B. Ex. 3.8 a.

b.

c.

d.

e.

B. Ex. 3.9

B. Ex. 3.10

Gasoline purchased is an expense because it is ordinarily used up in the current

generating revenue.

Payment to an employee for services rendered in March is a March expense. Such a

The payment to the attorney for services rendered in a prior period reduced an

expense.

The purchase of a copying machine does not represent an expense. The asset Cash is

exchanged for the asset Office Equipment, without any change in owners’ equity.

The dividend does not constitute an expense. Unlike payments for advertising, rent,

Revenue is recognized when it is earned, not necessarily when cash is received.

Thus, the airline will recognize revenue of $3,000,000 in its October income

Expenses are recognized when they are incurred, not necessarily when cash is paid.

Ex. 3.1 a.

b.

h.

Ex. 3.2 a.

1,000$

2,100

100

…

…

…

b.

Insurance ……………………………………………………………………

…

Gasoline (15,000 miles at 30 mpg. = $4.20/gal.) ……………………………

…

Expenses

Costs of owning and operating an automobile (estimates will vary; the following list is

only an example):

SOLUTIONS TO EXERCISES

Accounting period

Accounting cycle

Registration and license ……………………………………………………

…

Note to instructor: Most employers do base their reimbursement of driving expenses on an average

cost per mile. You may want to point out that the incremental costs of this trip are much less than the

average cost. Thus, employees usually benefit somewhat in the short-term when they are reimbursed

for using their own cars.

Although you spent no money during this trip, you incurred significant costs. For

example, you have used much of the gasoline in your tank. Also, the more miles you

drive, the higher your repair and maintenance costs, depreciation, and insurance.

Assuming that it cost you about 34 cents per mile to own and operate your vehicle,

about $34 would be a reasonable estimate of your “driving expenses.”

*Note to instructor: It is worth noting that including both depreciation and the “principal” portion of

the car loan would be “double-counting” the purchase price of the car. Depreciation issues are

introduced in Chapter 4.

Ex. 3.3 Nov. 1 120,000

120,000

870,000

15 3,200

3,200

…

…

Cash ……………………………………………………

…

Capital Stock ……………………………

…

Office Equipment ………………………………………

…

Accounts Payable ………………………

…

Issued stock in exchange for cash.

Land ……………………………………………………

…

and issuing a note payable for the remaining balance.

Purchased office equipment on account.

Ex. 3.5 a.

billion

Ex. 3.6

Revenue Expenses = Assets Liabilities =

INEII NEI

Ex. 3.7

a.

Revenue Expenses = Assets Liabilities =

NE I D NE I D

INEII NEI

NE NE NE D NE D

b. 1.

2.

7.

8.

Owners’

Equity

Balance Sheet

Balance Sheet

1.

Income Statement Net

Income

Owners’

Equity

Liabilities at the beginning of the year: $116.4 billion – $76.6 billion = $39.8 billion

41.0$

Net income ……………………………….

2.

Trans-

action

3.

Trans-

action

Paid an outstanding account payable.

Incurred wages expense to be paid at a later date.

Earned revenue to be collected at a later date.

Purchased tools and equipment by paying part in cash and issuing a note payable for the

remaining balance.

1.

Net

Income

Income Statement

Ex. 3.8 a. Apr. 5 Accounts Receivable …………………………… 11,000

May 17 Dividends ………………………………………. 2,000

June 10 Accounts Payable ……………………………… 4,500

Cash ……………………………………. 4,500

June 25 2,000

Cash ……………………………………. 2,000

b.

Dividends Payable ……………………………..

Paid cash dividend declared May 17.

payment due in 30 days.

Construction for bill sent April 5.

The following transactions will not cause a change in net income.

May 17: Declaration of a cash dividend.

Ex. 3.9 Transaction Net Income Assets Liabilities Equity

a. NE I NE I

b. NE I I NE

c. DNE I D

g

. NENENENE

h. NE NE NE NE

Ex. 3.10 a. May 3 Cash……………………………………………. 950,000

Capital Stock……………………………. 950,000

4 Office Rent Expense…………………………….. 1,800

20 120,000

Client Revenue……………………….. 120,000

26 8,000

Dividends Payable……………………… 8,000

31 32,000

Cash…………………………………… 32,000

May 20.

Salary Expense…………………………………

Paid salary expense incurred in May.

Dividends……………………………………….

Declared dividend to be distributed in June.

Accounts Receivable…………………………

Billed clients for services on account.

Issued capital stock for $950,000.

Purchased a company car. Paid $15,000 cash and

issued a $30,000 note payable for the balance.

Education.

