Chapter 13 – Statement of Cash Flows

13 STATEMENT OF CASH FLOWS

Chapter Summary

The statement of cash ows was introduced in Chapter 1. This chapter

begins by reviewing the purpose of the statement. Its usefulness to creditors

and investors in evaluating solvency is emphasized from the outset. The

classification of cash transactions into operating, investing, and financing

activities is explained in full. This section includes an explanation of the

reasoning behind the classification of interest receipts, interest payments,

and dividend receipts as operating activities. We also take the opportunity at

the outset to highlight the importance of cash ows from operating activities.

The approach to preparing the statement centers on analyzing the

income statement and the associated changes in noncash balance sheet

accounts. The approach is introduced using a simple illustration based on

changes in the balance of the marketable securities account. We then apply

this methodology to an example that develops the entire statement.

The direct method is used to compute cash ows from operating

activities. Discussion of the indirect method is also presented. Either or both

methods may be chosen at the option of the instructor.

The analysis of ows from investing and financing activities is

somewhat simpler than that for operating activities and the coverage is as a

result relatively brief.

The chapter concludes with a detailed discussion of the use of the SCF

in developing strategies to manage cash ows. Emphasis here is on the use

of the accounting information by internal management rather than investors

and creditors external to the firm.

Learning Objectives

1. Explain the purposes and uses of a statement of cash ows.

2. Describe how cash transactions are classified in a statement of cash

ows.

3. Compute the major cash ows relating to operating activities.

4. Compute the cash ows relating to investing and financing activities.

5. Distinguish between the direct and indirect methods of reporting

operating cash ows.

6. Explain why net income differ from net cash ows from operating

activities.

7. Compute net cash ows from operating activities using the indirect

method.

8. Discuss the likely effect of various business strategies on cash ows.

9. Explain how a worksheet may be helpful in preparing a statement of

cash ows.

Brief topical outline

AStatement of cash flows

1Purposes of the statement

2Example of a statement of cash flows – See Exhibit 13-1 (page 567)

3Classification of cash flows

aOperating activities

bInvesting activities

cFinancing activities

dWhy are receipts and payments of interest classified as operating

activities? – see Case in Point (page 568)

eCash and cash equivalents

fCash versus accrual information

BPreparing a statement of cash flows

1Operating activities

2Investing activities

3Financing activities

4Cash and cash equivalents

5Cash flows from operating activities

aCash received from customers

bInterest and dividends received

6Cash payments for merchandise and for expenses

aCash paid for purchases of merchandise

bCash payments for expenses

cCash paid to suppliers and employees

dCash payments for interest and taxes

eA quick review

7Cash flows from investing activities

aPurchases and sales of securities

bLoans made and collected – see Your Turn (page 576)

cCash paid to acquire plant assets

dProceeds from sales of plant assets

eA quick review

8Cash flows from financing activities

aShort-term borrowing transactions

bProceeds from issuing bonds payable and capital stock

cCash dividends paid to stockholders

dA quick review

9Relationship between the statement of cash flows and the balance sheet – see

Case in Point (page 579)

10 Reporting operating cash flows by the indirect method

aReconciling net income with net cash flows

bThe indirect method: a summary

cIndirect method may be required in a supplementary schedule

dThe statement of cash flows: a second look

CFinancial analysis and decision making

1Free cash flow – see Your Turn (page 584)

DManaging cash flows

1Budgeting: the primary cash management tool

2What priority should managers give to increasing net cash flows?

aShort-term results versus long-term growth

bOne-time boosts to cash flows

3 Some strategies for permanent improvements in cash flow

a Deferring income taxes

bPeak pricing

cDevelop an effective product mix – see Ethics, Fraud & Corporate

Governance (page 587)

EA worksheet for preparing a statement of cash flows

1Data for an illustration

aAdditional information

2The worksheet

aEntries in the middle column

3Entry

FConcluding remarks

Topical coverage and suggested assignment

Homework Assignment

(To Be Completed Prior to Class)

Class

Meetings on

Chapter

Topical

Outline

Coverage

Discussion

Questions

Brief

Exercises Exercises Problems

Critical

Thinking

Cases

1 A 1, 2, 3, 1, 3 1, 5 1, 6

2 B 6, 7, 8 5, 6 2, 4 2, 3 2

3 C – F 11, 13, 15 9 8, 9, 10 7, 8

Comments and observations

Teaching objectives for Chapter 13

In presenting the statement of cash flows, our teaching objectives are to:

1Explain the content and usefulness of this financial statement.

Financial Accounting, 16e 13- 3

2Provide a brief history of this financial statement, distinguishing it from the statement of

changes in financial position and emphasizing the need for information regarding cash flows

in this era of corporate “takeovers.”

3Describe the major classifications within the statement of cash flows. Emphasize the

relative importance of the net cash flow from operating activities.

4Briefly explain why it is that accounting records maintained on the accrual basis of

accounting do not show cash flows as balances of specific ledger accounts.

5Explain how cash flows may be determined by examining income statement accounts and

the changes in related balance sheet accounts.

6Illustrate the computation of the basic cash flows (direct method) relating to operating

activities. Emphasize the rationale underlying each computation.

7Explain the basic reasons why net cash flow from operating activities may differ from the

amount of net income.

8Illustrate the computation of cash flows relating to investing and financing activities. Again,

emphasize the rationale underlying each computation.

9Briefly compare and contrast the direct and indirect methods of reporting net cash flows

from operating activities.

10 Discuss the critical importance of managing cash flows and introduce strategic options for

management to improve cash flows from existing operations.

General comments

When the FASB acted to replace the statement of changes in financial position with a new

financial statement¾a statement of cash flows¾we believe the Board significantly improved the

quality of financial reporting and accounting education. The old statement of financial position

was difficult to read, to understand, and to teach. It could be prepared on any of several

bases¾including cash, working capital, and net quick assets. The “funds statements” included in

the annual reports of major companies were difficult to interpret and seldom comparable, and

they usually bore little resemblance to the textbook illustrations. And teaching “funds flow” was

not easy, especially at the introductory level. Typical teaching approaches usually involved

complicated working papers, mythical T accounts, and numerous confusing adjustments to the

net income figure.

We find the new statement of cash flows intuitively logical. Therefore, it should be more

meaningful to readers of financial statements and easier to explain in the classroom. The

phenomenon of cash flows from operations is now explained by such easy-to-understand

captions as “Cash collected from customers” and “Cash paid to suppliers and employees.”

Chapter 13 – Statement of Cash Flows

Compare this to the old approach of “Net income, plus depreciation, minus nonoperative gains,

plus nonoperative losses, etc., etc.”

The direct and indirect methods One area of controversy in presenting cash flows is whether

to use the direct or indirect method of determining the cash flow from operating activities. The

FASB recommends use of the direct method, but at present, the indirect method is far more

widely used in practice.

Without question, we opt for the direct method. Introductory students are able to

understand the direct method, as it explains in straightforward terms the nature of the cash flows

comprising “operating activities.” The indirect method is an abstraction, meaningful only to

someone who already understands clearly the differences between the accrual and cash basis of

accounting. Thus, we consider the direct method a “gift from heaven” to the introductory

accounting instructor.

Of course, not everyone sees it our way. Therefore we also present the indirect approach.

A Supplemental Topic presents a worksheet approach to the indirect method.

Supplemental Exercises

Group Exercise

Two methods of preparing the operating activities section of the cash

ow statement are discussed in the text: the indirect method and the direct

method.

Go to http://www.fasb.org/st/summary/stsum95.shtml and review

the FASB Statement No. 95 to see if the FASB has a preference on which

method to use in preparing the operating activities section.

Internet Exercise

Obtain the latest annual report for ExxonMobil at www.exxonmobil.com.

Examine the balance sheet. What amount of current liabilities is the

company reporting as of the end of the current accounting period? Now

obtain the statement of cash ows. How much cash did ExxonMobil

generate from operating activities during this accounting period? Was this

net cash ow from operating activities suffcient to pay the company’s

current liabilities? If not, how did the company obtain the necessary cash to

remain solvent?

10-MINUTE QUIZ A SECTION

In order to prepare the statement of cash flows for Rag Dolls Corporation for 2010, the

accountant has compiled the following data regarding cash flows:

Cash paid to acquire marketable securities……..……..……………………..….….... $ 370,000

Chapter 13 – Statement of Cash Flows

Proceeds from issuance of capital stock..……………..…………………..…..…….... 280,000

Proceeds from issuance of bonds payable….……..…………………..…..………..… 55,000

Payments to settle short-term debt.……………………………..…….……..……..…… 32,500

Interest and dividends received……………………………………………………..…….. 10,000

Cash received from customers………………………………………………….…….…... ?

Dividends paid……………………………………………………………….…….….….…... 130,000

Cash paid to suppliers and employees……..……………………..………………..…… 1,030,000

Interest paid…………………………………………………………………………………..…. 25,000

Income taxes paid………………………………………………………………………..….… 70,000

Cash and cash equivalents, January 1, 2010……….……………..…………...……... 43,000

Cash and cash equivalents, December 31, 2010………..…………….……..…….... 58,000

Using the above information, indicate the best answer for each question in the space provided.

