Problem 6-3A (Continued)

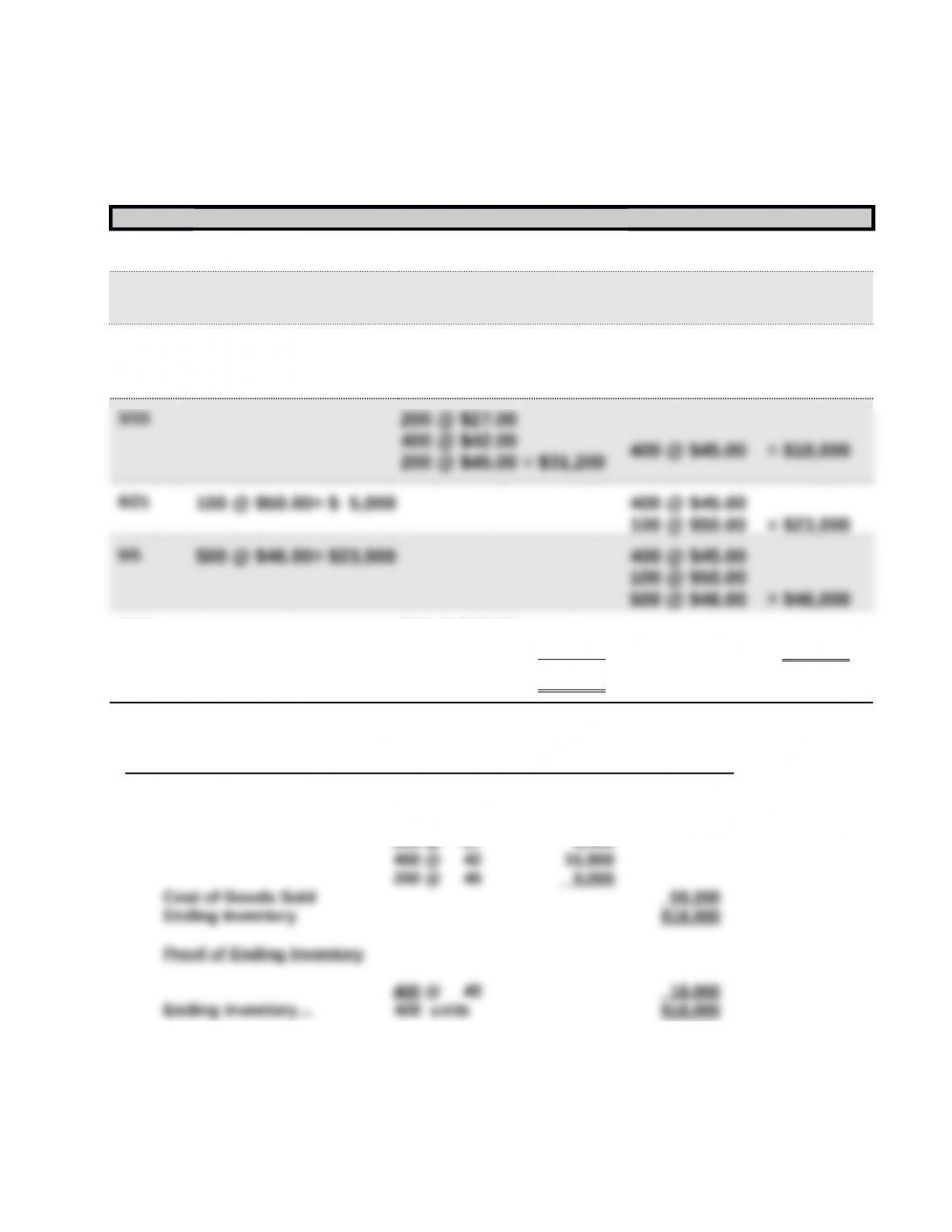

3b. LIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 600 @ $45.00 = $27,000

