20 Minutes, Medium

Nov

1

30,000

Accounts Receivable (Sampson Co.)

30,000

Dec

31

600

Interest Revenue

600

Aug.

1

32,700

Notes Receivable

30,000

Interest Revenue

2,100

Interest Receivable

600

b.

Aug.

1

32,700

Notes Receivable

30,000

Interest Receivable

600

Interest Revenue

2,100

c.

Accounts Receivable (Sampson Co.)

Assuming that note was defaulted.

defaulted note.

There are two reasons why the company adopts this policy: (1) The interest earned on the

note compensates the company for delaying the collection of cash beyond the standard due

PROBLEM 7.6B

a.

General Journal

MIDTOWN DISTRIBUTION

account receivable due today.

Notes Receivable

Accepted a 9-month, 12% note in settlement of an

Interest Receivable

To accrue interest for two months (November

was earned in current year).

20 Minutes, Medium

a.

Dec 31 125

2

,

350 962

Cash 3

,

437

,

c.

31 360

Interest Revenue 360

d.

e.

Bank Reconciliation

Office Su

pp

lies

PROBLEM 7.7B

General Journal

DATA MANAGEMENT, INC

.

Bank Service Char

g

es

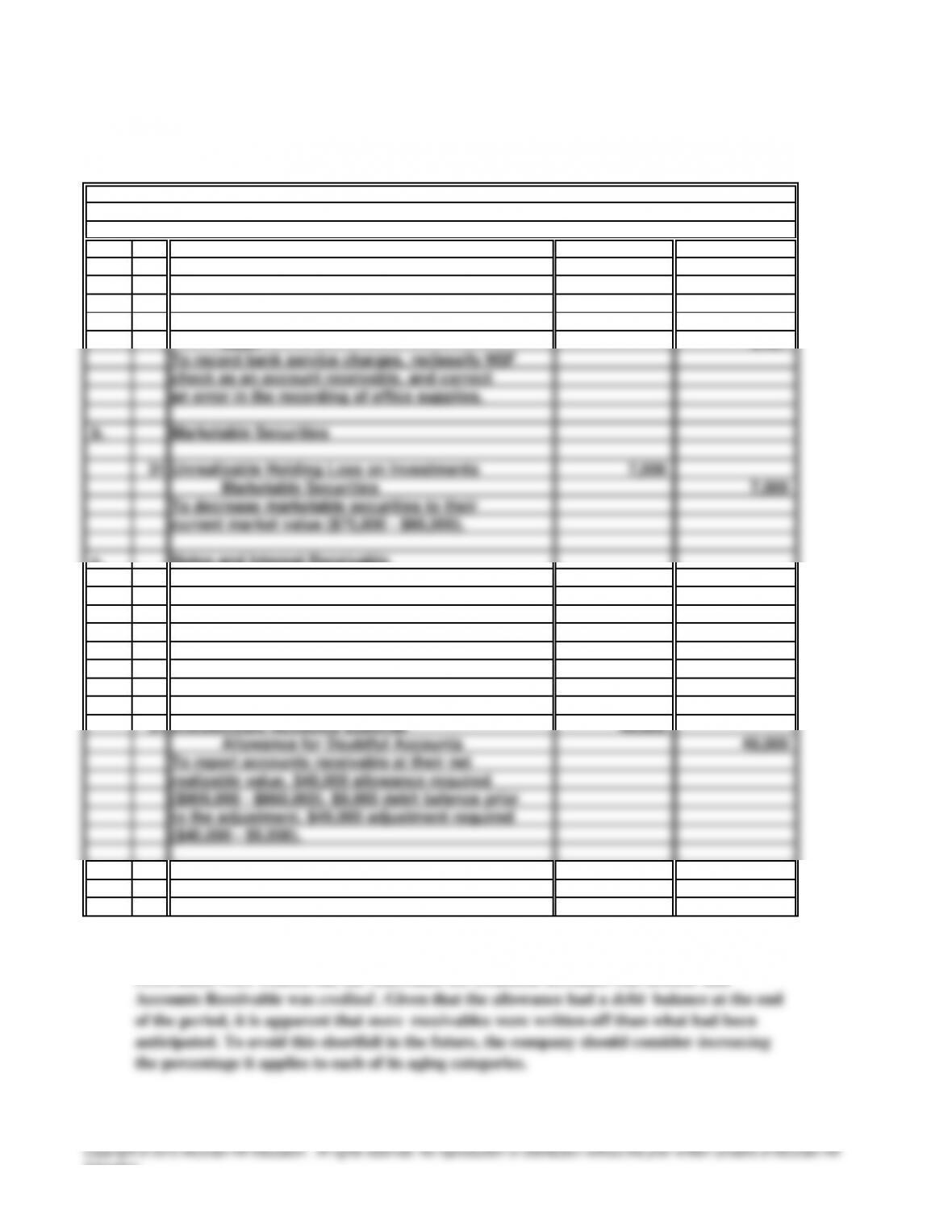

Accounts Receivable

In the prior period the company had established what it thought to be a reasonable credit

balance in the Allowance for Doubtful Accounts. Throughout the current period, as

receivables were written-off, the Allowance for Doubtful Accounts was debited and

Accounts Receivable at Net Realizable Value

Notes and Interest Receivable

Interest Receivable

To record accrued interest revenue on notes

receivable

(

$72,000 x 6% x 1/12

)

.

