c.

PROBLEM 8.1B

DOBBINS SUPPLY, INC. (concluded)

Yes. As shown in part a, the LIFO method resulted in the highest cost of goods sold figure, whereas

Education.

30 Minutes, Strong

(1) Average-cost method:

(a) Cost of goods sold on April 28:

8

,

111

$

40

,

555

$

(b) Ending inventory (7 units) at June 30:

32

,

444

$

25

,

500

57

,

944

$

,

$

y,

)

,

000$ 8

,

,

$

g

(

)

,

(b) Ending inventory (7 units) at June 30: 32

,

800

$

25

,

500 58

,

$

g

y,

,

$

,

000

$

(b) Ending inventory (7 units) at June 30: 32

,

000

$

25

,

500 57

,

500

$

3 units from

p

urchase on Ma

y

8

@

$8

,

500

Endin

g

inventor

y,

June 30

4 units from A

p

ril 19

p

urchase

@

$8

,

200

3 units from Ma

y

8

p

urchase

@

$8

,

500

4 units from

p

urchase of A

p

ril 1

@

$8

,

000

Cost of

g

oods sold

(

5 units

)

Total

4 units from A

p

ril 1

p

urchase

@

$8,000

PROBLEM 8.2B

a. Cost of goods sold and ending inventory

SEA TRAVEL: PERPETUAL SYSTE

M

3 units

p

urchased on Ma

y

8 at $8

,

500 each

Avera

g

e cost

(

as of A

p

ril 28

;

$73

,

000 ÷ 9 units

)

Cost of

g

oods sold

(

5 units

@

$8

,

111

)

Avera

g

e unit cost followin

g

A

p

ril 19

p

urchase:

4 units at A

p

ril 19 avera

g

e cost of $8

,

111

Education.

,

$

(

b. (1)

income tax returns. However, tax laws do require that taxpayers using LIFO for tax purposes

must also use the LIFO method for financial reporting purposes.

Problem 8.2B

SEA TRAVEL: PERPETUAL SYSTE

M

The LIFO method will result in the lowest net income, as it assigns the most recent (highest)

costs to the cost of goods sold. LIFO will result in the lowest net income whenever the most

(concluded)

Education.

20 Minutes, Medium

(1) Average-cost method:

Ending inventory at June 30:

8

,

208

$

57

,

456

$

Cost of goods sold through June 30: 98

,

$

,

(

,

$

,

$

,

,

$

g

y

,

$

,

,

$

Avera

g

e cost

(

$98

,

500 ÷ 12 units

)

Endin

g

inventor

y

(

7 units

@

$8

,

208

)

