Chapter 17 – Understanding Accounting and Financial Information

17-46

MAKING

ethical

decisions

PPT 17–40

Would You Cook

the Books?

WOULD YOU COOK the BOOKS?

17-40

• You are the only accountant employed by a small,

struggling dog food company.

• The company requests a bank loan to keep

operations going and your boss suggests you

record some revenue early.

• This is against accounting principles, but you

know if you don’t get the loan, you may lose your

job. What do you do?

PPT 17-39

Understanding Cash Flow

• Cash Flow — The difference between cash coming

in and cash going out of a business.

UNDERSTANDING CASH FLOW

17-39

LO 17-4

• Managing cash flow is

a key consideration of a

business and can be

particularly challenging

for small and seasonal

businesses.

test

prep

PPT 17-41

Test Prep

TEST PREP

17-41

• What are the key steps in preparing an income

statement?

• What’s the difference between revenue and

income on the income statement?

• Why is the statement of cash flows important in

evaluating a firm’s operations?

PPT 17-42

Using Financial Ratios

• Ratio Analysis — The assessment of a firm

’

s

financial condition using calculations and financial

ratios developed from the firm

’

s financial statements.

USING FINANCIAL RATIOS

17-42

LO 17-5

• Key ratios include:

– Liquidity ratios

– Leverage ratios

– Performance ratios

– Activity ratios

Chapter 17 – Understanding Accounting and Financial Information

17-47

pared to its financial objectives.

3. They also provide key insights into the firm’s per-

formance compared to other firms in the industry.

B. LIQUIDITY RATIOS measure the company’s ability to

turn assets into cash to pay its short-term debts.

1. Short-term debts are expected to be repaid within

one year.

2. The CURRENT RATIO is the ratio of a firm’s cur-

rent assets to its current liabilities.

a. Current ratio = Current assets

Current liabilities

b. Usually, a company with a current ratio of 2 or

better is considered a safe credit risk.

c. The ratio should be compared to that of com-

peting firms within the industry and to the

company’s current ratio in the previous year.

3. The ACID-TEST RATIO (or QUICK RATIO)

measures the cash, marketable securities, and

receivables of the firm, to its current liabilities.

a. Acid-test ratio =

Cash + Accounts receivable + Marketable securities

Current liabilities

b. This ratio is important to firms that have diffi-

culty converting inventory into quick cash.

C. LEVERAGE (DEBT) RATIOS measure the degree to

which a firm relies on borrowed funds in its operations.

Chapter 17 – Understanding Accounting and Financial Information

17-48

critical thinking

exercise 17-4

CALCULATING FINANCIAL RATIOS

(ADVANCED)

This exercise directs students to use the financial reports of a

company to calculate key financial ratios. (See the complete

exercise on page 17.92 of this manual.)

PPT 17-43

Commonly Used Liquidity Ratios

COMMONLY USED

LIQUIDITY RATIOS

17-43

LO 17-5

• Liquidity ratios measure a firm’s ability to turn

assets into cash to pay its short-term debts.

• Two key ratios are:

– Current ratio

– Acid-test ratio

• This information is found on the firm’s balance

sheet.

critical thinking

exercise 17-5

COMPARING INDUSTRY RATIOS

(BASIC)

An investor is considering investing in a regional hotel chain.

This exercise lets students compare the financial results for

four possible investments. (See the complete exercise on page

17.97 of this manual.)

Chapter 17 – Understanding Accounting and Financial Information

17-49

1. The DEBT TO OWNERS’ EQUITY RATIO

measures the degree to which the company is fi-

nanced by borrowed funds that must be repaid.

a. Debt to owners’ equity ratio =

Total liabilities

Owners’ equity

b. A ratio above 1 (above 100%) shows that a

firm has more debt than equity.

2. It is important to COMPARE RATIOS to those of

other firms in the same industry and to the com-

pany’s ratios in previous years.

D. PROFITABILITY (PERFORMANCE) RATIOS meas-

ure how effectively a firm is using its various re-

sources to achieve profits.