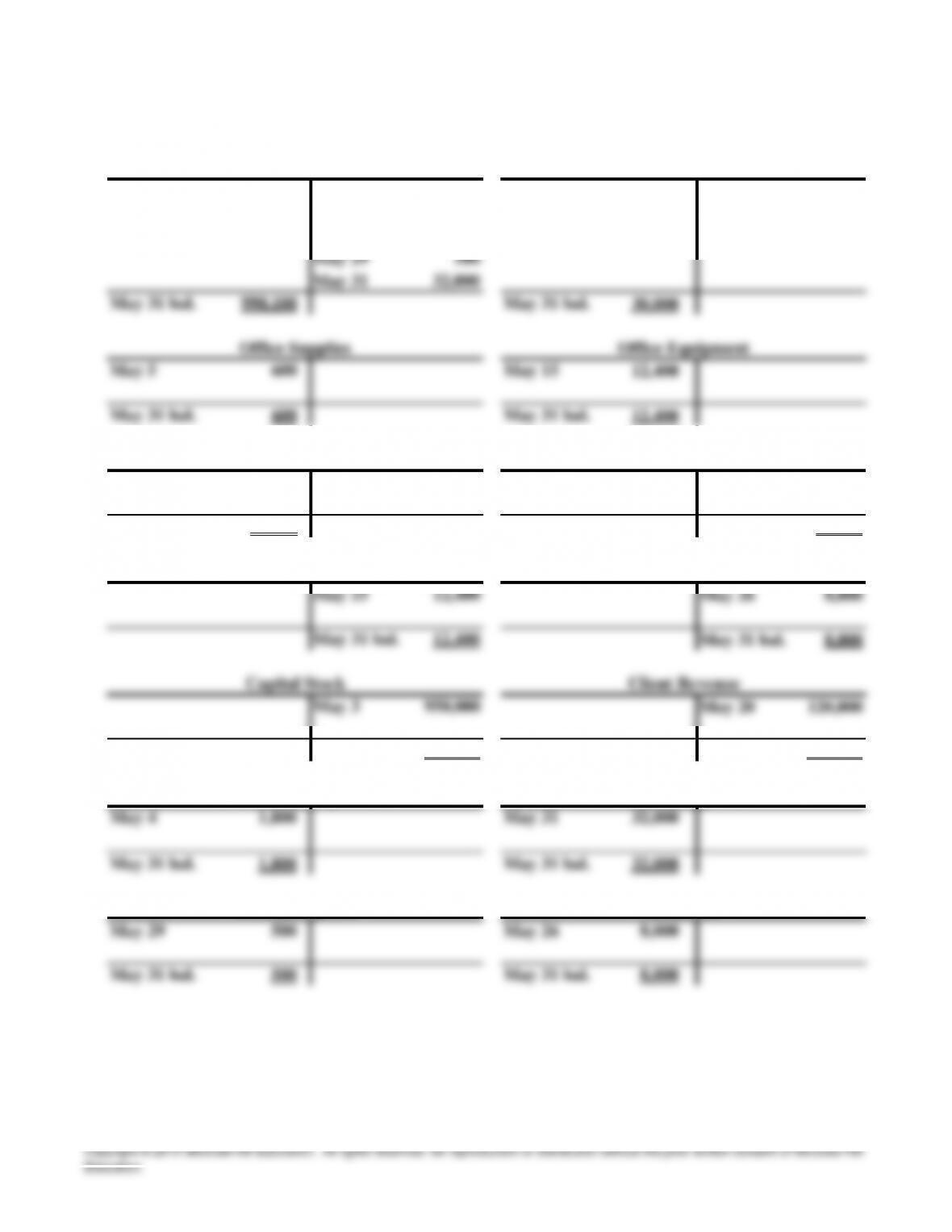

b. Cash

May 3 950,000 May 4 1,800 May 20 120,000 May 30 90,000

May 30 90,000 May 5 600

May 18 15,000

Vehicles Notes Payable

May 18 45,000 May 18 30,000

May 31 bal. 45,000 May 31 bal. 30,000

Accounts Payable Dividends Payable

May 31 bal. 950,000 May 31 bal. 120,000

Office Rent Expense Salary Expense

Utilities Expense Dividends

Accounts Receivable

c.

Janet Enterprises Incorporated

Trial Balance

May 31, 2015

Debit Credit

Cash……………………………………. 990,100$

Accounts receivable……………………

…

30,000

Office supplies………………………… 600

Office equipment……………………… 12,400

Vehicles……………………………….. 45,000

Notes payable…………………………. 30,000$

Accounts payable………………………. 12,400

Dividends payable…………………….. 8,000

Ex. 3.11 a. Sep. 2 Cash……………………………………………. 975,000

Capital Stock……………………………. 975,000

4 Land……………………………………………… 200,000

700,000

Cash ……………………………………. 100,000

29 60,000

Cash……………….…………………… 60,000

30 110,000

Accounts Receivable…………………… 110,000

Issued capital stock for $975,000.