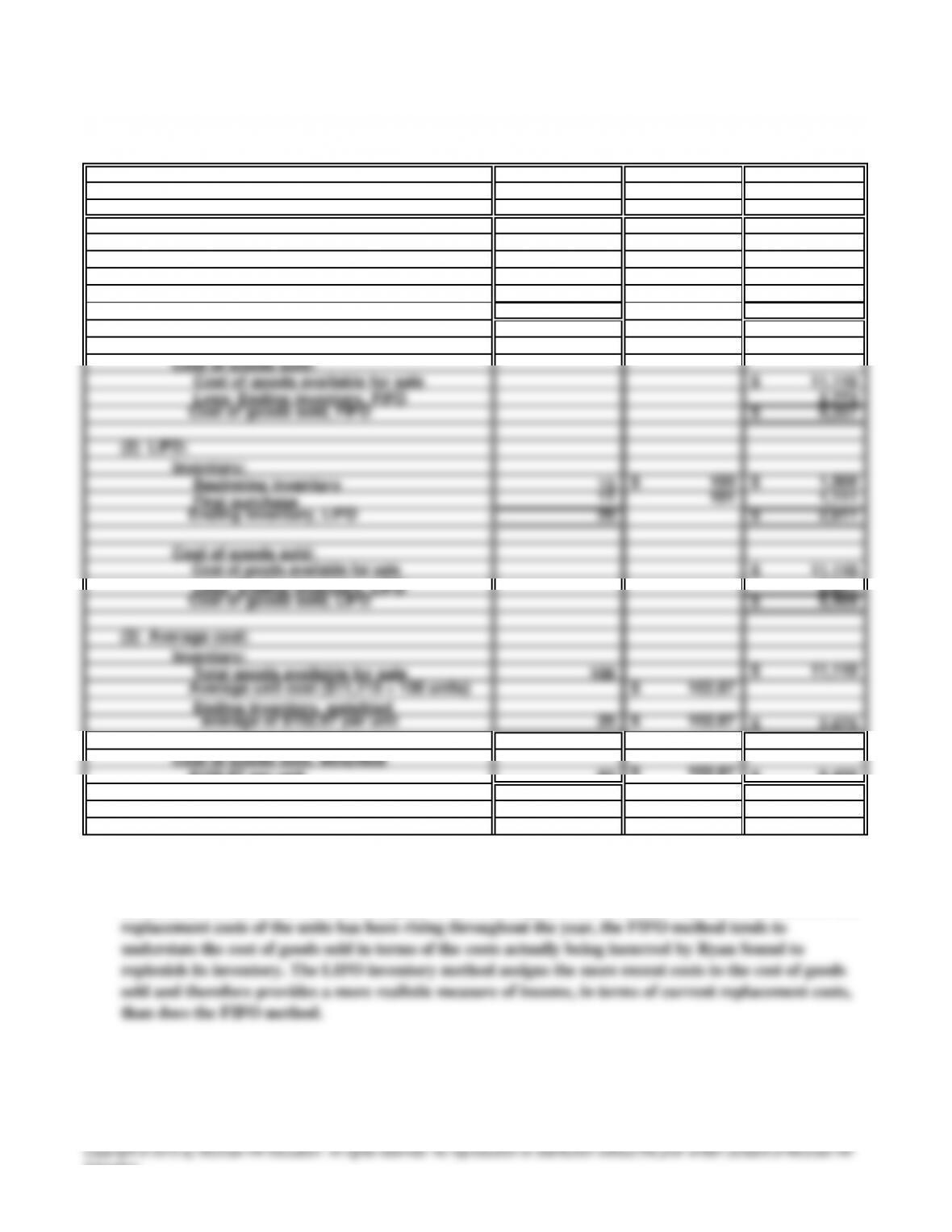

PROBLEM 8.3B

a. Cost of goods sold and ending inventory

SEA TRAVEL: PERIODIC SYSTEM

Education.

