Chapter 17 – Understanding Accounting and Financial Information

17-61

PPT 17-13

Public versus Private Accountants

PUBLIC vs. PRIVATE

ACCOUNTANTS

17-13

LO 17-2

• Private Accountants — Work in a single firm,

government agency, or nonprofit organization.

• Public Accountants — Provide accounting services

to individuals or businesses.

• Certified Public Accountants (CPAs) —

Accountants who have passed a series of

examinations established by the

American Institute of Certified Public Accountants

(AICPA) and met a states requirements for education

and experience.

This slide helps highlight the difference in public and pri-

vate accounting. This may be a good time to discuss what

accounting or finance careers will do for students:

• Develop them into a well-rounded business exec-

utives.

• Help them learn how to analyze and forecast fi-

nancial goals through utilization of historical da-

ta, competitor information and financial da-

ta/information.

• Make an impression at a multibillion-dollar cor-

poration.

• See the company increase its financial vitality by

being a part of the financial planning and report-

ing process.

(Source: Retailology.com.)

Chapter 17 – Understanding Accounting and Financial Information

17-62

PPT 17-14

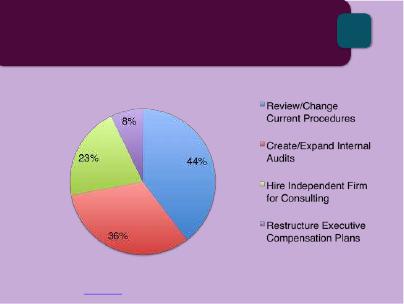

Ways to Improve Accounting Practices

WAYS to IMPROVE

ACCOUNTING PRACTICES

17-14

Source: www.soxlaw.com, accessed November 2014.

LO 17-2

1. This slide charts how to improve accounting practices.

2. If the events of the last 10 years have taught us any-

thing, it is that accurate financial data is critical for

creditors, investors, and managers to make informed

decisions.

3. The federal government has reacted with the passage

of Sarbanes-Oxley. This law, which went into effect in

2002, has five major components:

• Section 302: Periodic statutory financial re-

ports are to include certifications that the sign-

ing officers have reviewed the report; the re-

port does not contain any material untrue

statements or material omission or be consid-

ered misleading; the financial statements and

related information fairly present the financial

condition and the results in all material re-

spects; the signing officers are responsible for

internal controls and have evaluated these in-

ternal controls within the previous 90 days and

have reported on their findings; a list is pro-

vided of all deficiencies in the internal controls

and information on any fraud that involves

employees who are involved with internal ac-

tivities; and any significant changes in internal

controls or related factors that could have a

negative impact on the internal controls are re-

ported.

• Section 401: Financial statements published by

issuers are required to be accurate and present-

ed in a manner that does not contain incorrect

statements.

• Section 404: Issuers are required to publish in-

formation in their annual reports concerning

the scope and adequacy of the internal control

structure and procedures for financial report-

ing.

• Section 409: Issuers are required to disclose to

the public, on an urgent basis, information on

material changes in their financial condition or

operations.

• Section 802: Imposes penalties or fines and/or

up to 20 years’ imprisonment for altering, de-

stroying, mutilating, concealing, or falsifying

records, documents, or tangible objects with

the intent to obstruct, impede, or influence a

legal investigation.

(Source: www.soxlaw.com.)

Chapter 17 – Understanding Accounting and Financial Information

17-63

PPT 17-15

Dodd-Frank Act

DODD-FRANK ACT

17-15

PhotoCredit:NancyPelosi

LO 17-2

• Dodd-Frank Wall Street Reform and Consumer

Protection Act increased financial regulation by

increasing the power of the Public Company

Accounting Oversight Board.

• Act was brought on by the recent financial crisis.

PPT 17-16

Auditing Checks Accuracy

AUDITING CHECKS ACCURACY

17-16

LO 17-2

• Auditing — Reviewing and evaluating the information

used to prepare a company

’

s financial statements.

• Independent Audit — An evaluation and unbiased

opinion about the accuracy of a company

’

s financial

statements.