1Rag Dolls’ cash flow from investing activities during 2010 is:

a$390,000 net cash used by investing activities.

b$322,500 net cash provided by investing activities.

c$352,500 net cash used by investing activities.

d$360,000 net cash used by investing activities.

2Rag Dolls’ cash flow from financing activities during 2010 is:

a$322,500 net cash provided by financing activities.

b$172,500 net cash provided by financing activities.

c$127,500 net cash provided by financing activities.

d$375,000 net cash provided by financing activities.

3Rag Dolls’ cash flow from operating activities during 2010 is:

a$45,000 net cash provided by operating activities.

b$1,155,000 net cash used by operating activities.

c$240,000 net cash provided by operating activities.

d$195,000 net cash provided by operating activities.

4In the 2010 statement of cash flows for Rag Dolls Corporation, the amount of cash

received from customers is:

a$1,310,000.

b$1,103,000.

c$1,233,000.

d$1,293,000.

CHAPTER 13 NAME …………………………………….….….

#

10-MINUTE QUIZ B SECTION

Use the following information for questions 1 through 4.

Lester Corporation’s statement of cash flows for 2009 shows the following investing activities:

Proceeds from sale of marketable securities……….……………………..…..…….... $ 160,000

Purchase of land……………………………………………………………………….….…... (250,000)

Proceeds from sale of land……………………………………………………………….…. 125,000

Net cash provided by investing activities………………………..…..……..…….... $ 35,000

Chapter 13 – Statement of Cash Flows

Lester’s income statement for 2009 includes the following:

Loss on sale of marketable securities……..……………..………………..……..…….. $47,000

Gain on disposal of land……………………………………………………..….…….….… 65,000

1Refer to the above data. The cost of the land sold during 2009 was:

a$65,000. b$125,000. c$190,000. d$60,000.

2Refer to the above data. The cost (book value) of the marketable securities sold during

2009 was:

a$207,000. b$113,000. c$160,000. dSome other amount.

3Refer to the above data. Lester’s balance sheet at the end of 2008 showed Land of

$100,000. On the basis of the data presented above, compute the amount to be reported for

Land in Lester Corporation’s balance sheet at December 31, 2009.

a$250,000. b$350,000. c$290,000. dSome other amount.

4Refer to the above data. Lester’s balance sheet at the end of 2008 showed Investment in

Marketable Securities at $250,000. On the basis of the data presented above, compute the

amount to be reported for Investment in Marketable Securities in Lester Corporation’s

balance sheet at December 31, 2009.

a$43,000. b$110,000. c$137,000. d$253,000.

5Which of the following correctly describes a difference between the direct method and the

indirect method of computing operating cash flow?

aThe direct method is used when accounting records are kept on a cash basis; the

indirect method is used when accounting records are maintained on an accrual basis.

bThe direct method may be used only when a company maintains special journals for

cash receipts and cash disbursements; the indirect method is used in all other

situations.

cBoth the direct and the indirect methods result in the same net cash flow from

operating activities, but the format of this section of the statement of cash flows is

different under the alternative methods.

dThe direct method is used when all accounting records and bank statements are

available; the indirect method is used when some accounting records or documents

are missing or have been destroyed.

CHAPTER 13 NAME #

10-MINUTE QUIZ C SECTION

Using the following information, complete the statement of cash flows for Nutritional Foods for the year

ended December 31, 2010. Place parentheses around those figures in the statement representing cash outlays.

Payments for purchase of land……………………………………………………………..….….….….… $ 416,000

Proceeds from sale of land…………………………………………………………………………….….…. $58,000

Proceeds from issuance of capital stock..……………..……………………..…….……..……..…….. $347,000

Proceeds from issuance of bonds payable……………………………………………………………….. $99,000

Payments to settle short-term debt……………………………………………………………………….... $74,000

Interest and dividends received……………………………………………………………….…….….….. $49,500

Cash received from customers………………………………………………………………….….….…... $1,502,000

Dividends paid…………………………………………………………………………………………………... $182,000

Cash paid to suppliers and employees……..……………………..…………………………...……..…. $1,172,000

Interest paid …………………………………………………………………………………..….….….….… $66,000

Income taxes paid………………………………………………………………………………….….….….… $115,500

Financial Accounting, 16e 13- 7

Chapter 13 – Statement of Cash Flows

Cash and cash equivalents, January 1, 2010……….……………..…………………..…..……..……. $86,000

Cash and cash equivalents, December 31, 2010………..……………………..………..……..…….. ?