2/10 400 @ $42.00= $16,800 600 @ $45.00

400 @ $42.00 = $43,800

3/13 200 @ $27.00= $ 5,400 600 @ $45.00

400 @ $42.00 = $49,200

200 @ $27.00

9/10 500 @ $46.00

100 @ $50.00 = $28,000 400 @ $45.00 = $18,000

$59,200

LIFO alternate solution format

Cost of goods available for sale $77,200

Less: Cost of sales 500 @ $46 $23,000

100 @ 50 5,000

200 @ 27 5,400

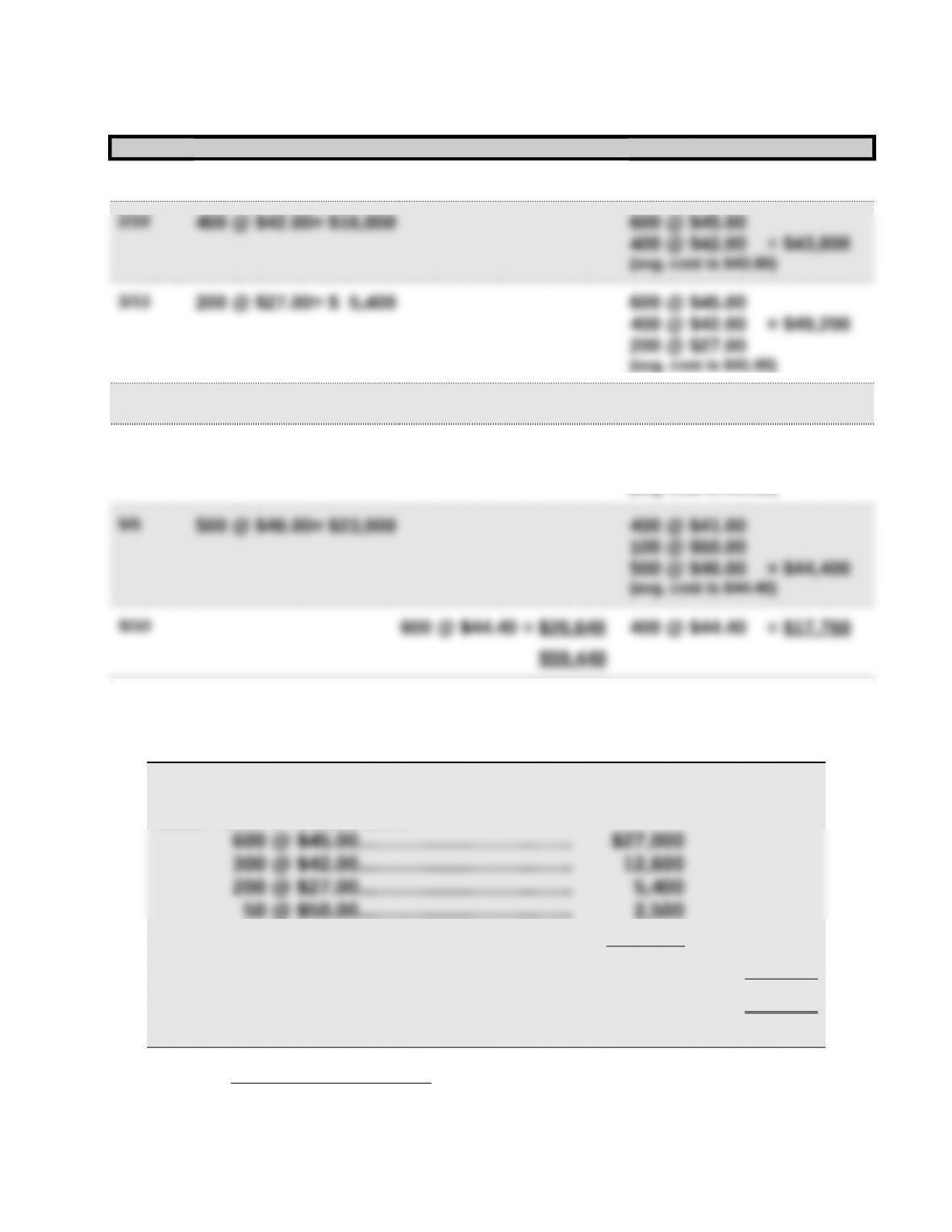

Problem 6-3A (Continued)

3c. Weighted Average

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 600 @ $45.00 = $27,000

3/15 800 @ $41.00 = $32,800 400 @ $41.00 = $16,400

8/21 100 @ $50.00= $ 5,000 400 @ $41.00

100 @ $50.00 = $21,400

(avg. cost is $42.80)

Problem 6-3A (Continued)

3d. Specific Identification

Cost of goods available for sale……………..… $77,200

Less: Cost of Goods Sold

250 @ $46.00…………………………….…. 11,500

Total cost of goods sold…………………………... 59,000

Ending Inventory……………………………………… $18,200

Proof of Ending Inventory

100 @ $42 $ 4,200

50 @ $50 $ 2,500

250 @ $46 11,500

Ending Inventory…. 400 units $18,200

4.

FIFO LIFO

Specific

Identifi-

cation

Weighted

Average

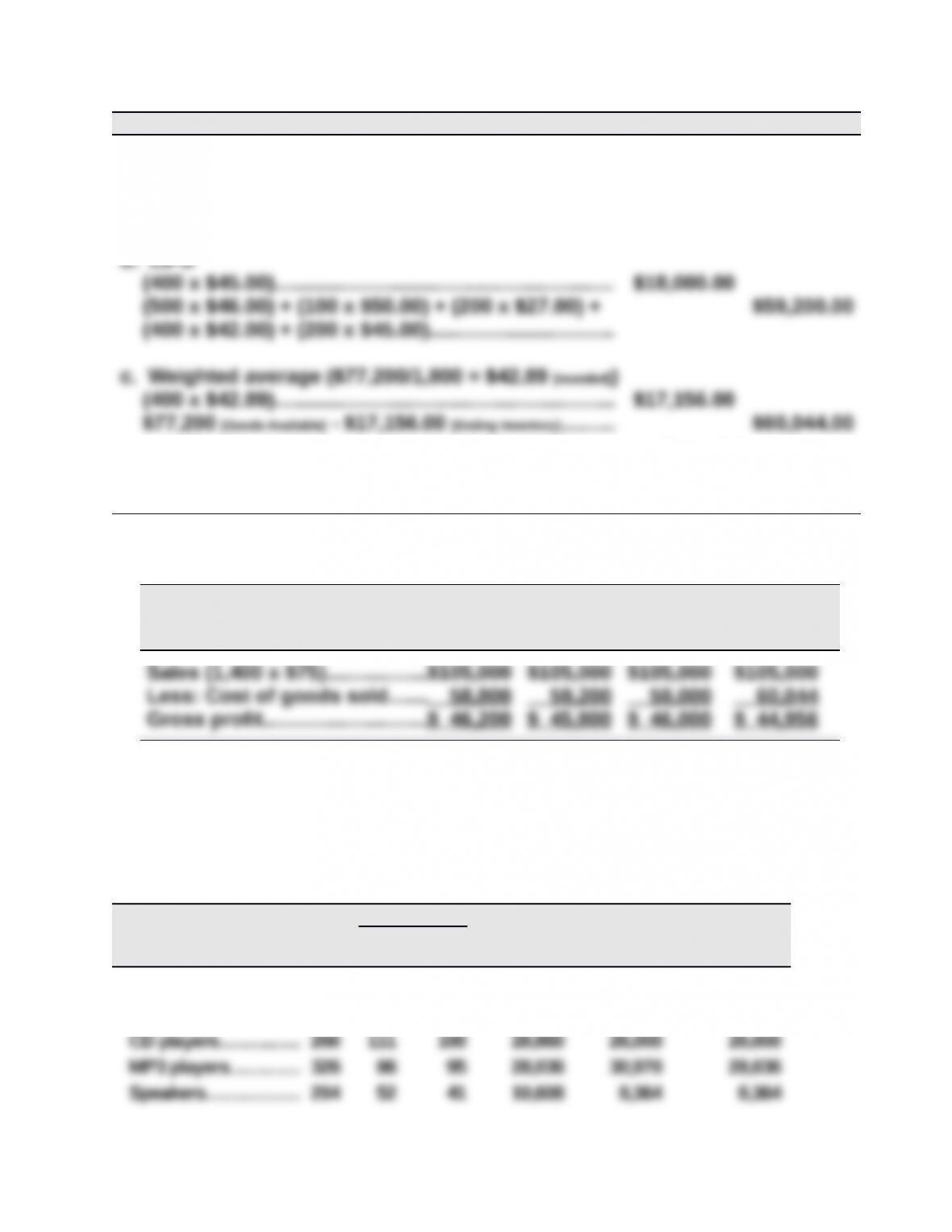

5. Montoure’s manager would likely prefer the FIFO method since this

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory……..….….…….….. 600 units @ $45.00 $27,000

Feb. 10………………………………………….. 400 units @ $42.00 16,800

2. Units in ending inventory

Units available (from part 1)………….…….……..1,800

3.

Ending Cost of

Periodic Inventory Inventory Goods Sold

a. FIFO

(400 x $46.00)……………………..….….…….…….…….….. $18,400.00

(600x$45.00) + (400x$42.00) + (200x$27.00) +

(100x$50.00) + (100x$46.00)……………………….……...

$58,800.00

d. Specific identification

(100 x $42.00) + (50 x $50.00) + (250 x $46.00)....... $18,200.00

$77,200 [Goods Available] – $18,200.00 [Ending Inventory]......... $59,000.00

4.

FIFO LIFO

Specific

Identifi-

cation

Weighted

Average

5. The manager would likely prefer the FIFO method since this methods’

gross profit is the largest at $46,200. This would give the manager the

highest bonus based on gross profit.

Problem 6-5A (50 minutes)

Per Unit Total Total LCM Applied

to Items

Inventory Items Unit

s Cost Market Cost Market

Audio equipment:

Receivers…..………... 345 $ 90 $ 98 $ 31,050 $ 33,810 $ 31,050

Video equipment:

Handheld LCDs…….. 480 150 125 72,000 60,000 60,000

Equity 2014 2015 2016

Reported………………………………… $1,387,000 $1,530,000 $1,242,000

Adjustments: 12/31/2014 error……. + 56,000

Part 2

Total net income for the combined three-year period ($756,000) is not affected

Part 3

The understatement of inventory by $56,000 results in an overstatement of cost of

goods sold by that same amount. The $56,000 overstatement of cost of goods

Problem 6-7AA (25 minutes)

Part 1

Number and total cost of units available for sale

23,000 units in beginning inventory @ $15…..…….….…….…. $ 345,000

30,000 units purchased @ $18………………………………………… 540,000

150,000 units available for sale ………………..….….…….…….….. $3,150,000

Part 2

a. FIFO periodic

Total cost of 150,000 units available for sale……………….. $3,150,000

Less ending inventory on a FIFO basis

b. LIFO periodic

Total cost of 150,000 units available for sale……………….. $3,150,000

Less ending inventory on a LIFO basis

c. Weighted average periodic

Total cost of 150,000 units available for sale……………….. $3,150,000

Less ending inventory at weighted average

Problem 6-8AA (50 minutes)

