Problem 6-3B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

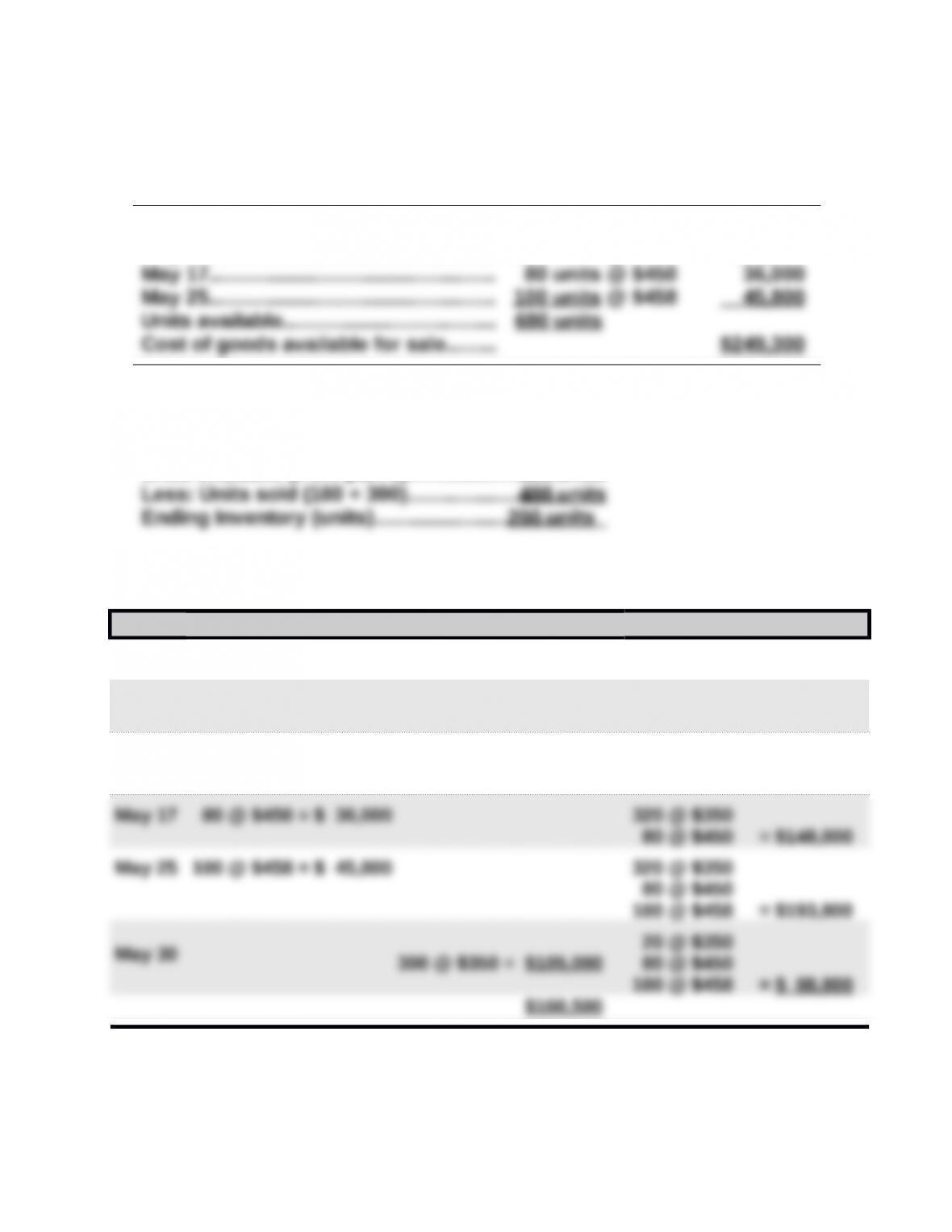

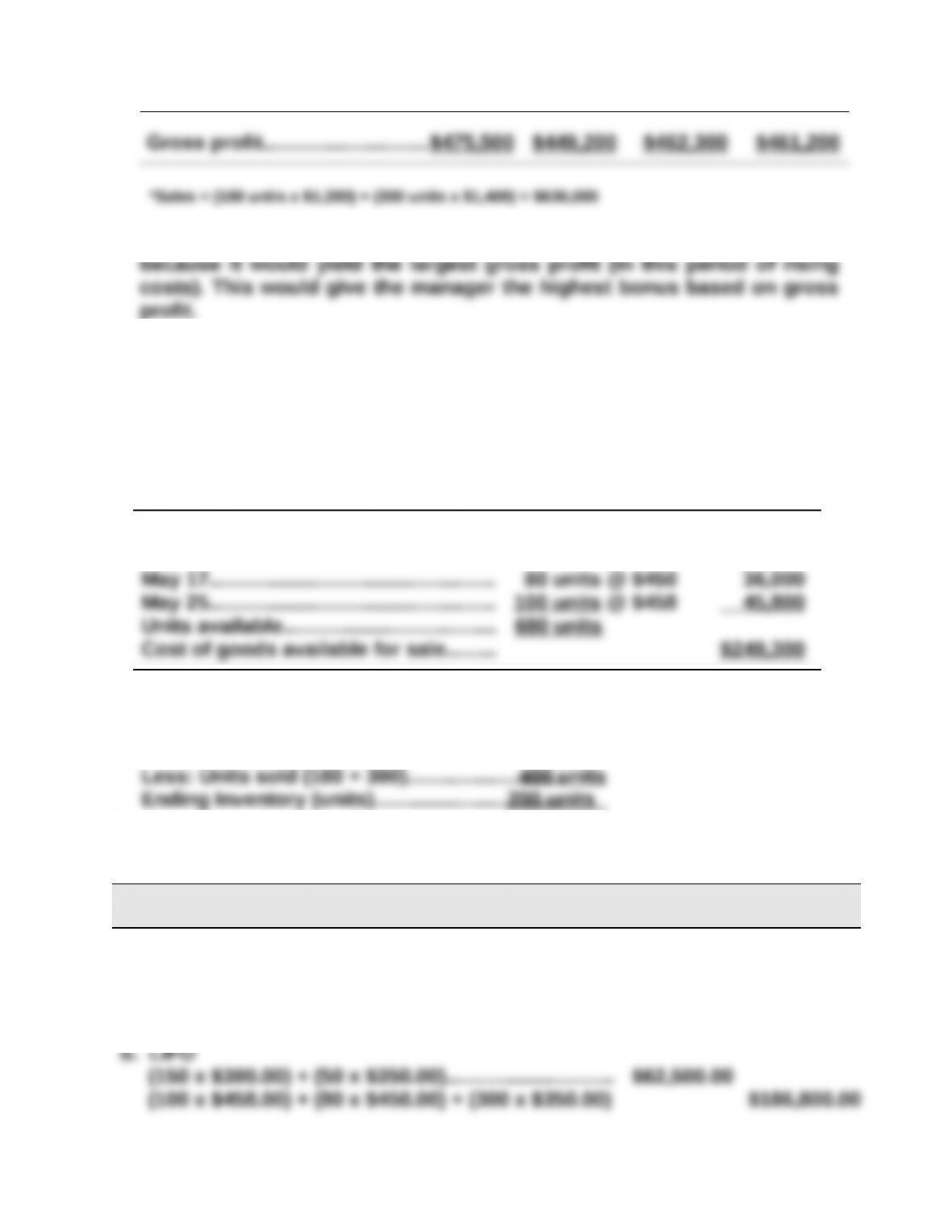

Beginning inventory……..……………….. 150 units @ $300 $ 45,000

