Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

e.

Under FIFO, the cost of goods sold is based on the oldest costs. Thus, relative to using

LIFO, the FIFO method will result in higher net income during periods of rising prices,

Ex. 8.4 a.

b.

1. $125,000

2. taxes x 40%)…………………………………………………………

…

$44,000

LIFO results in a hi

g

her cost of

g

oods sold than does FIFO when the re

p

lacement costs of

merchandise are rising. Under LIFO, the most recent (higher) costs are assigned to the

Dollar amounts stated in thousands:

Income before income taxes (as re

p

orted under FIFO) …………….

Income taxes expense under LIFO ($110,000 income before

2. 5

,

250 5

,

250

Cash ………………………………………………………………

Sales …………………………………………………..

To recognize the sales revenue from the sale of 15 WordCrafter

programs @ $350, cash.

Ex. 8.7 a.

b.

Ex. 8.8 a. 2015 2014

350,000$ 250,000$

Correction of understatement of inventory at end of 2014 ……………

…

(40,000) 40,000

310,000$ 290,000$

Compute gross profit amounts and gross profit percentages

for each year based on corrected data:

b.

Average cost $796.00 (200 units @ $3.98). (Average cost = $4380/1,100 units =

$3.98

)

FIFO, $990.00 (190 units @ $5.00 + 10 unit @ $4.00).

Compute corrected net income figures:

Net income as reported ………………………………………………..

Net income as corrected ……………………………………………..

Ex. 8.9 a.

Be

g

innin

g

inventor

y

, Januar

y

1 ……………………………………… $ 50,000

Net

p

urchases, Januar

y

1–29 …………………………………………

…

80,000

a. 58%

$348,000

Ex. 8.11 No. A company may use different inventory methods for different types or segments of its

inventor

y

. With res

p

ect to inventories, the consistenc

y

p

rinci

p

le means that the method used

to value a particular type of inventory should not be changed from one year to the next.

Using different inventory methods for various parts of a company's inventory is a common

and generally accepted practice.

lower than it was in June. At June 30, the percentage was 60% ($300,000 $500,000).

During July, however, the percentage was only 55.5%, based upon Phillips’ purchases

($222,000 $400,000).

Estimated ending inventory (at cost):

would have had the actual inventory figure at January 29, making it unnecessary to

compute an estimated figure using the gross profit method.

Inventory at time of theft is $89,400, computed as follows:

Ex. 8.10 Cost ratio during July ($522,000 $900,000) …………………………………

Estimated cost of goods sold ($600,000 58%) ………………………………

Ex. 8.12 a. 1.

2.

4.

5.

6.

7.

Although Ford has reported less net income as a result of using LIFO for a portion of its

inventory, it actually is better off than if it had exclusively used FIFO. There are only two

differences in the company’s financial position that result from the flow assumption in use.

One is a difference in cash position. As explained above, Ford has made lower tax payments

and therefore retained more cash as a result of using LIFO. The second difference is the

amount of inventory presented as a current asset in the statement of financial position,

which is less due to using LIFO for part of its inventory.

The gross profit rate would have been higher had the company been using FIFO for its

Net income would have been higher using FIFO for the entire inventory for the same

The inventory turnover rate would have been lower had the company used FIFO for

the entire purchase. This rate is the cost of goods sold, divided by average inventory.

The accounts receivable turnover rate (net sales divided by average accounts

receivable) would be unaffected by the inventory flow assumption in use. A flow

Cash payments to suppliers are unaffected by the inventory flow

Net cash flow from operating activities would have been lower had the company used

FIFO for the entire inventory. The only cash flow affected by the inventory flow

assumption in use is income taxes. By recording a lower cost of goods sold, the use of

FIFO would have resulted in higher taxable income and, therefore, larger tax

payments.

Ex. 8.13 a.

Cost of Goods Sold = =$12,499 = 6.5 times

Average Inventory $1,936

b. Days in Year = =

Number of days required to sell the average amount of inventory:

Inventory turnover rate (dollar amounts in millions):

$12,499

($1,943 + $1,928) ÷ 2

Ex. 8.14* a.

c.

Inventory turnover:

The company was more efficient in managing its inventory in the year ended January 31,

2012. The inventory turnover in the most recent year was 8.05, compared to 8.23 in the

previous year. This resulted in an average number of days required to sell inventory

* Supplemental Topic , "LIFO Reserves."

Ex. 8.15 a.

(

1

)

$48

,

912

b.