1. EARNINGS PER SHARE (EPS) is an important

ratio because earnings help stimulate growth.

a. The Financial Accounting Standards Board

requires companies to report their quarterly

earning per share two ways: basic and dilut-

ed.

b. BASIC EARNINGS PER SHARE (BASIC

EPS) measures the amount of profit earned

by a company for each share of common

stock it has outstanding.

c. Basic earnings per share =

Net income after taxes

Number of shares common stock outstanding

d. DILUTED EARNINGS PER SHARE (DILUT-

ED EPS) measures the amount of profit

Chapter 17 – Understanding Accounting and Financial Information

17-50

PPT 17-44

Leverage Ratios

LEVERAGE RATIOS

17-44

LO 17-5

• Leverage ratios measure the degree to which a

firm relies on borrowed funds in its operations.

• Key ratios include:

– Debt to Owner’s Equity Ratio

• This information is found on the firm’s balance

sheet.

PPT 17-45

Profitability Ratios

PROFITABILITY RATIOS

17-45

LO 17-5

• Profitability ratios measure how effectively a

firm’s managers are using the firm’s various

resources to achieve profits.

• Key ratios include:

– Basic earnings per share

– Return on sales

– Return on equity

• This information is found on the firm’s balance

sheet and income statement.

Chapter 17 – Understanding Accounting and Financial Information

17-51

earned by a company for each share of out-

standing common stock, but also takes into

consideration stock options, warrants, pre-

ferred stock, and convertible debt securities

that can be converted into common stock.

3. RETURN ON SALES is calculated by compar-

ing a company’s net income with its total sales.

Return on sales = Net income

Net sales

4. RETURN ON EQUITY (ROE) measures how

much was earned for each dollar invested by

owners.

a. The higher the RISK involved in an industry,

the higher the RETURN investors expect on

their investment.

b. It is calculated by comparing a company’s

net income with its total owner’s equity.

c. Return on equity = Net income after taxes

Total owners’ equity

5. These and other profitability ratios are vital

measurements of company growth and man-

agement performance.

E. ACTIVITY RATIOS measure the effectiveness of

the firm’s management in using the assets that are

available.

1. INVENTORY TURNOVER RATIO measures the

speed of inventory moving through the firm and

its conversion into sales.

Chapter 17 – Understanding Accounting and Financial Information

17-52

TEXT FIGURE 17.9

Accounts in the Balance Sheet and

Income Statement

This figure shows the major accounts included on the income

statement and the balance sheet.

PPT 17-46

Activity Ratios

ACTIVITY RATIOS

• This information is

found on the firm’s

balance sheet and

income statement.

17-46

LO 17-5

• Activity ratios measure how effectively

management is turning over inventory.

• Key ratios include:

– Inventory turnover ratio

Chapter 17 – Understanding Accounting and Financial Information

17-53

a. The more efficiently a firm manages its in-

ventory, the higher the return.

b. Inventory turnover ratio =

Cost of goods sold

Average inventory

c. A lower than average inventory turnover ra-

tio often indicates obsolete merchandise on

hand or poor buying practices.

d. Proper inventory control and expected inven-

tory turnover should be monitored.

F. Finance professionals use several other specific ra-

tios to learn more about a firm’s financial condition.

VI. SUMMARY

Chapter 17 – Understanding Accounting and Financial Information

17-54

bonus case 17-2

MANAGING BY THE NUMBERS

This case discusses how financially knowledgeable workers

helped improve one company’s finances. (See the complete

case, discussion questions, and suggested answers beginning on

page 17.102 of this manual.)

CONNECTING

ACROSS

borders

PPT 17-47

Speaking a Uni-

versal Accounting

Language

SPEAKING a UNIVERSAL

ACCOUNTING LANGUAGE

17-47

• Multinational companies must adapt their

accounting reporting to the rules of multiple

countries.

• Many countries have adopted

International Financial Reporting Standards

(IFRS) and are pushing to make them standard.

• The U.S. Securities & Exchange Commission

believes there should be such a standard.

PPT 17-48

Timeline for the Move to IFRS

TIMELINE for the MOVE to IFRS

17-48

Source: IFRS.org, accessed November 2014.

LO 17-5

• 2008: SEC offered proposed timeline

• 2009: 110 large companies had the option of using

IFRS

• 2012: SEC assessed progress of IFRS

• 2013: Final decision on the move to IFRS

• 2015: Large public companies will be required to

report in IFRS (pending SEC decision)

• 2016: All companies will be required to report in IFRS

(pending SEC decision)

test

prep

PPT 17-49

Test Prep

TEST PREP

17-49

• What’s the primary purpose of performing ratio

analysis using the firm’s financial statements?

• What are the four main categories of financial

ratios?

Chapter 17 – Understanding Accounting and Financial Information

17-55

PowerPoint slide notes

PPT 17-1

Chapter Title

Copyright © 2015 by the McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin

Understanding

Accounting

and

Financial

Information

CHAPTER 17

PPT 17-2

Learning Objectives

LEARNING OBJECTIVES

17-2

1. Demonstrate the role that accounting and financial

information play for a business and its stakeholders.

2. Identify the different disciplines within the accounting

profession.

3. List the steps in the accounting cycle, distinguish

between accounting and bookkeeping, and explain

how computers are used in accounting.

PPT 17-3

Learning Objectives

LEARNING OBJECTIVES

17-3

4. Explain how the major financial statements differ.

5. Demonstrate the application of ratio analysis in

reporting financial information.

Chapter 17 – Understanding Accounting and Financial Information

17-56

PPT 17-4

John Raftery

JOHN RAFTERY

Patriot Contractors

17-4

• Served in the Marines and

used his G.I. Bill to study

accounting.

• Completed an

entrepreneurship program

for veterans and launched

Patriot Contractors.

• He credits his knowledge of

accounting with the growth of

his business.

PPT 17-5

Name That Company

NAME that COMPANY

17-5

Accounting software makes financial information

available whenever the organization needs it.

We specialize in software that addresses the

accounting needs of small businesses that are

often very different from major corporations.

Name that company!

Companies: Intuit’s QuickBooks and Sage’s

Peachtree

PPT 17-6

What’s Accounting?

WHAT’S ACCOUNTING?

17-6

LO 17-1

• Accounting — Recording, classifying, summarizing

and interpreting of financial events and transactions in

an organization to provide interested parties needed

financial information.

• Outside parties – like employees, owners,

creditors, unions, investors and the government –

make use of a firm’s accounting information.

Chapter 17 – Understanding Accounting and Financial Information

17-57

PPT 17-7

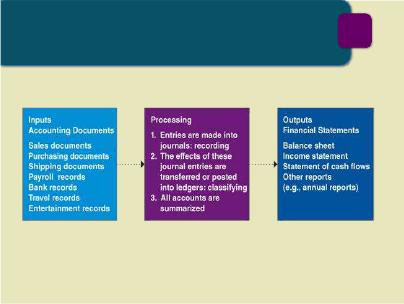

The Accounting System

The ACCOUNTING SYSTEM

17-7

LO 17-1

1. For students who are not taking an accounting

class, this slide can help them understand an ac-

counting system from a production perspective:

• Inputs: Sales documents, purchasing doc-

uments, payroll records travel expenses,

etc.

• Processing: Entries are made to journals;

then transferred into ledgers; and finally

summarized and reviewed to compile a tri-

al balance.

• Outputs: Development of financial state-

ments such as the balance sheet, income

statement, and statement of cash flows,

prepared for management personnel within

the company as well as interested parties

outside the company.

2. 1.It is very important for students to understand the

importance of integrity when calculating numbers.

Generally Accepted Accounting Principles

(GAAP) outlines procedures that are generally ac-

cepted in the accounting field.

3. Ask students: What role did questionable account-

ing procedures play with Enron, Fannie Mae, and

WorldCom?

Chapter 17 – Understanding Accounting and Financial Information

17-58

PPT 17-8

Accountants’ Responsibilities

ACCOUNTANTS’

RESPONSIBILITIES

17-8

LO 17-1

1. One of the biggest uses of accountants by business

is taxes and auditing. Explain to the class that the

theme of “integrity of numbers” is critical for busi-

ness.