NUTRITIONAL FOODS

Statement of Cash Flows

For the Year Ended December 31, 2010

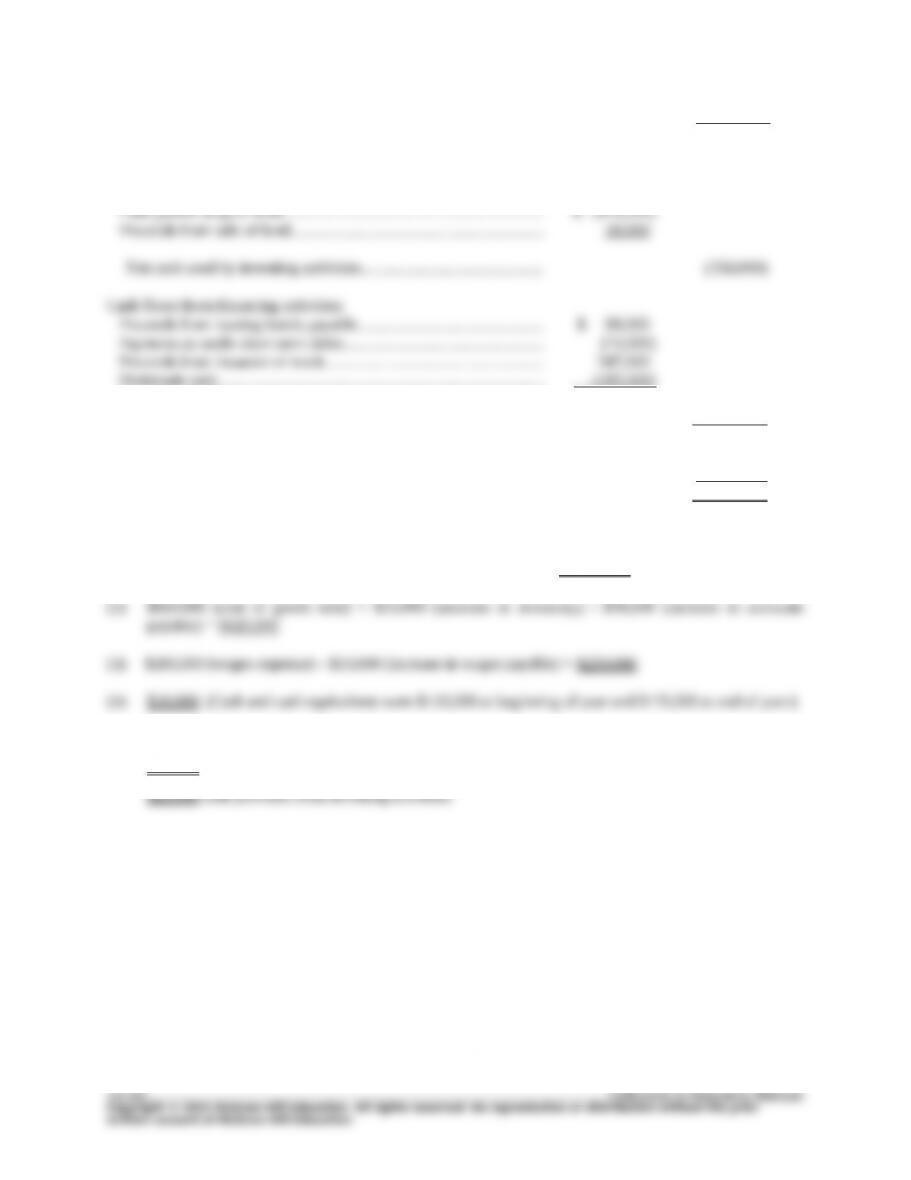

Cash flows from operating activities (direct method):

Cash received from customers………..…………………………….….. $

_________

Cash provided by operating activities……………………………..… $

$

_________

Cash disbursed for operating activities………..……...……..…….. (_______)

Net cash flows from operating activities……………………..…. $

Cash flows from investing activities:

$

_________

Net cash used by investing activities….………..……..……..….. ( )

Cash flows from financing activities:

$

_________

Net cash provided by financing activities ....………..……..….. _______

Net increase (decrease) in cash…..……………………………..……..……... $

Cash and cash equivalents, beginning of year….……..……..……..……. _______

Cash and cash equivalents, end of year.……………..……...……..…….... $______

CHAPTER 13 NAME #

10-MINUTE QUIZ D SECTION____________________________________

The following balance sheets are provided for Socrates Foods:

