12,000$

520

780

Book

Value

$600 $600 $15,400

800 1,400 14,600

800 2,200 13,800

800 3,000 13,000

Accumulated Book

Depreciation Value

$800 $800 $15,200

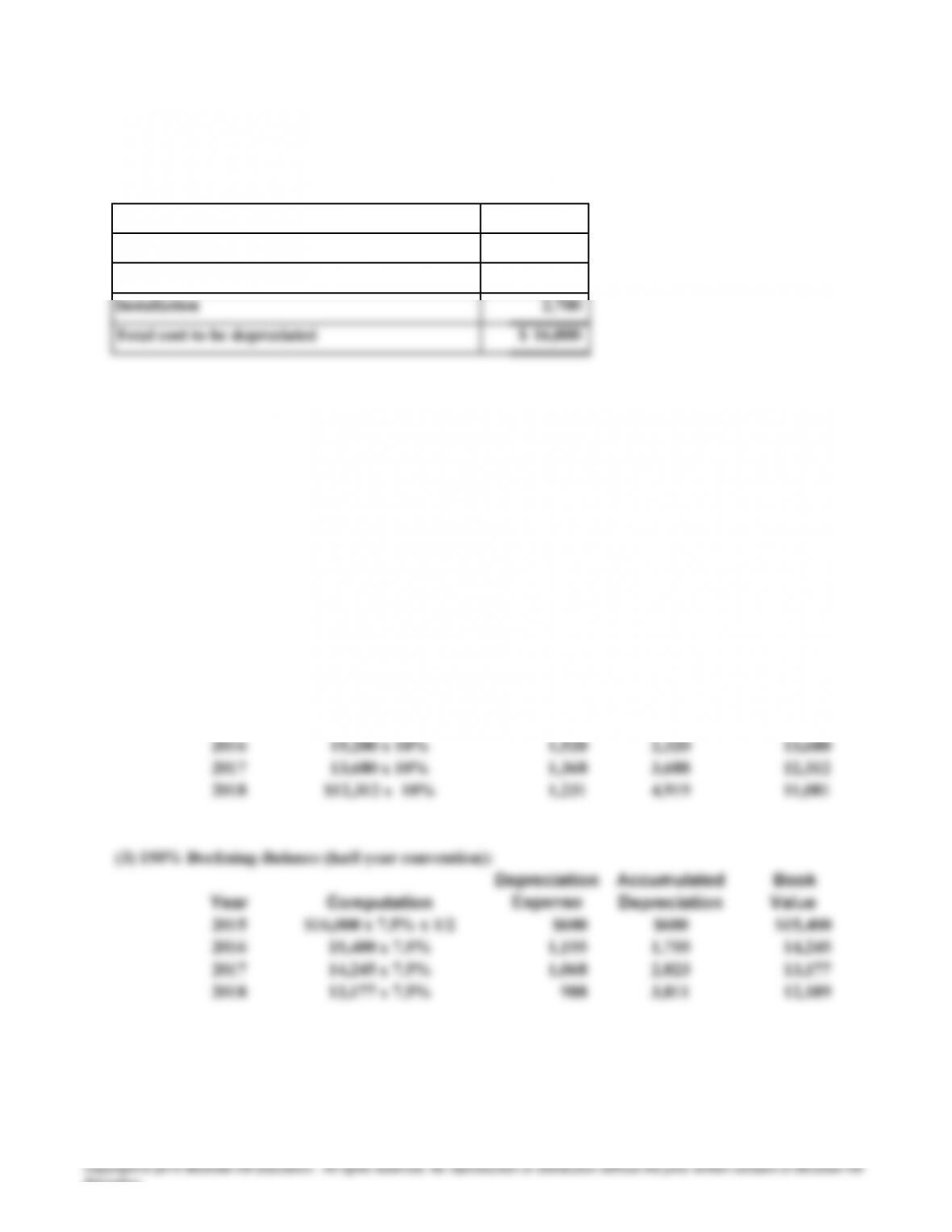

(2) 200% Declining-Balance (half-year convention):

$16,000 x 10% x 1/2

Year

2015

PROBLEM 9.3

A

50 Minutes, Strong

Accumulated

Depreciation

Depreciation

Expense

a. Costs to be depreciated include:

Cost of shelving

Freight charges

Sales taxes

16,000 x 1/20

16,000 x 1/20

2016

2017

2018

Computation

$16,000 x 1/20 x 9/12

Year

2015

HILLS HARDWAR

E

16,000 x 1/20

(1) Straight-Line Schedule (nearest whole month):

Depreciation

Expense

Computation

Education.

b.

d.

