Exercise 6-13 (20 minutes)

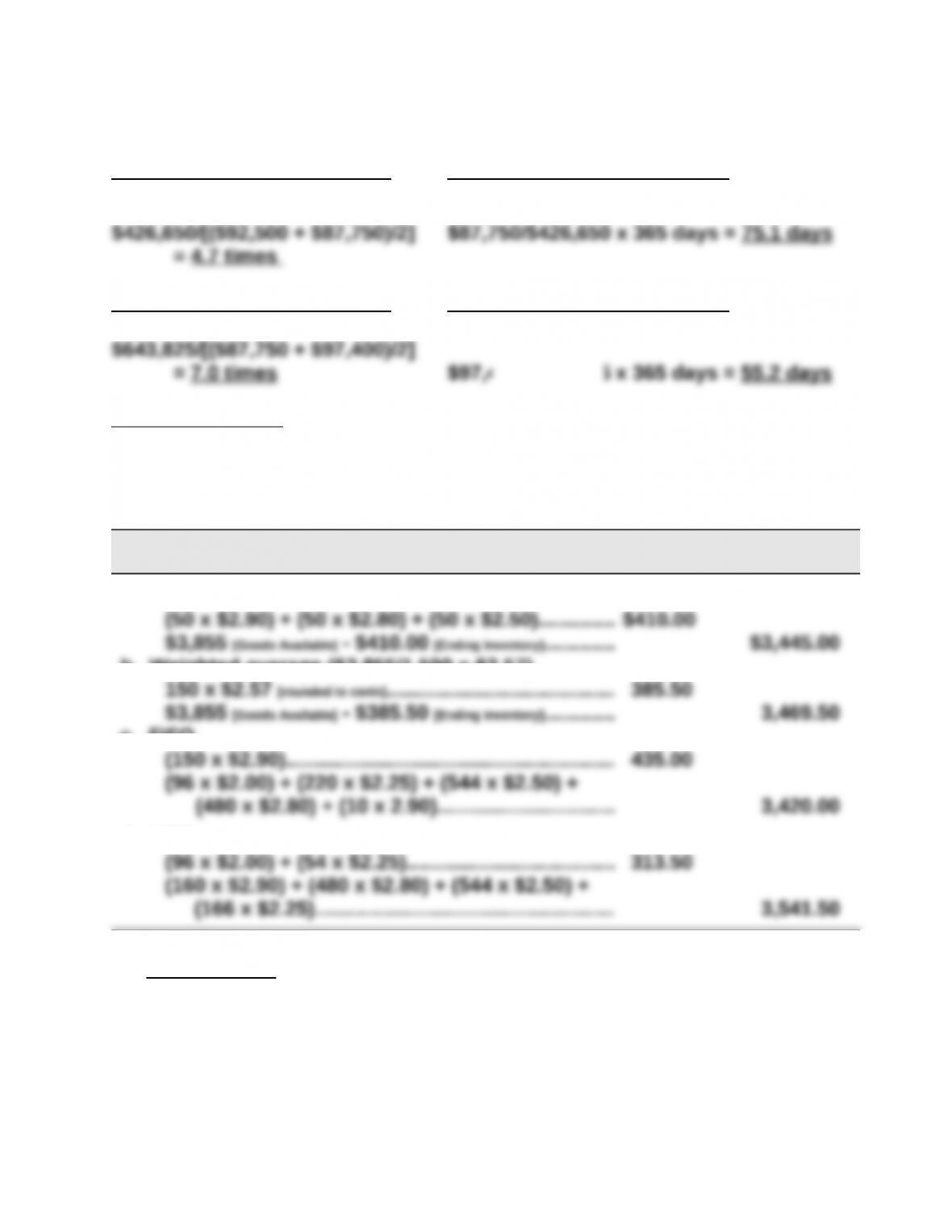

2014 Inventory turnover 2014 Days’ Sales in Inventory

2015 Inventory turnover 2015 Days’ Sales in Inventory

Analysis comment: It appears that during a period of increasing sales, Palmer

has been efficient in controlling its amount of inventory. Specifically, inventory

turnover increased by 2.3 times (7.0 – 4.7) from 2014 to 2015. In addition, days’

sales in inventory decreased by 19.9 days (75.1 – 55.2).

