25 Minutes, Medium

JENCO

a.

Nov 1 Interest Expense 1,000

1,633

Cash 2,633

c.

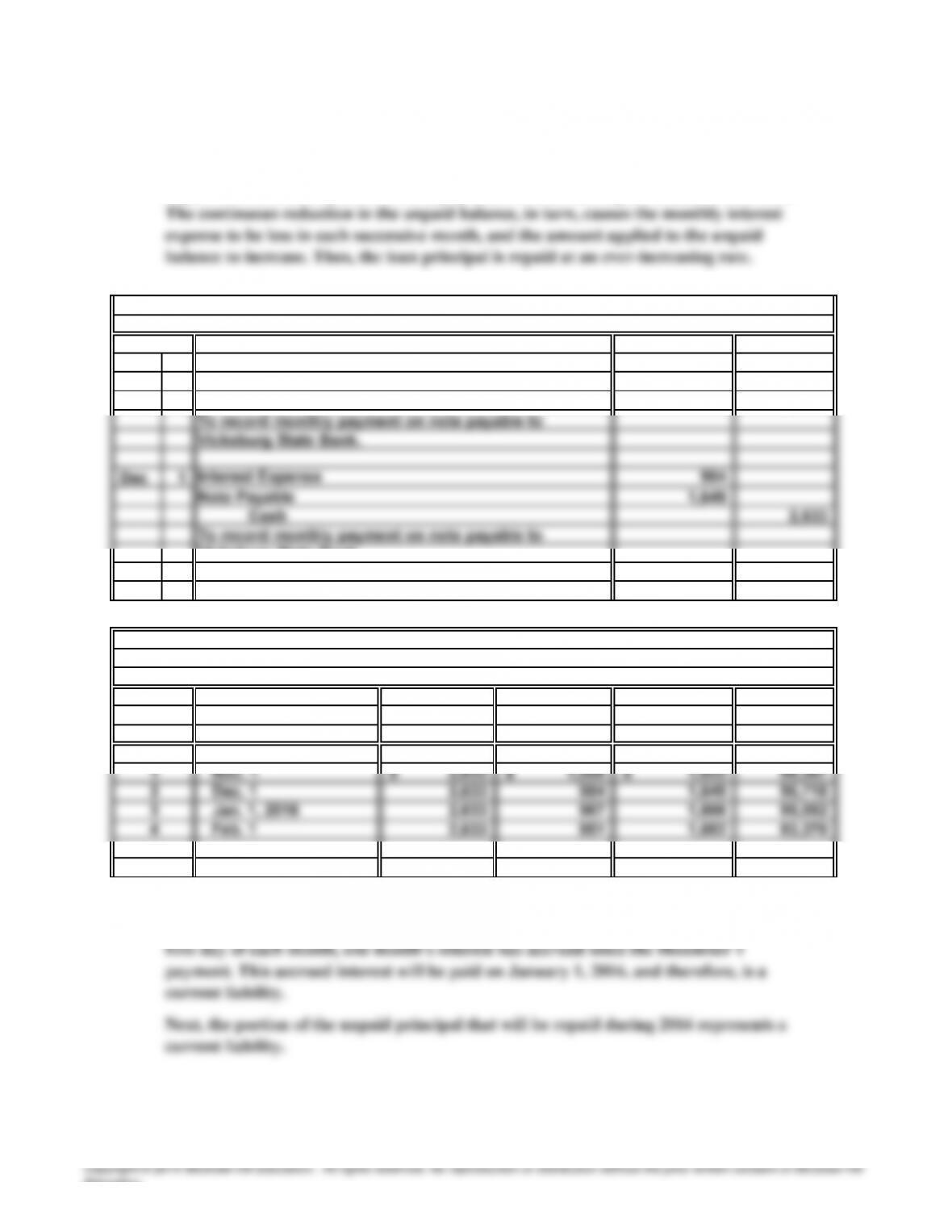

Reduction in

Monthly Interest Unpaid Unpaid

Payment Expense Balance Balance

100,000$

d.