• Certified Internal Auditors (CIAs) — Accountants

who have a bachelor

’

s degree and two years of

experience in internal auditing and pass an exam

administered by the Institute of Internal Auditors.

PPT 17-17

Elementary, Mr. Auditor, Elementary

ELEMENTARY,

MR. AUDITOR, ELEMENTARY

17-17

• Fraud damages businesses, no matter the size.

• The SEC has committed itself to fighting fraud but not

all auditors and CPAs are trained in finding fraud.

• Colleges are offering advanced degrees in forensic

accounting to meet the upcoming demand for these

accountants.

Chapter 17 – Understanding Accounting and Financial Information

17-64

PPT 17-18

Specialized Accountants

• Tax Accountants — Accountants trained in tax law

and are responsible for preparing tax returns or

developing tax strategies.

SPECIALIZED ACCOUNTANTS

17-18

LO 17-2

• Government and Not-for-

Profit Accounting —

Support for organizations

whose purpose is not

generating a profit, but

serving others according to a

duly approved budget.

PPT 17-19

Test Prep

TEST PREP

17-19

• What’s the key difference between managerial

and financial accounting?

• How’s the job of a private accountant different

from that of a public accountant?

• What’s the job of an auditor? What’s an

independent audit?

1. Managerial accounting provides information and

analysis to the managers inside the organization

and helps them make better informed decisions.

Managerial accounting is concerned with

measuring and reporting cost of production,

marketing, and other functions such as preparing

budgets; making sure business units stay within

their budgets and designing strategies to minimize

taxes. Financial accounting differs from

managerial accounting in that financial accounting

generates information for people primarily outside

the organization.

2. The private accountant works for a single firm,

government agency, or nonprofit organization.

While public accountants work for accounting

firms that provide accounting services for a fee.

Public accountants provide services to individuals

or businesses that include designing an accounting

system, selection of software to run the accounting

system. and analyzing an organization’s financial

performance.

3. Auditors are responsible for examining the finan-

cial health of the organization as well as looking

into the operational effectiveness and efficiencies

of the organization. An independent audit is an au-

dit conducted by public accounts who provide an

evaluation and unbiased opinion about the accuracy

of a company’s financial statements.

Chapter 17 – Understanding Accounting and Financial Information

17-65

PPT 17-20

The Accounting Cycle

The ACCOUNTING CYCLE

17-20

LO 17-3

• Accounting Cycle –– A six-step procedure that

results in the preparation and analysis of the major

financial statements.

With this slide, students are provided with the step-by-step

progression of the accounting cycle. Place particular em-

phasis on the accounting cycle to give the student an over-

view of reporting requirements. To start a discussion with

students ask the following questions before showing the

next few slides:

• Can you explain the differences between account-

ing and bookkeeping?

• What’s the difference between an accounting jour-

nal and a ledger?

• Why does a bookkeeper prepare a trial balance?

PPT 17-21

Bookkeeper’s Role

BOOKKEEPER’S ROLE

17-21

LO 17-3

• Bookkeeping — The recording of business

transactions. Bookkeepers divide a firm

’

s

transactions into meaningful categories and post

them into a record book or computer program called

a journal.

• Double-Entry Bookkeeping — Bookkeepers

record all transactions in two places so they can

check one list of transactions against the other for

accuracy.

PPT 17-22

Bookkeeper’s Tools

BOOKKEEPER’S TOOLS

17-22

LO 17-3

• Ledger — A specialized

accounting book or

program where all

information is in one place.

• Trial Balance — A

summary of all the

information in the account

ledgers.

Chapter 17 – Understanding Accounting and Financial Information

17-66

PPT 17-23

Technology and Accounting

TECHNOLOGY and ACCOUNTING

17-23

LO 17-3

• Computerized

accounting programs

post information

instantly and from

remote locations.

• Intuit’s QuickBooks

address the specific

needs of small

businesses.

PPT 17-24

Test Prep

TEST PREP

17-24

• How is the job of the bookkeeper different from

an accountant?

• What’s the purpose of accounting journals and a

ledger?

