Ex. 2.1 a. 1.

2.

SOLUTIONS TO EXERCISE

S

Assets are economic resources owned by the business entity.

Among the assets of American Airlines we might expect to find

investments, accounts receivable (say, from travel agents), fuel (in

Among the assets of a professional sports team are investments (in stocks and

bonds), notes receivable (often from players), training equipment, supplies, and

$36,300 Liabilities:

56,700 Notes payable ………………………

…

$207,000

12,400 Accounts payable ……………………

…

43,800

210,000 $250,800

90,000 Owners’ equity:

Capital stock …………………………

…

88,000

Balance Sheet

December 31, 2011

Total liabilities………………………

…

Liabilities & Owners’ Equity

Cash ………………………

…

Ex. 2.3 KINER COMPANY

Assets

Accounts receivable ………

…

Office Equipment …………

…

Building …………………….

.

Land…………….

Ex. 2.6 Assets = Liabilities + Owners’

II NE

NE* NE NE

DD NE

DD NE

INE I

II NE

INE I

NE* NE NE

NE* NE NE

Ex. 2.7

a.

b.

c.

d.

e.

$ 240,000

…

…

(2) Partners’ equity:

f

g

h

i

Note to instructor: These are examples, but many others exist.

Transaction

a

b

c

d

e

Johanna Spencer, capital …………………………………………

…

*Could be I/D offsetting

The purchase of office equipment (or any other asset) on credit will cause an increase

The cash payment of an account payable or note payable will cause a decrease in the

The collection of an account receivable will cause an increase in one asset (cash) and

The investment of cash in the business by the owners will cause an increase in an

The purchase of an automobile (or other asset) paying part of the cost in cash and

*$850,000 in assets $460,000 in liabilities = $390,000.

Ex. 2.9 a.

Ex. 2.10 a.

b.

The situations encountered in the practice of accounting and auditing are too

complex and too varied for all specific answers to be set forth in a body of official

Accountants must rely on their professional judgment in such matters as

determining (three required) (1) how to record an unusual transaction that is not

discussed in accounting literature, (2) whether or not a specific situation requires

disclosure, (3) what information will be most useful to specific decision makers, (4)

how an accounting system should be designed to operate most efficiently, (5) the

audit procedures necessary in a given situation, (6) what constitutes a fair

presentation of financial information, (7) whether specific actions are ethical and

are in keeping with the accountants’ responsibilities to serve the public interests.

amounts originally invested in the business by the owners, but says nothing about

the form in which the company now holds these resources—nor even whether the

resources are still on hand. Thus, the capital stock account has no direct effect upon

liquidity. On the other hand, the amount of the owners’ equity, related to the

amount of the liabilities is an important factor in evaluating liquidity.

of loans to the business. If the business is a partnership, all of the partners are

personally liable for the company’s debts.

On the other hand, if Spencer is organized as a corporation, a lender may look only

to the cor

p

orate entit

y

for

p

a

y

ment.

Note to instructor: You may wish to point out that some lenders would not make sizable loans to a

small corporation unless one or more of the stockholders personally guaranteed the loan. This is

accomplished by having the stockholder(s) cosign the note.

Cash is the most liquid of all assets. In fact, companies must use cash in paying most

bills. Therefore, cash contributes more to a company’s liquidity than any other

asset.

Cash received from revenues ………………………………

…

Cash paid for expenses ……………………………………

…

Cash flows from financing activities:

Cash received from sale of capital stock …………………

…

Ex. 2.11 WELLER COMPANY

Statement of Cash Flows

For the Month Ended October 31, 2015

Cash flows from operating activities: 12,000$ (7,600)

$

7,500$

17,000$ (7,800) 9,200

Statement of Cash Flows

For the Month Ended August 31, 2015

Ex. 2.14

Cash received from revenues ………………………………

…

Cash paid for expenses ………………………………………

Net cash provided by operating activities …………………

…

Cash flows from operating activities:

Cash flows from investing activities:

PRESTWICK COMPANY

Ex. 2.15

Ste

p

s to Window Dress

Impact on Financial Statements*

BS—Higher cash balance

IS—No impact

SCF—Higher cash from operating activities

Delay cash payment of expenses

at year-end (assume expense

alread

y

incurred

)

Note to instructor: Many examples of steps to improve the financial statements could

be cited. The ones listed below are those that the authors believe are most likely to be

identified b

y

students.

Ex. 2.16 a.

b. End

Home Depot reports a net income (earnings) of $4,535 million for the year ended

Februar

y

3, 2013.

Cash balances at the beginning and end of the year were:

a.

Liabilities & Owners’ Equity

Cash 31,400$ Liabilities:

Accounts receivable 10,600 Accounts payable 54,800$

Furnishings 58,700 Salaries payable 33,500

Equipment 39,200 Interest payable 12,000

Snowmobiles 15,400 Notes payable 620,000

Buildings 500,000 720,300$

Land 425,000 Owners’ equity:

(1) Computed as total assets, $1,080,300, less total liabilities, $720,300, less capital stock,

$ 135,000.

b.