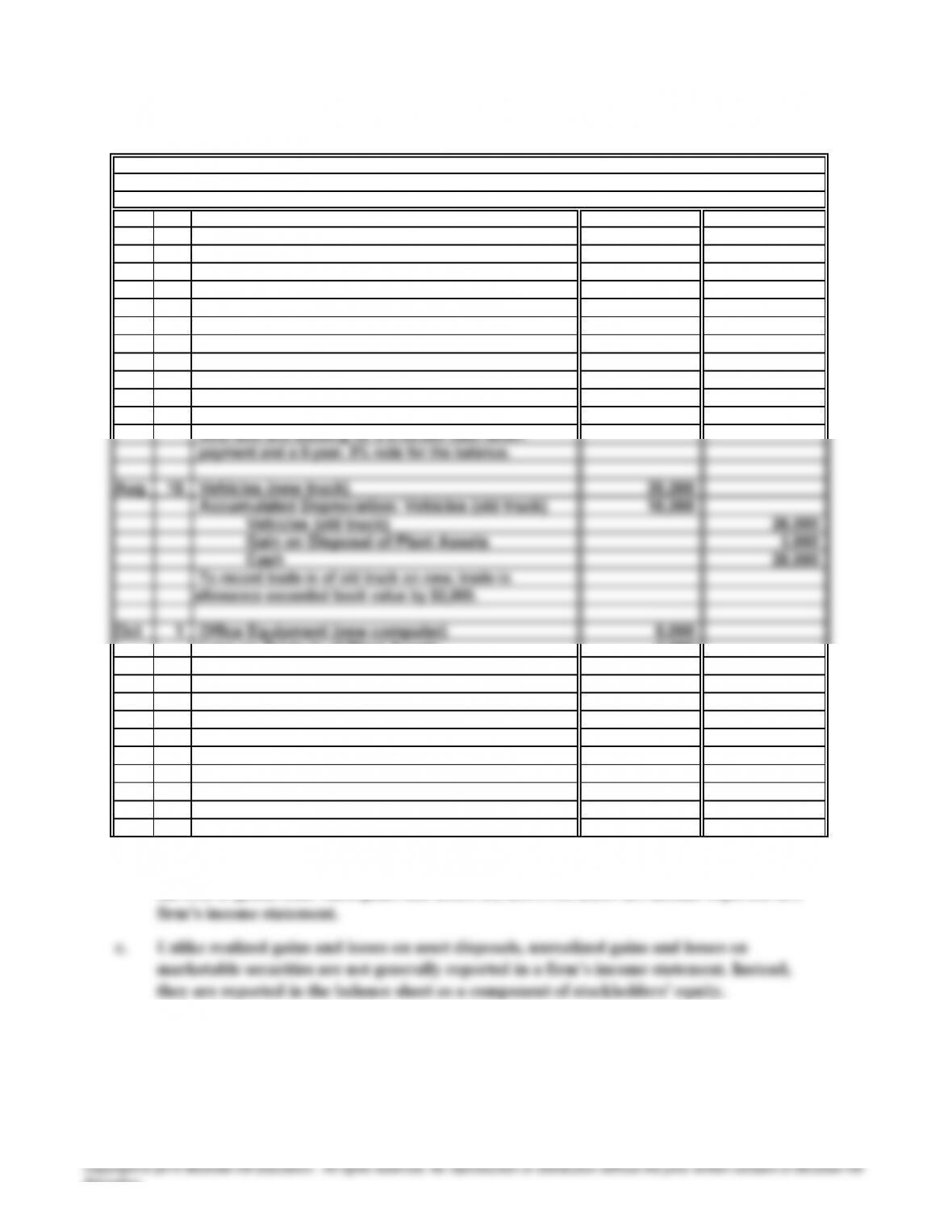

1. Journal entry assuming that the shelving was sold for $1,100:

1,100

8,600

9,000

700

To record sale of shelving for $1,100 cash.

2. Journal entry assuming that the shelving was sold for $175:

175

8,600

To record sale of shelving for $175 cash.

the end of 2018 ($11,081). Depreciation, however, is not a process of valuation.

Thus, the $11,081 book value is not an estimate of the shelving’s fair value at the

end of 2018.

A book value of $400 means that accumulated depreciation at the time of the

disposal must have been $8,600.

Cash

Accumulated Depreciation: Shelving

Accumulated Depreciation: Shelving

PROBLEM 9.3

A

HILLS HARDWARE (concluded

)

Hills Hardware may use the straight-line method in its financial statements to

achieve the least amount of depreciation expense in the early years of the shelving’s

Shelving

Gain on Disposal of Assets

Cash

Education.