• Why does a bookkeeper prepare a trial balance?

• How has computer software helped businesses in

maintaining and compiling accounting

information?

1. A bookkeeper classifies and summarizes the firm’s

financial data; while accountants interpret the data,

prepare financial statements, and report the

information to management.

2. The purpose of accounting journal is to divide the

firm’s transactions into meaningful categories to

keep information organized and manageable. A

ledger transfers information from an accounting

journal so managers can find information about a

single account in one place.

3. A bookkeeper prepares a trial balance to ensure the

figures in the account ledgers are correct and

balanced.

4. Computer software post information from journals

instantaneously even from remote locations so fi-

nancial information is readily available whenever

the organization needs it.

PPT 17-25

Financial Statements

• Financial Statement — A summary of all the

financial transactions that have occurred over a

particular period.

FINANCIAL STATEMENTS

17-25

LO 17-3

• Key financial statements of

business are:

– Balance sheet

– Income statement

– Statement of cash flows

Students often do not understand that financial statements

are more than a balance sheet but also incorporate the in-

come statement and statement of cash flows.

Chapter 17 – Understanding Accounting and Financial Information

17-67

PPT 17-26

The Fundamental Accounting Equation

The FUNDAMENTAL

ACCOUNTING EQUATION

17-26

LO 17-4

• Fundamental Accounting Equation — The basis

for the balance sheet.

• The equation must always be balanced and

includes the formula:

Ø Assets = Liabilities + Owners Equity

PPT 17-27

The Balance Sheet

The BALANCE SHEET

17-27

LO 17-4

• Balance Sheet —

The financial

statement that

reports a firm

’

s

financial condition

at a specific time.

See Figure 17.5 in the text for a sample balance sheet for

Very Vegetarian.

PPT 17-28

Assets

ASSETS

17-28

LO 17-4

• Assets — Economic resources owned by a firm.

Items can be tangible or intangible.

• Liquidity — Ease with which assets can be

converted into cash.

Chapter 17 – Understanding Accounting and Financial Information

17-68

PPT 17-29

Classifying Assets

CLASSIFYING ASSETS

17-29

LO 17-4

• Current Assets — Items that can or will be

converted to cash within one year.

• Fixed Assets — Long-term assets that are relatively

permanent such as land, buildings, or equipment.

• Intangible Assets — Long-term assets that have no

physical form but do have value such as patents,

trademarks, and goodwill.

Assets are divided into three categories according to how

fast they can be converted into cash.

PPT 17-30

Classifying Liabilities

CLASSIFYING LIABILITIES

17-30

LO 17-4

• Liabilities — What the business owes to others – its

debts.

• Accounts Payable — Current liabilities a firm owes

for merchandise or services purchased on credit.

• Notes Payable — Short or long-term liabilities a

business promises to pay by a certain date.

• Bonds Payable — Long-term liabilities that the firm

must pay back.

PPT 17-31

Owners’ Equity Accounts

OWNERS’ EQUITY ACCOUNTS

17-31

LO 17-4

• Owners’ Equity — The

amount of the business that

belongs to the owners minus

any liabilities of the owners.

• Retained Earnings —

Accumulated earnings from the

firm

’

s profitable operations that

are reinvested in the business.

Chapter 17 – Understanding Accounting and Financial Information

17-69

PPT 17-32

Test Prep

TEST PREP

17-32

• What do we call the formula for the balance

sheet? What three accounts does it include?

• What does it mean to list assets according to

liquidity?

• What is the difference between long-term and

short-term liabilities on the balance sheet?

• What is owners’ equity and how is it determined?

1. The formula for the balance sheet is referred to as

the fundamental accounting equation. This

equation includes the following three accounts:

assets, liabilities and owners equity.

2. Assets on the balance sheet are listed according to

how quickly they can be converted to cash.

Therefore, as you move down the balance sheet it

becomes more difficult to convert the assets into

“liquid” cash.

3. Liabilities are what the business owes to others.

The liability account is divided into current and

long-term liabilities. Common liability accounts

include: accounts payable, notes payable and

bonds payable.