20 Minutes, Medium

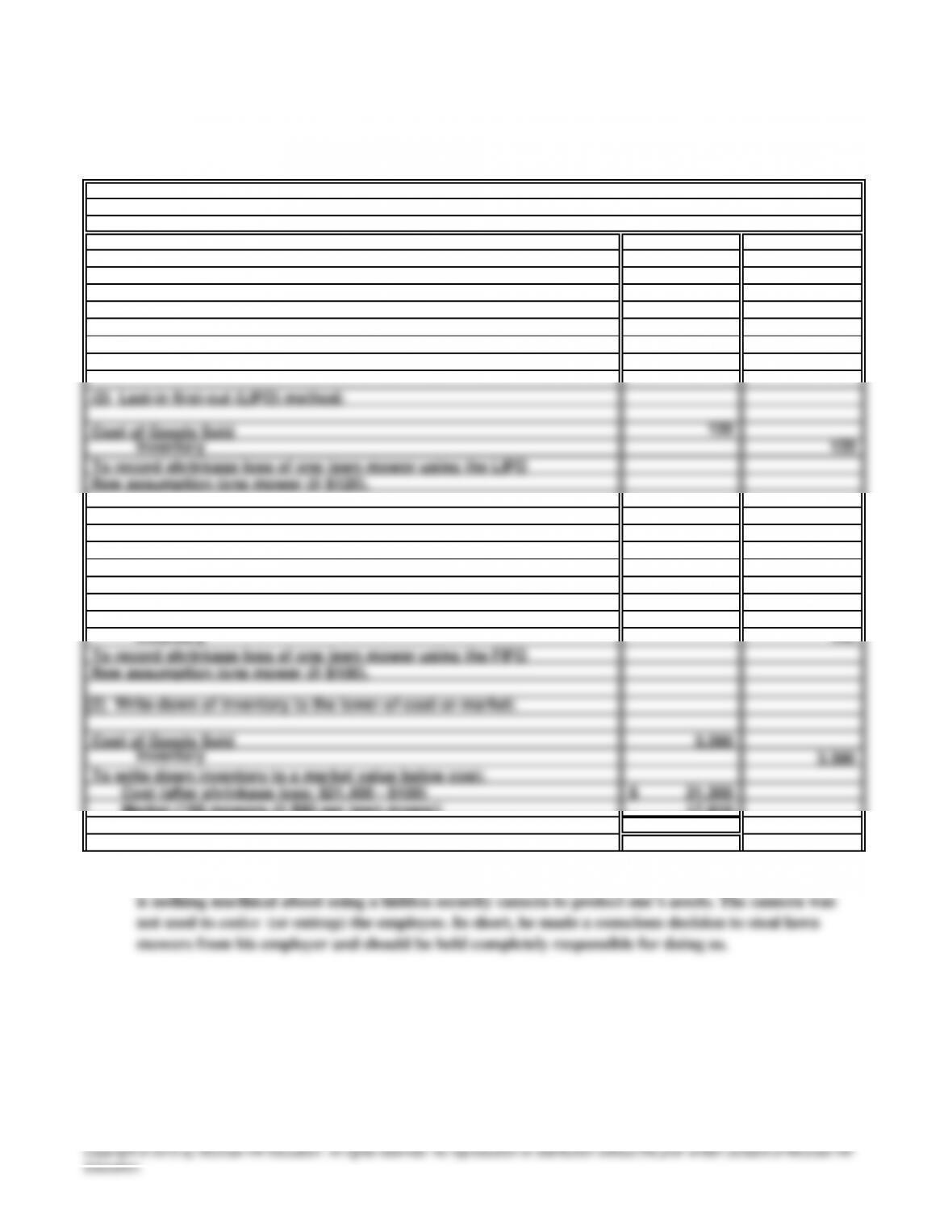

a. Shrinkage loss-one lawn mower

107

Inventor

y

107

g

g

p

y

g

g

(

)

g

y

$

17

,

910 3

,

390

$

c.

The only unethical act in this situation was committed by the employee against his employer. There

is nothing unethical about using a hidden security camera to protect one’s assets. The camera was

not used to entice (or entrap) the employee. In short, he made a conscious decision to steal lawn

mowers from his employer and should be held completely responsible for doing so.

Market

(

199 mowers

@

$90

p

er lawn mower

)

Loss from write-down to market value

(2) Write-down of inventory to the lower-of-cost-or-market:

Cost of Goods Sold

p

To record shrinka

g

e loss of one lawn mower usin

g

avera

g

e

cost of $107

(

$21

,

400 ÷ 200 mowers = $107

p

er mower

)

.

(

1

)

Avera

g

e-cost method:

PROBLEM 8.4B

SAM’S LAWN MAINTENANC

E

y

25 Minutes, Easy

U

n

it

s

U

n

it

C

os

t

T

o

t

a

l

C

os

t

a. Inventory and cost of goods sold:

(1) FIFO:

Fourth

p

urchase 16 108

$

1

,

728

$

Third

p

urchase

5

106 530

S

econ

d

P

urc

h

ase 5 103

$

515

$

26 2

,

773

$

C

8

$

11

101

1

E

26

2

$

$

,

C

8

$

26

102

$

,

$

,

$

y

y

PROBLEM 8.5B

RYAN SOUND

Endin

g

Inventor

y,

FIFO

Inventor

y

:

,

20 Minutes, Medium

a.

