,237

Current Assets

Total Current Assets $2,066,586

Fixed Assets

Land $510,000

Plant and Buildings 304,096

Equipment 218,500

Total Fixed Assets $1,744,701

Other Assets

Goodwill, Net $ 49,930

Total Other Assets $ 49,930

TOTAL ASSETS $3,861,217

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current Liabilities

Accounts Payable $226,977

Accrued Expenses and Other 380,496

Current Liabilities

Current Portion of Finance Debt 382,579

Total Current Liabilities $990,052

Long-Term Liabilities

Notes Payable $228,772

Bonds 380,000

Other Long-Term Liabilities 29,478

Total Long-Term Liabilities $ 638,250

Total Liabilities $1,628,303

Owner’s Equity

Common Stock $ 389,538

(342,196 Shares Outstanding)

Retained Earnings 1,843,377

Total Owners’ Equity $2,232,915

TOTAL LIABILITIES AND

STOCKHOLDERS’ EQUITY $3,861,217

Chapter 17 – Understanding Accounting and Financial Information

17-95

notes on critical thinking exercise 17-4

1. Calculate the requested financial ratios.

a. Current ratio. The current ratio is the ratio of the firm’s current assets to its current liabil-

ities, calculated as follows:

Current ratio =

Current assets s or $2,066,586

Current liabilities $ 990,520

2.086:1

b. Debt-to–equity ratio. The debt-to–equity ratio measures the degree to which the company

is financed by borrowed funds that must be repaid. It is calculated as follows:

Debt-to-equity ratio =

e. Earnings per share. Earnings per share measures the amount of profit earned by a com-

pany for each share of common stock it has outstanding:

Earnings per share =

Net income or $662,049

Number of shares outstanding 342,196

$1.935 per share

Chapter 17 – Understanding Accounting and Financial Information

17-96

2. Would you invest in Acme Incorporated? Why or why not?

The current ratio of 2.086 means that $2.086 in current assets is available for every $1.00 of cur-

rent liabilities. The firms should be able to meet short-term debt payments easily.

from $1.86 to $1.935.

Overall, the company seems to be profitable, with a healthy debt–to-equity ratio.

Chapter 17 – Understanding Accounting and Financial Information

17-97

Name: ___________________________

Date: ___________________________

critical thinking exercise 17-5

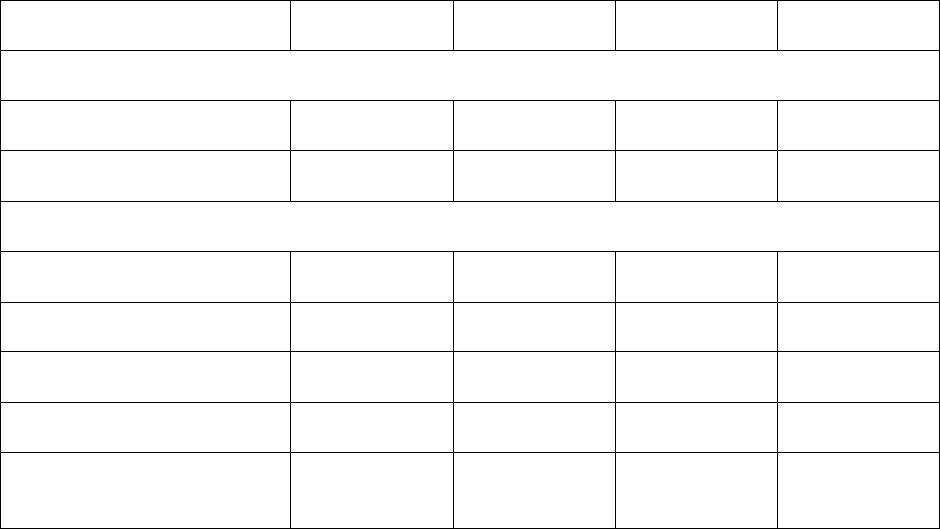

COMPARING INDUSTRY RATIOS (BASIC)

You are interested in investing in a regional hotel company and have investigated the fi-

nancial statements of four potential investments. Use the information in the table below to answer the

questions at the bottom of the page.

Hotel N

Hotel J

Hotel C

Hotel W

Information from the income statement

Total revenue

$10,099,000

$3,816,000

$428,806

$1,277,550

Total expenses

9,503,000

3,618,000

354,461

1,822,748

Information from the balance sheet

Current assets

1,946,000

1,020,000

68,629

526,549

Total assets

8,668,000

8,183,000

262,388

3,783,127

Current liabilities

2,356,000

895,000

101,091

693,809

Total liabilities

4,587,000

5,944,000

456,441

3,089,318

Total number of common

stock outstanding

225,800

389,000

32,312

168,238

(Use the table on the following page for your answers.)