2015

Note Payable

PROBLEM 10.4B

b.

General Journal

V

icksburg State Bank.

Amortization Table

Date

Issue date Oct. 1, 2015

(12%, 4-Year Mortgage Note Payable for $100,000;

Payable in 48 Monthly Installments of $2,633)

Interest Payment

The amount of the monthly payments exceeds the amount of the monthly interest

expense. Therefore, a portion of each payment reduces the unpaid balance of the loan.

At December 31, 2015, two amounts relating to this mortgage loan will appear as

current liabilities in the borrower’s balance sheet. First, as payments are due on the

first day of each month, one month’s interest has accrued since the December 1

payment. This accrued interest will be paid on January 1, 2016, and therefore, is a

current liability.

Period

Education.

V

15 Minutes, Easy

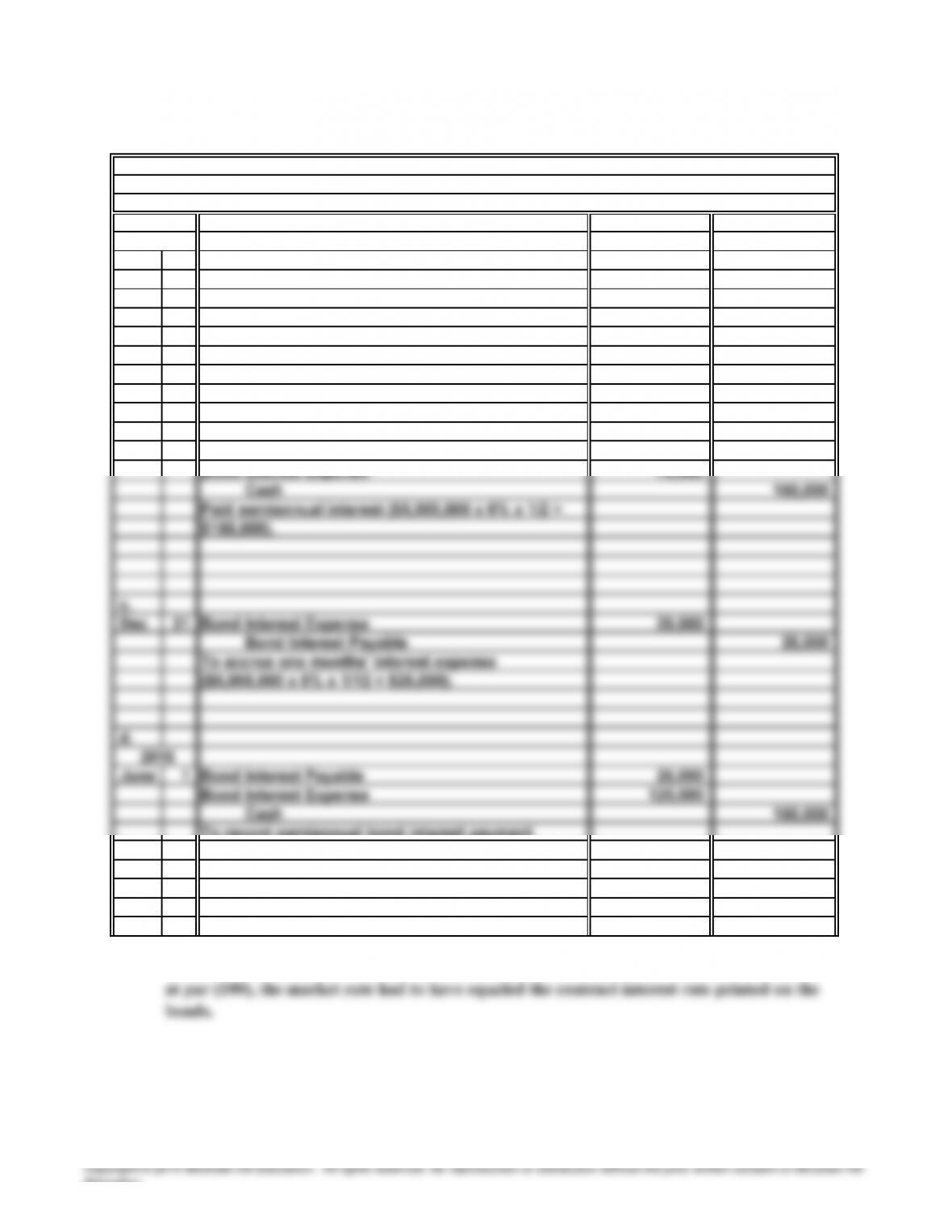

Sept 1 Cash 5,075,000

Bonds Pa

y

able 5,000,000

Bond Interest Pa

y

able 75,000

b.

Dec 1 75,000

e.

a.

PROBLEM 10.5B

General Journal

E

VENS MANUFACTURING COMPAN

Y

2015

bonds at 100 plus accrued interest for three

and interest expense for 5 months since Dec. 31

months ($5,000,000 x 6% x 3/12 = $75,000).

Bond Interest Payable

($5,000,000 x 6% x 5/12 = $125,000).

To record semiannual bond interest payment

Issued $5,000,000 face value of 6%, 10-yea

r

The market rate of interest on the date of issuance was 6%. Because the bonds were issued

at par (100), the market rate had to have equaled the contract interest rate printed on the

bonds.

Education.

