Chapter 09 – Accounting for Receivables

SERIAL PROBLEM — SP 9

Serial Problem — SP 9, Business Solutions (50 minutes)

1. a. Bad debts expense is recorded as 1% of total revenues:

$44,000 x .01 = $440.

2016

Mar. 31 Bad Debts Expense……………………………………….. 440

Allowance for Doubtful Accounts……....…….. 440

To record estimated bad debts.

2. Allowance Balance as of 3/31/16.……............ $457 Cr.

Less: Account written off..………..…………….. (100) Dr.

Allowance Balance as of 6/30/16.……............ $357 Cr. (before adjustment)

3. Many small business owners use the direct write-off method of

recording bad debts expense. The direct method is a simple and

straightforward method of accounting for bad debts expense. It can

also be justified if the amounts are immaterial. However, when the

9-543

Chapter 09 – Accounting for Receivables

Reporting in Action — BTN 9-1

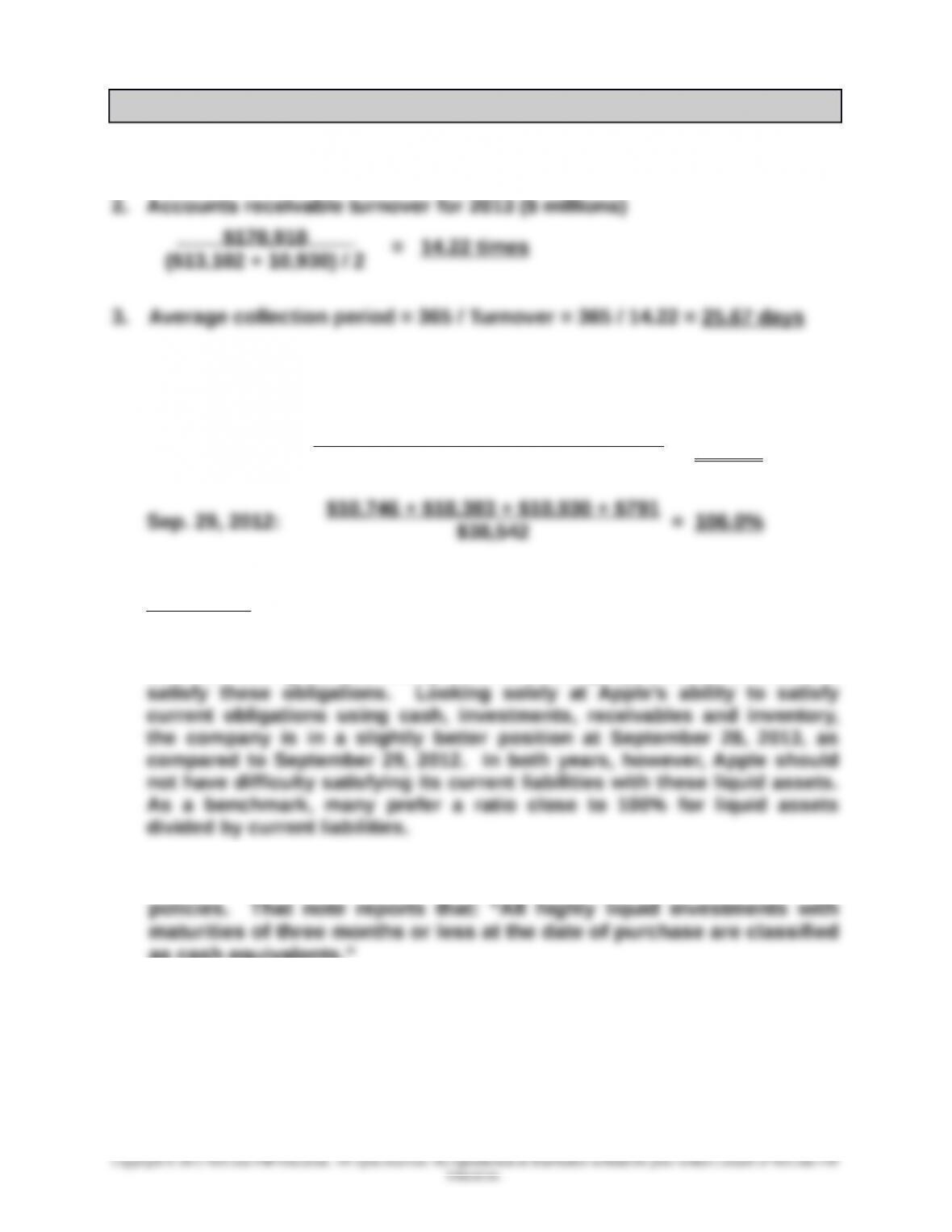

1. Apple’s receivables at September 28, 2013, are $13,102 million.

4. Liquid assets as a percent of current liabilities ($ millions)

Sep. 28, 2013: = 126.9%

Comments: Current liabilities are obligations that are due to be paid or

liquidated within one year or one operating cycle of the business,

whichever is longer. Typically, cash provided from the operations of the

business during the year along with the existing liquid assets are used to

5. Note 1 to Apple’s financial statements describes its accounting

as cash equivalents.”

6. Solution depends on the financial statement information obtained.

9-544

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

$14,259 + $26,287 + $13,102 + $1,764

$43,658

Chapter 09 – Accounting for Receivables

Comparative Analysis — BTN 9-2

1. Accounts Receivable Turnover ($ millions)

Apple (Current Year):

= 14.22 times

Apple (Prior Year):

