EXERCISES

Exercise 5-1 (30 minutes)

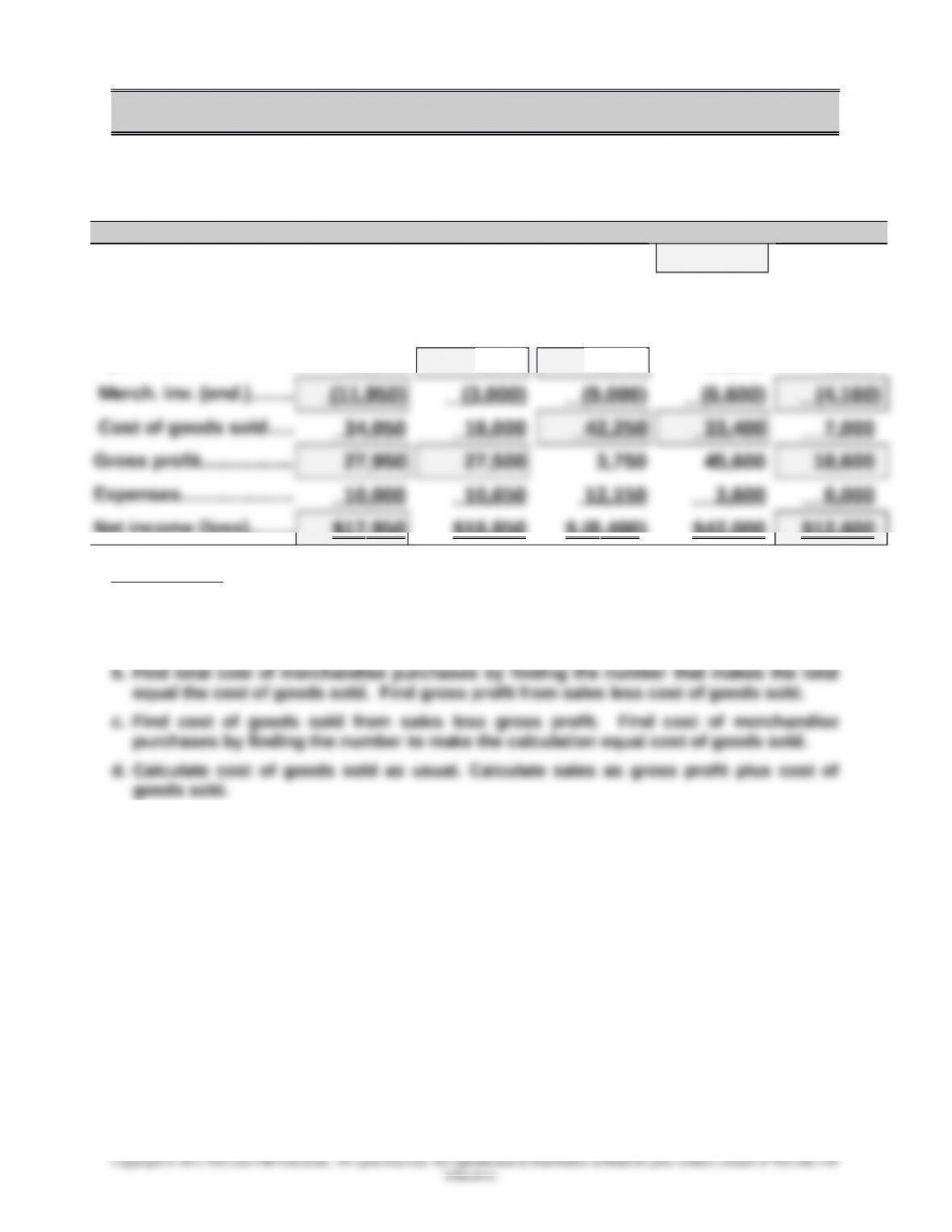

Note: The original missing numbers are blocked.

(a) (b) (c) (d) (e)

Sales……….………..….…. $62,000 $43,500 $46,000 $79,000 $25,600

Cost of goods sold

Merch. inv. (beg.)…..... 8,000 17,050 7,500 8,000 4,560

Total cost of merch.

purchases….….......... 38,000 1,950 43,750 32,000 6,600

Net income (loss)........ $17 ,950 $16 ,850 $ (8 ,400) $42 ,000 $12,600

Explanations:

a. Find merchandise inventory (ending) by subtracting cost of goods sold from goods

available for sale. Find gross profit as the difference between the sales and cost of

goods sold. Find net income as the gross profit less the expenses.

e. Find merchandise inventory (ending) by subtracting cost of goods sold from goods

available for sale. Find gross profit from sales less cost of goods sold. Find net

income as gross profit less expenses.