Exercise 6-14A (20 minutes)

Ending

Inventory

Cost of

Goods Sold

a. Specific identification

b. Weighted average ($3,855/1,500 = $2.57)

c. FIFO

d. LIFO

Income effect: FIFO provides the lowest cost of goods sold, the highest

gross profit, and the highest net income, which is not unexpected

during a period of rising costs.

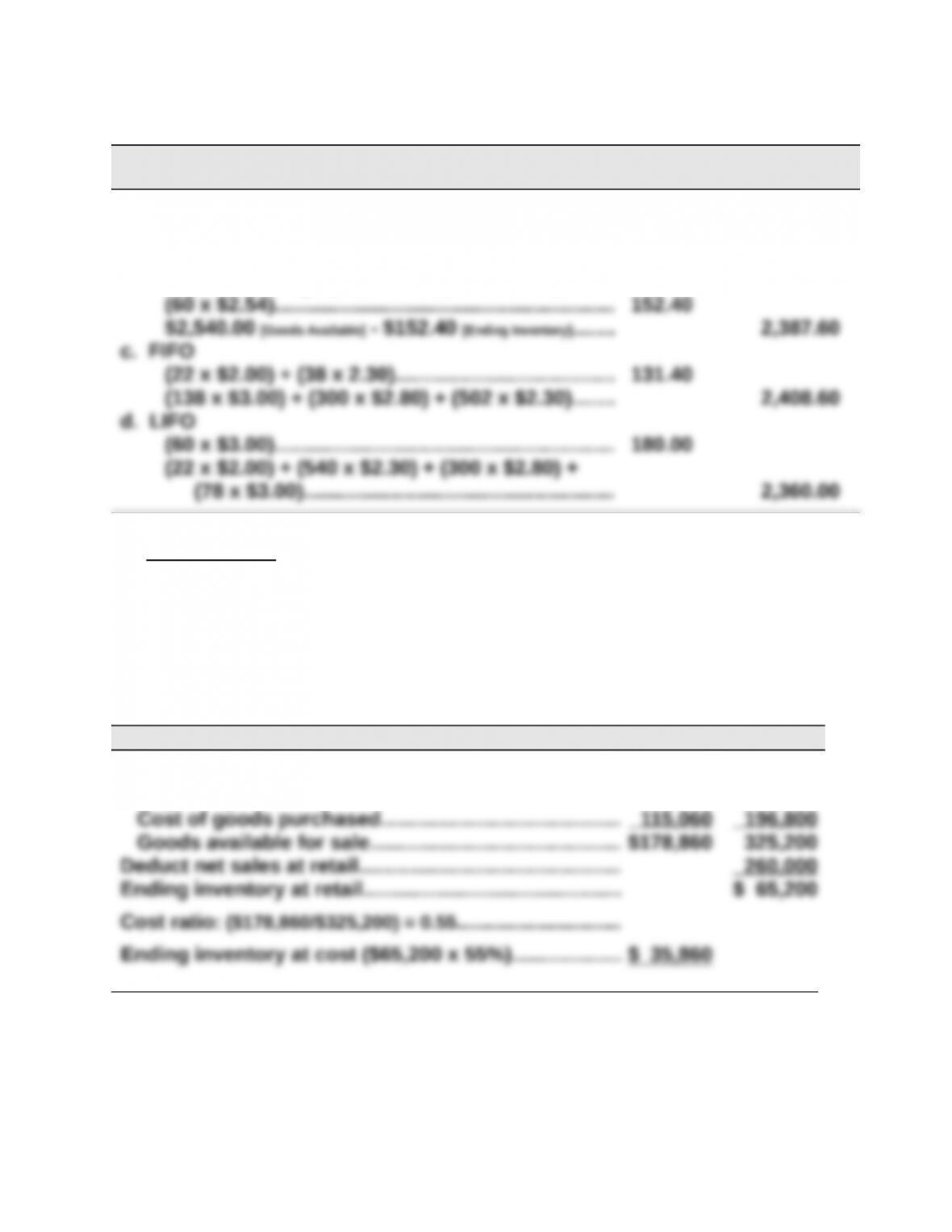

Exercise 6-15A (20 minutes)