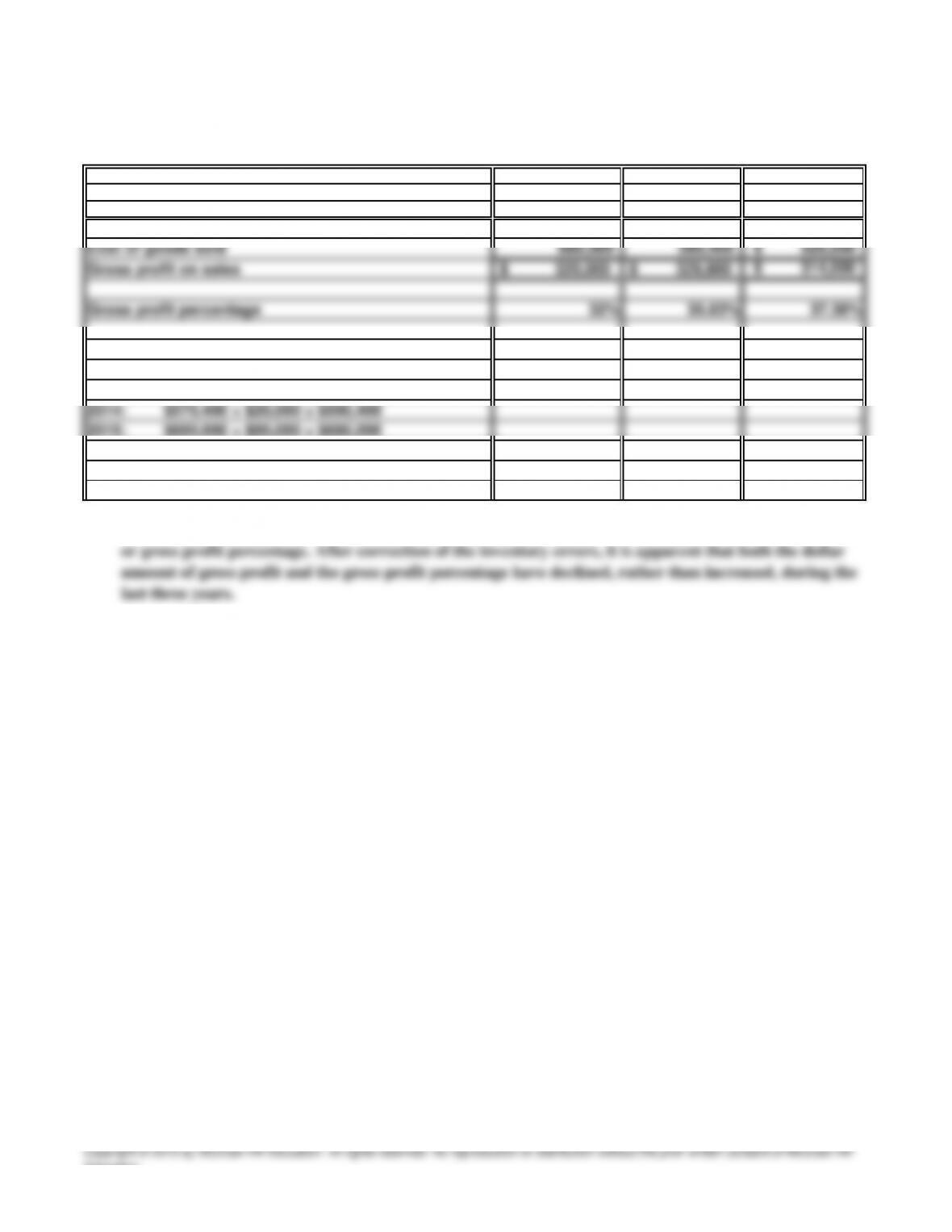

2015

2014

2013

Net sales 1,000,000$ 920,000$ 840,000$

PROBLEM 8.6B

CITY SOFTWARE

Cost of Goods Sold:

$546,000 – $20,000 = $526,000 2013:

Education.

25 Minutes, Medium

a.

330

,

000

$

600

,

000

b.

75

,

000

$

55%

41

,

250

$

44,000$

41

250

2

$

,

$

y

,

(

)

,

$

g

41

,

250

288

,

750

G

ross pro

fit

231

,

250

$

c.