Part 1

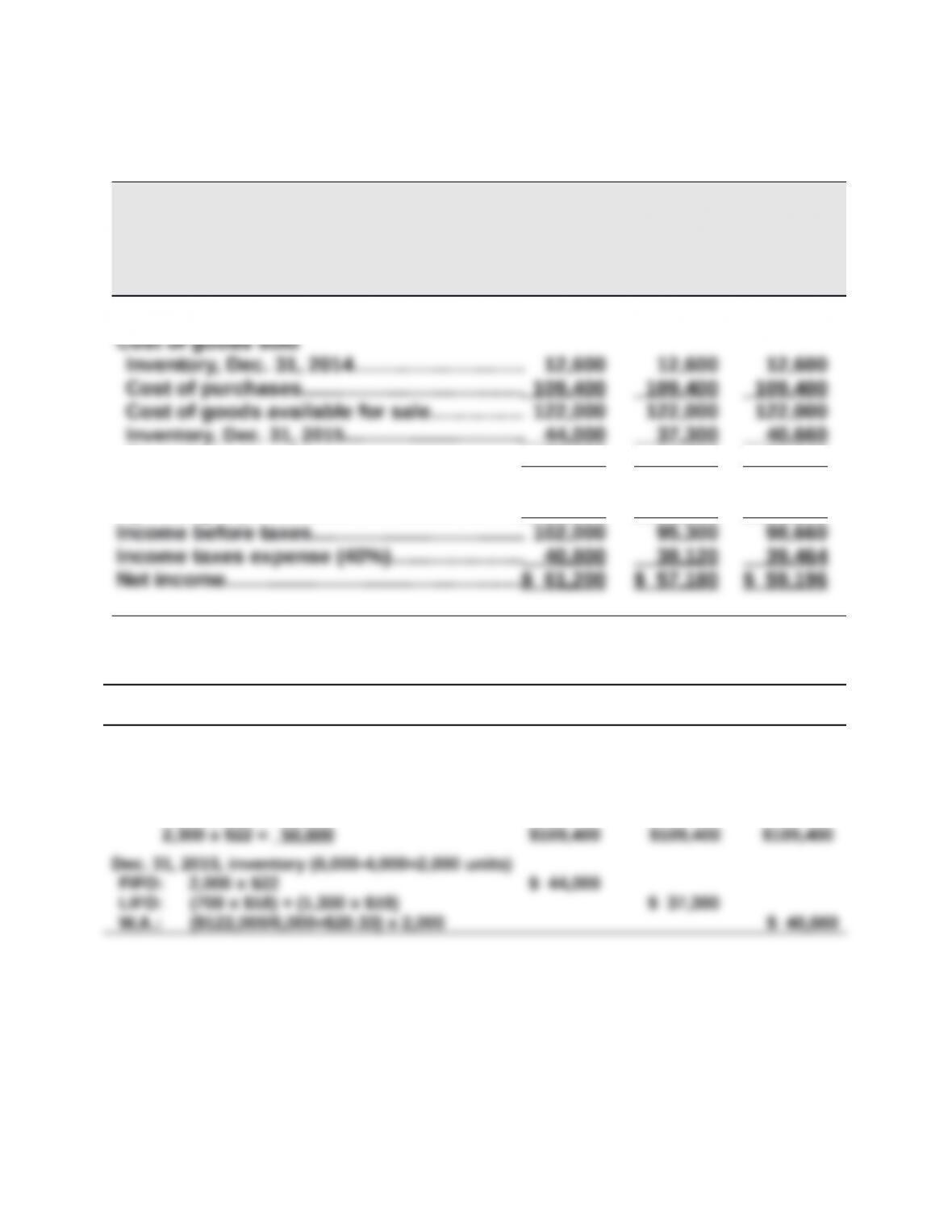

QP CORP.

Income Statements Comparing FIFO, LIFO, and Weighted Average

For Year Ended December 31, 2015

FIFO LIFO

Weighted

Average

Sales……………………………………………….……..$200,000 $200,000 $200,000

Cost of goods sold……………….…….…….….. 78,000 84,700 81,340

Gross profit……………………………………..….…. 122,000 115,300 118,660

Operating expenses…………………….…….…… 20,000 20,000 20,000

Supporting calculations FIFO LIFO

Weighted

Average

Dec. 31, 2014, inventory (700 x $18)………….…... $ 12,600 $ 12,600 $ 12,600

Purchases

1,700 x $19 = $32,300

800 x $20 = 16,000

500 x $21 = 10,500

Problem 6-8AA (Concluded)

Part 2

If QP Corp. had been experiencing declining costs in the acquisition of

inventory, we would observe the opposite results in our comparisons.

gross profit, and lower net income.

Part 3

Advantages

LIFO: Given the cost trends in the problem, the advantage of using LIFO is

that the lower net income will result in a lower tax obligation (tax deferral).

Disadvantages

LIFO: Given the cost trends in the problem, the disadvantage of using LIFO