2. Average Collection Period (or “Average Days’ Sales Uncollected”)

Apple (Current Year): 365 days / 14.22 times = 25.67 days

Apple (Prior Year): 365 days / 19.20 times = 19.01 days

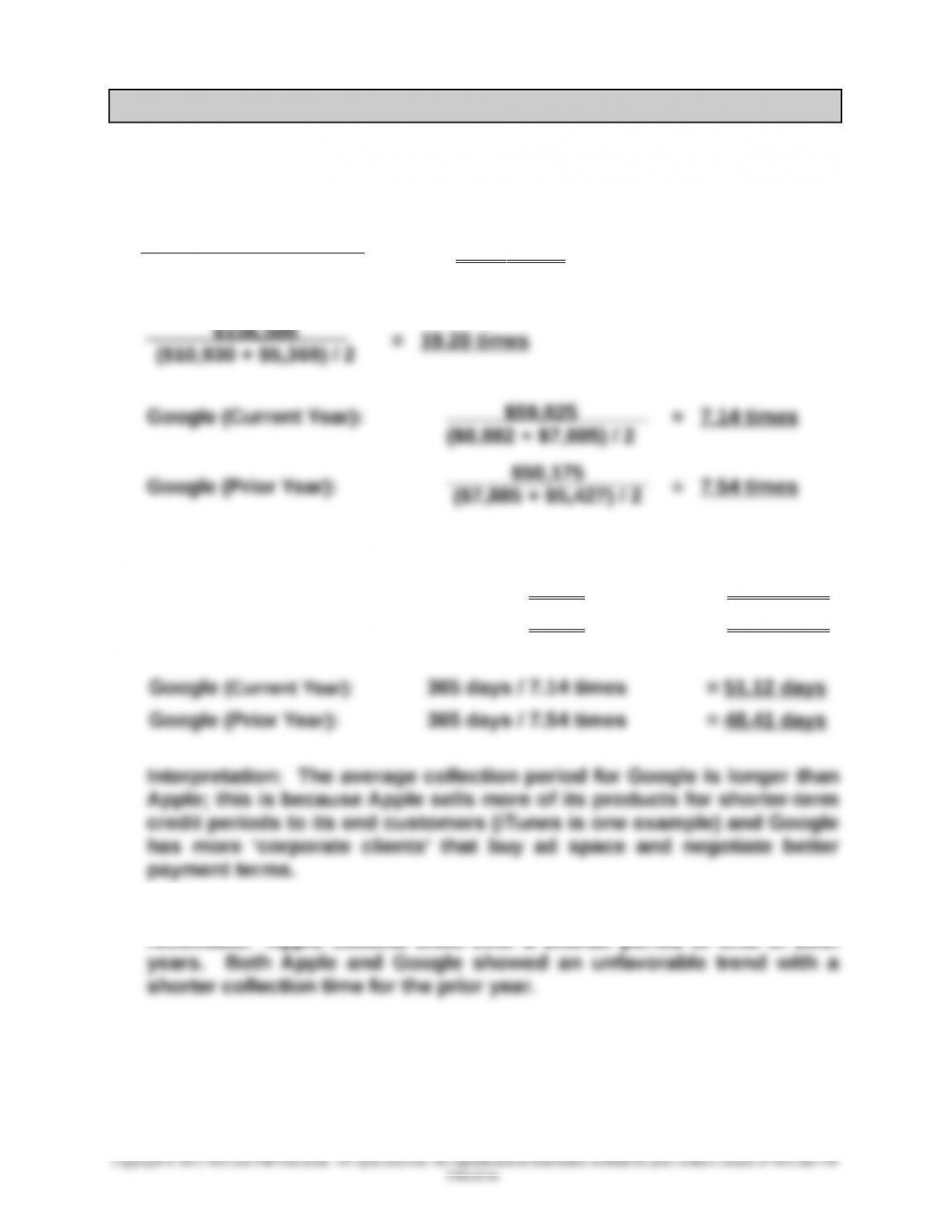

3. Both companies appear reasonably efficient in collecting accounts

receivable. Apple collects them over a shorter period of time in both

9-545

$170,910

($13,102 + $10,930) / 2

Chapter 09 – Accounting for Receivables

Ethics Challenge — BTN 9-3

1. If the estimate for bad debts is reduced then less Bad Debts Expense

will be recognized on the income statement resulting in a higher net

2. Accounting procedures often allow for alternate methods or require the

use of estimates. Therefore, managers have some leeway in their

3. An informed owner or an effective board of directors will be aware of

alternate accounting methods and how estimates can affect the

9-546

Chapter 09 – Accounting for Receivables

Communicating in Practice — BTN 9-4

TO: Sid Omar

FROM: (Your Name)

DATE: _______________

SUBJECT: Difference Between Bad Debts Expense and Allowance

For Doubtful Accounts

In accounting for credit sales and bad debts, we report sales revenue in the

period the sales are made, even though some credit sales do not result in

collections until the following period. Of course, some credit sales

eventually prove to be uncollectible. The fact that some accounts will

become uncollectible is what gives rise to bad debts expense and the

estimated percent times the annual sales for the period. This year’s bad

debts expense of $59,000 is calculated as 2% of the annual sales of

$2,950,000.