25 Minutes, Medium

Feb 10 Loss on Dis

p

osal of Plant Assets 2,200

Accumulated De

p

reciation: Office E

q

ui

p

ment 21,800

Office E

q

ui

p

ment 24,000

Scrapped office equipment; received no salvage value.

A

pr

1 Cash 100,000

Notes Receivable 800,000

Accumulated De

p

reciation: Buildin

g

250,000

Land 50,000

Buildin

g

550,000

Gain on Sale of Plant Assets 550,000

Loss on Trade-in of Plant Assets 3,500

Accumulated Depreciation: Office Equip. (old computer) 11,000

Office E

q

ui

p

ment

(

old com

p

uter

)

15,000

Cash 1,500

Notes Pa

y

able 6,000

Acquired new computer system by trading in old

computer, paying part cash, and issuing a 1-year,

8% note payable. Recognized loss equal to book value of

old computer ($4,000) minus trade-in allowance ($500).

b.

Gains and losses on asset disposals do not affect gross profit because they are not part of

the cost of goods sold. Such gains and losses do, however, affect net income reported in a

PROBLEM 9.4

A

a.

General Journal

HITCHCOCK DEVELOPERS

Education.

p

25 Minutes, Medium

a.

b.

d.

PROBLEM 9.5

A

REDDICK CORPORATION

Intangible asset. A patent grants its owner the exclusive right to produce a particular

product. If the patent has significant cost, this cost is regarded as an intangible asset and

Operating expense. Although the training of employees probably has some benefit

extending beyond the current period, the number of periods benefited is highly uncertain.

Therefore, current accounting practice is to expense routine training costs.

Intangible asset. Goodwill represents the expected value of future earnings in excess of

what is considered normal. The goodwill associated with Reddick’s purchase of the vinyl

costs) will be capitalized as an asset and amortized over the estimated useful life, limited to

20 years.

Education.

20 Minutes, Medium

220,000$

9.25

PROBLEM 9.6

A

KIVI SERVICE STATIONS

a. Estimated goodwill associated with the purchase of Joe’s Garage:

Actual average net income per year

Typical sales multiplier

Education.

30 Minutes, Medium

a.

b. $20,000

(6,400) $13,600

c.

PROBLEM 9.7

A

THAXTON, INC.

Depreciation expense for the first two years under the three depreciation methods is

determined as follows:

Less: Accumulated depreciation

The units of output method is directly tied to the miles driven rather than calendar time

and, as a result, the exact amount of depreciation expense to be recognized each accounting

Units-of-Output:

Truck

Education.

30 Minutes, Medium

a.

$275,000

75,000

$350,000

b.

c.

$350,000

(52,500) $297,500

60,000*

$357,500

Less: Accumulated depreciation

Patent

Plant and intangible asset sections of the balance sheet:

Amortization on the patent is calculated as follows (same for each year):

$75,000/5 years = $15,000

PROBLEM 9.8

A

ROTHCHILD, INC.