4. Owners’ equity is the amount of the business that

belongs to the owners, minus any liabilities the

business owes. The formula for owners’ equity is

assets minus liabilities.

PPT 17-33

The Income Statement

The INCOME STATEMENT

17-33

LO 17-4

• Income Statement — The

financial statement that

shows a firm

’

s bottom line –

that is, its profit after costs,

expenses, and taxes.

• Net Income/Net Loss —

The revenue left over after

costs and expenses.

PPT 17-34

The Income Statement

The INCOME STATEMENT

17-34

LO 17-4

• The formula for the income statement:

Revenue

– Cost of Goods Sold

= Gross Profit

– Operating Expenses

= Net Income before Taxes

– Taxes

= Net Income or Net Loss

See Figure 17.7 in the text for a sample income statement

for Very Vegetarian.

Chapter 17 – Understanding Accounting and Financial Information

17-70

PPT 17-34

Accounts of the Income Statement

ACCOUNTS of the INCOME

STATEMENT

17-35

LO 17-4

• Revenue is the monetary value a firm received for

goods sold, services rendered or other payments.

• Cost of Goods Sold (or Manufactured) —

Measures the cost of merchandise the firm sells or the

cost of raw materials and supplies it used in producing

items for resale.

• Gross Profit (or Gross Margin) — How much a

firm earned by buying (or making) and selling

merchandise.

PPT 17-35

The In’s and Out’s of Valuing Inventory

THE IN’S and OUTS of

VALUING INVENTORY

17-36

• Generally Accepted Accounting

Principles (GAAP) sometimes

permits accountants to use different

method of accounting for inventory.

• FIFO: First-In, First-Out

• LIFO: Last-In, First-Out

• Each valuation can affect income

and ending inventory valuation.

PPT 17-36

Accounts of the Income Statement

ACCOUNTS of the INCOME

STATEMENT

17-37

LO 17-4

• Operating Expenses – Cost

involved in operating a business,

such as rent, salaries and

supplies.

• Depreciation — The systematic

write-off of the cost of a tangible

asset over its estimated useful

life.

While depreciation is an expense, it is a noncash expense

for the company.

Chapter 17 – Understanding Accounting and Financial Information

17-71

PPT 17-38

The Statement of Cash Flows

The STATEMENT of CASH FLOWS

17-38

LO 17-4

• Statement of Cash Flows — Reports cash

receipts and cash disbursements related to the three

major activities of a firm:

1. Operations

2. Investments

3. Financing

See Figure 17.8 in the text for a sample statement of cash

flows for Very Vegetarian.

PPT 17-39

Understanding Cash Flow

• Cash Flow — The difference between cash coming

in and cash going out of a business.

UNDERSTANDING CASH FLOW

17-39

LO 17-4

• Managing cash flow is

a key consideration of a

business and can be

particularly challenging

for small and seasonal

businesses.

PPT 17-40

Would You Cook the Books?

WOULD YOU COOK the BOOKS?

17-40

• You are the only accountant employed by a small,

struggling dog food company.

• The company requests a bank loan to keep

operations going and your boss suggests you

record some revenue early.

• This is against accounting principles, but you

know if you don’t get the loan, you may lose your

job. What do you do?

Chapter 17 – Understanding Accounting and Financial Information

17-72

PPT 17-41

Progress Assessment

TEST PREP

17-41

• What are the key steps in preparing an income

statement?

• What’s the difference between revenue and

income on the income statement?

• Why is the statement of cash flows important in

evaluating a firm’s operations?

1. The key steps in preparing an income statement

are:

Revenue

−Cost of goods sold

= Gross profit (gross margin)

−Operating expenses

= Net income before taxes

−Taxes

= Net income or loss

2. Revenue is the monetary value of what a firm

receives for goods sold, services rendered, and

other payments such as rent. Income refers to the

bottom line which is the net income (or perhaps net

loss) the firm incurs from revenue minus sales

returns, costs, expenses, and taxes over a period of

time.