Determining Allowance For Doubtful Accounts

The Allowance for Doubtful Accounts unadjusted balance at the end of the

Doubtful Accounts balance. Prior to this year’s bad debts expense

calculation, the cumulative total of writing off specific accounts was

$16,000 greater than the cumulative total of the past years’ bad debts

expenses. Therefore, you could say that Allowance for Doubtful Accounts

had an “abnormal” balance of $16,000. Then, when this year’s bad debts

9-547

Chapter 09 – Accounting for Receivables

Taking It to the Net — BTN 9-5

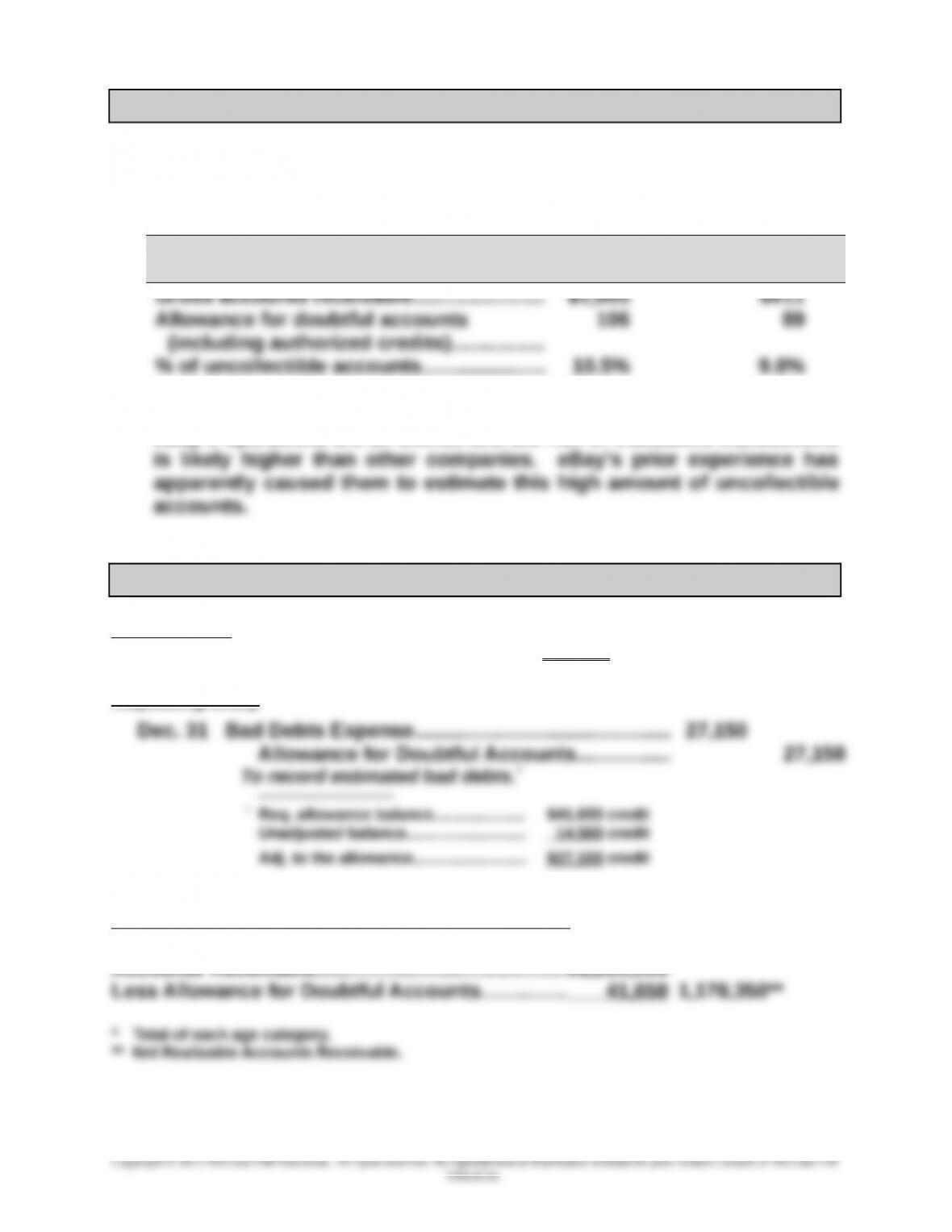

1. At December 31, 2013, eBay’s ($ millions) net accounts receivable were

$899, and at December 31, 2012, its net accounts receivable were $822.

2.

$ millions

December 31,

2013

December 31,

2012

3. These percentages seem high compared to other companies, but

eBay’s operations are all online, and the risk of fraudulent transactions

Teamwork in Action — BTN 9-6

Instructor note: Computations for the aging schedule are in the Problem 9-3A solution.

The check figure for total estimated uncollectibles is $41,650.

Adjusting entry

December 31, 2015, Balance Sheet Presentation

9-548

Chapter 09 – Accounting for Receivables

Entrepreneurial Decision — BTN 9-7

1. Computation of added annual net income or loss

a.

Added Monthly Net Income or Loss under Plan A

Increased sales………………………………………………….…… $250,000

Cost of sales………………………………………..…..……………. (135,500)

b.

Added Monthly Net Income or Loss under Plan B

Increased sales………………………………………………….…… $500,000

Cost of sales………………………………………..…..……………. (375,000)

9-549

Chapter 09 – Accounting for Receivables

Entrepreneurial Decision — BTN 9-7 continued

2. Plan (A) provides a slightly higher income, so if the client company can

only pursue one plan now, based purely on the financial aspect, it

should choose Plan (A).

Plan (B) is a way to expand sales, possibly into more locations. This is

an expansion of a distribution method now employed.

Hitting the Road — BTN 9-8

Telephone calls to VISA and American Express are the source of

information for this solution. VISA reports that the average transaction fee

it charges merchants is 3%. American Express has a range, depending on

9-550

Chapter 09 – Accounting for Receivables

Global Decision — BTN 9-9

1. Accounts Receivable Turnover (KRW in millions)

Samsung (Current Year): 228,692,667 ₩ = 8.38 times

27,875,934 + 26,674,596) / 2₩ ₩

9-551