Cost ratio

(p

er

p

art a

,

above

)

Endin

g

inventor

y

at cost

(

$75

,

000 x 55%

)

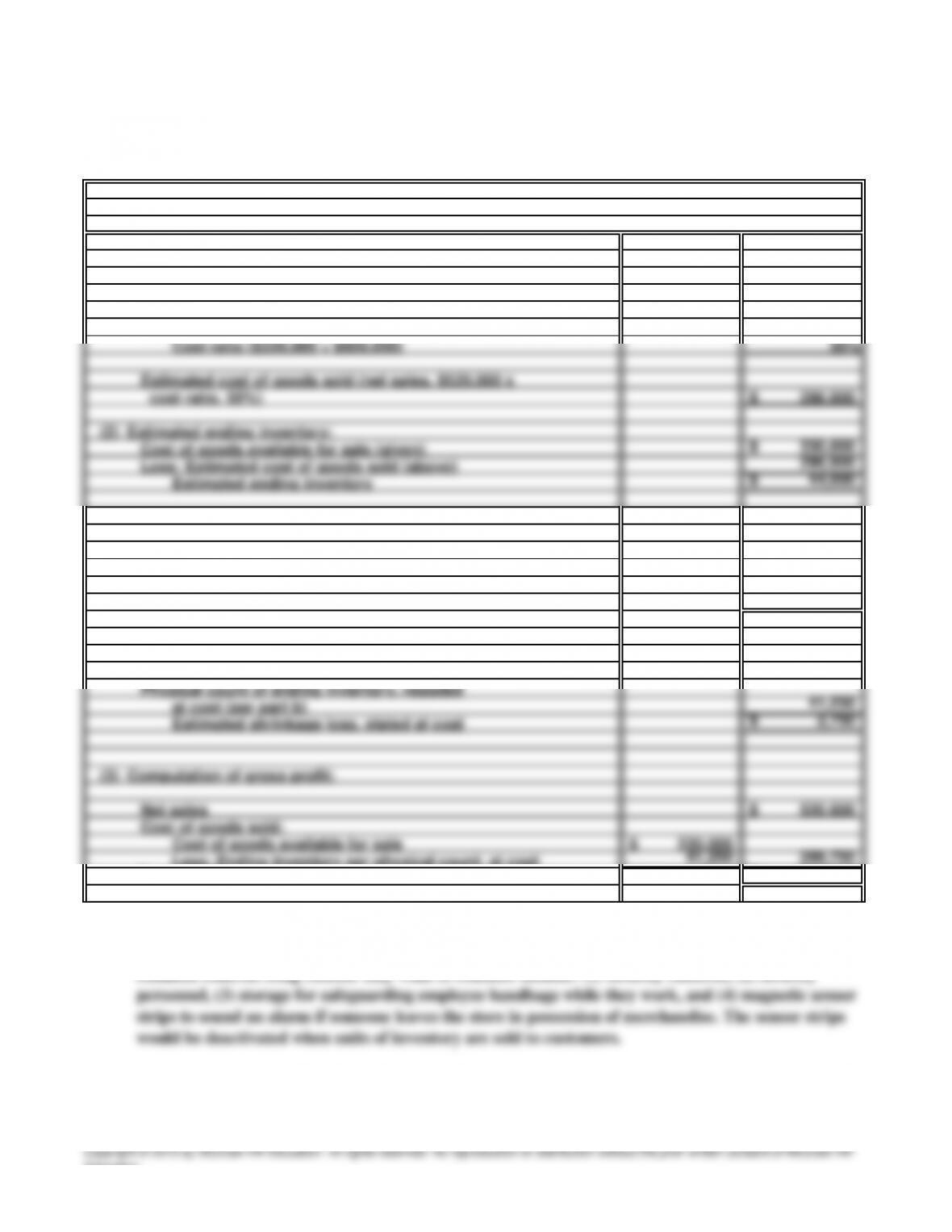

PROBLEM 8.7B

SONG MEISTE

R

(

1

)

Estimated cost of

g

oods sold:

Cost ratio for the current

y

ear:

Cost of

g

oods available for sale

Retail

p

rices of

g

oods available for sale

(

2

)

Estimated shrinka

g

e losses at cost:

Estimated endin

g

inventor

y

(p

er

p

art a

)

(

1

)

Restatin

g

p

h

y

sical inventor

y

from retail

p

rices to cost:

Ph

y

sical inventor

y

stated in retail

p

rices

CDs and recorded music in other formats can easily fit into someone’s pocket and “walk out of the

store.” Thus, it is important that effective controls be in place to reduce inventory shrinkage. Four

common controls Song Meister may want to consider include: (1) security cameras, (2) security

personnel, (3) storage for safeguarding employee handbags while they work, and (4) magnetic sensor

strips to sound an alarm if someone leaves the store in possession of merchandise. The sensor strips

would be deactivated when units of inventory are sold to customers.