1. What is the net profit (or net loss) for each company?

2. Calculate the return on sales for each company.

3. Calculate the total stockholders’ equity for each company.

Chapter 17 – Understanding Accounting and Financial Information

17-98

4. What is the current ratio for each company?

5. Calculate the return on equity ratio for each company.

6. What is the debt-to-equity ratio for each company?

7. Calculate the basic earnings per share for each company.

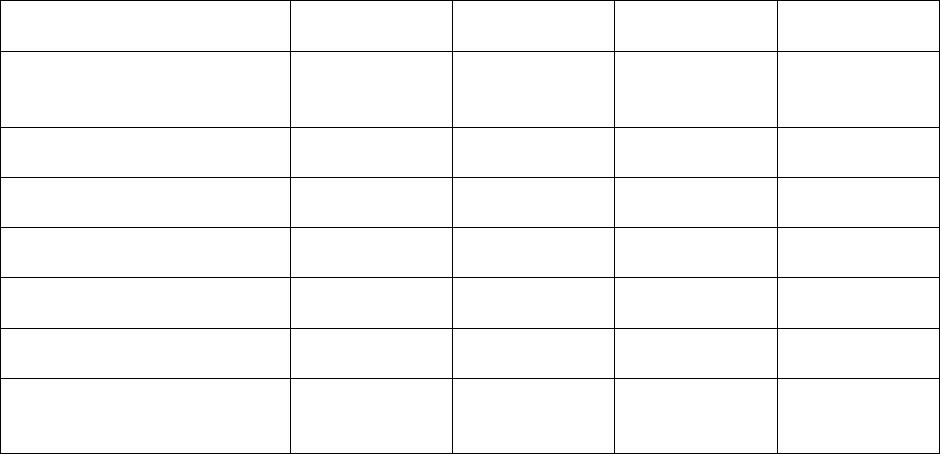

Hotel N

Hotel J

Hotel C

Hotel W

1. Net income (net profit or

net loss)

2. Return on sales

3. Current ratio

4. Stockholders’ equity

5. Return on equity

6. Debt-to-equity ratio

7. Earnings per share

(basic)

8. Which company would you rather invest in? Why?

Chapter 17 – Understanding Accounting and Financial Information

17-99

notes on critical thinking exercise 17-5

The requested financial information and ratios are given below.

Hotel N

Hotel J

Hotel C

Hotel W

1. Net income (net profit or

net loss)

$ 596,000

$ 198,000

$ 74,345

($545,198)

2. Return on sales

5.9%

5.2%

17.3%

(42.7%)

3. Current ratio

0.83

1.13

0.68

0.76

4. Stockholders’ equity

4,081,000

2,239,000

(194,053)

693,809

5. Return on equity

14.6%

8.8%

Not meaningful

(78.5%)

6. Debt-to-equity ratio

112%

265%

Not meaningful

445%

7. Earnings per share

(basic)

$2.64

$0.51

$2.30

($3.24)

Hotel N. Return on sales is in the midrange for the industry. The current ratio, while less than the ideal

2.0, is in line with two of the other three companies. Return on equity is healthy and at the top of

the industry, showing that the company has made good use of the funds invested by the investors.

The debt-to-equity is much higher than the ideal ratio of 100%. However, when compared to the

other companies in the industry, a 112% debt-to-equity ratio looks good. Earnings per share are

also at the top range in the industry.

Hotel J. Return on sales is in the midrange. Current ratio is at the top of the industry, showing a better

than average liquidity. Return on equity is not exceptional, but in the midrange for the industry.

Hotels C and W are horrible investment candidates. That leaves Hotels N and J. Hotel J is heavily

leveraged and would be more risky. Hotel N is a steady, safe performer. Knowing that there is a direct

relationship between risk and return, the investment decision would depend on the investors’ tolerance for

risk.

Chapter 17 – Understanding Accounting and Financial Information

17-100

bonus

cases

bonus case 17–1

THE BEST-LAID PLANS OFTEN GO AWRY

How you report revenues on the income statement makes a big difference in how profitable a

company looks. The problem is that stockholders are often fooled into investing in a firm that is not near-

ly as profitable as they think. A good example is that of Thousand Trails of Seattle. It sold campground

memberships for owners of recreation vehicles. It used the usual expensive promotions to get potential

buyers to come to the campgrounds. Once a potential customer was at the site, there was much pressure to

buy now, and the campgrounds were quite attractive. Once a customer got home and reconsidered the

investment, though, some backed out of the commitment, and that is where Thousand Trails got into dif-

ficulty.

The company recorded the full price of a membership (about $7,500) as revenue, even though

members paid only 40% down on average. Marketing expenses were running higher than payments, so

more cash flowed out than flowed in. To get cash, Thousand Trails sold its receivables.

In one year, Thousand Trails used $52 million more cash than it produced, a definite cash flow

problem. Nevertheless, it reported record earnings of $19.1 million, and the stock price went up to over

$29.

Two years later, the stock had fallen to less than $5, reflecting a 90% drop in earnings reported

(from $19 million to less than $2 million). What happened was that a lot of campground members

dropped out before paying in full. So Thousand Trails had to write off $11 million in paper revenues.

Marketing expenses were two times greater than down payments. Debt reached a horrendous 244% of

stockholders’ equity.