SOLUTIONS TO PROBLEMS SET

A

PROBLEM 2.1

A

ROCKY MOUNTAIN LODG

E

15 Minutes, Easy

Assets

ROCKY MOUNTAIN LODGE

Balance Sheet

December 31, 2015

The balance sheet indicates that Rocky Mountain Lodge is in a weak financial position.

The highly liquid assets—cash and receivables—total only $42,000, but the company has

15 Minutes, Easy

a.

b.

PROBLEM 2.2

A

MEMPHIS MOVING COMPAN

Y

Received $900 cash from collection of accounts receivable.

Purchased equipment for cash at a cost of $3,200.

Description of transactions:

Education.

15 Minutes, Medium

Owners’

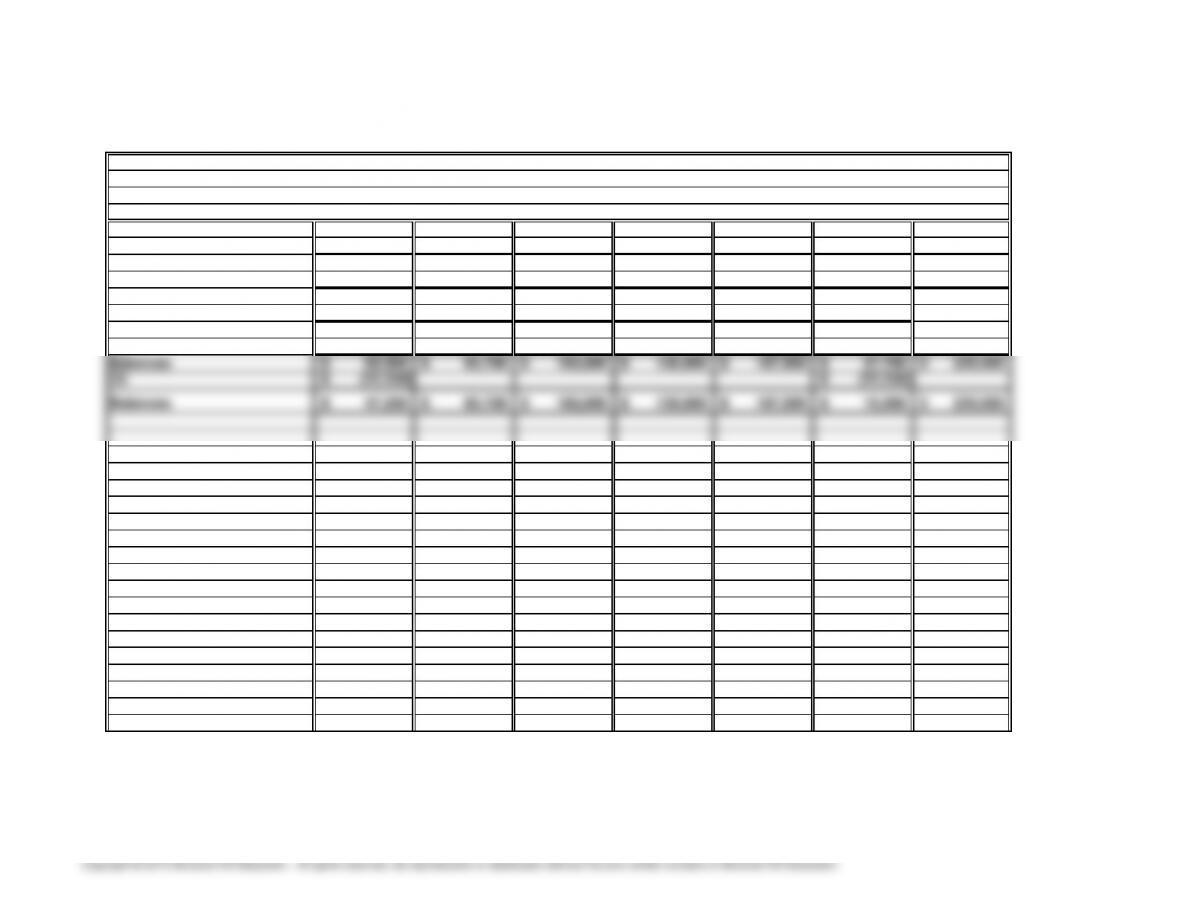

Assets = Equity

Office Notes

A

ccounts Capital

Cash + Equipment

+

Building + Land = Payable + Payable + Stock

December 31 balances 37,000$ 51,250$ 125,000$ 95,000$ 80,000$ 28,250$ 200,000$

(1) 35,000 35,000

Balances 72,000$ 51,250$ 125,000$ 95,000$ 80,000$ 28,250$ 235,000$

(2) (22,500) 55,000 35,000 67,500

Balances 49,500$ 51,250$ 180,000$ 130,000$ 147,500$ 28,250$ 235,000$

(3) 9,500 9,500

Balances 49,500$ 60,750$ 180,000$ 130,000$ 147,500$ 37,750$ 235,000$

(4) 20,000 20,000

MAXWELL COMMUNICATION

S

Liabilities +

PROBLEM 2.3

A

$

$