(

$900,000 – $860,000

)

. $9,000 debit balance

p

rior

to the ad

j

ustment. $49,000 ad

j

ustment re

q

uired

(

$40,000 – $9,000

)

.

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

,

40 Minutes, Strong

a.

General

Bank Statement

Ledger Balance

Balance

112,000

$

104,100

$

16,800

(12,400)

(100)

(2,500)

(900)

108,500

$

108,500

$

100

2,500

900

Cash

3,500

Money market accounts

150,000

$

High-grade, 60-day, commercial paper

5,000

Total cash equivalents

155,000

$

Total cash (from part a)

108,500

Cash and cash equivalents at 12/31/15

263,500

$

135

Interest Revenue

135

PROBLEM 7.8B

NSF check returned (Needham Company)

CIAVARELLA CORPORATION

Bank service charge

Preadjustment balances, 12/31/15

Outstanding Checks

Deposits in Transit

Accounts Receivable (Needham Company)

Computer Equipment

Error correction check #550

Bank Service Charge

The necessary entry to update the general

ledger is as follows:

Adjusted cash balance, 12/31/15

d.

540,000

$

(14,000)

(5,252,500)

6,480,000

2,500

1,756,000

$

12,000

$

(14,000)

64,800

62,800

1,693,200

$

e.

263,500

$

245,000

18,000

135

1,693,200

2,219,835

$

Cash and cash equivalents (part b.)

Marketable securities (at FMV, not cost)

Notes receivable (from Ritter Industries)

Interest receivable (part c.)

PROBLEM 7.8B

Accounts receivable written off during 2015

CIAVARELLA CORPORATION

Accounts receivable balance January 1, 2015

(continued)

Collections on account during 2015

Credit sales made during 20115

Reinstating Needham Company’s account

December 31, 2015

at December 31, 2015

Net realizable value of accounts receivable

Allowance for doubtful accounts balance

f.