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. Specific Identification

(50 x $2.80) + (10 x $2.00)……………………………… $160.00

$2,540.00 [Goods Available] – $160.00 [Ending Inventory]……. $2,380.00

b. Weighted Average ($2,540.00/1,000 = $2.54)

Income effect: LIFO provides the lowest cost of goods sold, the highest

gross profit, and the highest net income, which is not unexpected

during a period of declining costs.

Exercise 6-16B (20 minutes)

At Cost At Retail

Goods available for sale

Beginning inventory………………………………………….. $ 63,800 $128,400

Exercise 6-17B (20 minutes)

Goods available for sale

Inventory, January 1…………………………………………….. $ 225,000

* $795,000 – $11,550 + $18,800 = $802,250

Exercise 6-18 (15 minutes)

1. Samsung generally applies the (weighted) average cost assumption when

2. Under IFRS, Samsung would reverse inventory valuation losses if

inventory values increased in subsequent periods. Specifically, it would

PROBLEM SET A

Problem 6-1A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory………………………100 units @ $50.00 $ 5,000

March 5………………………………………..400 units @ $55.00 22,000

2. Units in ending inventory

Units available (from part 1)………………………820 units

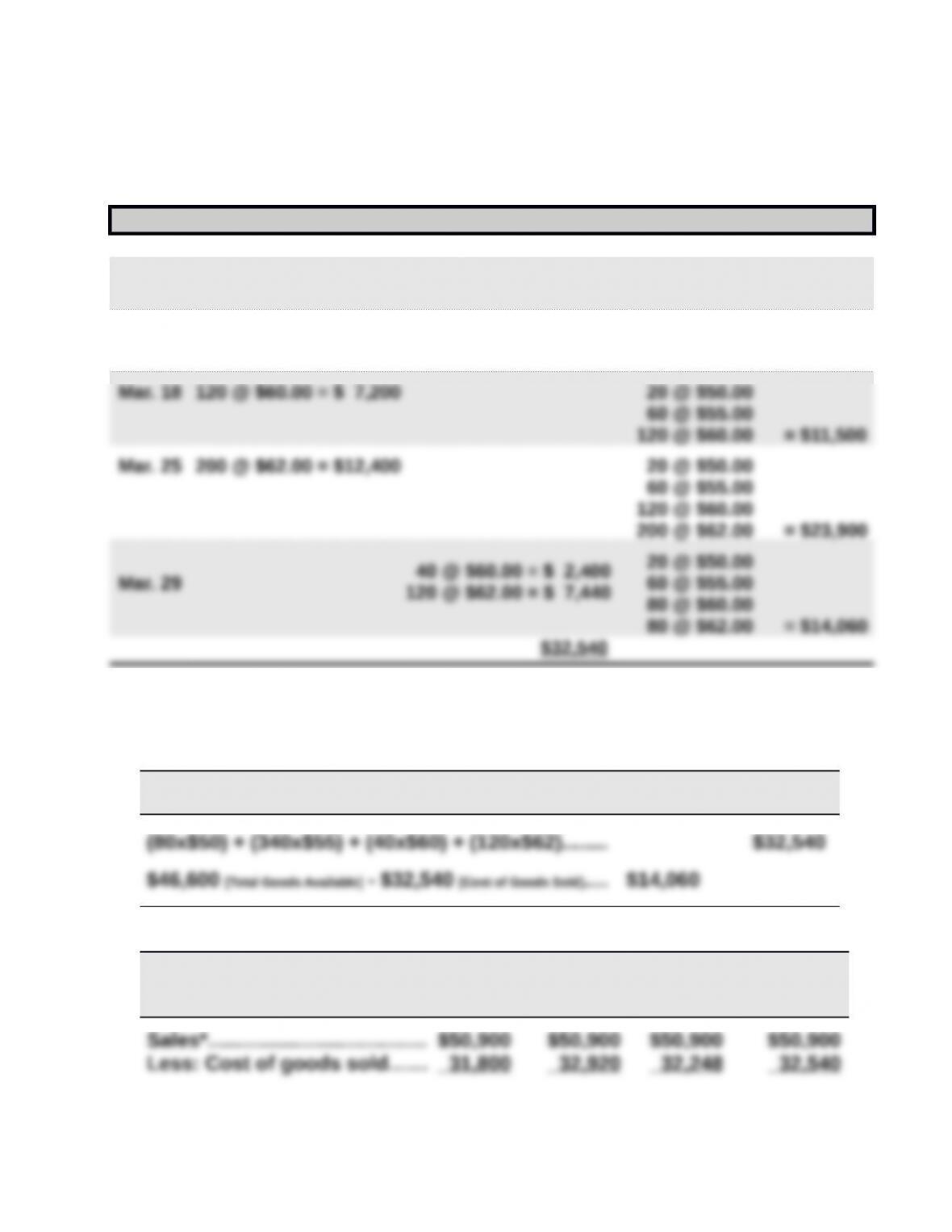

3a. FIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Mar. 1 100 @ $50.00 = $5,000

Mar. 5 400 @ $55.00 = $22,000 100 @ $50.00

Problem 6-1A (Continued)