Less: Endin

g

inventor

y

p

er

p

h

y

sical count

,

at cost

Education.

286

000

44

000

$

(

)

g

(g

)

(

g

y

20 Minutes, Strong

a. Computations based on LIFO valuation of inventory:

(1) Inventory turnover rate:

Cost of Goods Sold = 8,919$ 3.39 times

Average inventor

y

2,629$

Gross Profit = 4,066$ 31.3%

Net Sales 12,985$

b.

c.

You would ex

p

ect the ratios to be different under FIFO as follows:

Inventory turnover rate: Cost of goods sold lower, inventory higher, turnover lower

receivable being very low relative to its sales. This is explained by the fact that most of the

company’s sales are for cash or on bank credit cards which are quickly turned into cash for the

The company must have encountered increasing replacement costs for its merchandise during the

year.

PROBLEM 8.8B

J.C. Penne

y

Education.

30 Minutes, Strong

a.

b.

c.

SOLUTIONS TO CASES

OUR LITTLE SECRET

CASE 8.1

Lee confronts three related ethical issues. The first is that Our Little Secret’s past tax practices have

been both unethical and illegal. Lee should not be involved in such practices or, if she is in a position of

responsibility, allow them to continue.

Second, Lee has good reason to question the basic integrity of her prospective employer.

Is Frost’s statement that “no one knows how this all got started, or who was

responsible” really true? After all, Frost is suggesting that the fraud continue after Amy

accepts a position with Our Little Secret.

failing to report this income in prior years. Saying nothing and allowing the error to “flow through” is,

in essence, a scheme for evading these interest charges and penalties.

upon herself to notify the Internal Revenue Service or any other third party about the

company’s actions.

The solution proposed by Frost is unacceptable. To knowingly understate inventory in an income tax

A second course of action is to accept the position contingent upon the company agreeing to take

immediate steps to rectify the problem. This would include filing amended income tax returns for any

Third, there is the issue of confidentiality. Professionally accountants are ethically bound to treat as

Lee basically has two ethical courses of action to consider. First, she may decide that she does not wish

to associate herself with the company. Therefore, she simply may decline the job. If she chooses this

course, she should treat Frost’s disclosures during this interview as confidential information.

Education.

a.

b. (1) $188,000

28,000

If this sale can be delayed just two days , it will occur in 2016. Jackson Specialties then may use the

current $30 per-unit cost in determining the cost of this sale, regardless of when during 2016 the 8,000

units on order actually arrive. (The only limitation is that the year-end inventory must exceed the 5,000

units carried at the old acquisition costs.)

per unit, plus 2,000 units from Nov. 14, 1962 purchase at $6 per unit) ………………..

Note to instructor: Assuming a tax rate of 33%, this strategy could save the company more than $30,000 in

income taxes applicable to this sale. ($92,000 reduction in taxable gross profit x 33% = $30,360 tax savings.)

recent acquisition costs incurred during the fiscal year. If Jackson Specialties makes its 4,000-unit sale

on December 30, the cost of goods sold will be $120,000 only if the units on order arrive by year-end

(which is almost here). Otherwise, the cost of goods sold must be reported as only $28,000.

CASE 8.2

JACKSON SPECIALTIE

S

20 Minutes, Medium

Sales (4,000 units @ $47 per unit) ……………………………………………………..

While LIFO assigns old acquisition costs to inventory, it does not purport to coincide with the physical

movement of merchandise in and out of the business. Therefore, the units in inventory are not over 50

years old. In fact, they may have been purchased quite recently.

Gross profit if the units on order arrive before year-end:

Education.