December 31, 2015

January 1, 2015

1,756,000

$

540,000

$

62,800

12,000

1,693,200

$

528,000

$

6,480,000

$

5.83

times

62.61

days

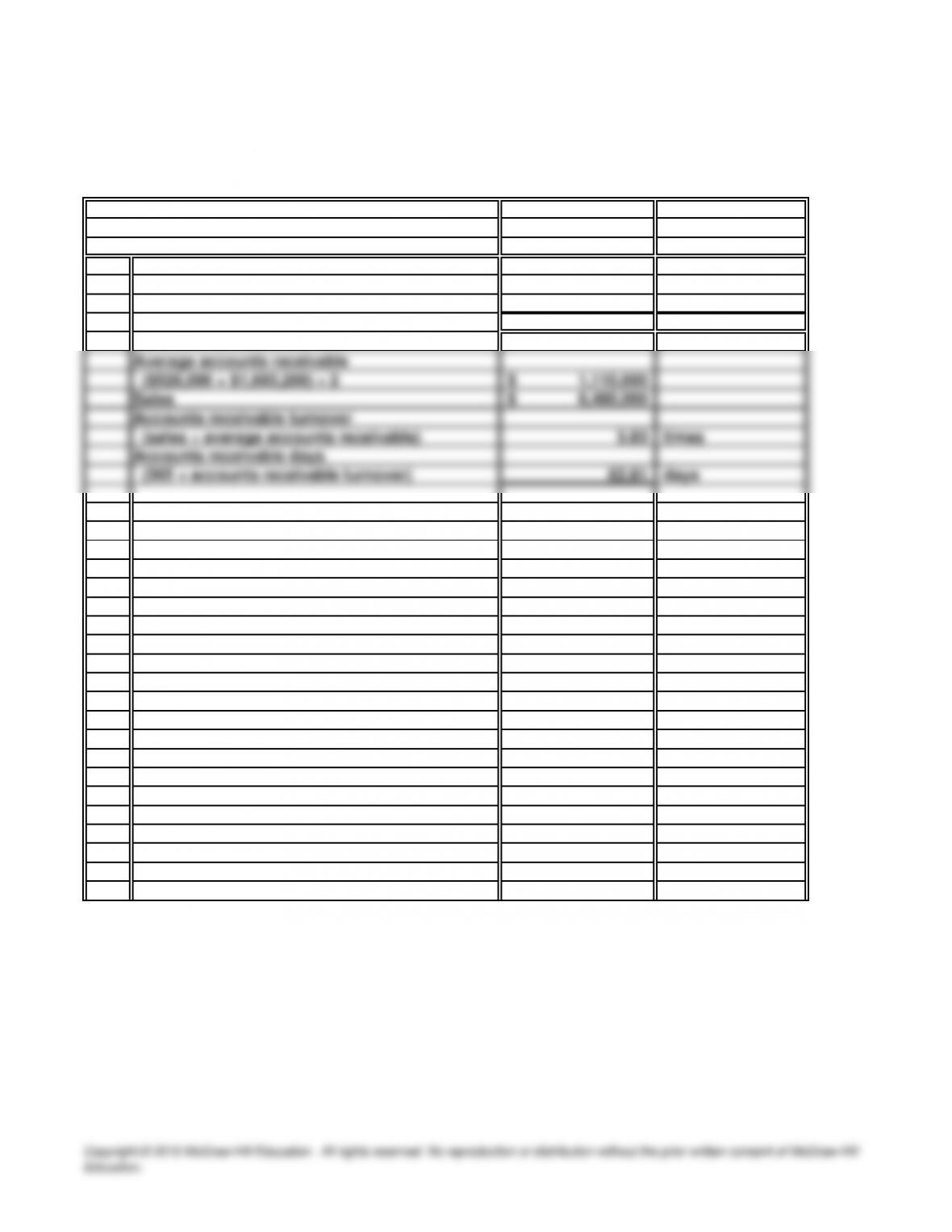

PROBLEM 7.8B

Allowance for doubtful accounts (part d.)

CIAVARELLA CORPORATION

Accounts receivable (part d.)

(concluded)

Net realizable value

(sales ÷ average accounts receivable)

Accounts receivable turnover

Ciavarella Corporation is slightly worse

than the industry average.

If the industry average is 60 days,

a.

CASE 7.1

ACCOUNTING PRINCIPLES

20 Minutes, Medium

This practice violates the matching principle. The expense relating to uncollectible accounts

is not recorded until long after the related sales revenue has been recognized. The distortion

40 Minutes, Strong

a.

b.

c.

CASE 7.2

ROCK, INC.

It is logical and predictable that the Double Zero policy—which calls for no down payment

and allows customers 12 months to pay—will cause an increase in sales. It also is predictable

that implementation of the Double Zero plan will cause cash receipts from customers to

recognition of uncollectible accounts expense to future periods. Therefore, the bookkeeper’s

measurement of net income in the latest month ignores entirely what may be a major expense

associated with sales of Double Zero accounts.

The uncollectible accounts expense has dropped to zero only because the company uses the

direct write-off method and the Double Zero plan has just begun. It is too early for specific

larger dollar amount of accounts receivable and the nature of these accounts.

The reduction in cash receipts should be temporary. Under the old 30-day account plan, the

company was collecting approximately all of its sales within 30 days, and cash collections

were approximately equal to monthly sales. With the Double Zero accounts, however, only

Education.

d.

e.

CASE 7.2

ROCK, INC.

(

concluded

)

The Double Zero receivables generate no revenue after the date of sale. Hence, they represent

resources that are “tied up” for up to 12 months without earning any return. As the company

Several means exist for a company to turn its accounts receivable into cash more quickly

than the normal turnover period. One approach is to offer credit customers cash discounts to

40 Minutes, Strong

a. 1.

2.

3.

4.

5.

6.

(1)

the users of its financial statements.

There is certainly nothing improper or unethical about offering customers a discount for

prompt payment, but an interesting accounting issue arises. A 10% discount is quite

Note to instructor: Few companies encounter bad debts of anywhere near 10% of

receivables. Therefore, the allowance for sales discounts might well be the larger of the

two allowances.

The need for an allowance for doubtful accounts is not based upon whether these

accounts are officially “overdue,” but whether they are collectible. The grace period is

CASE 7.3

ETHICS, FRAUD & CORPORATE GOVERNANC

E

WINDOW DRESSING

Inventory is not a financial asset. Generally accepted accounting principles call for

Combining all forms of cash, cash equivalents, and compensating balances under a single

caption is quite acceptable. In fact, it is common practice. But unused lines of credit are

balance sheet.

Having officers repay their loans at year-end only to renew them several days later is a

sham transaction. Its only purpose is to deceive the users of the financial statements. It

It is appropriate to report marketable securities at their current market value. Thus,

This situation poses two questions: (1) The valuation of inventory in conformity with

generally accepted accounting principles, and (2) whether Affections can depart from

generally accepted accounting principles in its reporting to creditors.

7.

b.

CASE 7.3

WINDOW DRESSING (continued)

Although these funds might actually be included in both year-end bank statements, they

are not really available to the company in both bank accounts. Thus, this check should be

included as an outstanding check in the year-end bank reconciliation of the account upon

There is nothing unethical about holding the meeting. Taking legitimate steps to “put the

company’s best foot forward” is both an ethical and widespread practice. In fact, any

Unless they clearly are told otherwise, users of financial statements reasonably may

assume that financial statements are based upon GAAP. If Affections departs from

GAAP and shows its inventory at current sales value, it must take appropriate steps to

make the users of the statements fully aware of this departure from GAAP.

inflated bank balances, then withdraws the funds from both banks and runs.

No time estimate, Medium

This assignment is based upon financial information that is continually updated. Thus, we are

unable to provide the same responses as students.

Note to instructor: It is important that students be guided to discover the wide range of cash

equivalent investment vehicles available to businesses, and the variation in the interest rates they

yield. It is also important that they consider the potential financial impact of selecting a cash

BANKRATE.COM

CASE 7.4

INTERNET