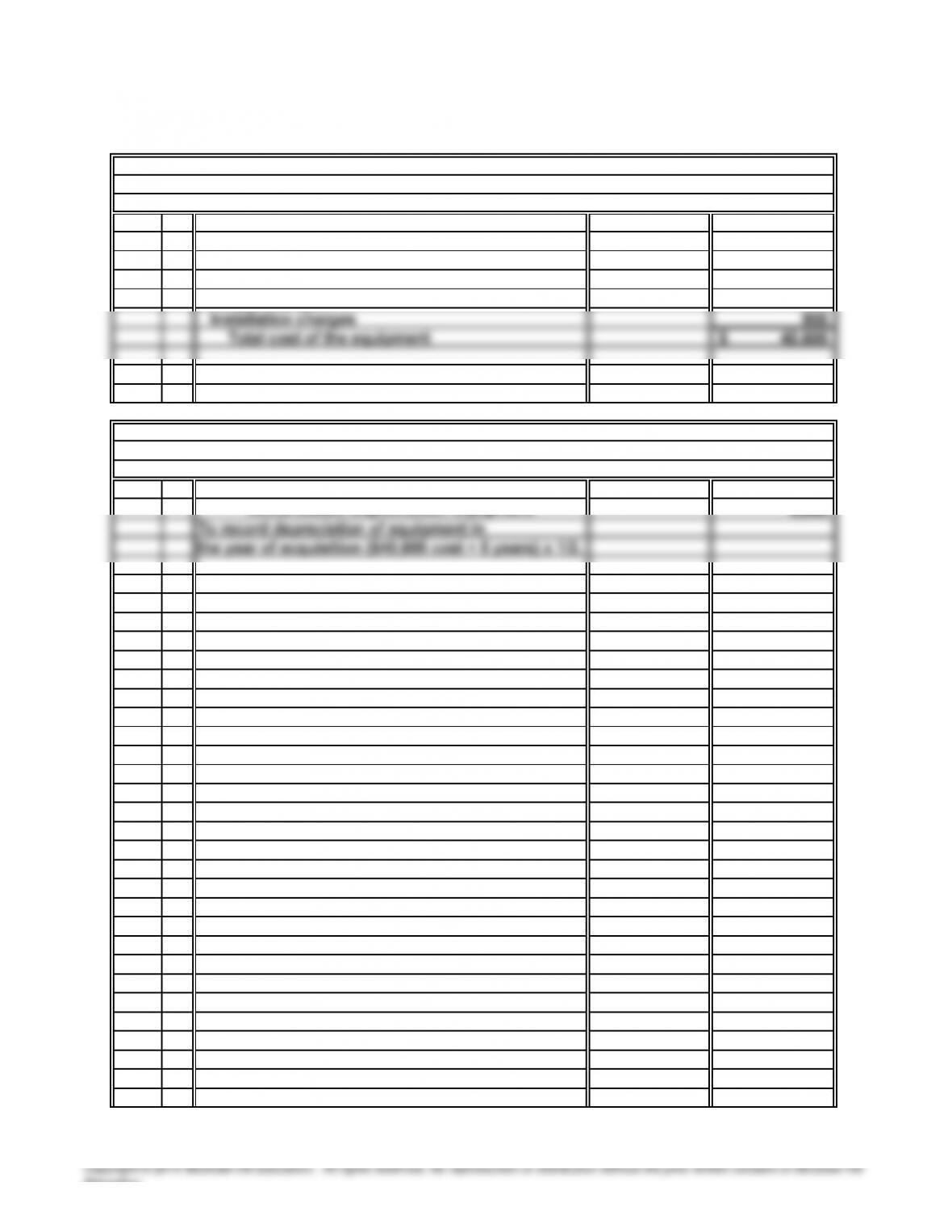

Depreciation is calculated on the following amount:

Purchase price

Plus: Expenditures to prepare asset for use

Total plant and intangible assets

*$75,000 – $15,000 = $60,000

Year 2

Depreciation expense for Year 1:

Depreciation expense for Year 2:

Year 1:

Equipment

The declining balance rate at 150% of the straight-line is:

100%/10 years = 10%; 10% x 1.5 = 15%

Education.

a.

b. (1)

PROBLEM 9.1B

SMITHFIELD HOTEL

25 Minutes, Easy

The cost of plant and equipment includes all expenditures that are reasonable and necessary

in acquiring the asset and placing it in a position and condition for use in the operation of

the business.

The purchase price of $37,000 ($42,000 – $5,000) is part of the cost of the equipment.

The list price ($42,000) is not relevant, as this is not the actual price paid by Smithfield

Education.

c.

Equipment account:

37,000$

2,100

600

Dec 31 4,060

Accumulated Depreciation: Equipment 4,060

PROBLEM 9.1B

SMITHFIELD HOTEL (concluded)

Purchase price ($42,000 − 5,000)

Expenditures that should be debited to the

Sales ta

x

d.

Freight charges

Depreciation Expense: Equipment

Education.

Book

Year Value

2013 $17,000 $17,000 $163,000

2014 34,000 51,000 129,000

2016 20,736 148,896 31,104

2017 12,442 161,338 18,662

2018 8,662 170,000 10,000

Accumulated Book

Year Depreciation Value

2013 $27,000 $27,000 $153,000

2014 45,900 72,900 107,100

Depreciation

Expense

153,000 x 30%

Accumulated

Depreciation

$170,000 x 1/5 x 1/2

170,000 x 1/5

31,104 x 40%

51,840 x 40%

18,662 – 10,000

PROBLEM 9.2B

45 Minutes, Medium

R & R, INC.

a. (1) Straight-Line Schedule:

$180,000 x 30% x 1/2

Computation

Computation

(3) 150% Declining-Balance Schedule:

Depreciation

Expense

Education.

c.

$ 58,000

$ 26,896

3. 150% Declining-Balance:

52,479

$ 5,521

The reported gain or loss on the sale of an asset has no direct cash effects. The only direct cash

effect associated with the sale of this machine is the $58,000 received by R & R, Inc. from the

buyer.

Book value on 12/31/16

1. Straight-Line

Gain on disposal

Gain on disposal

PROBLEM 9.2B

R & R, INC. (concluded)

Computation of gains or losses upon disposal:

Cash proceeds

Education.