End of Beginning

Year of Year

Cash and cash equivalents………………………………………………………….. $170,000 $120,000

Accounts receivable………………………………………………………………….. 80,000 65,000

Inventory…………………………………………………………………….….….…... 140,000 130,000

Plant and equipment (net)…..……………..……………………..……..………... 130,000 80,000

Total assets……………………………………………………………………………. $520,000 $395,000

Accounts payable (for merchandise)………..…………………...……..……… $ 65,000 $ 35,000

Wages payable…………………………………………………………………….…... 120,000 110,000

Long-term liabilities…………………..……………………....………..……..…… 95,000 70,000

Common stock…………………………………………………………………………. 100,000 100,000

Retained earnings……..……………………..……………………..……..……..…. 140,000 80,000

Total liabilities and owners’ equity…………..………………..……..…….... $520,000 $395,000

Chapter 13 – Statement of Cash Flows

Selected information from Socrates Foods’ current year income statement:

Sales ……………………………………………………………………………………………….….….…. $1,650,000

Cost of goods sold…………………………………………………………………………………..….… 840,000

Wages expense………………………………………………………………………………….….….….. 260,000

a Compute the following:

(1) Cash received from customers during the year….………………..……..……... $__________

(2) Cash payments for merchandise during the year…….………………………….. $__________

(3) Wages paid to employees during the year….……………………..…………….... $__________

(4) In Socrates Foods’ statement of cash flows, what amount would be reported as the net change in

cash and cash equivalents?

$__________ (increase/decrease)

b Socrates Foods recorded the sale of equipment as follows:

Cash………………………………………………………………………………. 25,000

Accumulated Depreciation: Equipment….……………...……..…….. 20,000

Loss on Disposal of Equipment………..……………………....……….. 15,000

Equipment…………………………………………………………………... 60,000

How would this transaction be reported in Socrates Foods’ statement of cash flows? (Assume the direct

method is being used.)

SOLUTIONS TO CHAPTER 13 10-MINUTE QUIZZES

QUIZ A QUIZ B

5C

QUIZ C

NUTRITIONAL FOODS

Statement of Cash Flows

For the Year Ended December 31, 2010

Cash flows from operating activities:

Cash received from customers…….……………..………..……..……..… $ 1,502,000

Interest and dividends received..……..…………………….……..……..… 49,500

Financial Accounting, 16e 13- 9

Chapter 13 – Statement of Cash Flows

Cash disbursed for operating activities..……………..………..……..… (1,353,500)

Net cash flows from operating activities……….…………………………. $ 198,000

Cash flows from investing activities:

Dividends paid………………………………………………………………….… (182,000)

Net cash provided by financing activities……..…………...……..…… 190,000

Net increase (decrease) in cash…..……………………………..……..……... $ 30,000

Cash and cash equivalents, beginning of year….……..……..……..……. 86,000

Cash and cash equivalents, end of year.……………..……...……..…….... $ 116,000

QUIZ D

a

(1) $1,650,000 (sales) – $15,000 (increase in accounts receivable) = $1,635,000

b$25,000 proceeds from disposal of equipment, classified as an investing activity or

Chapter 13 – Statement of Cash Flows

Assignment Guide to Chapter 13

Brief

Exercises Exercises Problems Cases Net

1 – 10 1 – 15 1 2 3 4 5 6 7 8 1 2 3 4 5 6

Time estimate (in minutes) < 15 < 15 40 40 25 30 60 25 25 50 25 15 45 15 20 30

Difficulty rating E E M M S M S E M S S E M E M M

Learning Objectives:

1, 2, 15 √

1. Explain the purposes and uses

of a statement of cash flows.

2. Describe how cash transactions

are classified in a statement of

cash flows. 8, 10

1, 2, 7, 11,

12, 15

3. Compute the major cash flows

relating to operating activities. 1, 3, 7 4, 5, 6

4. Compute the cash flows relating

to investing and financing

activities. 5, 6

3, 13, 14, 15

5. Distinguish between the direct

and indirect methods of

reporting operating cash flows.

6. Explain why net income differs

from net cash flows from

operating activities. 9 2, 4, 6, 9

7. Compute net cash flows from

operating activities using the

indirect method.2, 4 9, 10

8. Discuss the likely effects of

various business strategies on

cash flows. 8

9. Explain how a worksheet may

be helpful in preparing a

statement of cash flows.

13-11 Instructor’s Resource Manual