Part 3

In a banking context, a debit memo is notification from the bank that it has

debited the depositor’s account. Since the depositor’s account is a liability of the

bank (a credit balance account), the debit notification means the bank has

reduced the depositor’s account balance. Conversely, a credit memo is a

notification that the depositor’s account has been credited, which means the

bank has increased the depositor’s cash balance.

Problem 8-5B (50 minutes)

Part 1

SHAMARA SYSTEMS

Bank Reconciliation

May 31, 2015

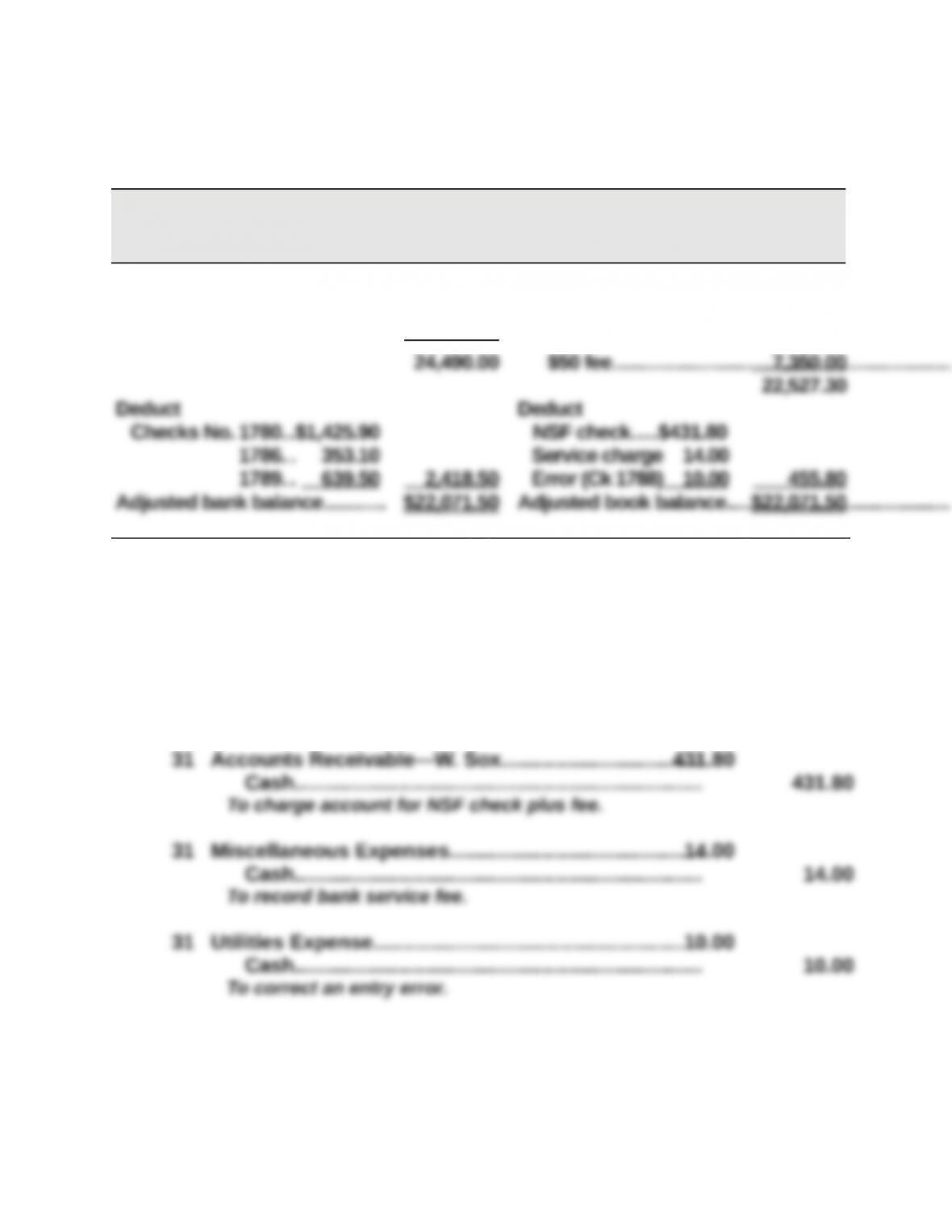

Bank statement balance……… $21,762.70 Book balance …………………………………………………………………………$15,177.30

Add Add

Deposit of May 31……………. 2,727.30

Proceeds of note less

Part 2

May 31 Cash…………………………………………………………………..7,350.00

Collection Expense……………………………………………..50.00

Notes Receivable………………………………………….. 7,400.00

To record note collection less fee.