35 Minutes, Strong

RODRIGUEZ PLUMBING COMPAN

Y

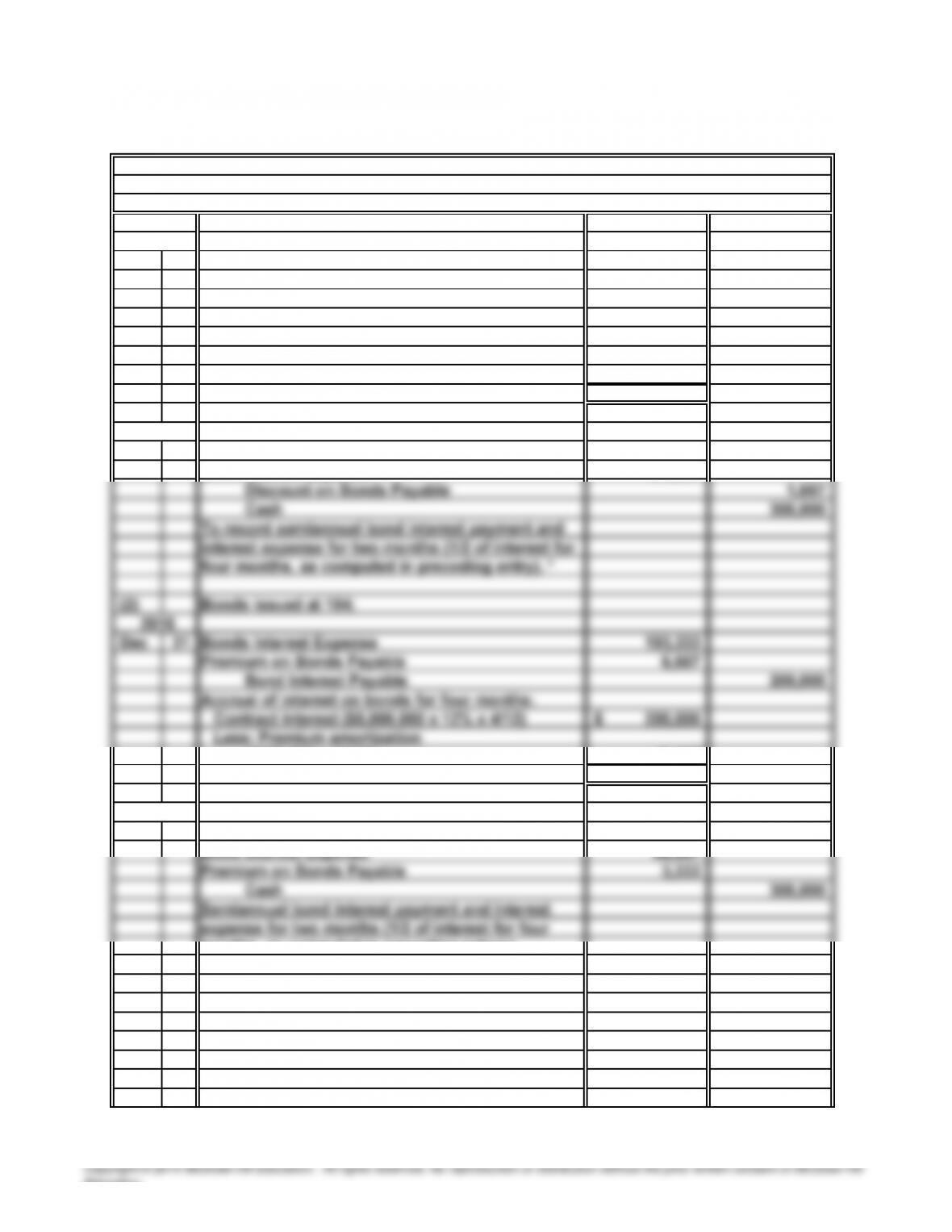

Dec 31 Bond Interest Expense 203,333

3,333

Bond Interest Pa

y

able 200,000

200,000$

3,333

203,333$

Mar 1 200,000

101,667

(

6,667

)

193,333$

Mar 1 200,000

2016

months, as computed in preceding entry).*

Bond Interest Payable

* Actual amount differs slightly due to rounding

To record accrual of bond interest expense for

2015

Discount on Bonds Payable

four months in 2015:

Discount amortization ($100,000 x 4/120)

Bond interest expense for four months

Contract interest ($5,000,000 x 12% x 4/12)

($200,000 x 4/120)

Bond interest expense for four months

PROBLEM 10.6B

a.

General Journal

(1) Bonds issued at 98:

2016

Bond Interest Expense

Bond Interest Payable

Education.

b.

Net bond liability at Dec. 31, 2016: Bonds Bonds

Issued Issued

at 98 at 104

5,000,000$ 5,000,000$

*

Less:Discount on bonds payable ($100,000 – $13,333) (86,667)

PROBLEM 10.6B

RODRIGUEZ PLUMBING COMPANY (concluded)

Bond payable

45 Minutes, Strong

a.

Liabilities: (in thousands)

Accounts payabl

e

48,000$

7,200

Accrued interest payabl

e

3,650

Notes payable (short-term) 75,000

Capital lease obligation (current portion) 3,000

I

8

100,000$

150

,

000

$

270

149

,7

30

300

,

000

$

2

,

000

302

,

000

15,000

110

000

T

881

80

$

c. (1) Computation of debt ratio:

Total liabilities

(

above

)

881,580$

Part d appears on the following page.

10% Bonds payable, due April 1, 201

6

8% Bonds payable, due October 1, 2016

Less: Discount on bonds payable

12% Bonds payable, due April 1, 201

8

Part b appears on the following page.

Add: Premium on bonds payable

Capital lease obligation (less current portion)

Current liabilities:

Accrued expenses payable (other than interest)

Long-term liabilities:

PROBLEM 10.7B

NEVADA UTILITY COMPAN

Y

December 31, 2015

Partial Balance Shee

t

NEVADA UTILITY COMPAN

Y

Education.

b. (1)

(2)

(6)

d.

PROBLEM 10.7B

NEVADA UTILITY COMPANY

(concluded)

As the 10% bond issue is being refinanced on a long-term basis (that is, paid from the

proceeds of a long-term bond issue rather than from current assets), it is classified as a

long-term liability rather than a current liability.

The 8% bonds will be repaid from a bond sinking fund rather than from current assets.