May 6……………………………….…………… 350 units @ $350 122,500

2. Units in ending inventory

Units available (from part 1)………….……………680 units

3a. FIFO perpetual

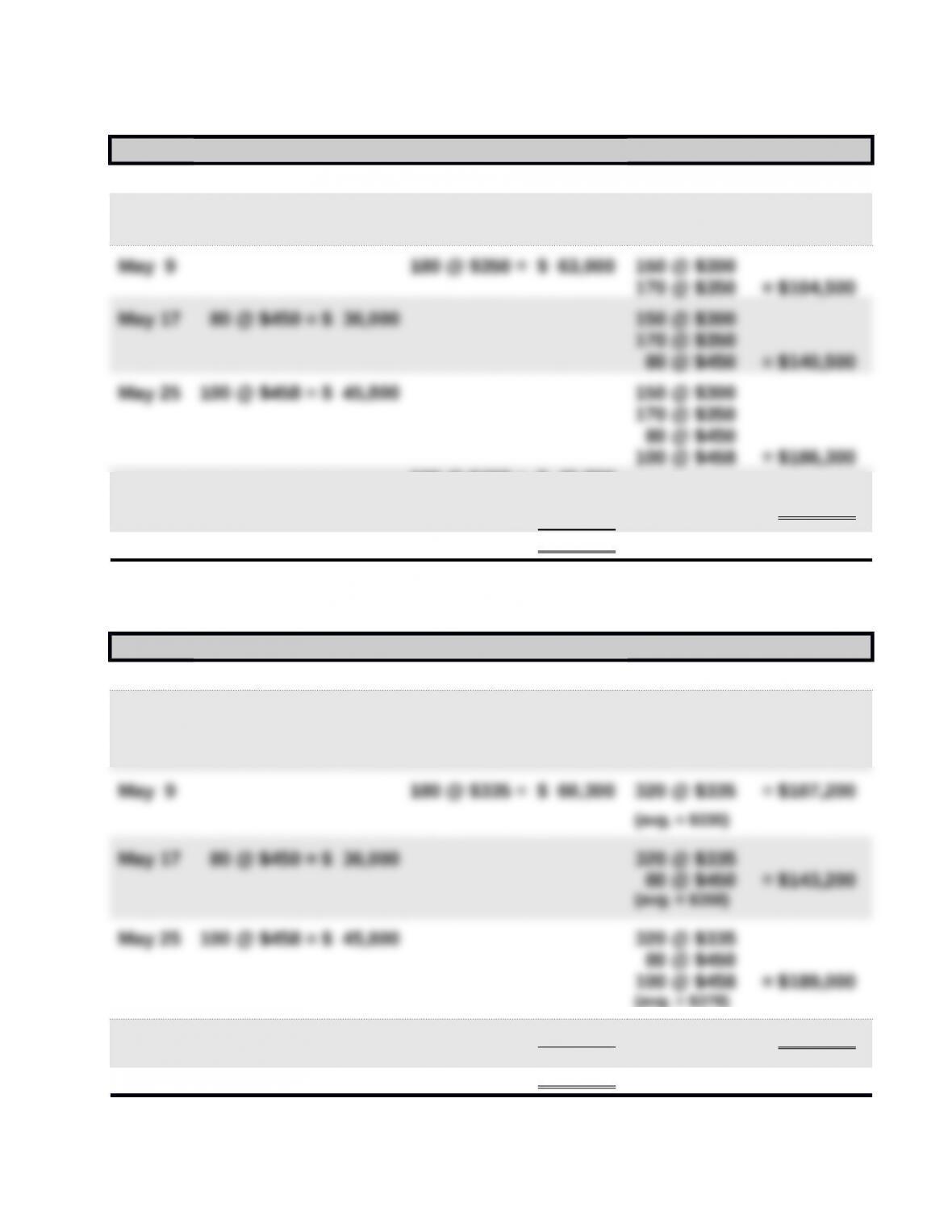

Date Goods Purchased Cost of Goods Sold Inventory Balance

May 1 150 @ $300 = $ 45,000

May 6 350 @ $350 = $122,500 150 @ $300

350 @ $350 = $167,500

May 9 150 @ $300 = $ 45,000

30 @ $350 = $ 10,500

320 @ $350 = $112,000

Problem 6-3B (Continued)

3b. LIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

May 1 150 @ $300 = $ 45,000

May 6 350 @ $350 = $122,500 150 @ $300

350 @ $350 = $167,500

May 30

100 @ $458 = $ 45,800

80 @ $450 = $ 36,000

120 @ $350 = $ 42,000

150 @ $300

50 @ $350 = $ 62,500

$186,800

3c. Weighted Average perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

May 1 150 @ $300 = $ 45,000

May 6 350 @ $350 = $122,500 150 @ $300

350 @ $350 = $167,500

(avg. = $335)

May 30 300 @ $378 = $113,400 200 @ $378 = $ 75,600

(avg. = $378)

$173,700

Problem 6-3B (Continued)

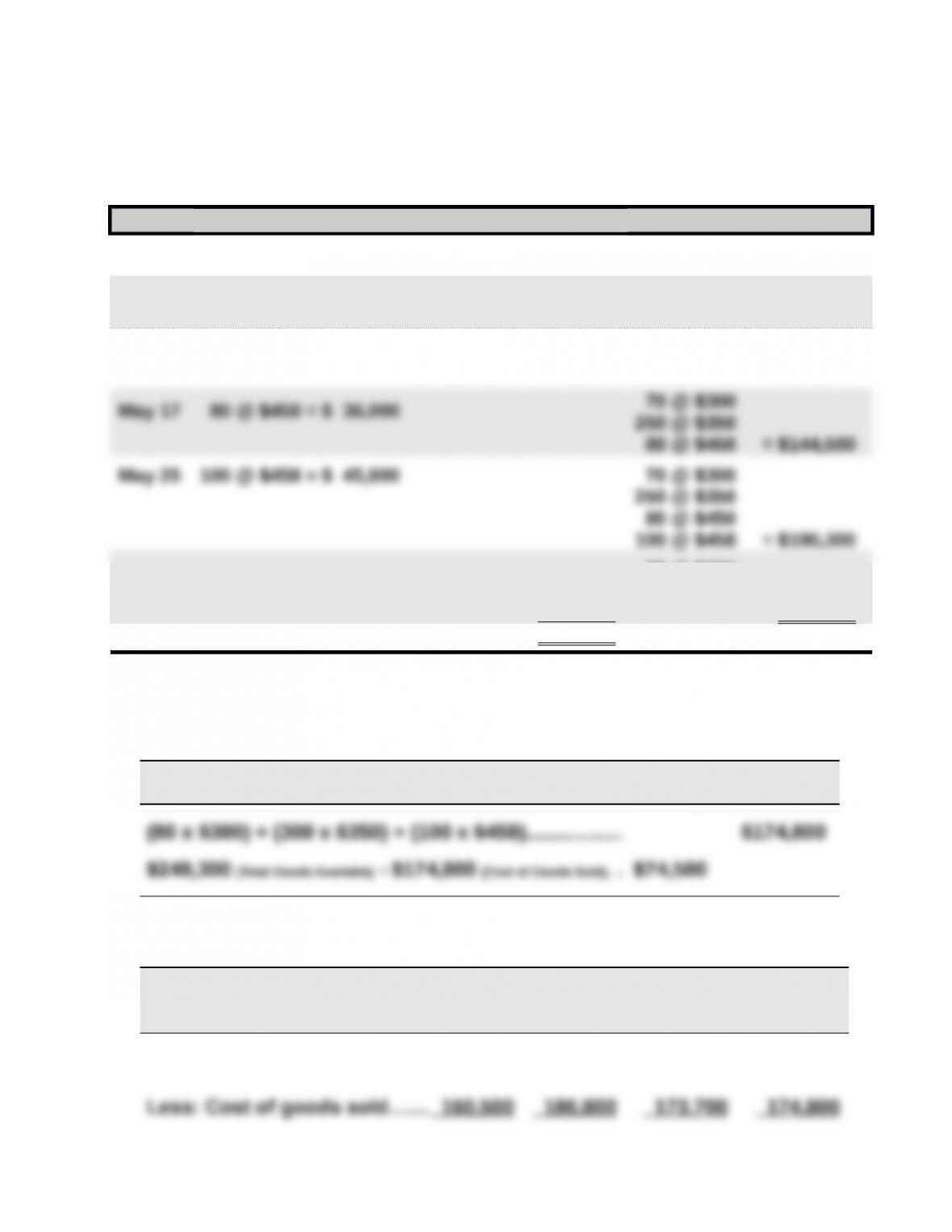

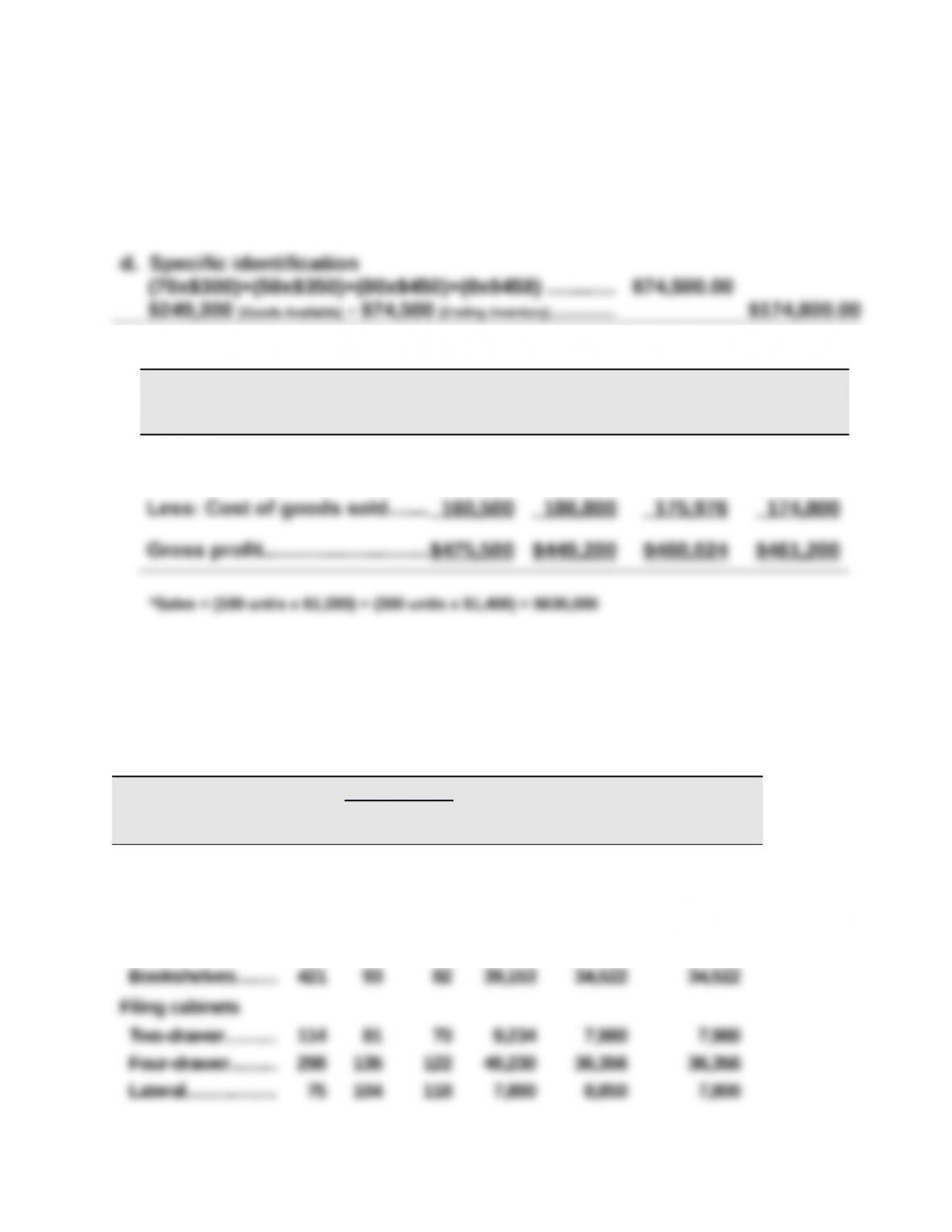

3d. Specific Identification

Date Goods Purchased Cost of Goods Sold Inventory Balance

May 1 150 @ $300 = $ 45,000

May 6 350 @ $350 = $122,500 150 @ $300

350 @ $350 = $167,500