(

1

)

365 da

y

s

78.5 da

y

s

Days in a year

Cost of sales year ended 2/3/13

Average days in inventory (365 ÷ 4.65)

Given an operating cycle of approximately 85 days, inventory accounts for approximately 92%

35 Minutes, Medium

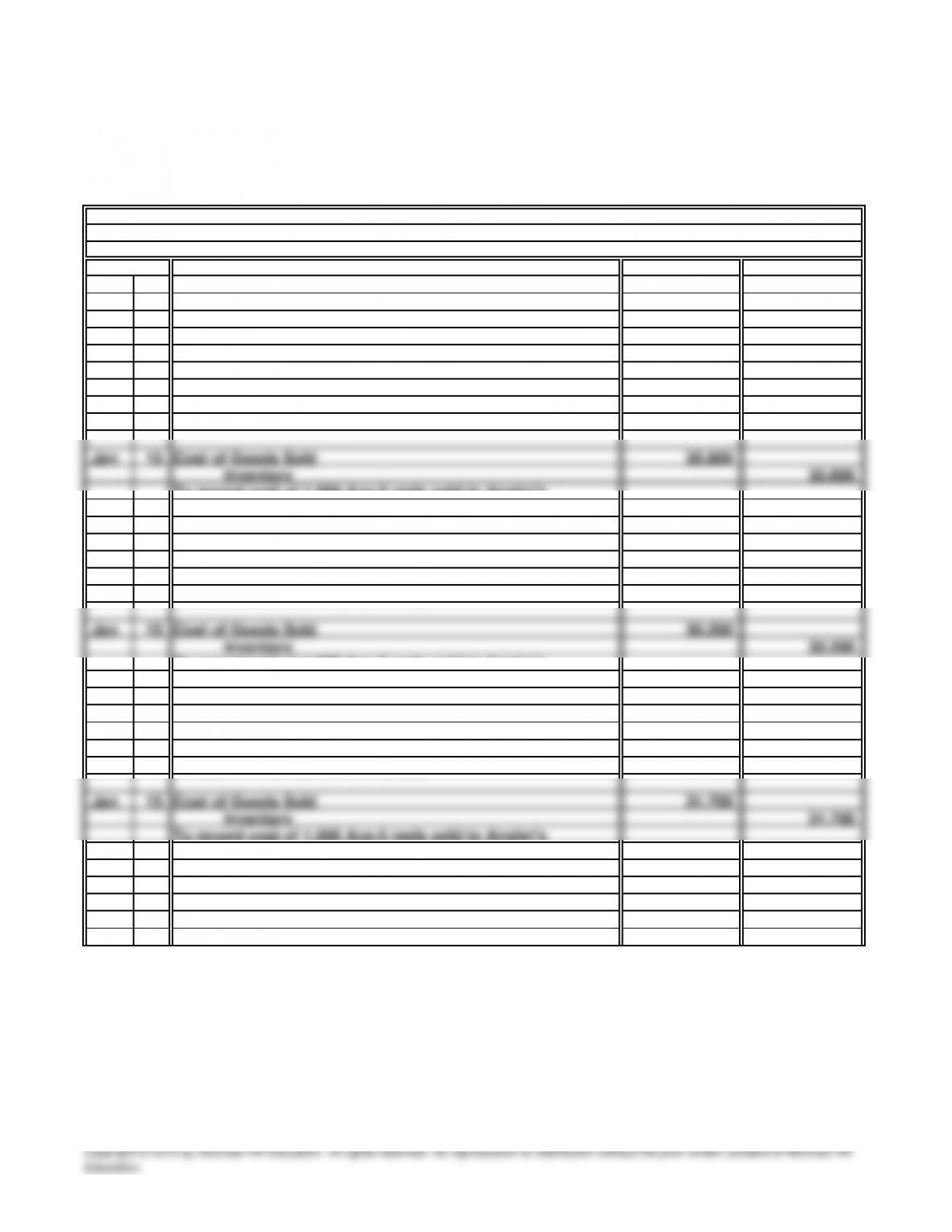

Jan 15 30

,

500

Inventor

y

30

,

500

units

@

$30.80

(

$46

,

200 total cost

,

divided b

y

1

,

500

assum

p

tion: 600 units

@

$29

,

p

lus 400 units

@

$32 = $30

,

200.

Warehouse. Cost determined b

y

the FIFO flow

assum

p

tion: 900 units

@

$32

,

p

lus 100 units

@

$29 = $31

,

700.

(

4

)

Last-in

,

First-out

(

LIFO

)

method:

To record cost of 1

,

000 Ace-5 reels sold to An

g

ler's

Warehouse. Cost determined b

y

the LIFO flow

SOLUTIONS TO PROBLEM SET

A

PROBLEM 8.1

A

SPORTS WORLD

Cost of Goods Sold

a.

2015

General Journal

(1) Specific identification method:

To record cost of 1

,

000 Ace-5 reels sold to An

g

ler's

To record cost of 1

,

000 Ace-5 reels sold to An

g

ler's

units

)

.

Warehouse: 500 units

@

$29

;

500 units

@

$32.

(

3

)

First-in

,

First-out

(

FIFO

)

method:

Warehouse b

y

the avera

g

e-cost method: 1

,

000

To record cost of 1

,

000 Ace-5 reels sold to An

g

ler's

(

2

)

Avera

g

e-cost method: