Problem 6-3A (Continued)

3c. Weighted Average

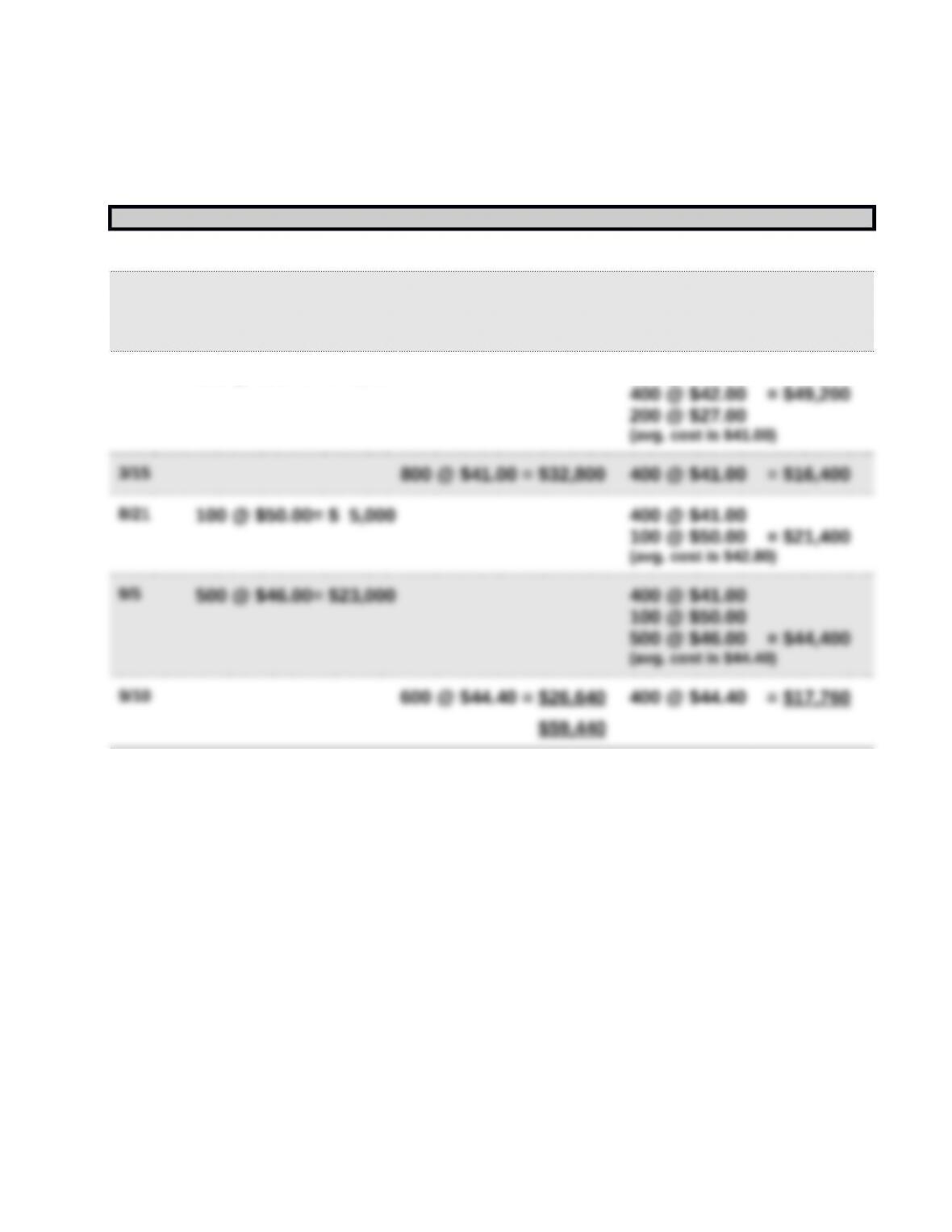

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 600 @ $45.00 = $27,000

2/10 400 @ $42.00= $16,800 600 @ $45.00

400 @ $42.00 = $43,800

(avg. cost is $43.80)

3/13 200 @ $27.00= $ 5,400 600 @ $45.00

Problem 6-3A (Continued)

3d. Specific Identification

Cost of goods available for sale………………. $77,200

Less: Cost of Goods Sold

600 @ $45.00………………………………. $27,000

Proof of Ending Inventory

100 @ $42 $ 4,200

4.

FIFO LIFO

Specific

Identifi-c

ation

Weighted

Average

Sales (1,400 x $75)……………..$105,000 $105,000 $105,000 $105,000

5. Montoure’s manager would likely prefer the FIFO method since this

Problem 6-4A (40 minutes)

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory……………………… 600 units @ $45.00 $27,000

Feb. 10………………………………………… 400 units @ $42.00 16,800

2. Units in ending inventory

Units available (from part 1)………………………1,800

Problem 6-4A (Concluded)

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(400 x $46.00)………………………………………………….. $18,400.00

(600x$45.00) + (400x$42.00) + (200x$27.00) +

(100x$50.00) + (100x$46.00)………………………………

$58,800.00

b. LIFO

4.

FIFO LIFO

Specific

Identifi-c

ation

Weighted

Average

5. The manager would likely prefer the FIFO method since this methods’

Problem 6-5A (50 minutes)

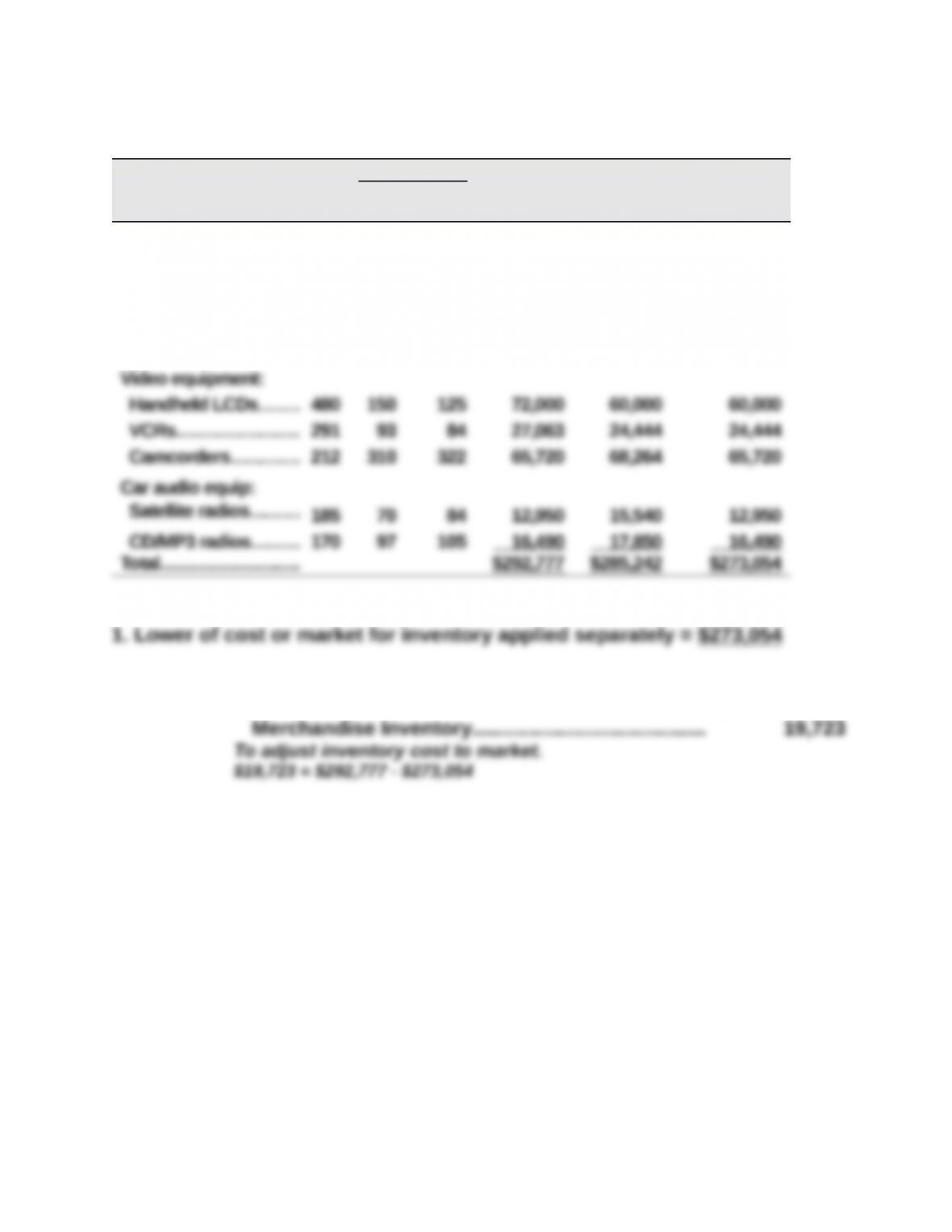

Per Unit Total Total LCM Applied

to Items

Inventory Items Unit

s Cost Market Cost Market

Audio equipment:

Receivers……………. 345 $ 90 $ 98 $ 31,050 $ 33,810 $ 31,050

CD players…………… 260 111 100 28,860 26,000 26,000

MP3 players…………. 326 86 95 28,036 30,970 28,036

Speakers…………….. 204 52 41 10,608 8,364 8,364

2.

Dec 31 Cost of Goods Sold…………………………………………….19,723

Problem 6-6A (35 minutes)

Part 1

(a)

Cost of goods sold 2014 2015 2016

Reported……………………………….. $ 615,000 $ 957,000 $ 780,000

(b)

Net income 2014 2015 2016

Reported……………………………….. $ 230,000 $ 285,000 $ 241,000

(c)

Total current assets 2014 2015 2016

Reported……………………………….. $1,255,000 $1,365,000 $1,200,000

(d)

Equity 2014 2015 2016

Reported……………………………….. $1,387,000 $1,530,000 $1,242,000

Part 2

Total net income for the combined three-year period ($756,000) is not affected

Part 3

The understatement of inventory by $56,000 results in an overstatement of cost of

Problem 6-7AA (25 minutes)

Part 1

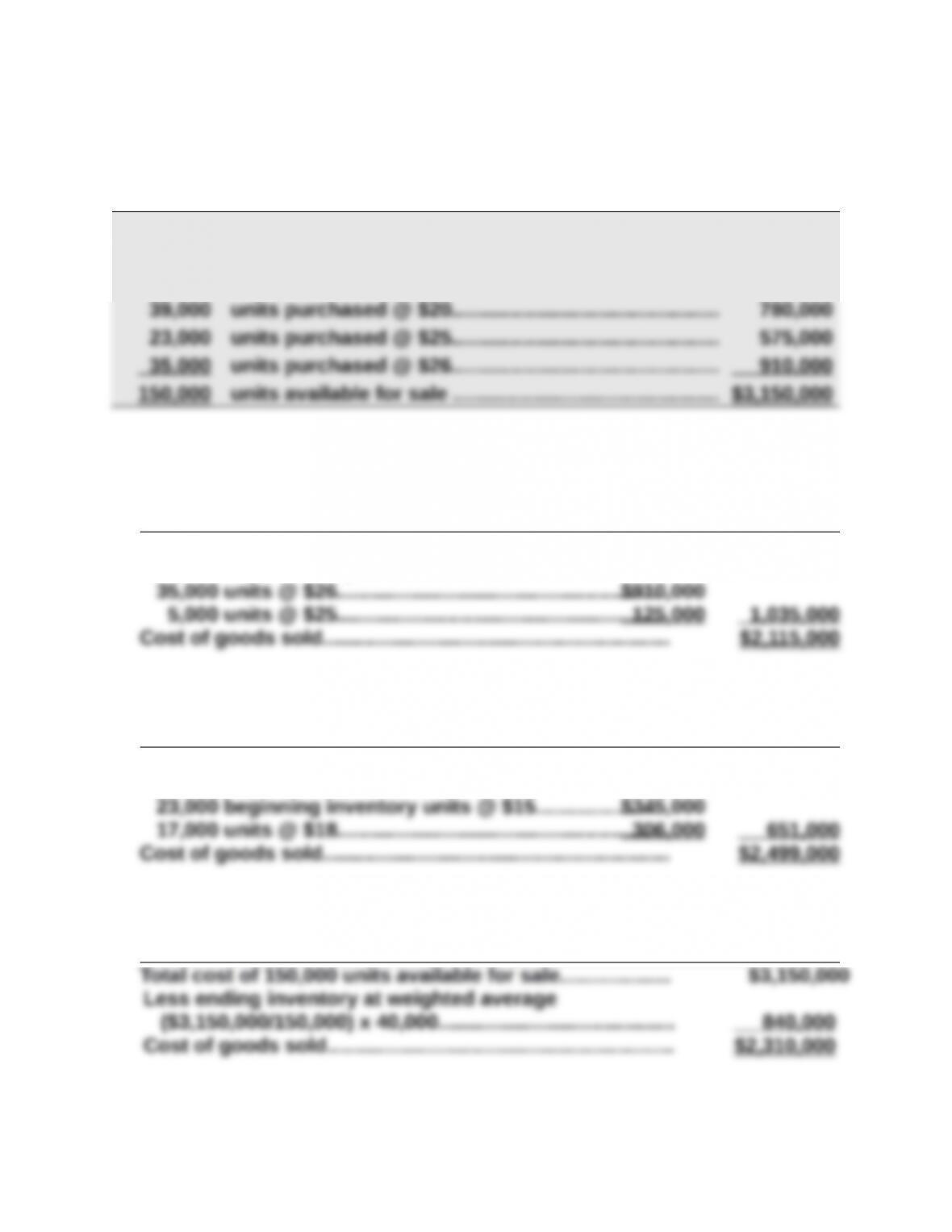

Number and total cost of units available for sale

23,000 units in beginning inventory @ $15…………………….. $ 345,000

30,000 units purchased @ $18………………………………………. 540,000

Part 2

a. FIFO periodic

Total cost of 150,000 units available for sale………………. $3,150,000

Less ending inventory on a FIFO basis

b. LIFO periodic

Total cost of 150,000 units available for sale………………. $3,150,000

Less ending inventory on a LIFO basis

c. Weighted average periodic

Problem 6-8AA (50 minutes)

Part 1

QP CORP.

Income Statements Comparing FIFO, LIFO, and Weighted Average

For Year Ended December 31, 2015

FIFO LIFO

Weighted

Average

Sales…………………………………………………….$200,000 $200,000 $200,000

Cost of goods sold

Inventory, Dec. 31, 2014……………………….. 12,600 12,600 12,600

Cost of purchases……………………………….. 109,400 109,400 109,400

Supporting calculations FIFO LIFO

Weighted

Average

Dec. 31, 2014, inventory (700 x $18)………………. $ 12,600 $ 12,600 $ 12,600

Purchases

1,700 x $19 = $32,300

Problem 6-8AA (Concluded)

Part 2

If QP Corp. had been experiencing declining costs in the acquisition of

Part 3

Advantages

LIFO: Given the cost trends in the problem, the advantage of using LIFO is

Disadvantages

LIFO: Given the cost trends in the problem, the disadvantage of using LIFO