Problem 8-5B (Concluded)

Part 3

There are several possible reasons why some prenumbered checks are

missing from the sequence of canceled checks returned with a bank

statement. Reasons include:

(1) Some of the checks in the numbered sequence may have cleared the

(2) Some of the checks in the numbered sequence may remain

(3) The issuer of the checks may have voided one or more of the checks

(4) Occasionally, a check will reach the bank but the bank will incorrectly

SERIAL PROBLEM — SP 8

Serial Problem — SP 8, Business Solutions (50 minutes)

Part 1

BUSINESS SOLUTIONS

Bank Reconciliation

March 31, 2016

Bank statement balance….. $67,566 Book balance………………………………………………………………………….$68,057

Add Add

Part 2

Mar. 25 Miscellaneous Expenses……………………………………..677 50

Cash……………………………………………………………..101 50

To record safety deposit box rental.

Reporting in Action — BTN 8-1

1.

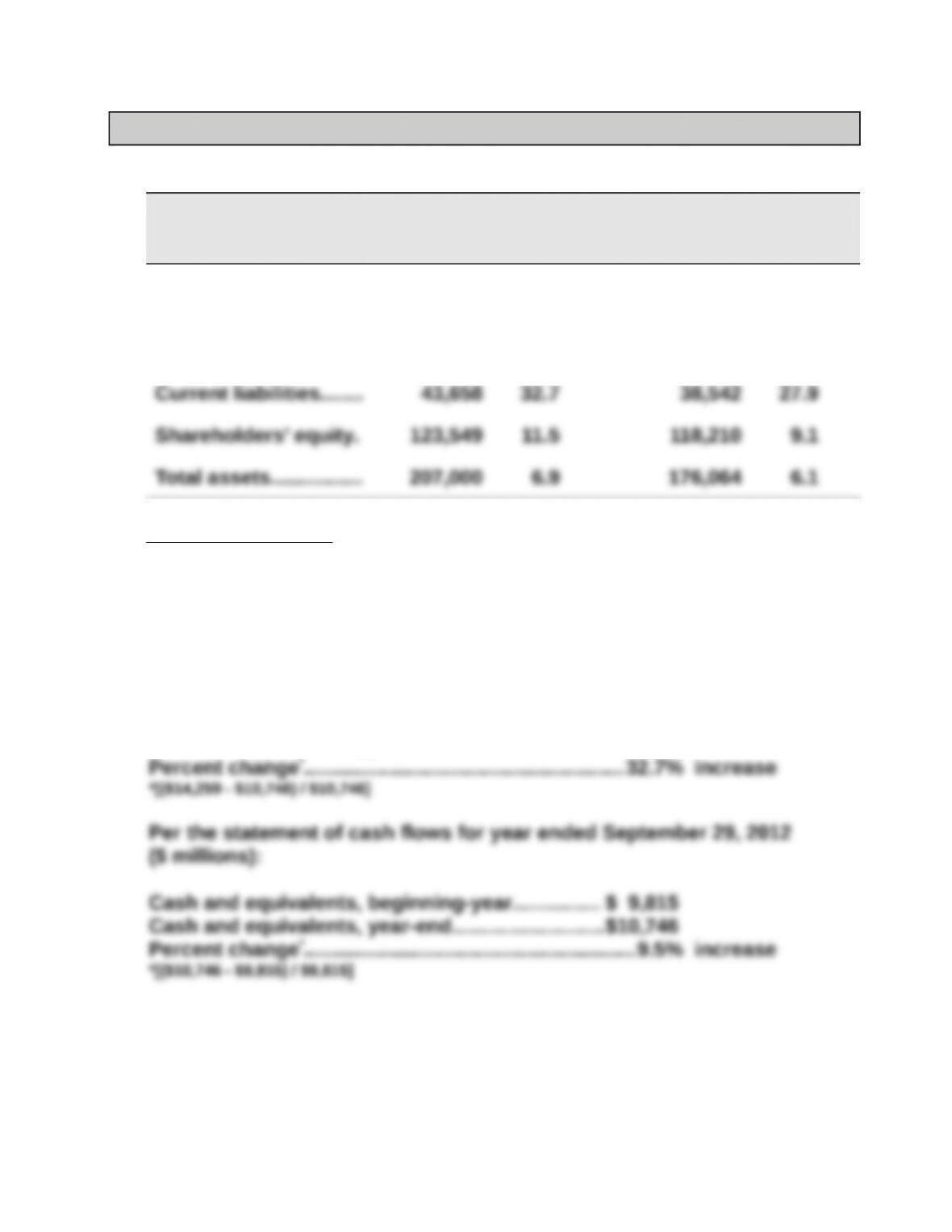

($ in millions)

Balance

September

28, 2013

Cash and

equivalents

as % of:

Balance

September

29, 2012

Cash and

equivalent

s as % of:

Cash and cash

equivalents………….. $ 14,259 — $ 10,746 —

Current assets……….. 73,286 19.5% 57,653 18.6%

Analysis comment: Cash and cash equivalents have slightly increased

as a percent of the various bases over this period. Looking at this

measure only, Apple’s liquidity position has probably slightly improved.