3. The statement of cash flows is important because it

answers such questions as: How much cash came

into the business from current operations? Did the

firm use cash to buy stocks, bonds, or other in-

vestments? Did it sell some investments that

brought in cash?

PPT 17-42

Using Financial Ratios

• Ratio Analysis — The assessment of a firm

’

s

financial condition using calculations and financial

ratios developed from the firm

’

s financial statements.

USING FINANCIAL RATIOS

17-42

LO 17-5

• Key ratios include:

– Liquidity ratios

– Leverage ratios

– Performance ratios

– Activity ratios

Ratio analysis provides an assessment of the firm’s finan-

cial condition. It can be extremely useful when results of a

ratio analysis are compared to industry peers.

Chapter 17 – Understanding Accounting and Financial Information

17-73

PPT 17-43

Commonly Used Liquidity Ratios

COMMONLY USED

LIQUIDITY RATIOS

17-43

LO 17-5

• Liquidity ratios measure a firm’s ability to turn

assets into cash to pay its short-term debts.

• Two key ratios are:

– Current ratio

– Acid-test ratio

• This information is found on the firm’s balance

sheet.

The acid-test ratio is sometimes referred to as the quick

ratio.

PPT 17-44

Leverage Ratios

LEVERAGE RATIOS

17-44

LO 17-5

• Leverage ratios measure the degree to which a

firm relies on borrowed funds in its operations.

• Key ratios include:

– Debt to Owner’s Equity Ratio

• This information is found on the firm’s balance

sheet.

PPT 17-45

Profitability Ratios

PROFITABILITY RATIOS

17-45

LO 17-5

• Profitability ratios measure how effectively a

firm’s managers are using the firm’s various

resources to achieve profits.

• Key ratios include:

– Basic earnings per share

– Return on sales

– Return on equity

• This information is found on the firm’s balance

sheet and income statement.

Chapter 17 – Understanding Accounting and Financial Information

17-74

PPT 17-46

Activity Ratios

ACTIVITY RATIOS

• This information is

found on the firm’s

balance sheet and

income statement.

17-46

LO 17-5

• Activity ratios measure how effectively

management is turning over inventory.

• Key ratios include:

– Inventory turnover ratio

PPT 17-47

Speaking a Universal Accounting Lan-

guage

SPEAKING a UNIVERSAL

ACCOUNTING LANGUAGE

17-47

• Multinational companies must adapt their

accounting reporting to the rules of multiple

countries.

• Many countries have adopted

International Financial Reporting Standards

(IFRS) and are pushing to make them standard.

• The U.S. Securities & Exchange Commission

believes there should be such a standard.

Chapter 17 – Understanding Accounting and Financial Information

17-75

PPT 17-48

Timeline for the Move to IFRS

TIMELINE for the MOVE to IFRS

17-48

Source: IFRS.org, accessed November 2014.

LO 17-5

• 2008: SEC offered proposed timeline

• 2009: 110 large companies had the option of using

IFRS

• 2012: SEC assessed progress of IFRS

• 2013: Final decision on the move to IFRS

• 2015: Large public companies will be required to

report in IFRS (pending SEC decision)

• 2016: All companies will be required to report in IFRS

(pending SEC decision)

1. This slide profiles the timeline for the move to In-

ternational Financial Reporting Standards.

2. International Financial Reporting Standards (IFRS)

are a set of accounting standards developed by the

International Accounting Standards Board (IASB)

that is becoming the global standard for the prepa-

ration of public company financial statements.

3. Ask students: What are some of the benefits of in-

ternational accounting standards?

4. If time permits have students explore the IFRS

website (www.ifrs.com) and review some of the

accounting case studies that the website presents.

PPT 17-49

Test Prep

TEST PREP

17-49

• What’s the primary purpose of performing ratio

analysis using the firm’s financial statements?

• What are the four main categories of financial

ratios?

1. Ratio analysis is the assessment of a firm’s finan-

cial condition, using calculations and financial rati-

os. Financial ratios are especially useful in com-

paring the company’s performance to its financial

objectives and to the performance of others in the

industry.

2. The four main categories of financial ratios are: li-

quidity, leverage, profitability and activity.