May 9 80 @ $300 = $ 24,000

100 @ $350 = $ 35,000

70 @ $300

250 @ $350 = $108,500

May 30 200 @ $350 = $ 70,000

100 @ $458 = $ 45,800

70 @ $300

50 @ $350

80 @ $450 = $ 74,500

$174,800

Specific identification—Alternative Computation

Cost of goods sold—80 units from beginning inventory, 300 [100+200] units from May

6 purchase, and 100 units from May 25 purchase

Ending Cost of

Specific Identification Inventory Goods Sold

Problem 6-3B (Continued)

4.

FIFO LIFO

Weighted

Average

Specific

Identifi-

cation

Sales*…………………………………$636,000 $636,000 $636,000 $636,000

5. The manager of Aloha Company likely will prefer the FIFO method

Problem 6-4B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory……..……………….. 150 units @ $300 $ 45,000

May 6……………………………….…………… 350 units @ $350 122,500

2. Units in ending inventory

Units available (from part 1)………….……………680 units

Problem 6-4B (Concluded)

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(100 x $458.00) + (80 x $450.00) + (20 x $350.00). . $88,800.00

(150 x $300.00) + (330 x $350.00)…………….………… $160,500.00

c. Weighted average ($249,300/680=$366.62 [rounded])

(200 x $366.62)………………………………………………… $73,324.00

$249,300 [Goods Available] – $73,324 [Ending Inventory]........... $175,976.00

4.

FIFO LIFO

Weighted

Average

Specific

Identifi-

cation

Sales*…………………………………$636,000 $636,000 $636,000 $636,000

5. The manager likely will prefer the FIFO method because it would yield

the largest gross profit (in this period of rising costs). This would give

the manager the highest bonus based on gross profit.

Problem 6-5B (50 minutes)