Building…………………………………………..

Cash……………………………………………

Salary Expense…………………………………

Recorded and paid salary expense.

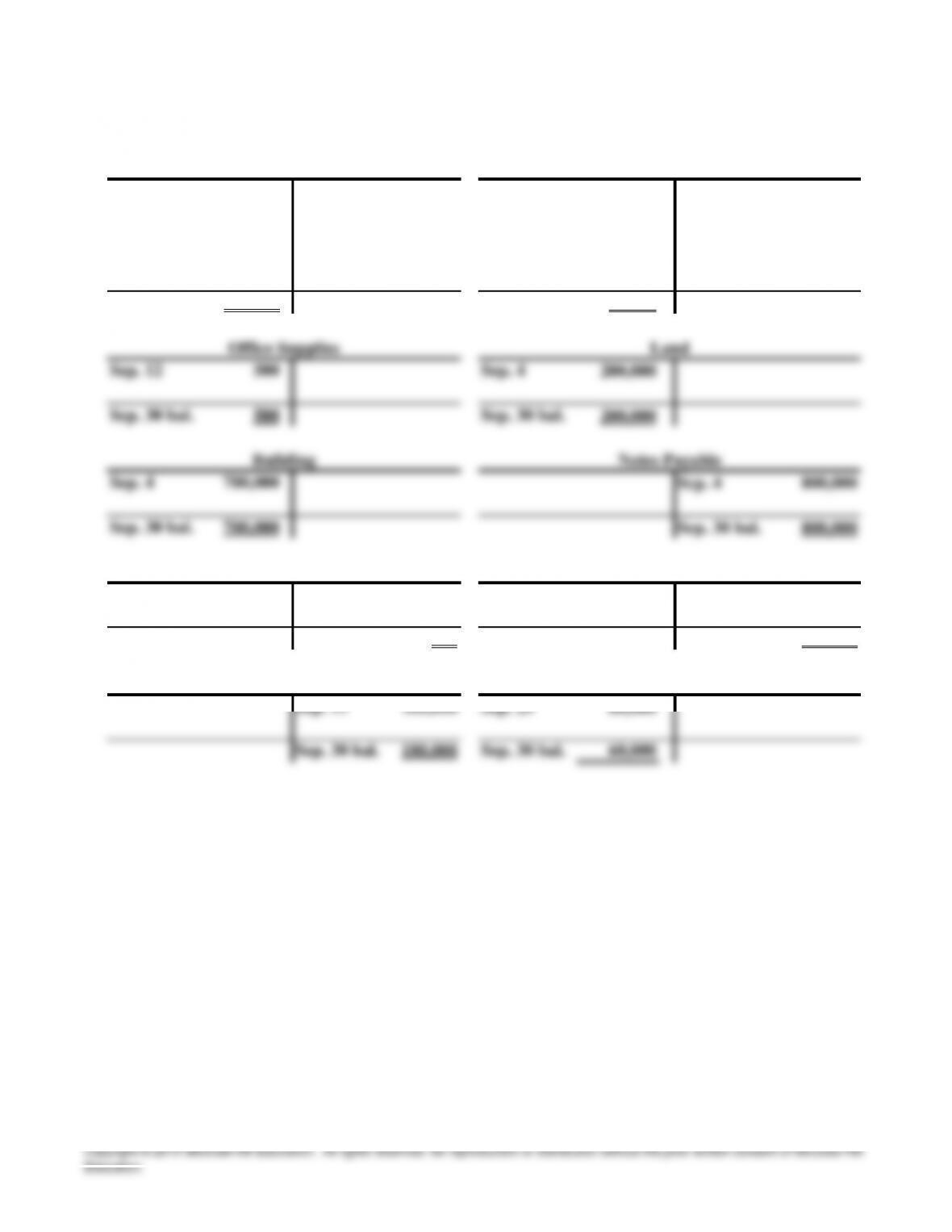

b. Cash

Sep. 2 975,000 Sep. 4 100,000 Sep. 19 180,000 Sep. 30 110,000

Sep. 30 110,000 Sep. 29 60,000

Sep. 30 bal. 925,000 Sep. 30 bal. 70,000

Accounts Payable Capital Stock

Sep. 12 500 Sep. 2 975,000

Sep. 30 bal. 500 Sep. 30 bal. 975,000

Client Revenue Salary Expense

Accounts Receivable