5-291

Exercise 5-2 (10 minutes)

Operating cycle of a merchandiser with credit sales follows (chronological):

2 (a) inventory made available for sale

Exercise 5-3 (20 minutes)

In today’s competitive world, organizations must concentrate on meeting their

customers’ needs and avoiding dissatisfaction. If these needs are not met and

dissatisfaction grows, the customers will deal with other companies or

An important early step in controlling returns is to have information about

their dollar amount. In addition, managers can set goals for reducing the

While a company’s sales return record is important for managers, it is also

valuable information for external decision makers. This information can help

5-292

Exercise 5-4 (30 minutes)

Apr. 2 Merchandise Inventory……………………………….. 4,600

Accounts Payable—Lyon….……………….... 4,600

Purchased merchandise on credit.

18 Merchandise Inventory …………………………….… 8,500

Accounts Payable—Frist………….………….. 8,500

Purchased merchandise on credit.

21 Accounts Payable—Frist….………………………... 1,100

Merchandise Inventory ……………………….. 1,100

Received an allowance on purchase.

5-293

Exercise 5-5 (30 minutes)

May 5 Accounts Receivable ……………………………….... 21,000

Sales ………………………………………………….. 21,000

Sold merchandise on credit (1,500 x $14).

b.

May 8 Sales Returns and Allowances……………………. 600

Accounts Receivable………..…………………. 600

Granted allowance for damaged merchandise.

5-294

Exercise 5-6 (15 minutes)

May 5 Merchandise Inventory……………………………… 21,000

Accounts Payable…………….………………… 21,000

Purchased merchandise on credit (1,500 x $14).

c.

May 15 Accounts Payable……………………………………… 680

Merchandise Inventory……………………….. 680

To record allowance for mis-colored goods and

return of mis-colored merchandise

$120 + (40 x $14).

5-295

Exercise 5-7 (30 minutes)

1. BUYER- Santa Fe Company

a) Credit Purchase

Merchandise Inventory..……………………………. 24,000

Accounts Payable…………….………………… 24,000

Purchased merchandise on credit.

2. SELLER – Mesa Company

a) Credit Sale

Accounts Receivable………………………………… 24,000

Sales………………………………………………….. 24,000

Sold merchandise on account.

Collected account receivable.

3. Amount borrowed to pay with discount……………….….. $ 23,280

Annual rate of interest ……………………………………………. x 8%

Interest per year……………………………………………….…….. $1,862.40

Interest per day ($1,862.40 / 365 days).………………….... $5.10*

5-296

Exercise 5-8 (25 minutes)

1. Entries for Sydney Company (BUYER):

May 11 Merchandise Inventory …………………….……… 40,000

20 Accounts Payable…………..……………………….. 38,600

Merchandise Inventory*…………………….. 1,158

Cash……………………………….………………… 37,442

Paid balance within the 3% discount period.

*($38,600 x .03).

2. Entries for Troy Corporation (SELLER):

May 11 Accounts Receivable……………..……….……….. 40,000

Sales…………………………………………………. 40,000

Sold merchandise on account.

21 Cash………………………………………………………... 37,442

Sales Discounts……………………………………….. 1,158

Accounts Receivable…………………………. 38,600

Collected account receivable.

5-297

Exercise 5-9 (30 minutes)

Merchandise Inventory

Balance, Dec. 31, 2014…........... 25,000 Purchase discounts received……..…………………….……………................................1,700

Balance, Dec. 31, 2015 20,000

Cost of Goods Sold

Cost of sales transactions….….

196,000

Returns by customers and

restored to inventory……………………………………………………..………....................2,100

5-298

Exercise 5-10 (20 minutes)

Perpetual

1)

Nov. 1 Merchandise Inventory……………………………….. 1,500

Accounts Payable……………………………….. 1,500

To record merchandise purchases on credit.

4)

Nov. 10 Merchandise Inventory……………………………….. 90

Cash………………………………………………….… 90

To record payment of freight charges.

Merchandise Inventory……………………………….. 130

Cost of Goods Sold……………………..………. 130

To record return of merchandise to inventory.

Instructor note: This second entry changes if the goods returned are defective. In this

case the returned inventory is recorded at its estimated value, not its cost. To illustrate, if

the goods (costing $130) returned are defective and estimated to be worth, say, $50, the

following entry is made: Dr. Merchandise Inventory for $50, Dr. Loss from Defective

Merchandise for $80, and Cr. Cost of Goods Sold for $130.

5-299

Exercise 5-11 (25 minutes)

Adjusting entries

Dec. 31 Sales Salaries Expense……………………………… 1,700

Salaries Payable…………………………..….…. 1,700

To record accrued salaries.

($30,000 – $28,450).

Closing entries

Dec. 31 Sales ……………………………………………………… 529,000

Income Summary……………………………… 529,000

To close temporary accounts with

credit balances.

Dec. 31 Income Summary……………………………………. 444,750

Sales Returns and Allowances………….. 17,500

Sales Discounts……………………………….. 5,000

balances.

Dec. 31 Income Summary……………………………………. 84,250

K. Emiko, Capital………..……………………. 84,250

To close Income Summary account.

5-300