Income taxes payable relate to the current year’s income tax return and, therefore, are

a current liability. Although deferred income taxes can include a current portion, all of

the deferred income taxes are stated to be a long-term liability.

Based solely upon its debt ratio and interest coverage ratio, Nevada Utility appears to be a

good credit risk. One must consider, however, that Nevada Utility is a utility company, not a

business organization that battles numerous competitors on a daily basis. Utility companies

Education.

20 Minutes, Strong

a.

Liabilities:

Unearned revenues 268,000$

145,000

Notes payable (current portion) 27,000

A

ccrue

d

b

on

d

i

nterest paya

bl

e

22

,5

00

462,500$

750,000$

b.

●

●

●

The lawsuit pending against the company is a loss contingency. It should be disclosed in

the financial statements, probably in the form of a note to the statements, but no liability

should be formally recognized until a reasonable estimate can be made and the

probability of loss is established.

The 3-year salary commitment to Fred Money, Chief Financial Officer, relates to future

events and, therefore, is not a liability at the present time.

*$150,000 – $27,000 – $123,000

**$260,000 – $145,000 = $115,000

The following items listed by the company have been excluded from current and long-term

liabilities for the reasons indicated:

Interest expense that will arise in the future from existing obligations is not yet a liability.

PROBLEM 10.8B

A

LEXANDER COMPAN

Y

Bonds payable

Current liabilities:

Income taxes payable

Long-term liabilities:

Education.

30 Minutes, Medium

a.

b.

d.

e.

SOLUTIONS TO CRITICAL THINKING CASE

S

LIABILITIES IN PUBLISHED

CASE 10.1

FINANCIAL STATEMENT

S

Wausau Paper’s liability for “current maturities” of long-term debt is common to most large

organizations. This liability arises as debt instruments originally classified as long-term near

their maturity dates. The principal amounts scheduled for repayment within the next year (or

Wells Fargo’s liability for interest-bearing deposits represents the amounts on deposit in

interest-bearing bank accounts. This liability arises from customers depositing money in these

accounts and is discharged whenever customers make withdrawals.

The New York Times’ liability for unexpired subscriptions is a form of unearned revenue

arising from customers paying in advance to receive the newspaper over a designated

payments to holders of winning tickets that have not yet been redeemed. This liability comes

into existence as horses win races, and it is discharged as the track redeems the winning

tickets.

As American Greetings is a manufacturer, it probably sells primarily to wholesalers or

retailers rather than directly to consumers. Apparently, the company allows its customers to

return merchandise that they are unable to sell and to receive a refund of the purchase price.

Given the seasonal nature of holiday greeting cards, wholesalers and retailers are quite likely

experiences. The liability is discharged by making cash refunds (or crediting the account

receivable of a customer making a return).

Education.

g.

h. GM’s liability for postretirement costs is an obligation to pay retirement benefits to

workers—some of whom are already retired and some of whom are currently employed by

Case 10.1

LIABILITIES IN PUBLISHED

Apple’s accrued marketing and distribution liability represents accrued marketing and

FINANCIAL STATEMENTS (concluded

)

Education.

20 Minutes, Strong

BOND PRICES

a.

b.

c.

CASE 10.2

A

BBOTT LAB

S

Differences in the length of time remaining until the bond issues mature is the major factor

influencing the current market prices. As bonds near their maturity dates, their market

The effective rate of interest is higher on issue A bonds. The less that investors pay for

The bonds of both issues pay the investors $60 over twelve months, computed as

follows:

Education.

25 Minutes, Medium

a.

1

2

CASE 10.3

LOSS CONTINGENCIES

The estimated loss from uncollectible accounts is a loss stemming from past events (credit

sales) and is uncertain in dollar amount until the accounts either are paid or become

obviously uncollectible. Therefore, this item is a loss contingency. Typically, the loss

The health, retirement, or even death of company executives are not loss contingencies and

are not recorded or disclosed in financial statements. For one thing, the impact of these

Education.