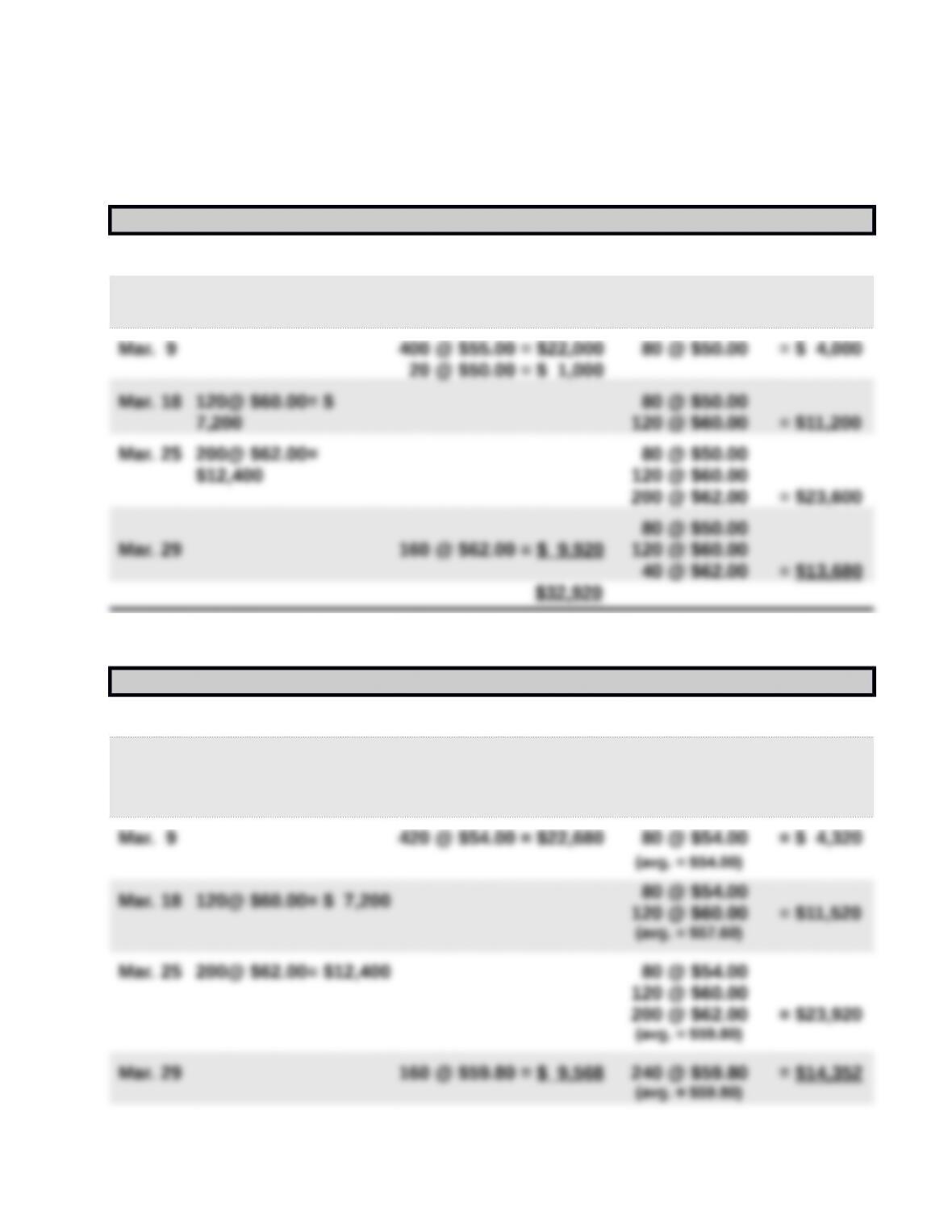

3b. LIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Mar. 1 100 @ $50.00 = $ 5,000

Mar. 5 400@ $55.00=

$22,000

100 @ $50.00

400 @ $55.00 = $27,000

3c. Weighted Average perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Mar. 1 100 @ $50.00 = $ 5,000

Mar. 5 400@ $55.00= $22,000 100 @ $50.00

400 @ $55.00 = $27,000

(avg. = $54.00)

Problem 6-1A (Concluded)

3d. Specific Identification

Date Goods Purchased Cost of Goods Sold Inventory Balance

Mar. 1 100 @ $50.00 = $ 5,000

Mar. 5 400 @ $55.00 = $22,000 100 @ $50.00

400 @ $55.00 = $27,000

Mar. 9 80 @ $50.00 = $ 4,000

340 @ $55.00 = $18,700

20 @ $50.00

60 @ $55.00 = $ 4,300

Specific identification—Alternative Computation

Cost of goods sold—80 units from beginning inventory, 340 units from March 5

purchase, 40 units from March 18 purchase, and 120 units from March 25 purchase

Ending Cost of

Specific Identification Inventory Goods Sold

4.

FIFO LIFO

Weighted

Average

Specific

Identifi-ca

tion

Problem 6-2A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory………………………100 units @ $50.00 $ 5,000

March 5………………………………………..400 units @ $55.00 22,000

2. Units in ending inventory

Units available (from part 1)………………………820 units

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(200 x $62.00) + (40 x $60.00)………………………… $14,800.00

(100 x $50.00) + (400 x $55.00) + (80 x $60.00)… $31,800.00

b. LIFO

Problem 6-2A (Concluded)

4.

FIFO LIFO

Weighted

Average

Specific

Identifi-cat

ion

Sales*………………………………..$50,900.00 $50,900.00 $50,900.00 $50,900.00

*Sales = (420 units x $85.00) + (160 units x $95.00) = $50,900

Problem 6-3A (40 minutes)

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory……………………… 600 units @ $45.00 $27,000

Feb. 10………………………………………… 400 units @ $42.00 16,800

2. Units in ending inventory

Units available (from part 1)………………………1,800

Problem 6-3A (Continued)