Meanwhile, stockholders were left wondering what happened to the company that was growing

so fast and making such good profits (at least on the income statement).

discussion questions for bonus case 17-1

1. Thousand Trails did nothing illegal in its reporting of revenues and profits. What does that tell

you about the need to carefully read and analyze income statements before you invest?

2. Can you see how cash flow problems can grow to unbelievable proportions in just a short time,

even when profits look good?

Chapter 17 – Understanding Accounting and Financial Information

17-101

notes on discussion questions for bonus case 17-1

1. Thousand Trails did nothing illegal in its reporting of revenues and profits. What does that tell

you about the need to carefully read and analyze income statements before you invest?

The fact is that income statements and balance sheets are very hard to analyze. Auditors go over

2. Can you see how cash flow problems can grow to unbelievable proportions in just a short time,

even when profits look good?

Yes, cash flow problems plague businesses, especially the ones that grow rapidly. The problem is

Chapter 17 – Understanding Accounting and Financial Information

17-102

bonus case 17–2

MANAGING BY THE NUMBERS

Katherine Potter knew a good thing when she saw it. At least, it seemed so at first. She was trav-

eling in Italy when she spotted pottery shops that made beautiful products ranging from ashtrays to lamps.

Some of the pottery was stunning in design.

Katherine began importing the products to the United States, and sales took off. Customers im-

mediately realized the quality of the items and were willing to pay top price. Katherine decided to keep

prices moderate to expand rapidly, and she did. Sales in the second three months were double those of the

first few months. Sales in the second year were double those of the first year.

Every few months, Katherine had to run to the bank to borrow more money. She didn’t really dis-

cuss her financial situation with her banker because she had no problems getting larger loans. You see,

she always paid promptly. To save on the cost of buying goods, Katherine always took trade discounts.

That is, she paid all bills within 10 days to save the 2% offered by her suppliers for paying so quickly.

Most customers bought Katherine’s products on credit. They would buy a couple of lamps and a

pot, and Katherine would allow them to pay over time. Some were very slow in paying her, taking six

months or more.

After three years, Katherine noticed a small drop in her business. The local economy was not do-

ing well, and many people were being laid off from their jobs. Nonetheless, Katherine’s business stayed

level. One day, the bank called Katherine and told her she was late in her payments. She told them she

had been so busy that she didn’t notice the bills. The problem was that Katherine had no cash available to

pay the bank. She frantically called several customers for payment, but they were not able to pay her, ei-

ther. Katherine was in a classic cash flow bind.

Katherine immediately raised her prices and refused to make sales on credit. She started delaying

payment on her bills and paid the extra costs. Then she went to the bank and went over her financial con-

dition with the banker. The banker noted her accounts receivable and assets. He then prepared a cash

budget and loaned Katherine more money. Her import business grew much more slowly thereafter, but

her financial condition improved greatly. Katherine had nearly gone bankrupt, but she recovered at the

last minute.

discussion questions for bonus case 17-2

1. How is it possible to have high sales and high profits and run out of cash?

2. Why did Katherine do better when she raised her prices and refused to sell on credit?

3. What was the nature of Katherine’s problem? Was she correct to go to the banker for help, even

though she owed the bank money? How could she have prevented some of the problems she

eventually found herself faced with?

Chapter 17 – Understanding Accounting and Financial Information

17-103

notes on discussion questions for bonus case 17-2

1. How is it possible to have high sales and high profits and run out of cash?

That is the classic description of a poor cash flow. A firm sells lots of merchandise on credit and

buys more, paying promptly. Credit sales are great, and the firm buys more merchandise on credit. One

2. Why did Katherine do better when she raised her prices and refused to sell on credit?

3. What was the nature of Katherine’s problem? Was she correct to go to the banker for help, even

though she owed the bank money? How could she have prevented some of the problems she even-

tually found herself faced with?

Katherine had a classic cash flow problem, and, yes, a bank is an excellent place to turn for help.

The bank can provide funds, help in designing a cash budget, and provide further guidance to avoid cash

Chapter 17 – Understanding Accounting and Financial Information

17-104

endnotes

i Source: Jody Heymann, “Bootstrapping Profits by Opening the Books,” Bloomberg Businessweek, September 23,

2010.

ii Source: Karthik Ramanna, “Why Fair Value Is the Rule,” Harvard Business Review, March 2013.

iii Lecture enhancer created by Michael McHugh.

iv Sources: Brady Dennis, “Congress Passes Financial Reform Bill,” The Washington Post, July 16, 2010; Paul Da-

vidson, Paul Wiseman, and John Waggoner, “Will New Financial Regulations Prevent Future Meltdowns?” USA

Today, June 25, 2010.

v Source: Scott Waller, “Whistleblower Tells Her Story,” The Clarion-Ledger, April 29, 2006.

vi The Internet is a dynamic, changing information source. Web links noted of this manual were checked at the time

of publication, but content may change over time. Please review the website before recommending it to your stu-

dents.