2. In addition to the reasons listed on the slide, ac-

countants can offer businesses the following value-

added services:

• Getting complete visibility of processes

• Seeing the true cost of a process or part of

a process

• Seeing the cost of process changes, volume

changes, headcount, wastage, scrap, re-

jects, nonconformance, downtime

• Seeing costs by job and by department

• Seeing and comparing costs of outsourcing

• Mapping business processes, organization-

wide or job specific

• Using scenario analysis to see how reengi-

neering will affect resources such as costs

and headcounts

PPT 17-9

Managerial Accounting

MANAGERIAL ACCOUNTING

17-9

LO 17-2

• Managerial Accounting — Provides information

and analysis to managers inside the organization to

assist them in decision making.

• Managerial accounting is involved with:

– Costs of production

– Costs of marketing

– Preparation and control of budgets

– Minimizing tax liabilities

Chapter 17 – Understanding Accounting and Financial Information

17-59

PPT 17-10

Users of Accounting Information

USERS of ACCOUNTING

INFORMATION

17-10

LO 17-2

1. This slide (Figure 17.2) gives the students an over-

view of the importance of accounting information

when managing a business. Accounting proce-

dures are the foundation for controlling mecha-

nisms that businesses put in place to measure per-

formance and plan for the future. Accounting in-

fluences decisions for managers in the following

ways:

• Understanding cost behavior and perform

cost–volume profit analysis

• Using cost allocation in planning and control

• Using job-order-costing and process–costing

to track the flow of costs to products

• Using relevant information to make market-

ing and production decisions

• Using capital budgeting techniques to make

long-term capital investment decisions

2. Accounting information can improve a company’s

ability to compete by:

• Using competitor information and sales

analysis to bring new concepts to the finan-

cial planning process

• Learning to spot financial trends to predict

strategic business decisions

• Learning how to integrate technology into

decision making

3. Explain to students the most important point of us-

ing this information to influence decision making is

to make sure you have the RIGHT information, at

the RIGHT time, and in the RIGHT format.

PPT 17-11

Financial Accounting

FINANCIAL ACCOUNTING

17-11

LO 17-2

• Financial Accounting — Financial information and

analyses are generated for people primarily outside

the organization. Outside users are interested in these

questions:

– Is the organization profitable?

– Is it able to pay its bills?

– How much debt does it owe?

• Annual Report — A yearly statement of the financial

condition, progress, and expectations of the firm.

Chapter 17 – Understanding Accounting and Financial Information

17-60

PPT 17-12

How to Read an Annual Report

• Key things to watch for and read:

HOW to READ

an ANNUAL REPORT

17-12

LO 17-2

– Management’s

discussion and

analysis of operations

– Balance sheet

– Income statement

– Statement of cash

flows

– Auditor’s opinion

1. This slide presents the key areas to read when ana-

lyzing a company’s annual report.

2. It is important that students understand that the an-

nual report is more than a balance sheet but con-

tains different areas that are just as important.

3. The auditor’s opinion is a critical area for students

to understand. Basically there are four different

types of opinion letters that can be submitted.

They are:

A. Unqualified opinion: An unqualified opin-

ion letter involves a certification made by

the independent CPA firm that the compa-

ny’s financial statements were prepared in

conformity with GAAP, and fairly repre-

sented the firm’s financial condition on the

statement date.

B. Qualified opinion: A qualified auditor’s

opinion letter is one in which the CPA has

included one or more specific qualifica-

tions to its assurance that the customer‘s fi-

nancial statements follow GAAP. This

means that one or more irregularities were

found, and that the customer could not or

would not correct these irregularities.

C. Adverse opinion: This is the most serious

of all the opinion letters that can accompa-

ny a customer‘s financial statements. When

a CPA firm discovers information during

the course of its audit that demonstrates

material noncompliance with GAAP ac-

counting rules, the CPA may choose to

submit an adverse opinion letter to accom-

pany the financial statements of the com-

pany under review.

D. Disclaimer of opinion: Due to scope limita-

tions, a CPA may be unwilling to express

any opinion about the accuracy of a cus-

tomer’s financial statements. A disclaimer

of opinion letter means the CPA does not

assume responsibility for the accuracy of

the company’s financial statements.

(Source: www.encyclopediaofcredit.com.)