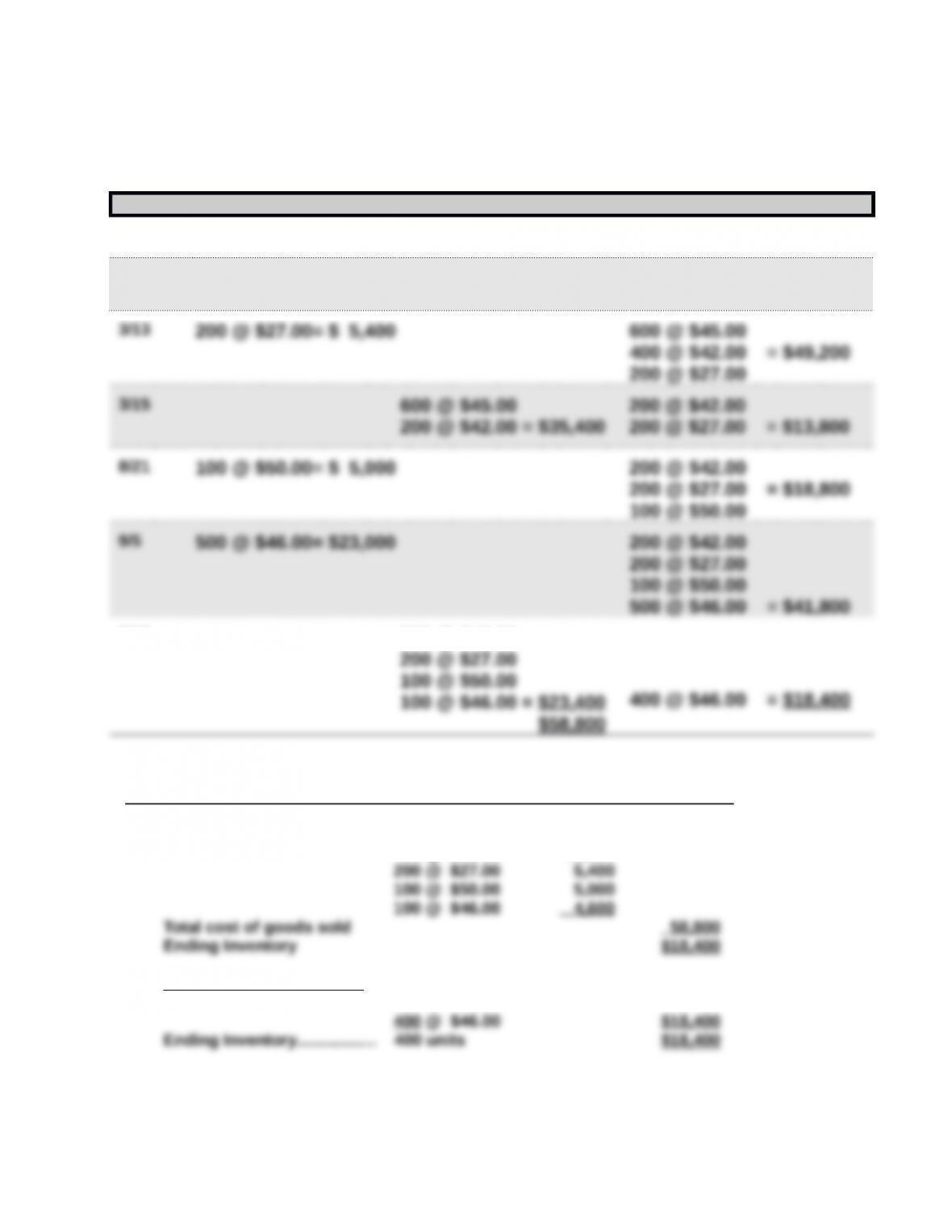

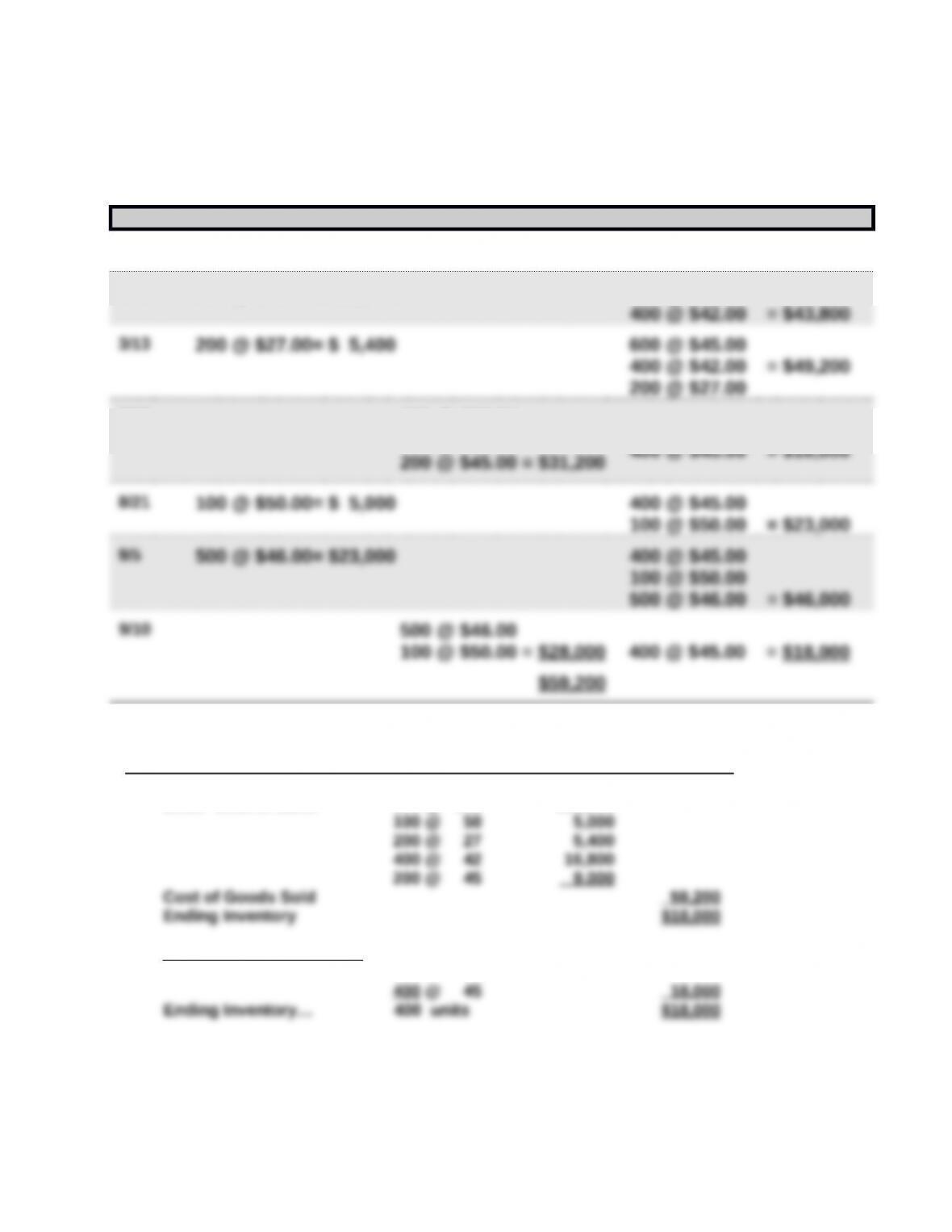

3a. FIFO perpetual

Date Goods Purchasd Cost of Goods Sold Inventory Balance

1/1 600 @ $45.00 = $27,000

2/10 400 @ $42.00= $16,800 600 @ $45.00

400 @ $42.00 = $43,800

9/10 200 @ $42.00

FIFO Alternate Solution Format

Cost of goods available for sale $77,200

Less: Cost of sales 600 @ $45.00 $27,000

400 @ $42.00 16,800

Proof of Ending Inventory

Problem 6-3A (Continued)

3b. LIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 600 @ $45.00 = $27,000

2/10 400 @ $42.00= $16,800 600 @ $45.00

3/15 200 @ $27.00

400 @ $42.00

LIFO alternate solution format

Cost of goods available for sale $77,200

Less: Cost of sales 500 @ $46 $23,000

Proof of Ending Inventory