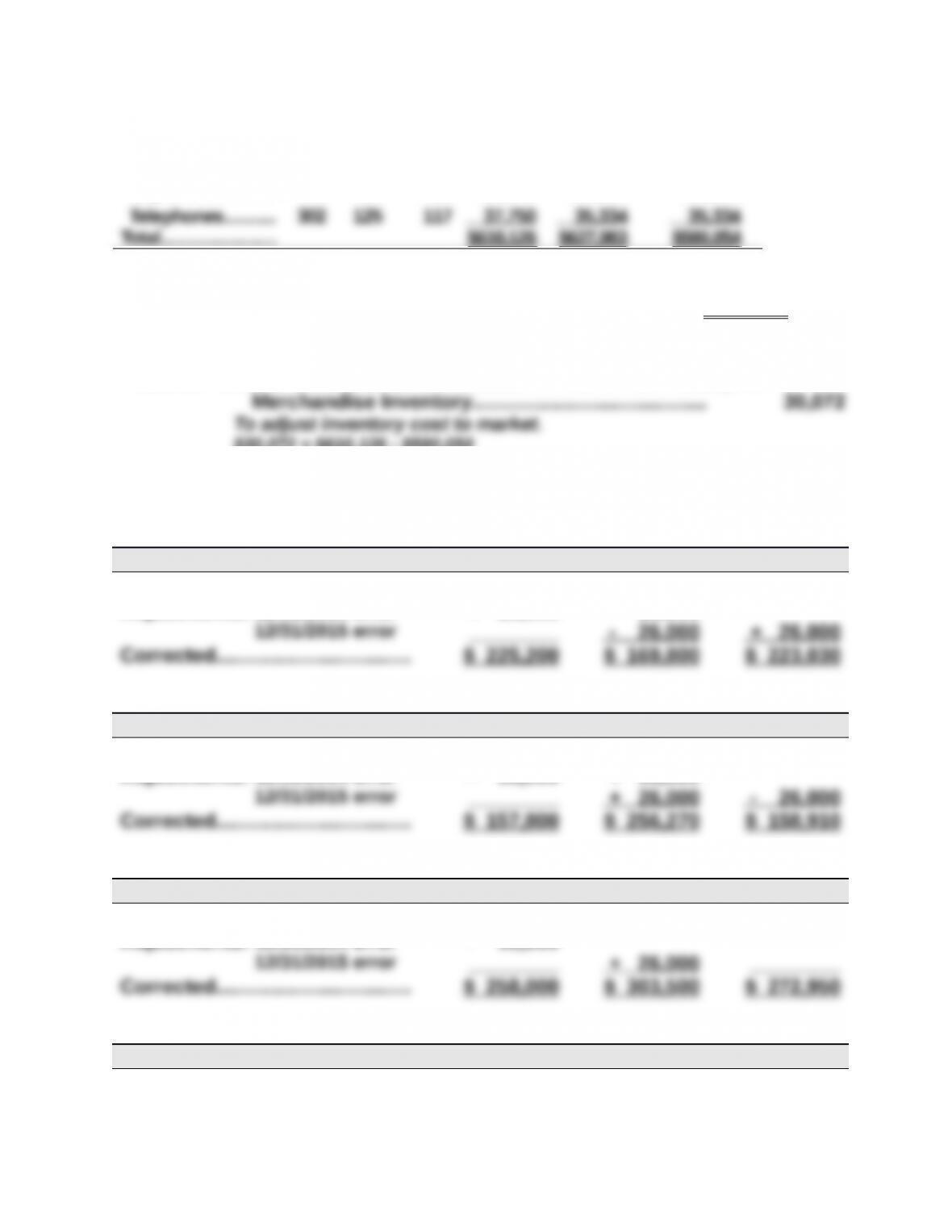

Per Unit Total Total LCM Applied

Inventory Items Units Cos

t

Market Cost Market to Items

Office furniture

Desks……..…....... 536 $261 $305 $139,896 $163,480 $139,896

Credenzas…........ 395 227 256 89,665 101,120 89,665

Chairs……………... 687 49 43 33,663 29,541 29,541

Office equipment

Fax machines...... 370 168 200 62,160 74,000 62,160

Copiers………….... 475 317 288 150,575 136,800 136,800

Corrected………..…………………………. $ 296,000 $ 341,000 $ 346,000

Part 2

Total net income for the combined three-year period ($572,980) is not affected by

understatement (or overstatement) in the following year.

Part 3

The overstatement of inventory by $18,000 results in an understatement of cost of

goods sold by that same amount. The $18,000 understatement of cost of goods

Problem 6-7BA (25 minutes)

Part 1

Number and total cost of units available for sale

6,500 units in beginning inventory @ $35….……………………. $ 227,500

11,500 units purchased @ $33…………………………………….……. 379,500

b. LIFO periodic

Total cost of 50,000 units available for sale….... $1,560,000

Less ending inventory on a LIFO basis

c. Weighted average periodic

Total cost of 50,000 units available for sale….... $1,560,000

Less ending inventory at weighted average cost