2. Per the statement of cash flows for year ended September 28, 2013

($ millions):

Cash and equivalents, beginning-year…………… $10,746

Cash and equivalents, year-end……………………..$14,259

Reporting in Action (Concluded)

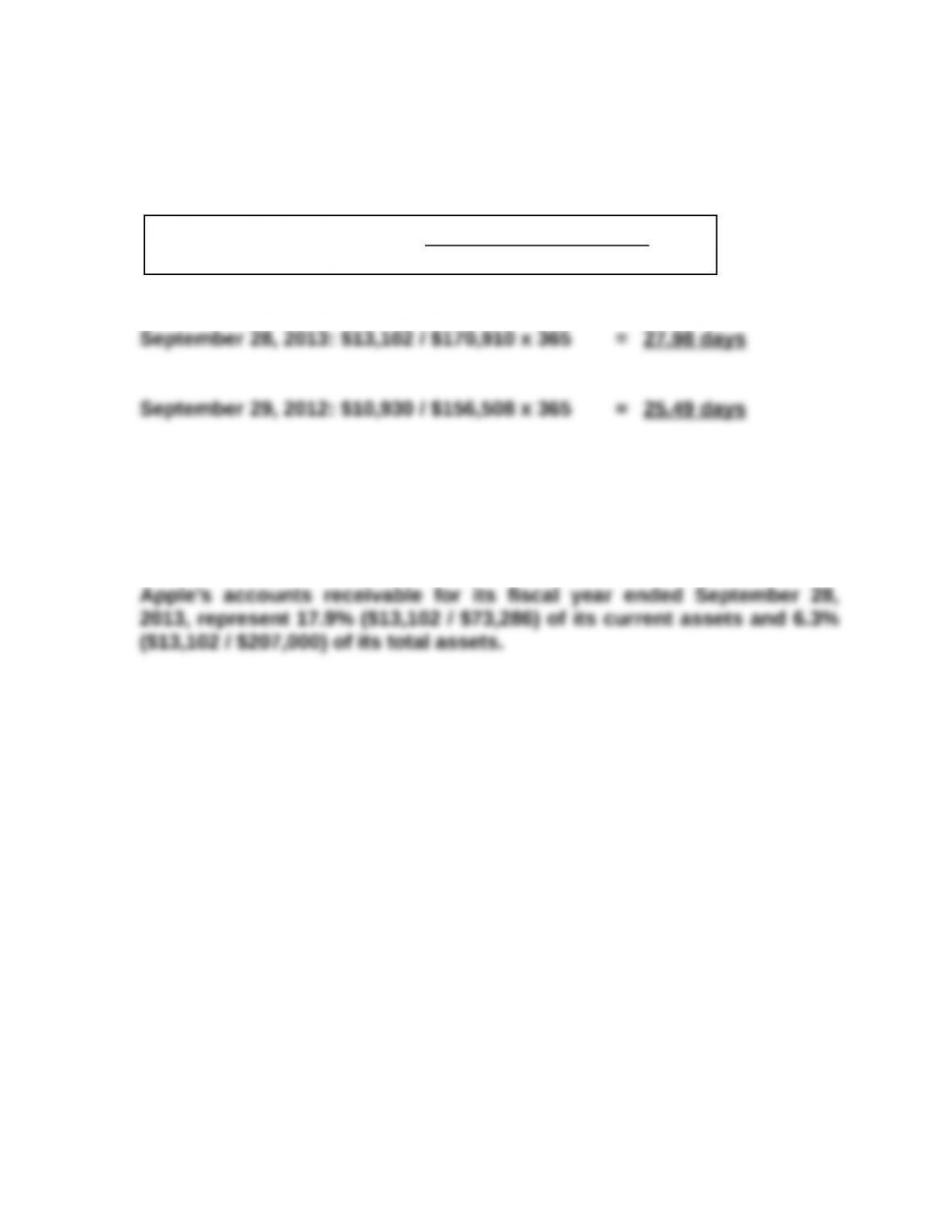

3. Days’ Sales Uncollected ($ thousands)

Days’ sales uncollected = x 365

The number of days of uncollected sales in accounts receivable has

increased from 25.49 days to 27.98 days. This increase of 2.49 days

indicates that the company’s assets are tied up in receivables for a

longer period of time.

4. Solution depends on the annual report information obtained.

Accounts receivable

Net sales

Comparative Analysis — BTN 8-2

Apple ($ millions)

Apple’s days’ sales uncollected has increased by 2.49 days. The

Google ($ millions)

Google’s days’ sales uncollected has decreased by 3.2 days. The

Comparative Analysis: Google’s decrease in days’ sales uncollected is

Accounts receivable

Net sales

Ethics Challenge — BTN 8-3

1. In a small business office it is very important that the owner of the

2. Unfortunately, due to collusion of the employees, the bank

3. Despite the collusion, the scheme is not foolproof. For example, some

ways in which the scheme might be uncovered or prevented include the

following:

A bank employee may become suspicious and call Dr. Conrad and

An astute patient might notice that his/her statement contains a

Dr. Conrad might be able to detect the fraud herself if she reviews the

Dr. Conrad could require approval for each miscellaneous credit.

4. Dr. Conrad should review her salary schedules for employees to make

sure that she is at least offering market pay. She may want to consider